Abstract

We analyse the effects of aggregating the level of disagreement in survey-based expectations. With this aim, we construct several indicators based on two metrics of disagreement: the standard deviation of the balance and a geometric measure of discrepancy. We use data from business and consumer surveys in eleven European countries and the Euro Area. We evaluate the dynamic response of economic growth to shocks in agents’ uncertainty gauged by the discrepancy measures in a bivariate vector autoregressive framework. We find that while the effect on economic activity to a shock in aggregate discrepancy is always negative for firms’ disagreement, the effect to consumers’ disagreement is positive in all countries except Italy. To shed some light regarding the effect of aggregating disagreement both across variables and economic agents on forecast accuracy, we also examine the predictive performance of the discrepancy indicators, using them to generate out-of-sample forecasts of economic growth. We do not find evidence that the aggregation of disagreement improves forecast accuracy. These findings are especially relevant when using cross-sectional dispersion of survey-based expectations of firms and households.

Similar content being viewed by others

Availability of Data and Material

The datasets used and/or analysed during the current study are: The Joint Harmonised EU Consumer Survey conducted by the European Commission, which can be freely downloaded at: https://ec.europa.eu/info/business-economy-euro/indicators-statistics/economic-databases/business-and-consumer-surveys_en. Gross Domestic Product provided by Eurostat at: https://ec.europa.eu/eurostat/web/national-accounts/data/main-tables.

References

Alessandri, P., & Mumtaz, H. (2019). Financial regimes and uncertainty shocks. Journal of Monetary Economics, 101, 31–46.

Alexopoulos, M., & Cohen, J. (2015). The power of print: Uncertainty shocks, markets, and the economy. International Review of Economics and Finance, 40, 8–28.

Altig, D., Barrero, J. M., Bloom, N., Davis, S. J., Meyer, B. H., & Parker, N. (2020). Surveying business uncertainty. Journal of Econometrics. (forthcoming).

Atalla, T., Joutz, F., & Pierru, A. (2016). Does disagreement among oil price forecasters reflect volatility? Evidence form the ECB surveys. International Journal of Forecasting, 32(4), 1178–1192.

Bachmann, R., Carstensen, K., Lautenbacher, S., & Schneider, M. (2018). Uncertainty and change: Survey evidence of firms’ subjective beliefs. Technical Report.

Bachmann, R., Carstensen, K., Lautenbacher, S., & Schneider, M. (2020). Uncertainty is more than risk—Survey evidence on Knightian and Bayesian firms. Technical Report.

Bachmann, R., Elstner, S., & Sims, E. R. (2013). Uncertainty and economic activity: Evidence from business survey data. American Economic Journal: Macroeconomics, 5(2), 217–249.

Baker, S. R., Bloom, N., & Davis, S. J. (2016). Measuring economic policy uncertainty. Quarterly Journal of Economics, 131(4), 1593–1636.

Basu, S., & Bundick, B. (2017). Uncertainty shocks in a model of effective demand. Econometrica, 85(3), 937–958.

Bekaert, G., Hoerova, M., & Lo Duca, M. (2013). Risk, uncertainty and monetary policy. Journal of Monetary Economics, 60(7), 771–788.

Binding, G., & Dibiasi, A. (2017). Exchange rate uncertainty and firm investment plans evidence from Swiss survey data. Journal of Macroeconomics, 51, 1–27.

Bloom, N. (2009). The impact of uncertainty shocks. Econometrica, 77(3), 623–685.

Caldara, D., Fuentes-Albero, C., Gilchrist, S., & Zakrajšek, E. (2016). The macroeconomic impact of financial and uncertainty shocks. European Economic Review, 88, 185–207.

Carriero, A., Clark, T. E., & Marcellino, M. (2018). Measuring uncertainty and its impact on the economy. Review of Economics and Statistics, 100(5), 799–815.

Cascaldi-Garcia, D., Sarisoy, C., Londono, J. M., Rogers, J., Datta, D., Ferreira, T., et al. (2020). What is certain about uncertainty?. International Finance Discussion Papers 1294. Washington: Board of Governors of the Federal Reserve

Castelnuovo, E. (2019). Domestic and global uncertainty: A survey and some new results. CESifo Working Paper Series 7900.

Cerda, R., Silva, A., & Valente, J. T. (2018). Impact of economic uncertainty in a small open economy: The case of Chile. Applied Economics, 50(26), 2894–2908.

Charles, A., Darné, O., & Tripier, F. (2018). Uncertainty and the macroeconomy: Evidence from an uncertainty composite indicator. Applied Economics, 50(10), 1093–1107.

Chuliá, H., Guillén, M., & Uribe, J. M. (2017). Measuring uncertainty in the stock market. International Review of Economics and Finance, 48, 18–33.

Claveria, O. (2018). A new metric of consensus for Likert scales. IREA Working Papers 2018/21. University of Barcelona, Institute of Applied Economics Research (IREA).

Claveria, O. (2019). A new consensus-based unemployment indicator. Applied Economics Letters, 26(10), 812–817.

Claveria, O. (2020). Uncertainty indicators based on expectations of business and consumer surveys. Empirica. (forthcoming).

Claveria, O., Monte, E., & Torra, S. (2019). Economic uncertainty: A geometric indicator of discrepancy among experts’ expectations. Social Indicators Research, 193(1), 91–114.

Clements, M., & Galvão, A. B. (2017). Model and survey estimates of the term structure of US macroeconomic uncertainty. International Journal of Forecasting, 33(3), 591–604.

Crespo, J., Huber, F., & Onorante, L. (2017). The macroeconomic effects of international uncertainty shocks. WU Working Paper Series 245.

Dibiasi, A., & Iselin, D. (2019). Measuring Knightian uncertainty. KOF Working Papers 456.

Dibiasi, A., & Sarferaz, S. (2020). Measuring macroeconomic uncertainty: A cross-country analysis. KOF Working Papers 479, 1–44.

Diebold, F. X., & Mariano, R. (1995). Comparing predictive accuracy. Journal of Business and Economic Statistics, 13(3), 253–263.

Dovern, J., Fritsche, U., & Slacalek, J. (2012). Disagreement among forecasters in G7 countries. Review of Economic and Statistics, 94(4), 1081–1096.

European Commission. (2020). Business and consumer surveys. https://ec.europa.eu/info/business-economy-euro/indicators-statistics/economic-databases/business-and-consumer-surveys_en. Accessed 3 Sep 2020.

Eurostat. (2020). Database. https://ec.europa.eu/eurostat/web/national-accounts/data/main-tables. Accessed 3 Sep 2020.

Girardi, A., & Reuter, A. (2017). New uncertainty measures for the euro area using survey data. Oxford Economic Papers, 69(1), 278–300.

Glas, A. (2020). Five dimensions of the uncertainty—Disagreement linkage. International Journal of Forecasting, 36(2), 607–627.

Glocker, C., & Hölzl, W. (2019). Assessing the economic content of direct and indirect business uncertainty measures. WIFO Working Paper 576/2019.

Gupta, R., Lau, C. K. M., & Wohar, M. E. (2019). The impact of US uncertainty on the Euro area in good and bad times: Evidence from a quantile structural vector autoregressive model. Empirica, 46(2), 353–368.

Hailemariam, A., & Smyth, R. (2019). What drives volatility in natural gas prices? Energy Economics, 80, 731–742.

Harvey, D. I., Leybourne, S. J., & Newbold, P. (1997). Testing the equality of prediction mean squared errors. International Journal of Forecasting, 13(2), 281–291.

Hauzenberger, N., Böck, M., Pfarrhofer, M., Stelzer, A., & Zens, G. (2018). Implications of macroeconomic volatility in the Euro area. ArXiv preprint, 1801, 02925.

Istiak, K., & Serletis, A. (2018). Economic policy uncertainty and real output: Evidence from the G7 countries. Applied Economics, 50(39), 4222–4233.

Jo, S., & Sekkel, R. (2019). Macroeconomic uncertainty through the lens of professional forecasters. Journal of Business & Economic Statistics, 37(3), 436–446.

Junttila, J., & Vataja, J. (2018). Economic policy uncertainty effects for forecasting future real economic activity. Economic Systems, 42(4), 569–583.

Jurado, K., Ludvigson, S., & Ng, S. (2015). Measuring uncertainty. American Economic Review, 105(3), 1177–1216.

Knight, F. (1921). Risk, uncertainty, and profit. Boston: Houghton Mifflin.

Kozeniauskas, N., Orlik, A., & Veldkamp, L. (2016). The common origin of uncertainty shocks. NBER Working Paper 22384. National Bureau of Economic Research (NBER).

Krüger, F., & Nolte, I. (2016). Disagreement versus uncertainty: Evidence from distribution forecasts. Journal of Banking & Finance, Supplement, 72, S172–S186.

Lahiri, K., & Sheng, X. (2010). Measuring forecast uncertainty by disagreement: The missing link. Journal of Applied Econometrics, 25(4), 514–538.

Meinen, P., & Roehe, O. (2017). On measuring uncertainty and its impact on investment: Cross-country evidence from the euro area. European Economic Review, 92, 161–179.

Mokinski, F., Sheng, X., & Yang, J. (2015). Measuring disagreement in qualitative expectations. Journal of Forecasting, 34(5), 405–426.

Morikawa, M. (2019). Uncertainty over production forecasts: An empirical analysis using monthly quantitative survey data. Journal of Macroeconomics, 60, 163–179.

Oinonen, S., & Paloviita, M. (2017). How informative are aggregated inflation expectations? Evidence from the ECB Survey of Professional Forecasters. Journal of Business Cycle Research, 13(2), 139–163.

Ozturk, E. O., & Sheng, X. S. (2018). Measuring global and country-specific uncertainty. Journal of International Money and Finance, 88, 276–295.

Paloviita, M., & Viren, M. (2014). Inflation and output growth uncertainty in individual survey expectations. Empirica, 41(1), 69–81.

Poncela, P., & Senra, E. (2017). Measuring uncertainty and assessing its predictive power in the euro area. Empirical Economics, 53(1), 165–182.

Rossi, B., & Sekhposyan, T. (2015). Macroeconomic uncertainty indices based on nowcast and forecast error distributions. American Economic Review, 105(5), 650–655.

Rossi, B., & Sekhposyan, T. (2017). Macroeconomic uncertainty indices for the euro area and its individual member countries. Empirical Economics, 53(1), 41–62.

Rossi, B., Sekhposyan, T., & Souprez, M. (2020). Understanding the sources of macroeconomic uncertainty. Barcelona GSE Working Paper 920. Barcelona Graduate School of Economics (GSE).

Sahinoz, S., & Cosar, E. E. (2019). Quantifying uncertainty and identifying its impacts on the Turkish economy. Empirica, 47(2), 365–387.

Sorić, P., & Lolić, I. (2017). Economic uncertainty and its impact on the Croatian economy. Public Sector Economics, 41(4), 443–477.

Yıldırım-Karaman, S. (2017). Uncertainty shocks, central bank, characteristics and business cycles. Economic Systems, 41(3), 379–388.

Zarnowitz, V., & Lambros, L. A. (1987). Consensus and uncertainty in economic prediction. Journal of Political Economy, 95(3), 591–621.

Funding

This research received no financial support.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no competing interests.

Code Availability

Not applicable.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

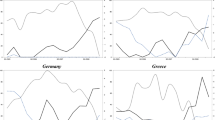

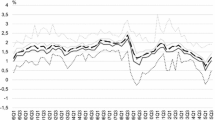

Figure 6 contains the evolution of the disagreement indicators presented in Sect. 2 computed with the geometric indicator of discrepancy (G).

Evolution of disagreement indicators (2003:01–2020:08)

Table 5 presents the results of the estimation of the VAR models.

Rights and permissions

About this article

Cite this article

Claveria, O. On the Aggregation of Survey-Based Economic Uncertainty Indicators Between Different Agents and Across Variables. J Bus Cycle Res 17, 1–26 (2021). https://doi.org/10.1007/s41549-020-00050-2

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s41549-020-00050-2