Abstract

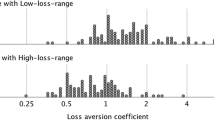

Experimental investigations of the probability weighting function over losses are scarce and all involve small payoffs. The paper aims to give new insight into the probability weighting function for losses, by eliciting it through a simple two-stage semi-parametric procedure over more realistic losses, and by investigating its sensitivity to the magnitude of the payoffs. Current data confirm previous evidence of convex utility functions and inverse-S-shaped weighting functions. Still, at least for small probabilities, probability weighting appears to be affected by the size of consequences: the larger the losses, the more aversive the gambles and the more pessimistic the subjects are.

Similar content being viewed by others

References

Abdellaoui, Mohammed. (2000). “Parameter-Free Elicitation of Utility and Probability Weighting Functions,” Management Science 46(11), 1497-1512.

Abdellaoui, Mohammed. (2002). “A Genuine Rank-Dependent Generalization of the von Neumann-Morgenstern Expected Utility Theorem,” Econometrica 70(2), 717-736.

Abdellaoui, Mohammed, Carolina Barrios, and Peter P. Wakker. (2002). “Reconciling Introspective Utility with Revealed Preference: Experimental Arguments Based on Prospect Theory,” CREED, Department of Economics, University of Amsterdam.

Allais, Maurice. (1988). “The General Theory of Random Choices in Relation to the Invariant Cardinal Utility Function and the Specific Probability Function: The (U, θ) Model, a General Overview.” In Bertrand Munier (ed.), Risk, Decision and Rationality. Dordrecht: D. Reidel Publishing Company.

Bleichrodt, Han and J. Luis Pinto. (2000). “A Parameter-Free Elicitation of the Probability Weighting Function in Medical Decision Analysis,” Management Science 46(11), 1485-1496.

Bostic, Raphael, Richard J. Herrnstein, and R. Duncan Luce. (1990). “The Effect on the Preference Reversal Phenomenon of Using Choice Indifferences,” Journal of Economic Behaviour and Organization 13, 193-212.

Camerer, Colin F. (1992). “Recent Tests of Generalizations of Expected Utility Theory.” In Ward Edwards (ed.), Utility Theories: Measurements and Applications. Boston: Kluwer Academic Publishers.

Camerer, Colin F. and Robin M. Hogarth. (1999). “The Effects of Financial Incentives in Experiments: A Review and Capital-Labor-Production Framework,” Journal of Risk and Uncertainty 19, 7-42.

Carbone, Enrica and John D. Hey. (1994a). “Estimation of Expected Utility and Non-expected Utility Preference Functionals Using Complete Ranking Data.” In Bertrand Munier and Mark J. Machina (eds.), Models and Experiments on Risk and Rationality. Dordrecht: Kluwer.

Carbone, Enrica and John D. Hey. (1994b). “Discriminating Between Preference Functionals: A Preliminary Monte Carlo Study,” Journal of Risk and Uncertainty 8, 223-242.

Carbone, Enrica and John D. Hey. (1995). “A Comparison of the Estimates of Expected Utility and Non-Expected Utility Preferences Functionals,” Geneva Papers on Risk and Insurance Theory 20, 111-133.

Chateauneuf, Alain and Michèle Cohen. (1994). “Risk Seeking with Diminishing Marginal Utility in a Non-Expected Utility Model,” Journal of Risk and Uncertainty 9, 77-91.

Cohen, Michèle. (1995). “Risk Aversion Concepts in Expected-and Non-Expected Utility Models,” The Geneva Papers on Risk and Insurance Theory 42, 370-380.

Currim, Imran S. and Rakesh K. Sarin. (1989). “Prospect versus Utility,” Management Science 35(1), 22-41.

Diecidue, Enrico and Peter P. Wakker. (2001). “On the Intuition of Rank-Dependent Utility,” Journal of Risk and Uncertainty 23(3), 281-298.

Fennema, Hein and Marcel Van Assen. (1999). “Measuring the Utility of Losses by Means of the Tradeoff Method,” Journal of Risk and Uncertainty 17(3), 277-295.

Goldstein, William M. and Hillel J. Einhorn. (1987). “Expression Theory and the Preference Reversal Phenomenon,” Psychological Review 94, 236-254.

Gonzalez, Richard and George Wu. (1999). “On the Shape of the Probability Weighting Function,” Cognitive Psychology 38, 129-166.

Green, Jerry R. and Bruno Jullien. (1988). “Ordinal Independence in Non-Linear Utility Theory,” Journal of Risk and Uncertainty 14, 355-388.

Harless, David W. and Colin F. Camerer. (1994). “The Predictive Utility of Generalized Expected Utility Theories,” Econometrica 62(6), 1251-1289.

Hogarth, Robin M. and Hillel J. Einhorn. (1990). “Venture Theory: A Model of Decision Weights,” Management Science 36(7), 780-803.

Kahneman, Daniel and Amos Tversky. (1979). “Prospect Theory: An Analysis of Decision Under Risk,” Econometrica 47, 263-291.

Köbberling, Veronika and Peter P. Wakker. (2003). “Preference Foundations for Nonexpected Utility: A Generalized and Simplified Technique,” Mathematics of Operations Research 28, 395-423.

Kühberger, Anton, Michael Schulte-Mecklenbeck, and Josef Perner. (1999). “The Effects of Framing, Reflection, Probability, and Payoff on Risk Preference in Choice Tasks,” Organizational Behavior and Human Decision Processes 78(3), 204-231.

Lattimore, Pamela K., Joanna R. Baker, and Ann D. Witte. (1992). “The Influence of Probability on Risky Choice: A Parametric Examination,” Journal of Economic Behavior and Organization 17, 377-400.

Laughhunn, Dan J., John W. Payne, and Roy Crum. (1980). “Managerial Risk Preferences for Below-Target Returns,” Management Science 26, 1238-1249.

Libby, Robert and Peter C. Fishburn. (1977). “Behavioral Models of Risk Taking in Business Decisions: A Survey and Evaluation,” Journal of Accounting Research 15, 272-292.

McCord, Mark R. and Richard de Neufville. (1983). “Empirical Demonstration that Expected Utility Decision Analysis is not Operational.” In Bernt P. Stigum and Fred Wenstop (eds.), Foundations of Utility and Risk. Dordrecht: D. Reidel Publishing Company.

Prelec, Drazen. (1998). “The Probability Weighting Function,” Econometrica 66(3), 497-527.

Quiggin, John. (1982). “A Theory of Anticipated Utility,” Journal of Economic Behavior and Organization 3, 323-343.

Quiggin, John. (1989). “Sure-Things-Dominance and Independence Rules for Choice Under Uncertainty,” Annals of Operations Research 19, 335-357.

Quiggin, John. (1993) Generalized Expected Utility Theory: The Rank-Dependent Model, Boston/Dordrecht/London: Kluwer Academic Publishers.

Saha, Atanu. (1993). “Expo-Power Utility: A Flexible Form for Absolute and Relative Risk Aversion,” American Journal of Agricultural Economics 75, 905-913.

Sarin, Rakesh K. and Peter P. Wakker. (1998). “Revealed Likelihood and Knightian Uncertainty,” Journal of Risk and Uncertainty 16, 223-250.

Schoemaker, Paul J.H. and John C. Hershey. (1992). “Utility Measurement: Signal, Noise and Bias,” Organizational Behavior and Human Decision Processes 52, 397-424.

Segal, Uzi. (1989). “Anticipated Utility: A Measure Representation Approach,” Annals of Operations Research 19, 359-373.

Segal, Uzi. (1993). “The Measure Representation: A Correction,” Journal of Risk and Uncertainty 6, 99-107.

Starmer, Chris. (2000). “Developments in Non-Expected Utility Theory: The Hunt for a Descriptive Theory of Choice Under Risk,” Journal of Economic Literature 38, 332-382.

Thaler, Richard H. and Eric J. Johnson. (1990). “Gambling with the House Money and Trying to Break Even: The Effects of Prior Outcomes on Risky Choices,” Management Science 36(6), 643-660.

Tversky, Amos and Craig R. Fox. (1995). “Weighing Risk and Uncertainty,” Psychological Review 102, 269-283.

Tversky, Amos and Daniel Kahneman. (1992). “Advances in Prospect Theory: Cumulative Representation of Uncertainty,” Journal of Risk and Uncertainty 5, 297-323.

Tversky, Amos and Peter P. Wakker. (1995). “Risk Attitudes and Decision Weights,” Econometrica 63, 1255-1280.

Von Winterfeld, Detlof and Ward Edwards. (1986) Decision Analysis and Behavioral Research. Cambridge: Cambridge University Press.

Wakker, Peter P. (1994). “Separating Marginal Utility and Probabilistic Risk Aversion,” Theory and Decision 36, 1-44.

Wakker, Peter P. and Daniel Deneffe. (1996). “Eliciting von Neumann-Morgenstern Utilities when Probabilities are Distorted or Unknown,” Management Science 42(8), 1131-1150.

Wakker, Peter P., Ido Erev, and Elke U. Weber. (1994). “Comonotonic Independence: The Critical Test Between Classical and Rank-dependent Utility Theories,” Journal of Risk and Uncertainty 9, 195-230.

Wu, George and Richard Gonzalez. (1996). “Curvature of the Probability Weighting Function,” Management Science 42, 1676-1690.

Yaari, Menahem E. (1987). “The Dual Theory of Choice Under Risk,” Econometrica 55(1), 95-115.

Author information

Authors and Affiliations

Rights and permissions

About this article

Cite this article

Etchart-Vincent, N. Is Probability Weighting Sensitive to the Magnitude of Consequences? An Experimental Investigation on Losses. Journal of Risk and Uncertainty 28, 217–235 (2004). https://doi.org/10.1023/B:RISK.0000026096.48985.a3

Issue Date:

DOI: https://doi.org/10.1023/B:RISK.0000026096.48985.a3