Abstract

In this paper we analyse the effects of trade and specialisation on regional business cycle co-movement in the Economic and Monetary Union. Using a novel and unique bilateral regional trade dataset, we find that regions with stronger trade linkages and similar economic structures have more synchronized cycles. These results suggest that policies fostering regional specialization at the European level may reduce business cycle synchronization across regions and countries. This, in turn, might generate macroeconomic tensions in the common currency area. On the other hand, market integration policies can foster regional cycle synchronization and favour the functioning of the monetary union.

Similar content being viewed by others

1 Introduction

The convergence of business cycles among European regions has recently emerged as a key issue for the sustainability of the European Economic and Monetary Union (EMU). The reason is that divergent regional cycles may undermine the consensus regarding monetary policy, ultimately reducing its effectiveness. This appears to be especially true in the absence of interregional risk-sharing mechanisms capable of absorbing idiosyncratic shocks.

The EMU represents the most ambitious example of a recently created currency union in the world. Interestingly, the international agreement among European countries presents at least two critical features that challenge the sustainability of the currency area. The first is the lack of specific provisions for the establishment of a common fiscal policy with a redistributive, and hence stabilising, capacity comparable to that of existing federal countries. This aspect has emerged in the European debate in recent years and has been studied in several contributions (see, among others, Furceri and Zdzienicka 2013).

The second crucial aspect is the increasing autonomy of policymaking in European regions, as well as metropolitan and rural territorial entities characterised by heterogeneous institutional models and economic structures. In particular, the relevance of regions in the institutional and economic architecture of the EMU has been growing over the last few years. Many countries have increased their degrees of fiscal and political decentralization, resulting in regions and other sub-national governmental tiers being in charge of substantial spending tasks as well as revenue sources (OECD 2009a).

Moreover, regions are major stakeholders of the Cohesion policy based on the European Structural and Investment Funds. Recently, the European regional policy has been explicitly redefined as a place-based policy aimed at exploiting comparative advantages and Marshallian agglomeration economies (OECD 2009b; Barca 2009; Ahner and Landabaso 2011; Barca et al. 2012). Such a territorial articulation of economic policy is relevant for the EMU as it may deepen the segmentation of European economic geography, increase interregional specialization, and reduce the synchronization of regional business cycles.

Existing studies on regional cycles and the EMU have focused on two main aspects: the role of the EMU in the convergence of European regions (Martin 2001; Fingleton et al. 2015); and the impact of pan-European interregional risk-sharing mechanisms on regional cycles (Basile and Girardi 2010). However, very few studies have analysed the determinants of business cycle synchronization among European regions, and even fewer have identified the potential channels through which regional and macroeconomic policies may affect the synchronization of regional cycles. The absence of adequate regional data or their incompleteness for the purpose of international comparison is one of the reasons behind the lack of studies on these topics.

Our paper fills this gap by bringing an established empirical model of the determinants of business cycle synchronization to the European regional dimension using a newly created dataset on imputed bilateral trade between regions of the EMU (Thissen et al. 2013a, b; Thissen and Gianelle 2014). The focus of our empirical analysis is on the impact of two factors that are especially influenced by European policies: (1) the regional specialization pattern, directly affected by regional place-based policies, and (2) interregional economic integration, affected by the pan-European economic integration policies.

We firstly calculate the degree of regional business cycle co-movement within the EMU in the 2000–2010 period. Then, we provide estimates of how regional specialization (i.e. dissimilarity of economic structures) and economic integration (proxied by bilateral trade intensity) affect such co-movement of the business cycles across European regions, controlling for financial and monetary factors such as FDI stocks and the existence of the euro. We also investigate the channels behind the direct effects of regional specialization and economic integration. This latter part of the analysis permits us to comment on factors such as the relative importance of intra-industry trade and inter-industry trade.

To the best of our knowledge, existing studies dealing with regional cycle synchronization do not employ bilateral data and either simply illustrate the behaviour of cycle co-movement (Fatás 1997; Montoya and De Haan 2008) or concentrate on different aspects such as regional investments and employment and productivity dynamics (Anagnastou et al. 2015; Marino 2013; Fingleton et al. 2015). Our study hence represents a novelty in many respects. A limitation of the paper is probably that, due to the lack of regionalised data, we can only control for financial integration at the national level. Nevertheless, we do not see this as a major drawback, as the degree of financial integration of regions is typically the result of national policies and is therefore determined at the country level. We also perform a thorough sensitivity analysis using alternative measures of regional financial integration which confirms our main results.

We find that trade intensity has a positive impact on business cycle co-movement, whereas sectorial specialization has a negative effect. Both results are economically substantial and robust across a variety of empirical specifications and confirm existing country-level evidence. It appears that the positive direct effect of trade on cycle synchronization can be primarily attributed to intra-industry trade, while the impact of specialization seems to depend mainly on the level of regional development. We discuss the implications of these results for the EMU and the European regional policy.

The remainder of the paper is organised as follows. Section 2 contains a brief review of the literature on EMU and regional cycles and on the determinants of business cycle synchronization for both countries and regions. Section 3 presents the empirical model and the data used for the analysis. Section 4 illustrates the results, and Sect. 5 provides a concluding discussion.

2 Background and Literature

The economic literature has long recognised the synchronization of business cycles across countries forming a currency union as an important condition to guarantee the alignment of incentives towards common monetary policy stances (Tavlas 2009). One simple reason for this is effectively summarised by De Haan et al. (2008): countries in the downward phase of the cycle prefer a more expansionary monetary policy to foster economic recovery, while countries in the upward phase of the cycle prefer a more restrictive policy in order to control price stability. Thus, the unique monetary policy of a currency union cannot suit all members when their business cycles are not synchronized.

In recent years, the synchronization of regional cycles has also emerged as a relevant topic in the debate on whether the EMU represents a viable currency area. The regional implications of the EMU have been discussed by economic geographers in a number of contributions. Martin (2001) analysed the impact of the EMU on the convergence of European regions, finding that while worker productivity across European regions has shown a weak convergence, employment growth has been sharply divergent. Fingleton et al. (2015) investigated whether regions within the eurozone have become more or less similar in their vulnerability and resilience to shocks since the creation of the monetary union. They concluded that common contractionary shocks had the biggest impact on the most geographically isolated regions, principally located in those peripheral countries that suffered the most from the recent economic crisis.

Others have focused on the effects of interregional risk-sharing mechanisms in the presence of diverging regional cycles forming a monetary union. Basile and Girardi (2010) analysed the impact of interregional insurance mechanisms (such as redistributive fiscal transfers) on the industrial specialization of European regions. Their analysis shows that industrial specialization is positively affected by risk-sharing mechanisms which help to “protect” the economic environment against idiosyncratic shocks even in the presence of diverging regional cycles.

However, despite the widespread interest in the effects of regional business cycle synchronization, there are almost no studies investigating its determinants. Economic theory has identified three main families of determinants of business cycle synchronization across countries: (1) the degree of relative specialization, i.e. the structural dissimilarity between the economies; (2) the degree of economic integration and trade; (3) the extent of fiscal integration.

The influential contribution by Frankel and Rose (1998) gave birth to a strand of literature investigating empirically the factors responsible for business cycle synchronization at the national level. In a seminal analysis taking into account potential endogeneity issues, they demonstrated that countries with closer trade links, proxying for economic integration, have more tightly correlated business cycles. Baxter and Kouparitsas (2005) also found a positive impact of trade intensity on cycle co-movement and concluded that bilateral trade and some gravity variables are the only robust determinants of such co-movement. Calderón et al. (2007) studied the differences between developing and developed countries and found that, while trade intensity affects business cycle correlation in both groups of countries, the effects are substantially larger among developed countries. On the other hand, Inklaar et al. (2008) concluded that fiscal and monetary policies matter more than trade in terms of the magnitude of the effects. Overall, despite a lack of consensus on the exact magnitude of the effects, the existing evidence suggests that pairs of industrialised countries exhibit a higher degree of business cycle co-movement if they trade more with each other.

Cross-country specialization, i.e. similarity in the sectorial structure of the economy, is another important factor for business cycle co-movement, as the presence of sector-specific shocks implies that the cycles of similar economies will tend to co-move. Aggregate shocks may also similarly affect cycle co-movement due to the sector-specific responses to such shocks (for instance, monetary shocks affect the various sectors of the economy differently due to their different market structures and labour market characteristics).

The existing empirical evidence on the role played by sectorial specialization suggests that country-pairs’ similarity in the sectorial structure may be substantially correlated to business cycle co-movement. Imbs (2004) used data for 20 countries in the 1980s and 1990s to find that the economic cycles of countries with similar economic structures are more correlated than those of countries differing in that respect. He also found trade to have a significant role in shaping the patterns of sectorial specialization, suggesting that trade might affect cycle synchronization via specialization and vice versa. Calderón et al. (2007) supported those findings by investigating a larger sample over a 40-year period.

The empirical literature above has been enriched by a number of recent contributions investigating additional potential determinants of synchronization. Financial integration is one of those, in its various dimensions such as globalisation (Kose et al. 2003), bank and portfolio linkages (Kalemli-Ozcan et al. 2013a, b; IMF 2013a, b, respectively), FDI (Keil and Sachs 2014; Jansen and Stokman 2011), net foreign asset positions (Imbs 2004), and debt market linkages (Davis 2014).

Finally, a number of studies specifically focus on Europe. Clark and van Wincoop (2001) compared the degree of synchronization of US regions with that of European countries and found that the former is higher than the latter. They concluded that the lower level of trade between European countries is the main reason behind this result, while the importance of specialization, monetary policy, and fiscal policy appears to be negligible. De Haan et al. (2008) documented that European cycles have gone through periods of divergence and convergence over the recent decades. They concluded that trade intensity plays a crucial role in increasing the synchronization of the cycles of European countries, more so than sectorial specialization, monetary and financial integration, and fiscal policy. However, there is no consensus on the magnitude of this effect.

Siedschlag (2010) concentrated on the role of trade intensity and sectorial specialization for the co-movement of the business cycles between the euro area countries on one hand and eight new EMU member countries on the other. Results point to both factors being positively associated with business cycle correlation, with sectorial specialization having an additional indirect effect due to its positive impact on trade intensity. Recent evidence provided by Busl and Kappler (2013) suggested that the role of trade could be smaller than previously thought, with FDI emerging as a crucial factor driving cycle synchronization of EMU countries.

The evidence reported so far is based on country-level analyses, as very few contributions explore the determinants of regional business cycle correlation. Siedschlag and Tondl (2011) used regional data and concluded that trade intensity positively affects the correlation between the regional growth rate of real gross value added (GVA) and the euro area average growth rate, while sectorial specialization and exchange rate volatility are negatively correlated to it. However, the authors did not employ bilateral trade data; therefore, their analysis differs substantially from the standard country-level analysis featured in the contributions briefly reviewed above.

Clark and van Wincoop (2001) also used regional data in their analysis, but only to a limited extent, and Belke and Heine (2006) studied the correlation of regional employment growth rather than regional GDP. Basile et al. (2014) found that firm heterogeneity lies behind a substantial part of the cyclical differences between the northern and the southern regions of Italy. Our contribution is therefore the first to offer an analysis testing the factors affecting the business cycle correlation in the EMU regions using a comprehensive bilateral dataset.

3 Empirical Strategy

This section is organised as follows: Sect. 3.1 illustrates the empirical model and the identification strategy. Section 3.2 contains a list of the variables and their exact definitions. Particular attention is devoted to the main variables of the empirical model: regional business cycle co-movement, bilateral trade intensity, and sectorial specialization.

3.1 The Empirical Model

We follow the approach proposed by Imbs (2004) to identify the effects of bilateral trade intensity and specialization on regional business cycle co-movement. This allows us to deal with potential issues of both simultaneity and endogeneity. Specifically, we define a system of three equations to explicitly model the dependencies between bilateral trade intensity and structural specialization on one side, and business cycle co-movement on the other side, as well as the linkages between the first two.

Then, we estimate this system of equations using alternative econometric techniques that allow for different hypotheses regarding the causal determination of the three main variables of interest. In particular, we allow for the possibility that business cycle co-movement, bilateral trade intensity, and the degree of structural dissimilarity between economies are to some extent co-determined (simultaneity); we also account for the potential endogeneity of the latter two variables in the equation explaining business cycle co-movement. The system is the following:

where ρ ij measures the bilateral business cycle correlation between region i and region j; T ij stands for the bilateral trade intensity between region i and region j; and S ij is a measure of the dissimilarities of economic structures (normally referred to as sectorial specialization) between region i and j. These three variables are assumed to be endogenously determined in the system. It is worth noting that the system also acknowledges the possibility that trade intensity may affect sectorial specialization and vice versa, as suggested by economic theory. Vectors \( {\mathbf{I}}_{{\mathbf{1}}}^{{{\mathbf{fin\_monet}}}} \), \( {\mathbf{I}}_{{\mathbf{2}}}^{{{\mathbf{gravity}}}} \), \( {\text{I}}_{ 3}^{\text{financial}} \) and \( {\mathbf{I}}_{{\mathbf{3}}}^{{{\mathbf{development}}}} \) are non-overlapping sets of additional explanatory variables considered to be exogenous. All variables except dummies and time-invariant variables are averages over the 2000–2010 period in the cross-sectional estimates.Footnote 1

Equation (1) is routinely used to assess the impact of trade intensity and specialization on business cycle synchronization. Vector \( {\mathbf{I}}_{{\mathbf{1}}}^{{{\mathbf{fin\_monet}}}} \) contains measures of financial and monetary integration which are modelled as exogenous to regional cycle correlations.Footnote 2 Equation (2) is a standard gravity equation augmented with an index of the structural dissimilarity of regional economies (S), with \( {\mathbf{I}}_{{\mathbf{2}}}^{{{\mathbf{gravity}}}} \) comprising an array of factors which have been proven to be strongly related with bilateral trade and are routinely regarded as exogenous: geographical factors (captured by a common border dummy and the distance between regional capital cities), cultural similarity (proxied with a common language dummy), and the size of regional economies (measured by the product of GDPs and the product of populations). Equation (3) is the one that is the least established in the literature. Besides trade intensity (T), it contains a set of exogenous explanatory variables which capture financial integration measures (I financial3 ) and economic/geographical factors (\( {\mathbf{I}}_{{\mathbf{3}}}^{{{\mathbf{development}}}} \)) which are likely to influence sectorial specialisation patterns and hence can contribute to explain differences in the economic structures across countries. More details on the variables included in the model and their construction is contained in Sect. 3.2 below.

We estimate Eqs. (1)–(3) using the following estimators: (1) equation-by-equation ordinary least squares (OLS), which assumes all regressors to be exogenous; (2) seemingly unrelated regressions (SUR), which account for simultaneity; (3) three-stage least squares (3SLS), which accounts for both simultaneity and endogeneity by instrumenting T and S with all exogenous variables.

The latter estimator allows us to address potential omitted-variable bias in Eq. (1) due for instance to common shocks hitting trading partner economies symmetrically and producing an increase in their business cycle correlation. All else being equal, a positive shock will also tend to increase foreign demand for both economies (therefore intensifying trade) and hence result in a positive correlation between business cycle co-movement and the intensity of bilateral trade. Meanwhile, a negative shock may decrease foreign demand for both economies, reduce trade intensity and consequently induce a negative correlation between business cycle co-movement and bilateral trade.

Endogeneity may also hinder the empirical identification of the effect of sectorial specialization on business cycle correlation in Eq. (1), since these two variables may respond to unobserved factors, like sector-specific shocks. The estimation of the model with the three alternative estimators listed above will permit us to better understand the relationships between our variables of interest.

The system of Eqs. (1)–(3) allows us to determine the direct effects of trade intensity and structural dissimilarity on business cycle co-movement, which is the focus of our analysis. These effects are captured by α 1 and α 2, respectively. Moreover, the model allows us to identify the indirect effects of these two variables by using information from Eqs. (2) and (3).

In fact, trade intensity can affect business cycle synchronization through its effect on sectorial specialization. This effect is captured by the coefficient γ 1 which, multiplied by α 2, will yield the indirect effect of trade intensity on cycle synchronization through specialization. At the same time, changes in the sectorial structure of trading partners can affect the intensity of bilateral trade. Specifically, β 1 in Eq. (2) captures the extent to which bilateral trade accounts for sectorial specialization in the two regions, i.e. intra-industry trade. A negative β 1 would then mean that regions with similar economic structures are associated with higher intra-industry trade. That coefficient, multiplied by α 1, will tell us about the indirect effect of specialization on cycle synchronization.

The direct effects of trade intensity and sectorial dissimilarity are presented and discussed in Sect. 4.1. By means of some additional computations, the indirect effects are calculated in Sect. 4.2, where we also investigate the direct effects further in order to assess the relative importance of intra-industry trade versus inter-industry trade and to analyse separately the components of the direct effect of specialization on the correlation of business cycles.

3.2 Data and Measurement

Our analysis uses annual data for 244 NUTS2 regions of 23 EU countries from 2000 to 2010. The variable measuring business cycle co-movement, which is the dependent variable of Eq. (1), ρ ij , is calculated as the bilateral correlation of the cyclical components of real GDP between regions i and j. The GDP cyclical component is obtained by applying the Hodrick-Prescott filter to the 1980–2010 real GDP series (as done by, among others, Kose and Yi 2006) taken from the European Regional Database published by Cambridge Econometrics.Footnote 3 While it is hard to summarise how all the pairs of EU regions behave in terms of the synchronization of their business cycles, it is interesting to note that the 10 most synchronized regions in our sample are all within the UK (with the highest value associated with the Essex—Greater Manchester pair).

The variable accounting for trade intensity among EU regions, T ij , is based on a unique and novel dataset made available by the PBL Netherlands Environmental Assessment Agency and the European Commission (Thissen et al. 2013a, b; Thissen and Gianelle 2014). The series were constructed following the methodology proposed by Simini et al. (2012).Footnote 4 The dataset contains annual data on imputed bilateral trade in consumer prices for European NUTS2-level regions in the 2000–2010 period. The dataset also contains trade flows with the rest of the world and consumption within regions, so total trade adds up to regions’ total production. All data are consistent with national accounts and regional trade hubs are accounted for so that all estimated trade flows refer to final destinations.

We use (separately) two alternative measures of bilateral trade intensity. The first measure is computed as follows:

where X ijt stands for the exports of region i to region j, M ijt for the imports of region i from region j, and X it and M it (X jt and M jt ) are the total exports and total imports of region i (j), respectively. Our second measure of trade intensity, T 2,ij , first proposed by Frankel and Rose (1998), simply differs in the denominator by replacing the total trade flows of regions iandjwith their GDPs. In our baseline specification, we employ T 1,ij as the measure of trade intensity but, as shown in the sensitivity analysis part of the paper, our results are comparable when using T 2,ij below:

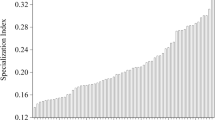

As for specialization, we use what is normally referred to as the Krugman specialization index. This is in fact a measure of similarity in the economic structures of the regional economies, which is why we sometimes refer to it as a measure of differences in the sectorial composition of the regional economies. We construct this measure using GVA data for six economic sectors (agriculture; industry; construction; wholesale, retail, transport and distribution, communications, hotels and catering; financial and business services; non-market services) retrieved from the Cambridge Econometrics regional dataset.Footnote 5 The measure, used by Imbs (2004) and Calderón et al. (2007) among others, is calculated as follows:

where s n,i and s n,j stand for the GVA shares of industry n in region i and in region j, respectively. For robustness purposes, we also measure specialization in an alternative way. The second measure of structure similarity, S 2,ij , is built by considering only the GVA shares of the industry/manufacturing sector to acknowledge its importance in determining the regional trade flows (most traded goods are indeed produced by the manufacturing sectors).

Table 1 shows the summary statistics for the endogenous variables of the system, i.e. cycle synchronization (ρ ij ) and the two alternative series used to account for trade intensity (T ij ) and sectorial specialization (S ij ). Descriptive statistics for our dependent variable (ρ ij ) reveal that the business cycles of European regions are on the whole considerably synchronized (mean 0.593). There is, however, high variability across pairs of regions with cycle synchronization ranging from a maximum of 0.996 to a minimum of −0.842.

The following variables included in the system formed by Eqs. (1)–(3) are considered to be exogenous. Vector \( {\mathbf{I}}_{{\mathbf{1}}}^{{{\mathbf{fin\_monet}}}} \) contains variables controlling for monetary integration and for financial integration. We control for monetary integration with two dummy variables related to the choice of countries to adopt the euro as their currency or to peg their currency to the euro: europeg_europeg and europeg_non-europeg. The former takes the value 1 when both regions belong to countries of the euro area or whose currencies are pegged to the euro, and 0 otherwise.Footnote 6 The second dummy, europeg_non-europeg, takes the value 1 when either region i or regionj belongs to a country of the euro area or to a country whose currency is pegged to the euro and the other does not, and 0 otherwise. Thus, the reference category (i.e. the omitted dummy) is that of regional pairs in countries not belonging to the euro area or whose currencies are not pegged to the euro. This implies that, for instance, a positive value of the europeg_europeg coefficient would suggest that the GDP of regions in countries that are both members of the euro area or that have their currency pegged to the euro co-moves more than the GDP of regions outside the euro area or whose currencies are not fixed to the euro, all else being equal.

The measure of financial integration contained in \( {\mathbf{I}}_{{\mathbf{1}}}^{{{\mathbf{fin\_monet}}}} \) is computed using data on FDI stocks from the OECD Foreign Direct Investment Database. Despite the focus of our analysis being on regions, the financial integration measure is a country-level one, due to the lack of bilateral regional data on FDI. In the sensitivity analysis, we also employ a regional measure of financial integration using information on the number of multinational companies in the various EMU regions taken from the ORBIS database. Thus, the measure of (national) financial integration used in the baseline estimates is the following:

where FDI i,t and FDI j,t stand for the total FDI stocks received by the countries to which regions i and j belong. This measure captures the total degree of financial integration through the FDI of the countries to which the pairs of regions belong. The regional FDI measure (FDI_reg ij ) used for the additional estimates carried out for robustness purposes is computed by allocating national FDI to regions using the shares of multinational firms located in those regions; due to the lack of detailed information on the location of firms’ plants in the ORBIS database, this variable can only provide an approximation of the actual activity of multinationals in each region. In particular, the shares are obtained by dividing the number of multinational companies in each region by the total number of multinational companies in the country to which the region belongs. Although the number of multinationals is certainly related to the FDI stocks received by a country, the assumption behind such a procedure is quite demanding (namely, that each multinational is of an equal size), therefore we feel more comfortable utilising this alternative measure of financial integration only for robustness purposes rather than in the baseline.

The \( {\mathbf{I}}_{{\mathbf{2}}}^{{{\mathbf{gravity}}}} \) vector in Eq. (2) includes the following set of standard gravity variables to explain bilateral trade intensity. The distance between regions’ capital cities is expressed in (the logarithm of) kilometres.Footnote 7 The common border and language dummy variables refer to the countries to which regions pertain and are taken from the Centre d’Etudes Prospectives et d’Informations Internationales (CEPII) database. The logarithmic products of the regional populations and regional GDPs (taken from the Cambridge Econometrics regional dataset) are also included in the \( {\mathbf{I}}_{{\mathbf{2}}}^{{{\mathbf{gravity}}}} \) vector as they normally feature in standard gravity models.

Finally, Eq. (3) includes as determinants of sectorial specialization both trade intensity and the vector of controls \( {\mathbf{I}}_{{\mathbf{3}}}^{{}} \). The latter includes (in I financial3 ) a measure of financial integration which differs from the one used in Eq. (1), as it is calculated using the net foreign assets position (NFA) from the External Wealth of Nations database of Lane and Milesi-Ferretti (2011). The index is defined as follows:

where NFA i,t and NFA j,t are the NFAs of the countries where region i and region j are located. Previous studies have found that financial integration is an important determinant of sectorial socialization. In particular, financially integrated countries tend to have dissimilar industrial sectorial patterns (Kalemli-Ozcan et al. 2003). Hence, the reason for including this control is that we expect the degree of sectorial similarity of two regions to be influenced by variations in their degrees of financial integration.

Included in the \( {\mathbf{I}}_{{\mathbf{3}}}^{{{\mathbf{development}}}} \) vector are the following variables accounting for the different stages of regional development: the (log) product of the regional areas, the (log) product of regional GDP per capita, and the (log) GDP per capita gap between the two regions defined as follows: ΔGDP_pc = max [(Y pc i /Y pc j ), (Y pc j /Y pc i )].

The inclusion of the product of GDP per capita is explained by the fact that pairs of rich countries tend to have more similar economic structures (Imbs 2004). Furthermore, in order to account for the possibility of such a relationship being non-monotonic [e.g. countries may initially diversify and then respecialize once they reach a relatively high level of income per capita, according to Imbs and Wacziarg (2003)], the gap between per capita GDPs is also included as a control. Finally, the product of the geographic areas is included in order to control for the fact that larger regions may be more likely to have more diversified and similar economic structures in comparison to smaller ones (Siedschlag 2010).

4 Results

Before moving to the results of the regression analysis, it is worth having a look at the simple correlations between business cycle synchronization and the various measures of trade intensity and sectorial specialization (Table 2). Although such correlations are only superficially informative due to the various simultaneity and endogeneity concerns illustrated above, they can provide useful information for the subsequent econometric analysis.

First, trade intensity is positively correlated to business cycle synchronization (the second measure more so than the first one), while sectorial specialization is negatively correlated to it (in this case the first measure exhibits a higher coefficient in absolute terms than the second one). Although very preliminary, this finding confirms the available country-level evidence reviewed in Sect. 2 on the positive (negative) impact of trade intensity (sectorial specialization) on cycle co-movement. This seems to be a first result supporting the suitability of the bilateral regional dataset that we are putting to the test using the workhorse model normally used to study business cycle synchronization at the country level. Second, trade intensity and sectorial specialization are negatively correlated irrespective of the measures used for the two variables. Finally, both measures of trade intensity and both measures of sectorial specialization are highly correlated with each other (0.882 and 0.727 respectively).

4.1 Baseline Results: Direct Effects

The results of the estimation of the cross-sectional baseline specification of the system of Eqs. (1)–(3) are presented in Table 3 (in all cases T 1,ij and S 1,ij are used to measure trade intensity and sectorial specialization, respectively). Logarithms of all right-hand-side variables except the dummies are used in the estimates in line with previous empirical analyses. The first column of Table 3 contains the equation-by-equation OLS estimates, the second shows the SUR estimates, and the last column contains the 3SLS estimates. The comparison between the OLS and the other estimates permits us to understand how results are affected when accounting for both simultaneity and endogeneity (3SLS). In general, results are consistent across the various estimators, with the main differences related to the magnitudes of the estimated effects.

In Eq. (1), with business cycle synchronization as the dependent variable, the effect of trade intensity is positive and highly statistically significant. The OLS point estimates imply that doubling trade results in a correlation of real GDP that is 0.034 higher.Footnote 8 This appears to be in line with existing country-level evidence. For example, Imbs (2004) finds that as trade intensity doubles, bilateral GDP correlations increase by 0.048, whereas Kose and Yi (2006) estimate a 0.033 increase for the same trade intensity increase. So, the more two regions trade with each other, the more their real GDPs will co-move. In economic terms, this result is by no means insignificant. An increase in bilateral trade among EU regions would impact their business cycle synchronization significantly, as the 0.034 impact described above is equal to 6% of the average degree of business cycle synchronization in the whole sample. Clearly, such an impact would be more important for the regions which are currently less synchronized (such as the Darmstadt region in Germany and the Slaskie region in Poland, whose cycle synchronization in the sample is equal to 0.00002) than for those whose cycles already co-move significantly.

Also in line with existing evidence, the coefficient associated with sectorial specialization is estimated to be negative and statistically significant (at the 1% level). This indicates that dissimilarity of the economic structures is associated with lower correlations of business cycles. In particular, the point estimates indicate that when S 1,ij doubles, the correlation of bilateral regional cycles decreases by 0.063. This amounts to almost 11% of the average degree of cycle synchronization in our sample, again highlighting the economic meaningfulness of our econometric results.

As for the controls included in Eq. (1), it appears that greater financial integration fosters correlations of business cycles, confirming recent literature results (see, among others, Montinari and Stracca 2015; Keil and Sachs 2014; Jansen and Stokman 2011). The monetary integration dummies related to the euro peg are all positive. This suggests that, all else being equal, the GDPs of regions in countries outside the euro area or whose currency is not pegged to the euro co-move less than those of regional pairs whose currency is the euro or fixed to the euro, as well as those of regional pairs in which just one is in the euro area or whose currency is pegged to the euro and the other is not (in line with Frankel and Rose 1998).

Turning to Eq. (2), with trade intensity as the dependent variable, results confirm the roles played by the well-established gravity variables in determining bilateral trade flows. Distance has the expected negative sign, whereas border, language, the product of regional GPDs and the product of their populations are all associated with positive and statistically significant coefficients. The negative (and significant at the 1% level) coefficient of S 1 captures the effect of structural dissimilarities on intra-industry trade.

In line with Imbs (2004), the estimated γ 1 coefficient of Eq. (3) shows that higher trade intensity leads regions to become more similar, possibly showing that trade is acting as a vehicle of knowledge transfer, inducing regions to specialize in similar industries (i.e. learning by imitating). Financial integration (measured by ΔNFA) has the predicted effect on specialization (documented, among others, by Kalemli-Ozcan et al. 2003, and Imbs 2004) as predicted by the new economic geography approach: more financially integrated economies tend to choose different specialization patterns. Also consistent with previous studies, pairs of rich regions (signalled by high values of the product of GDP per capita, GDP_pc) have lower values of specialization, whereas pairs of regions at different stages of development (captured by the gap between GDPs, ΔGDP) tend to have more different economic structures. Finally, our results show that pairs of bigger regions (as measured by the product of their geographical areas, Area) are associated with more dissimilar economic structures.

It is worth commenting on how simultaneity and endogeneity affect the results of Eq. (1) reported in Table 3, something that can be gauged by looking at the results in the estimated coefficients across the three estimators that we have used. Overall, with the exception of small changes in the magnitude of the point estimates, results are comfortingly consistent. The 3SLS estimation yields a higher point estimate of the trade coefficient α 1, implying that if trade intensity doubles, business cycle correlation increases by 0.041. This is indeed what is found by both Frankel and Romer (1999) and Imbs (2004).

This result reveals that instrumenting trade intensity with gravity variables attenuates a downward endogeneity bias. Similarly, when instrumenting specialization with financial integration and variables accounting for the stages of diversification, we obtain a higher point estimate of α 2, suggesting that the correlation of bilateral regional cycles decreases by 0.090 as sectorial dissimilarity doubles. These are crucial results in terms of policy implications related to the EMU and the European Commission’s policies targeting regional development. As we argue in detail in our concluding discussion in Sect. 5, regional place-based policies promoting specialization may decouple regional cycles, while market integration policies would have the opposite effect.

4.2 Beyond the Baseline: Indirect Effects and Transmission Channels

Our empirical strategy makes it possible to disentangle the direct and indirect effects of both trade and specialization on business cycle synchronization by utilising some further computations. In Sect. 4.1 we presented the direct effects of trade intensity and specialization; in this section, we report their indirect effects and further investigate the channels behind the direct effects captured by the estimated α 1 and α 2 coefficients. Following the structure proposed by Imbs (2004), Part A of Table 4 below illustrates how to compute such effects, whereas Part B reports the estimated values as implied by the 3SLS estimates in the last column of Table 3.

As stated previously, the indirect (via trade) effect of specialization on business cycle co-movement can be captured by the α 1 β 1 interaction. It can be further argued that α 1 β 1 is a part of the total direct effect of trade on business cycle synchronization. As β 1 captures the extent to which trade between European regions is due to similarities in their respective economic structures, the α 1 β 1 interaction can also be interpreted as a measure of how intra-industry trade directly affects cycle synchronization. Then, α 1 β 2 can be seen as the direct effect of Ricardian (inter-industry) trade on synchronization.

The numbers contained in Part B of Table 4 show that the positive direct effect of trade on cycle synchronization can be mainly attributed to intra-industry trade (−0.0818), with inter-industry trade (i.e. trade intensity explained by the gravity variables rather than by specialization) accounting for a smaller portion (0.0023).Footnote 9 This is not surprising given that regions in developed countries tend to trade more intra-industry than inter-industry. This result is in line with what was found by Imbs (2004) using a country-level dataset. The immediate policy implication is that regional cycle synchronization may be positively affected by economic integration policies aimed at improving access to local markets and firm internationalisation, more than by measures aiming for instance at cross-country and cross-region division of labour or value-chain creation.

Similarly, it is possible to further explore the direct, and negative, effect of specialization on business cycle synchronization. This effect can be induced either by trade flows (α 2 γ 1, which also gauges the indirect effect—via specialization—of trade on cycle synchronization), by financial integration (α 2 γ 2), or by the level of development and diversification reached by the regions’ pairs (α 2 γ 3).

The numbers reported in Part B of Table 4 also show that the stages of development play a prominent role (0.0296) in explaining the negative effect of specialization on cycle synchronization. From a policy point of view, fostering convergence of regional economic fundamentals appears to be a crucial factor for increasing business cycle synchronization. Regional trade intensity also emerges as a relevant component (0.0128), whereas financial integration seems to play only a minor role (−0.0018), in contrast to country-level analyses where financial integration is found to be the most relevant component after the stages of development (Imbs 2004).

The additional estimates, the results of which are contained in the “Appendix”, demonstrate the robustness of our findings. In a nutshell, the results hold up: (1) with alternative series to measure both trade intensity and sectorial specialization (T 2,ij and S 2,ij ); (2) when applying the Fisher transformation to the dependent variable which is otherwise bounded between −1 and 1; (3) when using an alternative filter to extract the cyclical component of real GDP (the Baxter-King rather than the Hodrick-Prescott one); (4) when replacing the financial integration variable with its regional counterpart; (5) in panel estimates that fully exploit the time dimension of the data spanning from 2000 to 2010. Please see the “Appendix” for further details on those robustness checks.

5 Concluding Discussion

Understanding the complex relationship between the regional and the supranational dimensions of economic policy in Europe is crucial for establishing a form of economic governance capable of exploiting the advantages of both monetary integration and agglomeration economies. Our paper contributes to this research topic by identifying the factors that influence regional business cycle synchronization, including in light of the influence of regional and macroeconomic policies.

We find that trade integration has a positive impact on business cycle co-movement, whereas dissimilarity of regional economic structures has a negative effect. According to our estimates, doubling bilateral regional trade leads real GDP correlation to rise by between 0.034 and 0.041. Doubling the index of economic structure dissimilarity makes the correlation of bilateral regional cycles decrease by between 0.063 and 0.098. Moreover, it appears that the positive direct effect of trade on cycle synchronization is mostly driven by intra-industry trade, while the impact of specialization works mainly through differences in the regional stages of development.

These findings bear interesting policy implications for European economic policy. With respect to regional specialization, it is worth recalling that the latest European Cohesion policy is inspired by the idea that each region should pursue economic prosperity based on its distinctive assets and by developing its own specialization profile with respect to the other European regions (Foray and Van Ark 2007; Barca 2009; Foray et al. 2009, 2011). The notion of smart specialisation guides investment in research and innovation and aims at constructing regional “competitive advantages” by exploring and discovering region-specific innovation opportunities around which to build a critical mass of activities.

Specialization and differentiation of economic structures may indeed foster competitiveness and increase resilience to asymmetric shocks at the aggregate pan-European level. However, according to our empirical results, a strict interpretation of those policies promoting growth via higher regional specialization may also lead to less synchronized regional cycles. In the absence of effective supranational compensatory mechanisms (Furceri and Zdzienicka 2013), this could in turn weaken consensus on the monetary policy stance within the currency union. Ultimately, this would reduce the effectiveness of the common monetary policy [Carlino and Defina (1998) warned against such a possibility with a study on monetary policy and regional specialization].

On the other hand, the fact that differences in the stages of development of the regional economies are a key channel behind the decoupling effect of specialization on business cycles highlights the importance of the convergence-fostering objective of Cohesion policies, especially for less developed regions.

As regards economic integration via interregional trade linkages, our results support the idea that pan-European policies aimed at fostering market integration can indeed favour business cycles’ convergence. Moreover, the evidence we found on the prevailing importance of intra-industry trade calls for the implementation of general policies aimed at improving the functioning of the European single market for goods and services. For instance, one such policy could enhance the common regulatory framework by supporting factor mobility. This should be accompanied by encouraging competition in national and regional production systems in the European arena, for example by supporting firms’ internationalization and access to local markets.

Whether the specialization effect or the trade integration effect will prevail is a matter for further empirical investigation which constitutes an exciting research agenda. Our paper has provided novel evidence of the potential tension existing between different levels of European economic governance We argue that European policymakers should adopt an analytical approach integrating the regional and pan-European perspectives, and paying special attention to the trade-offs and possible complementarities existing between the different levels and objectives of European policies. The dynamics arising from such complex interactions should be adequately monitored.

Notes

We concentrate on cross-sectional evidence and we use panel estimates as a robustness check (see Sect. 4.2 and the “Appendix”). Most of the existing empirical literature on cycle synchronization is indeed cross-sectional, and 10 years is generally considered a sufficient time span to compute meaningful real GDP correlations.

Recently there has been a growing interest in studying further the role of financial integration in shaping business cycle co-movement, as noted in the literature review above. However, due to the lack of bilateral financial integration data among regions, we treat the financial integration variable as exogenous in the model. As part of the robustness checks in Sect. 5 we construct and employ a measure of financial integration at regional level, again as an exogenous control.

The other filter routinely used in the literature is the band pass filter by Baxter and King. However, being a double filter, the BK filter is more appropriate for quarterly data. Nevertheless, in the robustness analysis we show that our results remain unchanged when the cyclical component is obtained using the BK filter.

The use of a broad classification of sectors is employed, among others, by Clark and van Wincoop (2001).

Given that the sample period goes from 2000 to 2010, the regions of 12 countries are considered to be part of the euro area (Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, Netherlands, Portugal and Spain) and the regions of 5 countries are considered to be pegged to the euro (Denmark, Estonia, Lithuania, Latvia and Slovenia).

The distance measures were calculated by the authors using the STATA commands geocode3 and traveltime3 which calculate geographical distances by using latitude and longitude coordinates obtained from Google Maps and Yahoo! Maps, see Ozimek and Miles (2011) for more details.

Given the lin-log specification of the model, this number results from the multiplication of the T 1 coefficient by the logarithm of 2.

The gravity-induced component of trade is obtained with the following additional regression: first, a gravity model is estimated with T 1,ji as the dependent variable. Second, the trade fitted value just obtained in Eq. (1) estimated as part of a 2SLS system also involving Eq. (3) is used in order to control for the endogeneity of sectorial specialization. A similar procedure is used for the stages of development's effects of specialization. p values for the joint significance of each coefficient's product (obtained with Sobel tests) are reported in brackets.

Results are available upon request.

References

Ahner, D., & Landabaso, M. (2011). Regional policies in times of austerity. European Review of Industrial Economics and Policy, 2.

Anagnastou, A., Panteladis, L., & Tsiapa, M. (2015). Disentangling different patterns of business cycle synchronicity in the EU regions. Empirica 42(3), 615–641.

Barca, F. (2009). An agenda for a reformed cohesion policy: A place-based approach to meeting European Union challenges and expectations. Independent Report prepared at the request of Danuta Hübner, Commissioner for Regional Policy. Brussels.

Barca, F., McCann, P., & Rodríguez-Pose, A. (2012). The case for regional development intervention: Place-based versus place-neutral approaches. Journal of Regional Science, 52(1), 134–152.

Basile, R., De Nardis, S., & Pappalardo, C. (2014). Firm heterogeneity and regional business cycles differentials. Journal of Economic Geography, 14(6), 1087–1115.

Basile, R., & Girardi, A. (2010). Specialization and risk sharing in European regions. Journal of Economic Geography, 10(5), 645–659.

Baxter, M., & Kouparitsas, M. A. (2005). Determinants of business cycle comovement: A robust analysis. Journal of Monetary Economics, 52, 113–157.

Belke, A., & Heine, J. A. (2006). Specialization patterns and the synchronicity of regional employment cycles in Europe. International Economics and Economic Policy, 3(2), 91–104.

Busl, C., & Kappler, M. (2013). Does foreign direct investment synchronize business cycles? Results from a panel approach. WWWforEurope working paper no. 23.

Calderón, C., Chong, A., & Stein, E. (2007). Trade intensity and business cycle synchronization: Are developing countries any different? Journal of International Economics, 71, 2–21.

Carlino, G., & Defina, R. (1998). The differential regional effects of monetary policy. The Review of Economics and Statistics, 80(4), 572–587.

Clark, T. E., & Van Wincoop, E. (2001). Borders and business cycles. Journal of International Economics, 55(1), 59–85.

Davis, J. S. (2014). Financial integration and international business cycle co-movement. Journal of Monetary Economics, 64, 99–111.

De Haan, J., Inklaar, R., & Jong-A-Pin, R. (2008). Will business cycles in the euro area converge? A critical survey of empirical research. Journal of Economic Surveys, 22(2), 234–273.

Fatás, A. (1997). EMU: Countries or regions? Lessons from the EMS experience. European Economic Review, 41(3), 743–751.

Fingleton, B., Garretsen, H., & Martin, R. (2015). Shocking aspects of monetary union: The vulnerability of regions in Euroland. Journal of Economic Geography. doi:10.1093/jeg/lbu055.

Foray, D., David, P. A., & Hall, B. (2009). Smart specialisation—The concept. Knowledge economists Policy Brief No. 9. European Commission, Expert Group "Knowledge for Growth".

Foray, D., David, P. A., & Hall, B. (2011). Smart specialisation: From academic idea to political instrument, the surprising career of a concept and the difficulties involved in its implementation. MTEI working paper 2011-001. École Polytechnique Fédérale de Lausanne.

Foray, D., & Van Ark, B. (2007). Smart specialization in a truly integrated research area is the key to attracting more R&D to Europe. Knowledge economists Policy Brief No. 1. European Commission, Expert Group "Knowledge for Growth".

Frankel, J. A., & Romer, D. (1999). Does trade cause growth? The American Economic Review, 89(3), 379–399.

Frankel, J. A., & Rose, A. K. (1998). The endogeneity of the optimum currency area criteria. The Economic Journal, 108(449), 1009–1025.

Furceri, D., & Zdzienicka, A. (2013). The Euro area crisis: Need for a supranational fiscal risk sharing mechanism? IMF working paper. WP/13/198. September 2013.

Gianelle, C., González, I., Goenaga, X., & Thissen, M. (2014). Smart specialisation in the tangled web of European inter-regional trade. European Journal of Innovation Management, 17(4), 472–491.

Giannone, D., Lenza, M., & Reichlin, L. (2010). Business cycles in the Euro Area, chapter 4. In A. Alesina & F. Giavazzi (Eds.), Europe and the Euro (p. 141). Chicago: The University of Chicago Press, National Bureau of Economic Research.

Imbs, J. (2004). Trade, finance, specialization and synchronization. Review of Economics and Statistics, 86(3), 723–734.

Imbs, J., & Wacziarg, R. (2003). Stages of diversification. The American Economic Review, 93(1), 63–86.

IMF. (2013a). Dancing together? Spillovers, common shocks, and the role of financial and trade linkages, chapter 3. World economic outlook, pp 81–112

IMF. (2013b). The Yin and Yang of capital flow management: Balancing capital inflows with capital outflows, chapter 4. World economic outlook, pp 113–133

Inklaar, R., Jong-A-Pin, R., & De Haan, J. (2008). Trade and business cycle synchronization in OECD countries—A re-examination. European Economic Review, 52, 646–666.

Jansen, J., & Stokman, A. (2011). International business cycle comovement: Trade and foreign direct investment. DNB Working Papers No. 319, Netherlands Central Bank, Research Department.

Kalemli-Ozcan, S., Papaioannou, E., & Perri, F. (2013a). Global banks and Crisis Transmission. Journal of International Economics, 89, 495–510.

Kalemli-Ozcan, S., Papaioannou, E., & Peydró, J. L. (2013b). Financial regulation, financial globalization, and the synchronization of economic activity. The Journal of Finance, 68(3), 1179–1228.

Kalemli-Ozcan, S., Sørensen, B. E., & Yosha, O. (2003). Risk sharing and industrial specialization: Regional and international evidence. American Economic Review, 93(3), 903–918.

Keil, J., & Sachs, A. (2014). Determinants of business cycle synchronization. In M. Kappler & A. Sachs (Eds.), Business cycle Synchronisation and Economic Integration: New Evidence from the EU (pp. 95–148). Germany: ZEW Economic Studies, Mannheim.

Kose, M. A., Prasad, E. S., & Terrones, M. E. (2003). How does globalization affect the synchronization of business cycles? American Economic Review, 93(2), 57–62.

Kose, M. A., & Yi, K. M. (2006). Can the standard international business cycle model explain the relation between trade and comovement? Journal of International Economics, 68(2), 267–295.

Lane, P., & Milesi-Ferretti, G. M. (2011). Cross-border investment in small international financial centres. International Finance, 14(2), 301–330.

Marino, F. (2013). Business cycle synchronization across regions in the EU12: A structural-dynamic factor approach. New York: Mimeo.

Martin, R. (2001). EMU versus the regions? Regional convergence and divergence in Euroland. Journal of Economic Geography, 1(1), 51–80.

Montinari, L., & Stracca, L. (2015). Trade, finance or policies: What drives the cross-border spill-over of business cycles? ECB working paper (forthcoming).

Montoya, L. A., & de Haan, J. (2008). Regional business cycle synchronization in Europe? International Economics and Economic Policy, 5(1–2), 123–137.

OECD. (2009a). The fiscal autonomy of sub-central governments: An update. Technical Report 9, OECD Publishing.

OECD. (2009b). TDPC meeting at ministerial level (31 March 2009). Policy report, GOV/TDPC/MIN(2009)1.

Ozimek, A., & Miles, D. (2011). Stata utilities for geocoding and generating travel time and travel distance information. Stata Journal, 11(1), 106–119.

Siedschlag, I. (2010). Patterns and determinants of business cycle synchronization in the enlarged European Economic and Monetary Union. Eastern Journal of European Studies, 1(1), 21–44.

Siedschlag, I., & Tondl, G. (2011). Regional output growth synchronization with the Euro Area. Empirica, 38, 203–221.

Simini, F., González, M. C., Maritan, A., & Barabási, A. (2012). A universal model for mobility and migration patterns. Nature, 484, 96–100.

Tavlas, G. S. (2009). The benefits and costs of monetary union in Southern Africa: A critical survey of the literature. Journal of Economic Surveys, 23(1), 1–43.

Thissen, M., Diodato, D., & Van Oort, F. G. (2013a). Integrated regional Europe: European regional trade flows in 2000. Working Paper No. 1035. PBL Netherlands Environmental Assessment Agency. The Hague. 20 June.

Thissen, M., & Gianelle, C. (2014). S3 Inter-regional trade and competition tool. Accessed February 12, 2015, http://s3platform.jrc.ec.europa.eu/s3-trade-tool

Thissen, M., Van Oort, F. G., Diodato, D., & Ruijs, A. (2013b). Regional competitiveness and smart specialization in Europe. Place-based development in international economic networks. Cheltenham: Edward Elgar.

Acknowledgments

The authors would like to thank Francesco di Comite, Dimitrios Kyriakou, Diego Martínez López, Jean Imbs, Mark Thissen, Iulia Siedschlag, Livio Stracca, and the participants in the 55th ERSA congress in Lisbon (August 2015) for helpful comments and feedback on previous versions of this paper. Special thanks are due to the Editor and two anonymous referees for insightful suggestions, and to Anna Atkinson for the language editing. The usual disclaimer applies.

Author information

Authors and Affiliations

Corresponding author

Additional information

Disclaimer The views expressed are purely those of the authors and may not in any circumstances be regarded as stating an official position of the European Commission.

Appendix

Appendix

This appendix presents the various robustness checks performed to support the empirical analysis reported in the paper. First, we employed alternative series to measure both trade intensity and sectorial specialization. Tables 5, 6 and 7 report the OLS, SUR, and 3SLS estimates of the system when using T 1,ij and S 2,ij , T 2,ij and S 1,ij , and T 2,ij and S 2,ij , respectively. All the findings reported above are confirmed by these additional estimations, with mostly minor changes in the magnitudes of the estimated coefficients.

Second, we checked the soundness of our estimates in relation to the nature of the dependent variable. The correlation of the cyclical component of real GDP being bounded between −1 and 1, while the explanatory variables are continuous variables, we applied the Fisher transformation to normalise the distribution of the former and eliminate a possible source of bias in the estimated parameters. Column (1) of Table 8 shows the 3SLS results of our baseline specification (T 1,ij and S 1,ij ) where the dependent variable has been Fisher-transformed. The estimations show that our main results remain unchanged (the only notable change is in the europeg_non-europeg dummy whose coefficient becomes negative).

Third, we checked the sensitivity of our results to the choice of GDP filter and re-estimated the baseline model, extracting the cyclical components of real GDP using the Baxter-King filter rather than the Hodrick-Prescott one. Column (2) of Table 8 shows that all our main results are confirmed, although the europeg_europeg coefficient becomes statistically not significant from zero at standard levels.

Fourth, as anticipated in Sect. 3.2, we replace the financial integration variable included as a control in Eq. (1) with its regional counterpart. Column (3) of Table 8 reports the estimated coefficients of the baseline specification of the system of Eqs. (1), (2) and (3) where the country-level financial integration variable computed using FDI (FDI) is substituted by its regional version (FDI_reg) calculated using information on the number of multinationals per region. Once again, all our main findings are confirmed by these additional estimates, the main difference being the magnitude of the coefficients associated with the financial integration variable itself (its effect on business cycle co-movement is confirmed to be positive as in the baseline specification). We read these results as reassuring in terms of robustness, but we refrain from drawing additional insights due to the demanding assumptions behind the construction of the FDI_reg variable discussed previously.

Furthermore, our main results still hold when including regional dummies and when excluding from the sample the UK regions which are those with the highest level of GDP co-movement in the sample.Footnote 10

Finally, we exploited the time dimension of the data (spanning from 2000 to 2010) to carry out panel estimations of the empirical model formed by Eqs. (1), (2) and (3). We see this step of the analysis as a robustness check because there is a significant change with respect to the dependent variable of Eq. (1), which in a panel context can only be considered a proxy for business cycle synchronization. In the panel model, the dependent variable of Eq. (1) is constructed as the absolute difference between two regions’ real GDP growth rates.Footnote 11 On the other hand, the advantage of panel estimates lies in the possibility to simultaneously include year dummies to control for events common to all regions and changing over time, country-pair dummies to control for unobserved country-pairwise heterogeneity, and regional time-invariant regressors. The panel results (reported in column (4) of Table 8) confirm once again our main findings: all variables have the sign expected and remain significant at the 1% level (the only exception being the monetary integration variables whose coefficient becomes negative and the europeg_non-europeg dummy whose effect is now significant at the 10% level only). Keeping in mind the important caveats differentiating the cross-sectional from the panel framework, the impact of both trade and specialization on business cycle co-movements is confirmed in terms of sign, and appears to be smaller in terms of magnitude (the latter finding is in line with other studies using panel methods, see for example the working paper version of Imbs (2004)).

Rights and permissions

Open Access This article is distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution, and reproduction in any medium, provided you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made.

About this article

Cite this article

Gianelle, C., Montinari, L. & Salotti, S. Interregional Trade, Specialization, and the Business Cycle: Policy Implications for the EMU. J Bus Cycle Res 13, 1–27 (2017). https://doi.org/10.1007/s41549-017-0012-y

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s41549-017-0012-y

Keywords

- European regions

- Business cycle synchronization

- Trade

- Sectorial specialization

- Economic and Monetary Union