Abstract

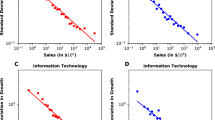

THE large-scale dynamical properties of some physical systems depend on the dynamical evolution of a large number of nonlinearly coupled subsystems. Examples include systems that exhibit self-organized criticality1 and turbulence2,3. Such systems tend to exhibit spatial and temporal scaling behaviour–power–law behaviour of a particular observable. Scaling is found in a wide range of systems, from geophysical4 to biological5. Here we explore the possibility that scaling phenomena occur in economic systemsá-especially when the economic system is one subject to precise rules, as is the case in financial markets6–8. Specifically, we show that the scaling of the probability distribution of a particular economic index–the Standard & Poor's 500–can be described by a non-gaussian process with dynamics that, for the central part of the distribution, correspond to that predicted for a Lévy stable process9–11. Scaling behaviour is observed for time intervals spanning three orders of magnitude, from 1,000 min to 1 min, the latter being close to the minimum time necessary to perform a trading transaction in a financial market. In the tails of the distribution the fall-off deviates from that for a Lévy stable process and is approximately exponential, ensuring that (as one would expect for a price difference distribution) the variance of the distribution is finite. The scaling exponent is remarkably constant over the six-year period (1984-89) of our data. This dynamical behaviour of the economic index should provide a framework within which to develop economic models.

Similar content being viewed by others

References

Bak, B., Tang, C. & Wiesenfeld, K. Phys. Rev. Lett. 59, 381–384 (1987).

Nelkin, M. Adv. Phys. 43, 143–181 (1994).

Meneveau, C. & Sreenivasan, K. R. J. Fluid. Mech. 224, 429–484 (1991).

Olami, Z., Feder, H. J. S. & Christensen, K. Phys. Rev. Lett. 68, 1244–1247 (1992).

Peng, C.-K. et al. Phys. Rev. Lett. 70, 1343–1346 (1993).

Brock, W. A. in The Economy as a Complex Evolving System (ed. Anderson, P. W., Arrow, J. K. & Pines, D.) 77–97 (Addison-Wesley, Redwood City, 1988).

Brock, W. A., Hsieh, D. A. & LeBaron, B. Nonlinear Dynamics, Chaos, and Instability. Statistical Theory and Economic Inference (MIT Press, Cambridge, MA, 1991).

Scheinkman, J. A. & LeBaron, B. J. Business 62, 311–327 (1989).

Shlesinger, M. F., Frisch, U. & Zaslavsky, G. (eds) Lévy Flights and Related Phenomena in Physics (Springer, Berlin, 1995).

Bouchaud, J.-P. & Georges, A. Phys. Rep. 195, 127–293 (1990).

Shlesinger, M. F., Zaslavsky, G. M. & Klafter, J. Nature 363, 31–37 (1993).

Bachelier, L. J. B. Théorie de la Speculation (Gauthier-Villars, Paris, 1900).

Osborne, M. F. M. Oper. Res. 7, 145–173 (1959).

Mandelbrot, B. B. J. Business 36, 394–419 (1963).

Fama, E. F. J. Business 38, 34–105 (1965).

Clark, P. K. Econometrica 41, 135–155 (1973).

Engle, R. F. Econometrica 50, 987–1007 (1982).

Bollerslev, T., Chou, R. Y. & Kroner, K. F. J. Econometrics 52, 5–59 (1992).

Officer, R. R. J. Am. statist. Ass. 67, 807–812 (1972).

Hsu, D.-A., Miller, R. B. & Wichern, D. W. J. Am. statist. Ass. 69, 108–113 (1974).

Lau, A. H.-L., Lau, H.-S. & Wingender, J. R. J. Business Econ. Statist. 8, 217–223 (1990).

Akgiray, V. J. Business 62, 55–80 (1989).

Mantegna, R. N. Physica A179, 232–242 (1991).

Tucker, A. L. J. Business Econ. Statist. 10, 73–81 (1992).

Lévy, P. Théorie de I'Addition des Variables Aléatoires (Gauthier-Villars, Paris, 1937).

Brock, W. A. & Kleidon, A. W. J. Econ. Dyn. Contr. 16, 451–489 (1990).

Mantegna, R. N. & Stanley, H. E. Phys. Rev. Lett. 73, 2946–2949 (1994).

Shlesinger, M. F. Phys. Rev. Lett. 74, 4959 (1995).

Feller, W. An Introduction to Probability Theory and Its Applications (Wiley, New York, 1971).

Akgiray, V. & Booth, G. G. J. Business Econ. Statist. 6, 51–57 (1988).

Author information

Authors and Affiliations

Rights and permissions

About this article

Cite this article

Mantegna, R., Stanley, H. Scaling behaviour in the dynamics of an economic index. Nature 376, 46–49 (1995). https://doi.org/10.1038/376046a0

Received:

Accepted:

Issue Date:

DOI: https://doi.org/10.1038/376046a0

- Springer Nature Limited

This article is cited by

-

Business cycle and herding behavior in stock returns: theory and evidence

Financial Innovation (2024)

-

Analysis of earthquake hypocenter characteristics using chaos game representation

Computational Geosciences (2023)

-

Improvement in Hurst exponent estimation and its application to financial markets

Financial Innovation (2022)

-

Analytical and simulational approaches to the relation between the stock market liquidity and the traders’ utility

Artificial Life and Robotics (2022)

-

Amalgamated Free Lévy Processes as Limits of Sample Covariance Matrices

Journal of Theoretical Probability (2022)