Abstract

The COVID-19 pandemic is damaging economies across the world, including financial markets and institutions in all possible dimensions. For banks in particular, the pandemic generates multifaceted crises, mostly through increases in default rates. This is likely to be worse in developing economies with poor financial market architecture. This paper utilizes Bangladesh as a case study of an emerging economy and examines the possible impacts of the pandemic on the country’s banking sector. Bangladesh’s banking sector already has a high level of non-performing loans (NPLs) and the pandemic is likely to worsen the situation. Using a state-designed stress testing model, the paper estimates the impacts of the COVID-19 pandemic on three particular dimensions—firm value, capital adequacy, and interest income—under different NPL shock scenarios. Findings suggest that all banks are likely to see a fall in risk-weighted asset values, capital adequacy ratios, and interest income at the individual bank and sectoral levels. However, estimates show that larger banks are relatively more vulnerable. The decline in all three dimensions will increase disproportionately if NPL shocks become larger. Findings further show that a 10% NPL shock could force capital adequacy of all banks to go below the minimum BASEL-III requirement, while a shock of 13% or more could turn it to zero or negative at the sectoral level. Findings call for immediate and innovative policy measures to prevent a large-scale and contagious banking crisis in Bangladesh. The paper offers lessons for other developing and emerging economies similar to Bangladesh.

Similar content being viewed by others

Introduction

The COVID-19 pandemic is causing havoc across the global economic and financial sphere, as it emerges as the biggest test for financial systems since the 2008–09 global financial crisis (GFC). The Asian Development Bank predicts that the global economic cost of the pandemic is likely to be between $5.8 and $8.8 trillion (about 6.4–9.7% of world GDP) (Park et al. 2020). More than anything else, the unprecedented macroeconomic and health systems shocks are likely to have spillover effects on financial systems of every nation in a wide range of channels. As the pandemic pushes aggregate demand, production, trade and economic activities to slow down and unemployment to rise, financial institutions (FIs) in almost every country fear an increasing risk of fallout without government support (IMF 2020).

An increasing number of studies suggest that the COVID-19 pandemic has already begun to ravage economies by causing problems with all sorts of macroeconomic indicators including aggregate demand, production, supply, trade flows, savings, investments, and employment, which could deepen poverty and trigger a possible recession or depression (Chen et al. 2020; Coibion et al. 2020; ILO 2020; Barua 2020a, b, c; World Bank 2020a; OECD 2020a; Baldwin and de Mauro 2020). In a pandemic-ridden or a post-pandemic world, such damage could threaten the survival and sustainability of FIs, financial stability and security, and regulatory discipline across countries—be they developed or developing (Stiller and Zink 2020; FSB 2020; BIS 2020; Baret et al. 2020; Cecchetti and Schoenholtz 2020; Mann 2020; Beck 2020; World Bank 2020c; World Economic Forum 2020). Above all, the severest blow will be faced by banks. This is because banks normally face a broader range of risks relative to other FIs (e.g., interest rate, liquidity, credit, market, and reputational risks) and are more closely interconnected with everyday activities of economic agents, namely individuals, firms, and the government (Stulz and Carey 2006).

Banks traditionally deal with a wide range of risks and the pandemic is going to increase their severity through liquidity crunch, credit squeeze, increases in non-performing assets and default rates, reducing returns from loans and investments, declining market interest rates, and triggering contagious bank-run (Larbi-Odam et al. 2020; Cecchetti and Schoenholtz 2020; Goodell 2020; World Bank 2020c, d; Stiller and Zink 2020). As such, banks are likely to see increases in a number of risks, such as credit risk, liquidity risk, market risk, and interest rate risk. This is likely to be worse in developing countries where banks serve millions of individuals and firms with relatively less financial and economic capacity under a weaker policy environment and aggressive market competition (Wilson 2020; Tyson 2020). The COVID-19 pandemic, particularly in developing countries, could result in a complex set of simultaneous outcomes; for example, a mass-default of loans, recoveries becoming complex and harder, savings exhausted by customers to support daily living, decreased availability of loanable funds, and depressed new investment demand (Lagoarde-Segot and Leoni 2013). In most developing and many emerging economies, banks are the engine of economic growth as they are the dominant source for both long-term and short-term capital financing. The role and power of banks is immense particularly in countries where the financial system is underdeveloped due to weak or non-existent securities markets, the lack of effective and adequate legal infrastructure, the lack of innovative and necessary financial instruments, and technology and innovation playing a limited role (Barua 2019; Barua et al. 2017; Allen et al. 2014; Barua and Barua 20192019). As in many emerging economies, banks predominantly fuel the rapid economic growth, and damage to the fund mobilization process may cause significant downside economic effects in these countries.

All things considered, the pandemic could substantially threaten the performance, survival, and growth of banks in developing countries, particularly in those where banks play a dominant role in the economy (Damak et al. 2020). Understanding the effects on banks in emerging economies could render valuable information about the implications of the pandemic for developing countries. However, this requires a careful case by case examination.

A growing volume of literature highlights the potential COVID-19 implication for banks; however, much of it remains mostly applicable to developed countries (World Economic Forum 2020; FSB 2020; BIS 2020; Cecchetti and Schoenholtz 2020; Stiller and Zink 2020; Strietzel et al. 2020). Given this gap, this paper considers Bangladesh as a case study of developing and emerging economies and assesses the possible impacts of the COVID-19 pandemic on its banking sector. There are several factors that make Bangladesh an ideal case for examination. First, the country is expected to grow at a rate higher than countries like China and India and is considered to have the potential to drive the world economy in the next few decades (ADB 2020a). Second, the banking sector in Bangladesh remains the major source of long-term funds and investments necessary to fuel the country’s faster growth (Mujeri and Rahman 2009). Third, Bangladesh’s financial sector remains significantly underdeveloped as it has a limited-scale and unstable securities markets (e.g., only weakly efficient equity market, no bond or derivative market), poorly effective and adequate regulatory infrastructure, a poor degree of innovation, and technology still only plays a minor role (Nguyen et al. 2011). Finally, the country’s banking sector is already overburdened with a high default rate and non-performing loan/asset (NPL) ratio, which puts Bangladesh in the list of top countries with high NPL ratios in Asia and the Pacific (Dey 2019). All things considered, examining the case of Bangladesh could render valuable lessons for other emerging and/or developing economies, particularly for those with similar economic and financial architecture.

The paper begins with presenting a theoretical framework of the possible implications for banks in general, which is equally applicable to Bangladesh’s banking sector. Then, using a stress testing model designed and prescribed by Bangladesh Bank—the central bank of Bangladesh—the paper estimates the pandemic’s effects under different NPL scenarios on three critical dimensions of banks: firm value, capital adequacy, and operating performance. For a better understanding of the likely impacts, assessments are carried out at the individual bank and sectoral levels and across five bank size categories. Given the limited literature on the banking sectoral-level implications in developing countries, the paper contributes by not only offering novel assessments to the growing literature on COVID-19’s implications for banks, but also developing the first scenario-based estimates with respect to Bangladesh’s banking sector. As such, it offers valuable contributions to the understanding of implications for banks, particularly in emerging economies. The rest of the paper is structured in five sections; section two outlines the theoretical mapping of COVID-19 implications, section three presents the methodology; section four presents the results and discussions; followed by a conclusion in the final section.

Mapping the COVID-19 implications for banks

Since the COVID-19 pandemic is a novel experience for the world, the literature regarding its implications for banks is still developing. Yet, lessons from globally spilled-over systemic financial crises such as the global financial crisis (GFC) of 2008 could have some relevance, particularly because the effects are likely to be similar. Systemic events external to the banking system such as economic recessions, pandemics, war, political unrest, and environmental disasters could have massive adverse effects on the firm value and performance of banks, forcing many to fail or go bankrupt in extreme cases. The 2008–09 GFC is such a phenomenon, during which many cited ‘epidemiology’ as a reference point to explain the spillover of volatility and financial and economic distress situations through an intra-financial system, considering that the crisis outcomes are contagious like a pandemic (Caballero and Simsek 2009; Roubini 2008). The comparison argues that the outbreak and spillover effects of systemic economic and financial crises spread fast through both the intra-financial and inter-financial systems approach. Because of this nature, global or large-scale systemic crises could be termed as contagious just like the COVID-19 pandemic (Cecchetti and Schoenholtz 2020; Bachman 2020). As such, financial bubbles behave like disease pandemics and they should be treated the same way (Shiller 2020; Haldane and May 2011).

Disease pandemics such as COVID-19 produce a complex and diverse set of consequences for banks and threaten banking system stability (FSB 2020; Aldasoro et al. 2020). Figure 1 shows the mapping of possible implications of the COVID-19 pandemic for banks in a ‘no policy intervention’ scenario. The prevalence of the pandemic for a prolonged period with a subsequent complete lockdown may push banks to an inevitable crisis. Across economies, as an immediate shock of the lockdown and social distancing measures in response to the pandemic, production has halted, demand for goods and services—mainly for non-essentials—has slumped, factories and offices are completely or partly shut-down, transports and logistics are restricted, and public movement as a whole is highly restricted domestically and internationally (Barua 2020a, b).

Source: authors developed

Mapping the impacts of the COVID-19 pandemic for banks.

Many of the immediate shocks turn out to be long-lasting over time, as countries continue enforcing lockdowns and strict social distancing over a longer period to curb the virus’s spread. For instance, it has been over eight months to date that such measures have been widely and strictly enforced across almost all economies of the world. The worldwide lockdowns and economic shocks in turn cause a severe disruption in the international trade of goods and services, due to reduced import demand internationally, limited movement of international transport and logistics carriers, and stricter entry requirements of goods and people imposed by many countries (Barua 2020b; WTO 2020; OECD 2020b; Rigden 2020). These have already started to generate severe macroeconomic costs for many nations through a sustained fall in aggregate demand and supply, slump in price levels, massive layoffs and job cuts, unfavorable exchange rate movement, and increases in risk and uncertainty for current or potential private-sector investments (World Bank 2020b).

Because of the diverse macroeconomic shocks, bank borrowers—individuals and firms—face high risk of default (Vidovic and Tamminaina 2020). The banking sector may see a steep rise in default risk and rates because of reduced incomes and cash inflows to their borrowers due to the economic slow-down and forced shutdown. The crisis will be worse for borrowers relying on exports to the international market, as the world economy struggles to survive from the pandemic. These effects will also be severe for small businesses whose only lifeline is doing day-to-day business and generating enough operating cash inflows to survive (Dua et al. 2020). Also, small businesses have little capital support and cushion to protect them from economic adversities. During and after the pandemic, banks that have a substantial lending exposure, particularly to export-oriented industries and small businesses, may see a steep rise in default rates. Further, the overall situation may turn many borrowers into willful defaulters and may increase the credit risk of the banks. It is possible that the market value of collaterals provided against secured loans may decline in value, further enhancing the credit and default risk for banks (Baret et al. 2020).

In addition to default risk, banks may also face liquidity crises as many depositors may choose to withdraw their savings to support their living and health expenses (Baret et al. 2020). Due to the pandemic, income opportunities for people and firms have become increasingly limited, which might force them to spend their savings. In particular, people losing jobs will desperately try to survive on their savings. This, if continued for too long, will cause liquidity shortage and limit the lending capacity of banks (Cheney et al. 2020).

Due to economic slow-down domestically and globally, demand for loans will slump, as is already happening in many economies. As firms limit their operation and production, demand for both short- and long-term financing declines substantially with no possibility of rebound until the economy as a whole recovers (Ryan et al. 2020). It will hurt banks’ basic business model and revenue generation and could create a large revenue shock in countries where lending dominates the business portfolio of banks, as is the case for many developing and emerging economies. The problem could be further intensified by the limits in lending capacity faced by banks due to liquidity shortage because of increased withdrawals (Cheney et al. 2020). Furthermore, incomes from both interest and non-interest sources are likely to fall due to a reduced international trade, foreign exchange dealing, and transaction services. Interest incomes could further fall as banks in many countries have already commenced waiving fees and charges, increasing credit card limits, granting mortgage payment holidays and access to fixed saving accounts in an effort to help their clients survive the pandemic (Ryan et al. 2020; Yousufani et al. 2020).

Much of the cumulative outcome of the affects discussed so far will be increases in NPLs and a reduction in asset quality for banks. A persistent scenario like this would necessarily lower the asset value or firm value of banks. A lower risk-weighted value of assets will in turn lower capital adequacy of banks, threatening the banks’ financial solvency, survival, and sustainability. The capital adequacy of banks could also decline as many banks could try to utilize part of their Tier 1 or 2 capitals to support their operating and financial sustainability.

After the 2008–09 global financial crisis, regulators across the world emphasized the idea that banks should hold substantial buffers to survive through dramatic downturns. To make it effective, the Basel Committee issued an enhanced capital adequacy (BASEL-III) accord to improve the banking sector’s ability to absorb shocks arising from financial and economic stress (BIS 2017). However, lessons from the large-scale financial crises remain mostly unheard, particularly in developing and emerging economies where banks aggressively compete. In addition, in many developing and/or emerging economies, financial markets are weakly efficient, suffer from insufficient regulatory infrastructure, lack innovation and adoption of cutting-edge technology, and are crippled with moral hazards and adverse selection problems driven by political interventions (Görg et al. 2020; Dominguez et al. 2009). The COVID-19 pandemic is likely to make things significantly worse in these countries. As a case of such emerging economies, this paper examines the possible impacts of the pandemic on Bangladesh’s banking sector.

Methodology

This section provides details about method specification, shock design, and data to be used in the paper.

Method specification

To develop a theoretical foundation and scenario-based assessments of COVID-19 implications for the Bangladesh banking sector, this paper follows a quantitative approach. To develop scenario-based estimates of the likely impacts on banks, the paper uses a stress testing model designed and prescribed for the banking sector by Bangladesh Bank. All banks are required to follow the model in their regular business practices. The model is described in detail in the stress testing guidelines in Bangladesh Bank (2010), published by the Department of Offsite Supervision of the central bank. The paper uses the model to estimate like impacts on three dimensions—capital adequacy, operating performance, and firm value. In this paper, capital adequacy is measured by the level of the capital adequacy ratio (CAR), operating performance is measured by the level of interest incomes (INT), and firm value is approximated by the value of total risk-weighted assets (RWA).

For credit risk stress testing, Bangladesh Bank (2010) provides multiple models in response to six different types of credit shocks—namely, increases in overall NPLs; increases in NPLs in only textiles and ready-made garment industries; increases in NPLs of top ten large borrowers of a bank; shifts in NPL categories; fall in fire sale value of collaterals; and extreme events. Due to COVID-19, the biggest and most imminent shock for the banking sector is credit shock, particularly through increased default rates and NPLs across all sectors and industries. The COVID-19 driven credit shock could be a lifetime test for the survival of many banks, since the Bangladesh banking sector is already crippled with high NPL rates and loan pricing recently has been capped down to less than two digits by the central bank of the country. As a result, while there might be other sources of shocks arising for banks, credit risk shock through increased NPLs is likely to be the biggest one. All things considered, the paper uses the model prescribed for increases in overall NPLs. Following is the detail formulation of how the Bangladesh Bank (2010) model can be used for testing the effects on the value of RWA, CAR, and INT.

If a bank \(i\) has \({L}_{t}\) as the total amount of loans and advances and \({N}_{t}\) as the total amount of NPLs in the pre-pandemic time \(t\), the value of total performing loans \({P}_{t}\) stands:

If rates of NPLs increase by a magnitude of \(\delta\) over a period \(t+n\) during and post COVID pandemic, the value of new NPL (\({K}_{n}\)) becomes:

where \(n\) is the period of the active pandemic and time taken in the future to return to a normal or pre-pandemic state; and \(\delta =1, 2, 3,\dots , r percentage point\) is the magnitude of NPL shocks due to the COVID-19 pandemic over the period \(n\). When a bank has a pre-pandemic state capital \({C}_{t}\) and RWA value \({A}_{i,t}\), the revised \(C\) and \(R\) due to the increased NPLs \({K}_{n}\) becomes,

According to Bangladesh Bank (2010), two other factors need to be subtracted from the initial \({C}_{t}\) and \({A}_{t}\)—provisions for NPLs (after adjustment of eligible securities; if any) and Tax adjustment provisions (not yet applicable). However, these items are optional depending on whether these requirements are applicable for a bank; this means not all banks would have the two items for adjustment in the stress testing process. Furthermore, data and information about these items are mostly private and not made publicly available by banks. In this research, the items are excluded from adjustment due to the unavailability of necessary data.

Using a bank’s pre-pandemic state \({C}_{i,t}\) and \({A}_{i,t}\), the pre-pandemic state CAR can be calculated by dividing the value of capital by the value of risk-weighted assets of a bank as follows:

Using Eq. (5), the new CAR after adjusting the increases in NPLs (\({K}_{n}\)) is as follows:

Thus, the effects or changes in CAR for a bank due to the increases in NPLs (\({K}_{n}\)) through the NPL shock magnitude \(\delta\) becomes:

If there are m banks in the sector, the sector-wide effect involving all \(m\) number of banks using (7) could be calculated by,

where \(s\) indicates simple average, \(w\) indicates weighted average and weights (\(w\)) obtained by dividing CAR of each bank by the total CAR of all banks.

Since the increases in NPLs (\({K}_{n}\)) through the NPL shock magnitude \(\delta\) reduces the value of risk-weighted assets (\({A}_{t}\)), the effects or changes in the value of RWA for a bank can be derived as follows:

In percent terms,

Following previous formulations, the sector-wide effect involving all \(m\) number of banks could be calculated using (11) by,

where \(s\) indicates simple average, \(w\) indicates weighted average and weights (\(w\)) obtained by dividing RWA of each bank by the total RWA of all banks.

Increases in NPLs would mean a loss in interest incomes from the proportion of loaned amounts that are defaulted. This means the loss in interest incomes would depend on the amount of loan (or the percent of total loan) that is defaulted and the interest rates that were due to be received from that loan. In this case, if an increase in NPL for a particular loan happens by \(\delta\) due to the COVID-19 effects and interest rates were to be charged at \(R\) for that loan, then the loss in interest income from that loan in percentage terms for a bank would be:

where \(\gamma\) and \(R\) signify interest income loss (in %) and interest rates (in %) for a specific loan (\(l\)) of a bank (\(i\)). While Eq. (10) can be applied to one loan particularly, it can also be applied at the aggregate level for all applicable loans of a bank, which this research aims at. This will require aggregating a bank’s total loan defaulted and using a measure of overall \({R}_{i}\) and \({\delta }_{i}\) across all loans of the bank. As a way-out, using an average interest rates \(\stackrel{-}{R}\) and total default rates \(\delta\) of a bank \(i\) across all loans, Eq. (10) can be rewritten:

Following the previous formulation, the average sector-wide effect involving all \(m\) number of banks in the sector could be calculated using (15) by,

where \(s\) indicates simple average;

In this paper, the effects of total NPL shocks \(\delta\) on CAR, RWA values, and interest income for each bank are estimated using Eqs. (7), (9), and (15), respectively, and then for sector-wide effects using Eqs. (8), (9), (12), (13), and (16). The sector-wide examinations are extended by clustering banks into four different sizes: smaller, medium smaller, medium larger, and larger. The design of the total NPL shocks \(\delta\) and the detail of the bank data and their size classifications are explained the following sections.

Designing the NPL shocks to banking sector

The impact scenarios to be estimated using the stress testing model require predicting a range of possible changes in NPLs, i.e., magnitudes of increases in NPLs, which reflect the credit shock arising due to the COVID-19 impacts. As of now, no scholarly work provides any particular estimate of the likely increases in NPLs in Bangladesh due to COVID-19, which makes the task of this paper difficult. However, there is no denying that NPLs are likely to aggressively increase in Bangladesh due to COVID-19. Among all affected sectors, two sectors could produce major NPL shocks for Bangladesh’s banking sector—ready-made garment (RMG) and textiles and small and medium enterprises (SMEs) (ADB 2020b; Paul 2020; Lalon 2020). The paper considers the two sectors as the main sources of possible NPL shocks; the fall of RMG and textile industry borrowers could be devastating since these industries constitute 80% of the country’s exports revenues, and the fall of SMEs is critical as they are considered the new engine of growth and employment for the country’s economy. Textile, RMG, and SMEs’ combined share more than two-thirds of loans disbursed by the banking sector in Bangladesh, according to the Bangladesh Bank (2017).

The latest available data published in the Field Survey Report of Bangladesh Bank (2017) show that the share of outstanding loans (USD 7851.7 millionFootnote 1) in RMG and textiles industries stands at about 13.37% as of 2016 (about USD 1050 million). On the other hand, total outstanding SME loans stand at 19.74% as of September 2019 (3087.1 million total) (Bangladesh Bank 2020). Reliable data for 2019 RMG and Textiles industries are not available. Based on a conservative assumption that the share of both sectors remain the same to date, the SME and the RMG and textiles industries together makes a total share of about 33.11% of total loans outstanding. This means that in the worst-case scenario of the fallout from the COVID-19 pandemic, about 33.11% of total loans disbursed by banks may fall into risk and be defaulted; and banks may never be able to recover any part of the loans. It is worth-noting that the Bangladesh Garment Manufacturer and Exporters Association reports that orders worth about USD 3.15 billion in 1134 factories have already been cancelled or delayed as of April 2020 due to the pandemic (UNB 2020). This value is three times larger than the total outstanding loan in the RMG and textiles, which means the pandemic could threaten the entirety or a substantial portion of the loan outstanding in the sectors. For example, if 10% of the order values represents bank credit, then a loss of 10% (about USD 0.315 billion or 31.5 million) would constitute a 30% NPL shock (USD 31.5 out of 1050 million). The latest impact data about the SME sector, however, are not available from any reliable sources.

However, the actual default or NPL increases could be anywhere below or equal to 33.11% and a reliable prediction is as yet unavailable. Given this, this paper considers 35 scenarios beginning from 1 to 35% at a 1% interval and estimates their likely impacts on RWA values, CAR, and INT. The estimates are then analyzed at the bank and all-banks or sectoral level and across bank size categories for a deeper insight.

Data

The paper considers 30 commercial banks (out of a total of 60 banks in the sector) of Bangladesh that are publicly listed in the Dhaka Stock Exchange Limited. Appendix Table S1 shows the list of the 30 banks. Appendix Table S3 shows the descriptive summary of the data. Considering the market share of loans in the SME and RMG and textiles sectors, 35 scenarios for NPL shocks are considered from 1 to 35%, i.e., \(\delta\) takes a value from 1 to 35%. To explore the effects on RWA, CAR, and INT, data are obtained for pre-pandemic level 2018 values of total capital, risk-weighted assets, total loans, and total NPLs (Appendix Table S7).

To explore the aggregate level effects on INT using Eqs. (15) and (16), annual lending interest rates for each bank are obtained from Bangladesh Bank (2020) that were applicable in 2018 across five different lending products/sectors: (i) term loans to large and medium scale industries, (ii) term loans to small industries, (iii) working capital loans to large and medium industries, (iv) working capital loans to small industries, and (v) trade financing. Bangladesh Bank (2020) reveals bank-wise interest rates involving upper and lower limits for each of the products/sectors separately. For each of the 30 banks included in this research, the highest, the lowest, and the average of all interest rates across all five products/sectors as of 2018 are considered for analysis. This allows this research to produce aggregate level interest income effects for each bank separately for three difference scenarios assuming upper, lower, and average interest rates, i.e., \(R\) in Eq. (15) takes three different values—the upper, lower, and average levels of interest rates—and interacts with 35 different NPL shock possibilities (\(\delta\)) to produce a large number of possible scenarios of interest income effects. A complete list of interest rate data for each bank is provided in Appendix Table S2.

For an extended analysis, the 30 banks are classified in this paper in 4 size categories based on the values of RWA in million US Dollar: smaller (< 2000), medium-smaller (2000– < 3000), medium-larger (3000– < 4000), and larger (> = 4000). The size categories are defined based on relative RWA values across all banks. Appendix Table S1 lists the size category for each bank.

Pre-pandemic data summary

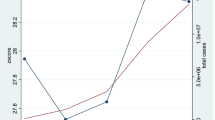

Table 1 shows the pre-pandemic status of different parameters key to this study, and Figs. 2, 3 show the bank-wise NPL and CAR. It is noticeable that the NPL ratio among the 30 banks averages at 9% with the upper bound as high as 82%. Capital adequacy stands as high as 17.0%; however, the lower bound stands at − 125.1%. The large and negative CAR and the largest NPL values can be specifically attributed to ICB Islamic Bank Limited (Figs. 2, 3)—which went bankrupt in 2006 as Oriental Bank Limited due to extremely poor asset quality and had to undergo multiple ownership changes and massive transformations under a government bailout package.

Source: Author’s calculations

Pre-pandemic levels of 2018 total loan outstanding and NPL ratio by bank.

Source: Author’s calculations

Pre-pandemic levels of 2018 risk-weighted asset and capital adequacy by bank.

Results and discussion

This section discusses the estimated effects of COVID-19 NPL shocks on firm value (RWA value), capital adequacy (CAR), and interest incomes (INT) of banks.

Effects on firm value (RWA values)

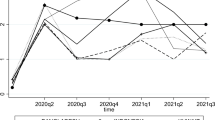

Figure 4 shows the estimated bank-wise effects of COVID-19 NPL shocks on RWA values using Eq. (9). Figure 4a is presented mainly to display the general trend across all banks rather than focusing on an individual bank. The figure shows that the greater the NPL shock is, the larger the reduction in RWA values in percentage terms for each bank. However, the degree of RWA value decline varies across banks. The rate of increase in RWA value reductions is larger than the rate of increase in NPL shocks. This is reflected in Fig. 4a as banks could face RWA value reductions of close to 50% due to a 33% increase in NPLs, denoted by the vertical line. The 33% is considered as the highest possible NPL shock in this paper, as explained in the methodology section. At the highest 33% NPL shock, there are also banks that could see a decline as low as approximately 5% in RWA values. Figure 4b shows the key summary statistics by bank. Among all banks, the largest decline in RWA values is likely for banks with Islamic service models, particularly FSIBL, IBBL, and SIBL. A wide range (upper and lower value) of these banks shown in Fig. 4b suggest that at any level of NPL shock, these banks are likely to bear the largest effect.

Source: Author’s estimate

Bank-wise shock to RWA values due to NPL increases.

Table 2 shows the average decline in RWA values at the sectoral level (average across all banks) using Eqs. (12) and (13) using two methods: (1) simple average (SAVE) and (2) weighted average (WAVE) using individual weight for each bank based on their existing RWA. Both methods suggest similar estimates of average decline in RWA at different NPL shocks. The largest shock of 33% is likely to bring about a 29.7–30.8% decline at the sectoral level.

Figure 5 presents the average estimated decline in RWA values categorized by size of banks, calculated by two methods: one, simple arithmetic mean across banks in a certain category, and the other, by weighted average using individual weight for each bank within a certain category. Both Fig. 5a, b clearly show that at any level of NPL shock, the largest effects will be experienced by large banks, followed by medium-small banks. Based on both averaging methods, RWA values could decline for larger banks by 35.7–38.0% and medium-smaller banks by 31–31.4%. By contrast, smaller banks are likely to be safer as the estimates suggest the smallest magnitudes of declines in RWA values (24.2–26.9%) for these banks at any levels of NPL shocks. Overall, the figures suggest that while all banks will be affected more or less, larger banks could face heavier burdens. This could be partly explained by the significantly larger lending size and exposure of these banks. The key summary statistics presented in Fig. 5 also deliver the same message. The range of RWA value falls is bigger for banks in larger and medium-smaller categories compared to the other categories and the overall simple average for the whole sector.

Source: Author’s estimates

Overall simple average RWA shock by bank size category.

Effects on capital adequacy (CAR)

The likely effects of NPL shocks on CAR for each bank are estimated using Eq. (7) and presented in Fig. 6a, b corresponding to the different levels of NPL shocks. The figures should be considered mainly to evaluate the general patterns across all banks rather than focusing on an individual bank. At a 20% NPL shock for most banks and at a 25% shock for all banks, CAR turns negative. At the highest shock of 33%, CAR ranges from about -3 to -30% for most banks, and the revised CAR is at the worst level for ICB, FSIBL and IBBL. Figure 6c, d also suggest the same findings.

Source: Author’s estimates

Bank-wise capital adequacy ratio under different NPL shock scenario.

Figure 7 presents the sectoral average of revised CAR and changes in CAR using Eqs. (8) and (9). Figure 7a shows that sectoral average CAR is likely to go negative at a 9–13% NPL shock. This is be a great concern since CAR is the key measure of bank solvency and stability. The COVID-19-driven business and economic downturn is likely to last for a longer period, during which the RMG and textile exporters and the SME business are the biggest victims. Given the banking sector’s high exposure to RMG and textile and SMEs, a 9–13% NPL shock is not impossible. In such a case, the sectoral average of CAR will go negative, which could threaten the survival of many banks with high exposure to the two sectors. At the highest 33% NPL shock, the sectoral average of CAR reaches − 27.8 to − 30.5%, with a fall by 38.7 and 40.4% from the pre-pandemic levels according to the two averaging methods.

Source: Author’s estimates

Sectoral CAR and changes in CAR under different NPL shock scenario.

Figures 8, 9 show the effects by bank size category. Figure 8a shows that smaller banks bear the highest vulnerability. However, it should be noted that the line for smaller banks in Fig. 8a is affected by the inclusion of ICB Islamic bank in this category. Considering this fact and the other three figures, a greater degree of vulnerability of larger and smaller banks can be confirmed. At an NPL shock of about 11%, CAR for banks in these two categories are likely to turn negative, while it goes negative at about 14% for banks in the other two categories (Fig. 8b). Looking at Fig. 8c, d, the vulnerability of large banks can be reconfirmed, as they appear to see larger changes in CAR at any level of NPL shocks.

Source: Author’s estimates

CAR and changes in CAR by size category of banks under different NPL shock scenario.

Source: Author’s estimates

Key stats of CAR and changes in CAR by size category of banks under different NPL shock scenario.

Recall that Fig. 7 overall shows that CAR effects grow bigger at a faster rate and larger magnitude as the NPL shock increases. In other words, a larger NPL shock will result in a disproportionately larger CAR impact for all banks compared to a smaller NPL shock. Figure 9 reiterates these findings through presenting key summary statistics. The range (area between upper and lower level) of effects in Fig. 9a–d reconfirm a bigger effect for larger banks compared to other categories and the sectoral average.

The assessments overall suggest that larger NPL shocks will put more banks into trouble. As NPL shocks become bigger, the number of banks being able to maintain the minimum CAR requirement approaches zero. According to BASEL-III and Bangladesh Bank regulations, all banks are required to maintain a minimum CAR of 10% without a buffer and 12.5% with an extra capital conservation buffer (Bangladesh Bank 2014). While the 10% CAR requirement is the mandatory minimum for banks in Bangladesh, the 2.5% buffer is generally intended to protect banks from unexpected shocks in the credit market (Bangladesh Bank 2014).

Figure 10 shows that a 10% NPL shock will force CARs of all 30 banks to fall below the minimum requirement of 10%. On the other hand, only a 7% NPL shock will force CARs to fall below 12.5%. The findings indicate the possibly of a deeper systemic crisis, considering that the sectoral average (mean CAR of 30 banks) CAR already stands at about 9% (See Table 1). A 7–10% NPL shock is very much possible due to the pandemic. Recall that according to Bangladesh Bank (2017), the share of outstanding loans in RMG and textiles industries stands at about 13.37% as of 2016 (about USD 1050 million). The BGMEA reports that orders worth about USD 3.15 billion in 1134 factories have been cancelled or delayed as of April 2020 due to the pandemic (UNB 2020). Considering this data, Table 3 shows different scenarios of NPL shocks that could be generated from the permanent loss of revenue from the RMG and textiles order cancellations and delays during the COVID-19 pandemic.

Source: authors’ developed

Number of banks with less than minimum CAR requirement due to NPL shocks.

Table 3 shows that if only 5% of the total value (i.e., revenue) of the orders cancelled in the RMG and textiles industries are backed, financed by or constitute a bank credit, and if that 5% is permanently lost due to the order cancellations and the borrower defaults, it could generate an NPL shock of about 15%, with a multiplier effect of ‘three’. Similarly, a 10% loss in revenue could generate a 30% NPL shock and a 20% loss could eat up about 60% of the total loan outstanding in the two sectors. At the extreme end, if one-third (33%) of the total order value cancelled is backed or financed by a bank credit, and it is lost permanently and the borrower defaults, it could eat up about 100% of the total outstanding loans. Overall, Table 3 suggests that the amount of loss in the value of export orders has a multiplier effect on NPLs of three in the banking sector. In other words, 1% of permanently lost order value could generate an NPL shock of about 3%. On the other hand, the previous assessments showed that a 10% NPL shock would drag CAR of all banks to below the minimum requirement of 10%. Considering the multiplier effect, it will require a permanent loss of just over 3% values of the delayed or cancelled RMG and textiles export orders.

All things considered, the CAR effects display a worrying picture for the stability of the banking sector in Bangladesh. A 7–10% NPL shock will force all banks go under the minimum level of CAR requirements by the BASEL-III accord. In such cases, the sector would require financial assistance or fund injection of roughly USD 73.5 [63.0 + (94.5–63.0)/3] to 105 [94.5 + (126.0–94.5)/3] million to take sectoral CAR back to the pre-pandemic state. Furthermore, a 9–13% or more sector-wide NPL shock could push sectoral CAR to go zero or negative, in which case roughly USD 189 to 325.5 million of financial assistance would be required to restore sectoral CAR to the pre-pandemic level. As banks suffer from capital shortage and inadequacy to cover their assets, a persistence of the situation (which is likely given the global trends of the virus’s spread) for a longer period may put the entire banking sector in a solvency and sustainability crisis and may trigger bank runs.

Effects on interest incomes (INT)

Figure 11 presents the estimated effects on interest incomes using Eq. (15). The effects are estimated using bank-specific three interest rate scenarios—upper, lower, and average interest rates. All banks are likely to see falls in interest incomes due to NPL shocks. Under the three interest-rate scenarios, banks such as Brac, City, Rupali, and Jamuna are likely to face the biggest drops in interest income at any level of NPL shocks.

Source: Author’s estimates

Fall in interest income by bank under different NPL scenario.

At the sectoral level in Table 4 using Eq. (16), the average fall is likely to be around 3.2 (lower interest rates scenario) to 4.5% (upper interest rates scenario) at the highest level of assumed NPL shocks, while the average rates scenario suggests it to be 3.7%. It is noticeable that the divergence between the lower and upper interest scenario is expanding. This means that as NPL shocks grow bigger, the interest income effects grow at an even larger magnitude. In other words, a larger NPL shock will result in disproportionately larger falls in interest incomes for all banks compared to a smaller NPL shock.

The average effects across bank size categories are presented in Table 4. The table shows that the medium-larger banks are likely to see the biggest declines in interest incomes across all levels of NPL shocks. Considering all three interest rate cases, the estimated effects across all categories are likely to range from a 3.2 to 5.5% fall in interest incomes across the three interest rate scenarios. Furthermore, the higher interest rate scenario suggests a greater level of fall in interest incomes across all banks compared to the lower and average rate scenarios.

Conclusion

The COVID-19 pandemic poses a significant threat to the sustainability of banks globally. It will most likely be worse in developing and emerging economies, where financial systems are weak. As a case of an emerging economy that is considered to have strong economic potential, this paper considers Bangladesh and examines the possible impacts of the pandemic on the country’s banking sector. The Bangladesh banking sector already has a high level of NPLs and is crippled with many systemic problems. Using a state-designed stress testing model of the country, the paper estimates the impacts on three particular dimensions—firm value (risk-weighted asset value), capital adequacy, and operating performance (interest incomes) of banks—under different NPL shock scenarios. The shock range is defined based on the banking sector’s exposure to the two sectors—RMG & textiles and SMEs—that are the biggest victim of the pandemic. Findings suggest that all banks are likely to see a fall in their risk-weighted asset values, capital adequacy ratios, and interest incomes. The decline in all three dimensions will be disproportionately greater for larger NPL shocks. At the sectoral level, the NPL shocks will generate a sector-wide decline in all three dimensions. However, findings suggest that larger banks are relatively more vulnerable. Findings further indicate that the loss in RMG exports has a multiplier effect of ‘three’ on NPL ratios. A 10% NPL shock could force all banks to lose their minimum capital adequacy requirement and a shock of 13% or more will force sectoral CAR down to zero or negative; which is possible due to the just over 3–5% loss in RMG export order values. Given that the value of the cancelled RMG export orders are already three times larger than the sectors’ total outstanding loan taken from the banking sector and that overall economic recovery remains uncertain, NPL shocks could realistically be well over 10%. If this happens and persists, it may trigger bank-runs and systemic banking sector crises. Overall, findings call for immediate, phase-wise, and innovation-driven policy measures with a long-term approach to prevent an imminent banking sector crisis in Bangladesh. The findings could be considered as a warning sign for other emerging and developing countries where banks have high lending exposure to COVID-19-sensitive sectors and traditionally suffer from poor asset quality, high rates of NPLs, and weaker policy and regulatory frameworks. In general, the paper’s broad message is that COVID-19 is likely to put financial and capital stress on banks across all economies regardless. The findings, however, should be considered in the context of a few limitations. First, the paper includes only the publicly listed banks due to data availability issues, and expanding upon this will require private data access; second, the paper uses a stress-testing model designed by Bangladesh Bank, which is relatively simpler; and third, the stress-testing model used does not consider tax adjustments. As such, the consideration of additional complexities could require the development of a completely new model and could be considered for further research. Based on this research’s applications, further research could also consider using the Bangladesh Bank’s stress-testing models for assessing COVID-19’s likely impacts on non-bank financial institutions.

Notes

All loan figures are originally reported in Bangladesh Taka and converted to USD using the 2018 average exchange rate of 1 USD = 84 BDT based on Bangladesh Bank data.

References

ADB (2020a) Asian development outlook 2019: fostering growth and inclusion in Asian Cities. Mandaluyong City: Asian Development Bank. https://doi.org/10.22617/FLS190445-3

ADB (2020b) COVID-19 and the ready-made garments industry in Bangladesh. Asian Development Bank. https://www.adb.org/sites/default/files/linked-documents/54180-001-sd-04.pdf. Accessed 27 June 2020

Aldasoro I, Fender I, Hardy B, Tarashev N (2020) Effects of Covid-19 on the banking sector: the market’s assessment (No. 12). Bank for International Settlements

Allen F, Carletti E, Gu X (2014) The roles of banks in financial systems. Oxford Handbooks Online. https://doi.org/10.1093/oxfordhb/9780199688500.013.0002

Bachman D (2020) The economic impact of COVID-19 (novel coronavirus). Deloitte Insights. https://www2.deloitte.com/us/en/insights/economy/covid-19/economic-impact-covid-19.html. Accessed 28 June 2020

Baldwin R, di Mauro BW (eds) (2020) Economics in the time of COVID-19. CEPR Press, London

Bangladesh Bank (2010). Guidelines on Stress testing. Department of Offsite Supervision. Bangladesh Bank. https://www.bb.org.bd/aboutus/regulationguideline/apr212010stressdos.pdf. Accessed 22 Aug 2020

Bangladesh Bank (2014) Guidelines on Risk Based Capital Adequacy Revised Regulatory Capital Framework for banks in line with Basel III. December. Bangladesh Bank. https://www.bb.org.bd/mediaroom/baselii/dec212014basel3_rbca.pdf. Accessed 23 June 2020

Bangladesh Bank (2017) Study on Credit Risk arising in the Banks from Loans Sanctioned against Inadequate Collateral. Field Survey Report, Special Research Work. Bangladesh Bank. https://www.bb.org.bd/pub/research/sp_research_work/srw1702.pdf. Accessed 15 June 2020

Bangladesh Bank (2020) Major Economic Indicators: Monthly Update. March, Volume 3. Bangladesh Bank. https://www.bb.org.bd/pub/monthly/selectedecooind/magecoindmarch2020.pdf. Accessed 27 June 2020

Baret S, Celner A, O’Reilly M, Shilling M (2020). COVID-19 potential implications for banking and capital markets sector. Deloitte Insights. https://www2.deloitte.com/content/dam/insights/us/articles/6693_covid-19-banking/DI_COVID-19-banking.pdf. Accessed 28 June 2020

Barua S (2019) Financing sustainable development goals: a review of challenges and mitigation strategies. Bus Strategy Dev 3(3):277–293. https://doi.org/10.1002/bsd2.94

Barua S (2020a) Understanding coronanomics: the economic implications of the coronavirus (COVID-19) pandemic. SSRN Electron J. https://doi.org/10.2139/ssrn.3566477

Barua S (2020b) COVID-19 pandemic and world trade: Some analytical notes. SSRN 3577627.

Barua S (2020c) The impact of COVID-19 on air pollution: evidence from global data. SSRN: https://doi.org/10.2139/ssrn.3644198

Barua S, Barua B (2019) Internationalization of Bangladesh banking sector: lessons from an emerging economy. In: Sikdar A, Pereira V (eds) Business and management practices in South Asia. Palgrave Macmillan, Singapore

Barua S, Khan T, Barua B (2017) Internationalization and performance: evidence from Bangladeshi banks. J Dev Areas 51(2):105–118

Beck T (2020) Finance in the times of coronavirus. In: Baldwin and di Mauro (eds) Economics in the time of COVID-19. CEPR Press, pp 73–76

BIS (2017) Basel III: Finalising post-crisis reforms. Bank for International Settlements. https://www.bis.org/bcbs/publ/d424.pdf

BIS (2020) Measures to reflect the impact of Covid-19. Basel Committee on Banking Supervision, Bank for International Settlement. https://www.bis.org/bcbs/publ/d498.pdf. Accessed 29 June 2020

Caballero RJ, Simsek A (2009) Complexity and financial panics. NBER Working Paper, 14997. Cambridge. https://www.nber.org/papers/w14997

Cecchetti SG, Schoenholtz KL (2020) Contagion: Bank runs and COVID-19. In: Baldwin and di Mauro (eds) Economics in the time of COVID-19. CEPR Press, pp 77–80

Chen H, Qian W, Wen Q (2020) The impact of the COVID-19 pandemic on consumption: learning from high frequency transaction data. SSRN 3568574

Cheney J, Hittner R, Hogan, C, Wang P (2020) COVID-19 impact on bank liquidity risk management and response. Deloitte & Touche LLP. https://www2.deloitte.com/content/dam/Deloitte/us/Documents/regulatory/covid-regulators-response.pdf

Coibion O, Gorodnichenko Y, Weber M (2020) Labor markets during the covid-19 crisis: a preliminary view. NBER Working Paper no. w27017, Cambridge

Damak M, Freue C, Chugh G, Yalovskaya N, Tan M, Tan I et al. (2020). Banks In Emerging Markets 15 Countries, Three COVID-19 Shocks. S&P Global. https://www.spglobal.com/_assets/documents/ratings/research/2020-05-26-banks-in-emerging-markets-15-countries-three-covid-19-shocks.pdf

Dey B (2019) Managing nonperforming loans in Bangladesh. Asian Development Bank. https://doi.org/10.22617/BRF190507-2

Dominguez KM (2009) International reserves and underdeveloped capital markets. In: NBER International Seminar on Macroeconomics, vol 6, no. 1, pp 193–221. The University of Chicago Press, The National Bureau of Economic Research

Dua A, Jain N, Mahajan D, Velasco Y (2020) COVID-19’s effect on jobs at small businesses in the United States. Mckinsey & Company. https://www.mckinsey.com/industries/social-sector/our-insights/covid-19s-effect-on-jobs-at-small-businesses-in-the-united-states. Retrieved 8 July 2020

FSB (2020) COVID-19 pandemic: financial stability implications and policy measures taken. Financial Stability Board. https://www.fsb.org/wp-content/uploads/P150420.pdf. Accessed 2 July 2020

Goodell J (2020) COVID-19 and finance: agendas for future research. Finance Res Lett 35:101512. https://doi.org/10.1016/j.frl.2020.101512

Görg H, Krieger-Boden C, Nunnenkamp P (2020) Poor countries have the least-developed financial systems—that has to change. World Economic Forum. https://www.weforum.org/agenda/2016/08/poor-countries-have-the-least-developed-financial-systems-that-has-to-change/

Haldane AG, May RM (2011) Systemic risk in banking ecosystems. Nature 469(7330):351–355

ILO (2020) COVID-19 and the world of work: impact and policy responses. International Labor Organization. https://www.ilo.org/wcmsp5/groups/public/---dgreports/---dcomm/documents/briefingnote/wcms_738753.pdf. Accessed 8 July

IMF (2020) Global Financial Stability Report: Markets in the time of Covid-19. Washington DC: International Monetary Fund. https://www.imf.org/~/media/Files/Publications/GFSR/2020/April/English/text.ashx?la=en

Lagoarde-Segot T, Leoni P (2013) Pandemics of the poor and banking stability. J Bank Finance 37(11):4574–4583. https://doi.org/10.1016/j.jbankfin.2013.04.004

Lalon RM (2020) COVID-19 vs Bangladesh: Is it Possible to Recover the Impending Economic Distress Amid this Pandemic? (April 18, 2020). Manuscript. SSRN: https://doi.org/10.2139/ssrn.3579697

Larbi-Odam C, Awuah K, Frimpong-Kwakye J (2020) Financial risk implications of COVID-19 on banks. Deloitte. https://www2.deloitte.com/content/dam/Deloitte/gh/Documents/financial-services/gh-financial-risk-implications-of-COVID-19-on-banks.pdf

Mann CL (2020) Real and financial lenses to assess the economic consequences of COVID-19. In: Baldwin and di Mauro (eds) Economics in the Time of COVID-19. CEPR Press, pp 81–86

Mujeri MK, Rahman MH (2009) Financing long term investments in Bangladesh: capital market development issues. Bangladesh Bank. https://ideas.repec.org/p/ess/wpaper/id2060.html. Accessed 8 July 2020

Nguyen CV, Islam AM, Ali MM (2011) The Current State of the Financial Sector of Bangladesh: An Analysis. AIUB Bus Econ Working Paper Series. https://orp.aiub.edu/WorkingPaper/WorkingPaper.aspx?year=2011

OECD (2020a) Foreign direct investment flows in the time of COVID-19. Organisation for Economic Co-operation and Development. https://www.oecd.org/coronavirus/policy-responses/foreign-direct-investment-flows-in-the-time-of-covid-19-a2fa20c4/

OECD (2020b) COVID-19 and international trade: issues and actions. Organisation for Economic Co-operation and Development. https://www.oecd.org/coronavirus/policy-responses/covid-19-and-international-trade-issues-and-actions-494da2fa/

Park C, Villafuerte J, Abiad A, Narayanan B, Banzon E, Samson J et al. (2020) An updated assessment of the economic impact of COVID-19. Asian Development Bank https://doi.org/10.22617/BRF200144-2

Paul TC (2020, June 19) COVID-19 and its impact on Bangladesh economy. The Financial Express. https://thefinancialexpress.com.bd/views/opinions/covid-19-and-its-impact-on-bangladesh-economy-1592580397. Accessed 1 July 2020

Rigden D (2020) COVID-19: impact on international trade, transport and infrastructure. Crowe UK. https://www.crowe.com/uk/croweuk/insights/covid-19-international-trade. Accessed 8 July 2020

Roubini N (2008) The coming financial pandemic. Foreign Policy, March–April (165):44–48

Ryan D, Babczenko K, Niang N, Litton G (2020) COVID-19 and the banking and capital markets industry. PwC. https://www.pwc.com/us/en/library/covid-19/coronavirus-banking-and-capital-markets.html. Retrieved 8 July 2020

Shiller RJ (2020) COVID-19 has brought about a second pandemic: financial anxiety. World Economic Forum. https://www.weforum.org/agenda/2020/04/pandemics-coronavirus-covid19-economics-finance-stock-market-crisis/. Accessed 2 July 2020

Stiller M, Zink T (2020) Impact of COVID-19 on the European Banking Industry. IDC Perspective. International Data Corporation. https://www.idc.com/getdoc.jsp?containerId=EUR246178520. Accessed 27 June 2020

Strietzel M, Juchem K, Maus S, Küst C, Förster F, Kuonen S (2020) The German Banking Market in the Covid-19 Crisis: Rising Risks, Falling Revenues. Roland Berger. https://www.rolandberger.com/nl/Point-of-View/Financial-industry-and-COVID-19-Risks-increase-revenues-decrease.html. Accessed 23 June 2020

Stulz RM, Carey M (eds) (2006) The Risks of Financial Institutions. University of Chicago Press, Chicago

Tyson J (2020) The impact of Covid-19 on Africa’s banking system. Overseas Development Institute. https://www.odi.org/blogs/17013-impact-covid-19-africa-s-banking-system. Accessed 26 June 2020

UNB (2020) Coronavirus: BGMEA reports $3.15 billion order cancellation. The Business Standard. https://tbsnews.net/coronavirus-chronicle/covid-19-bangladesh/coronavirus-bgmea-reports-315-billion-order-cancellation. Accessed 1 July 2020

Vidovic L, Tamminaina P (2020) The Outlook for Corporate Credit Risk; COVID-19 Pandemic And Macroeconomic. S&P Global. https://www.spglobal.com/marketintelligence/en/news-insights/research/the-outlook-for-corporate-credit-risk-covid-19-pandemic-and-macroeconomic

Wilson E (2020, March 2) Coronavirus is cost and opportunity for Asia’s banks. Euromoney. https://www.euromoney.com/article/b1kl4kc07s51cv/coronavirus-is-cost-and-opportunity-for-asias-banks. Accessed 28 June 2020

World Bank (2020a) Global Economic Prospects, June 2020. Washington DC: World Bank. https://doi.org/10.1596/978-1-4648-1553-9. Accessed 08 July

World Bank (2020b) COVID-19 to Plunge Global Economy into Worst Recession since World War II. https://www.worldbank.org/en/news/press-release/2020/06/08/covid-19-to-plunge-global-economy-into-worst-recession-since-world-war-ii

World Bank (2020c) COVID-19 Outbreak: Capital Markets Implications and Response. COVID-19 Notes; Finance Series. March 25 https://pubdocs.worldbank.org/en/776691586478873523/COVID-19-Outbreak-Capital-Markets.pdf

World Bank (2020d) The Economic and Social Impact of COVID-19. Western Balkans Regular Economic Report no. 17. https://documents1.worldbank.org/curated/en/790561591286827718/pdf/The-Economic-and-Social-Impact-of-COVID-19-Financial-Sector.pdf. Accessed 1 July 2020

World Economic Forum (2020) Impact of COVID-19 on the Global Financial System. April. https://www3.weforum.org/docs/WEF_Impact_of_COVID_19_on_the_Global_Financial_System_2020.pdf. Accessed 1 July 2020

WTO (2020) Trade set to plunge as COVID-19 pandemic upends global economy. World Trade Organization. https://www.wto.org/english/news_e/pres20_e/pr855_e.htm

Yousufani M, Courbe J, Babczenko K (2020) How retail banks can keep the lights on during the COVID-19 crisis—and recalibrate for the future. https://www.pwc.com/us/en/library/covid-19/coronavirus-impacts-retail-banking.html. Accessed 8 July 2020

Funding

This research has not used any external funding and therefore has no funding-related declaration.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

They have no known competing financial interests or personal relationships that could have appeared to influence the work reported in this paper.

Ethical approval

No ethics approval is applicable for this research since the research involves no humans and/or animals.

Electronic supplementary material

Below is the link to the electronic supplementary material.

Rights and permissions

About this article

Cite this article

Barua, B., Barua, S. COVID-19 implications for banks: evidence from an emerging economy. SN Bus Econ 1, 19 (2021). https://doi.org/10.1007/s43546-020-00013-w

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s43546-020-00013-w