Abstract

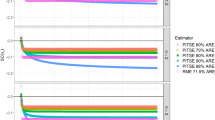

One approach used for analyzing extremes is to fit the excesses over a high threshold by a generalized Pareto distribution. For the estimation of the shape and scale parameters in the generalized Pareto distribution, under some restrictions on the value of the scale parameter, maximum likelihood, method of moments and probability weighted moments' estimators are available. However, these are not robust estimators. In this paper we implement a robust estimation procedure known as the method of medians (He and Fung, 1999) to estimate the parameters in the generalized Pareto distribution. The asymptotic distribution of our estimator is normal for any value of the shape parameter except −1.

Similar content being viewed by others

References

Dupuis, D.J., “Estimating the probability of obtaining nonfeasible parameter estimates of the generalized Pareto distribution,” Journal of Statistical Computation and Simulation 54, 197–209, (1996).

Dupuis, D.J., “Exceedances over high thresholds: a guide to threshold selection,” Extremes 1(3), 251–261, (1998).

Dupuis, D.J. and Field, C.A., “Robust estimation of extremes,” The Canadian Journal of Statistics 26(2), 199–215, (1998).

Dupuis, D.J. and Tsao, M., “A hybrid estimator for generalized Pareto and extreme-value distributions,” The Communications in Statistics, Theory and Methods 27(4), 925–941, (1998).

Embrechts, P., Klüppelberg, C., and Mikosch, T., Modelling Extremal Events for Insurance and Finance, Springer: Berlin, 1997.

Hampel, F.R., Ronchetti, E.M., Roussccuw, P.J., and Stahel, W.A., Robust Statistics: The Approach Based on Influence Functions, Wiley: New York, 1986.

He, X. and Fung, W.K., “Method of medians for life time data with Weibull models,” Statistics in Medicine 18, 1993–2009, (1999).

Hosking, J.R.M. and Wallis, J.R., “Parameter and Quantile estimation for the Generalized Pareto distribution,” Technometrics 29(3), 339–349, (1987).

Huber, P.J., Robust Statistics, Wiley: New York, 1981.

Smith, R.L., “Threshold methods for sample extremes.” In: Statistical Extremes and Applications, (J. Tiago de Oliveira, ed.), D. Reidel: Dordrecht, 621–638, (1984).

Smith, R.L., “Maximum likelihood estimation in a class of nonregular cases,” Biometrika 72(10), 67–90, (1985).

Author information

Authors and Affiliations

Rights and permissions

About this article

Cite this article

Peng, L., Welsh, A. Robust Estimation of the Generalized Pareto Distribution. Extremes 4, 53–65 (2001). https://doi.org/10.1023/A:1012233423407

Issue Date:

DOI: https://doi.org/10.1023/A:1012233423407