Abstract

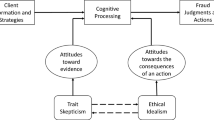

This study adapts the theory of reasoned action (Ajzen and Fishbein, 1980) to the behavior of fraudulent reporting on financial statements so as to examine the effects of moral reasoning and self-monitoring on intention to report fraudulently, using structural equation modeling. The paper seeks to investigate two of the red flags for financial statement fraud identified in Loebbecke et al.'s (1989) paper: client management displays a significant lack of moral fiber and client personnel exhibit strong personality anomalies. As expected, high moral reasoners are more influenced than low moral reasoners by their own attitude towards the behavior. Contrary to prior research, low self-monitors are found to be more influenced than high self-monitors by subjective norms. Future research is recommended to investigate the counter-intuitive results for self-monitors, to consider the implications of group decision making as regards the promulgation of fraudulent financial statements, and to examine additional red flags for financial statement fraud.

Similar content being viewed by others

References

Ajzen, I. and M. Fishbein: 1980, Understanding Attitudes and Predicting Social Behavior (Prentice-Hall, NJ).

American Institute of Certified Public Accountants: 1997, Statement of Auditing Standards No.82: Consideration of Fraud in a Financial Statement Audit (AICPA, New York, NY).

Atkinson, J. W. and P. O'Connor: 1963, Effects of Ability Groupings in Schools Related to Individual Differences in Characteristics in Achievement-related Motivation.Cooperative Research Project No.1283 (University of Michigan, Ann Arbor).

Bentler, P. M.: 1998: EQS for Windows 5.7b (Multivariate Software, Inc., Encino, CA).

Brief, A. P., J. M. Dukerich, P. R. Brown and J. F. Brett: 1996, ‘What's Wrong with the Treadway Commission Report? Experimental Analyses of the Effects of Personal Values and Codes of Conduct on Fraudulent Financial Reporting', Journal of Business Ethics 15, 183–198.

Bollen. K. A.: 1989, Structural Equations and Latent Variables (Wiley Interscience, New York).

Burnkrant, R. E. and T. J. Page Jr.: 1988, ‘The Structure and Antecedents of the Normative and Attitudinal Components of Fishbein's Theory of Reasoned Action', Journal of Experimental Social Psychology 24, 66–87.

Byrne, B. M.: 1994. Structural Equation Modeling with EQS and EQS/Windows (Sage Publications).

Covey, M. K., S. Saladin and P. J. Killen: 1988, ‘Self-Monitoring, Surveillance, and Incentive Effects on Cheating', The Journal of Social Psychology 129(5), 673–679.

Crowne, D. P. and D. Marlowe: 1964, The Approval Motive (Wiley, New York).

Fischer, D. G. and C. Fick: 1993, ‘Measuring Social Desirability: Short Forms of the Marlowe-Crowne Social Desirability Scale', Educational and Psychological Measures, 427–424.

Gillett, P. R. and N. Uddin: 2002, 'CFO Intentions to Report Fraudulently on Financial Statements', Working Paper.

Hu, L. and P. M. Bentler: 1999, ‘Cutoff Criteria for Fit Indexes in Covariance Structure Analysis: Conventional Criteria Versus New Alternatives', Structural Equation Modeling 6(1), 1–55.

Kohlberg, L.: 1964, ‘Development of Moral Character and Moral Ideology', in H. Hoffman and L. Hoffman (eds.), Review of Child Development Research, Vol. 1 (Russell Sage Foundation, New York).

Kohlberg, L.: 1984, Essays on Moral Development.Volume II The Psychology of Moral Development (Harper and Row, Publishers Inc., New York).

Loebbecke, J. K., M. M. Eining and J. J. Willingham: 1989, ‘Auditors' Experience with Material Irregularities: Frequency, Nature, and Detectability', Auditing, A Journal of Practice and Theory 9(1), 1–28.

Malinowski, C. I. and C. P. Smith: 1985, ‘Moral Reasoning and Moral Conduct: An Investigation Prompted by Kohlberg's Theory', Journal of Personality and Social Psychology 49, 1016–1027.

Palmrose, Z. V.: 1987, ‘Litigation and Independent Auditors: The Role of Business Failures and Management Fraud', Auditing: A Journal of Practice and Theory 6(2), 90–103.

Rest, J. R.: 1979, Development in Judging Moral Issues (University of Minnesota Press, Minneapolis).

Schwartz, S. H., K. A. Feldman, M. E. Brown and A. Heingartner: 1969, ‘Some Personality Correlates of Conduct in Two Situations of Moral Conflict', Journal of Personality 37(1), 41–57.

Snyder, M.: 1974. ‘The Self-Monitoring of Expressive Behavior in High School and College', Journal of Personality and Social Psychology 30, 526–537.

Author information

Authors and Affiliations

Rights and permissions

About this article

Cite this article

Uddin, N., Gillett, P.R. The Effects of Moral Reasoning and Self-Monitoring on CFO Intentions to Report Fraudulently on Financial Statements. Journal of Business Ethics 40, 15–32 (2002). https://doi.org/10.1023/A:1019931524716

Issue Date:

DOI: https://doi.org/10.1023/A:1019931524716