Abstract

The effect of volatility on an economy has been widely discussed in previous studies, both theoretically and empirically. However, few studies have considered the effect of volatility on electricity demand. The purpose of this study is to analyze the effect of oil price volatility on electricity demand in Turkey. Annual balanced panel data on provinces of Turkey covering two different time periods, 1990–2001 and 2004–2014, are used. In this context, a dynamic panel data model is estimated using the system generalized method of moments estimation approach. The results show negative short-run effect of oil price volatility on electricity demand for the period 2004–2014. Moreover, although demand for electricity is found to be price inelastic during the period between 1990 and 2001, the results show that it is elastic during the period 2004–2014. This could be due to the electricity market liberalization policies implemented through the enactment of the Electricity Market Law in 2001. In conclusion, to minimize the costs associated with volatility, policy-makers should focus on better management of external supply and demand shocks by fiscal and monetary authorities, and on dissemination of energy efficiency and conservation applications.

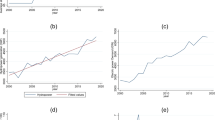

Source: Author’s representation based on data obtained from the Transmission Company of Turkey

Source: Author’s representation based on data obtained from the Statistical Institute of Turkey (TURKSTAT)

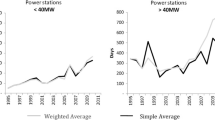

Source: Author’s representation based on data obtained from the Transmission Company of Turkey

Source: Author’s own elaboration using QGIS 2.10.1

Source: Author’s own elaboration

Similar content being viewed by others

Notes

Readers are invited to refer to the author’s Ph.D. thesis for a detailed literature review.

The conditional variance of the crude oil price growth is calculated by estimating the ARMA(8, 1)- GARCH(2, 2) model under the generalized error distribution assumption using the daily spot crude oil price (Cushing, OK WTI Spot Price FOB, $/barrel) taken from the U.S. Energy Information Administration (EIA) database. Estimation results are available upon request.

Due to space limitations, the estimation results are not presented here, but are available upon request. The lower and upper bounds for good estimates were found to be 0.623949 and 0.944886, respectively.

Due to space limitations, estimation results are not presented, but are available upon request. The lower and upper bounds for good estimates were found to be 0.6478829 and 0.8653593, respectively.

References

Akarsu, G. (2017). Analysis of regional electricity demand for Turkey. Regional Studies, Regional Science, 4(1), 32–41. doi:10.1080/21681376.2017.1286231.

Amusa, H., Amusa, K., & Mabugu, R. (2009). Aggregate demand for electricity in South Africa: An analysis using the bounds testing approach to cointegration. Energy Policy, 37(10), 4167–4175. doi:10.1016/j.enpol.2009.05.016.

Andrews, D. W. K., & Lu, B. (2001). Consistent model and moment selection procedures for GMM estimation with application to dynamic panel data models. Journal of Econometrics, 101(1), 123–164.

Arellano, M., & Bond, S. (1991). Some tests of specification for panel data—Monte-Carlo evidence and an application to employment equations. Review of Economic Studies, 58(2), 277–297.

Arellano, M., & Bover, O. (1995). Another look at the instrumental variable estimation of error-components models. Journal of Econometrics, 68(1), 29–51.

Arize, A. C. (2000). U.S. petroleum consumption behavior and oil price uncertainty: Tests of cointegration and parameter instability. Atlantic Economic Journal, 28(4), 463–477. doi:10.1007/BF02298398.

Atakhanova, Z., & Howie, P. (2007). Electricity demand in Kazakhstan. Energy Policy, 35(7), 3729–3743. doi:10.1016/j.enpol.2007.01.005.

Bahmani-Oskooee, M., & Xi, D. (2011-2012). Exchange rate volatility and domestic consumption: A multicountry analysis. Journal of Post Keynesian Economics, 34(2), 319–330.

Baltagi, B. H. (2008). Econometric analysis of panel data. West Sussex: Wiley.

Berument, M. H., Dincer, N. N., & Mustafaoglu, Z. (2012). Effects of growth volatility on economic performance—Empirical evidence from Turkey. European Journal of Operational Research, 217(2), 351–356.

Bloom, N. (2009). The impact of uncertainty shocks. Econometrica, 77(3), 623–685.

Blundell, R., & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87(1), 115–143.

Bohi, D. R., & Zimmerman, M. B. (1984). An update on econometric studies of energy demand behavior. Annual Review of Energy, 9, 105–154.

Bond, S. R. (2002). Dynamic panel data models: A guide to micro data methods and practice. London: Institute for Fiscal Studies.

Box, G., & Jenkins, G. (1970). Time series analysis: Forecasting and control. San Francisco: Holden-Day.

Carlos, A. P., Notini, H., & Maciel, L. F. (2009). Brazilian electricity demand estimation: What has changed after the rationing in 2001? An application of time varying parameter error correction model. Paper presented at the 31th Meeting of the Brazilian Econometric Society, Foz do Iguaçu, Paraná, 9-11 December.

Chakir, R., Bousquet, A., & Ladoux, N. (2004). Modeling corner solutions with panel data: Application to the industrial energy demand in France. Empirical Economics, 29(1), 193–208. doi:10.1007/s00181-003-0194-0.

Chen, S.-S., & Hsu, K.-W. (2012). Reverse globalization: Does high oil price volatility discourage international trade? Energy Economics, 34(5), 1634–1643. doi:10.1016/j.eneco.2012.01.005.

Chiou-Wei, S.-Z., Zhu, Z., Chen, S.-H., & Hsueh, S.-P. (2016). Controlling for relevant variables: Energy consumption and economic growth nexus revisited in an EGARCH-M (Exponential GARCH-in-Mean) model. Energy, 109, 391–399. doi:10.1016/j.energy.2016.04.068.

Cologni, A., & Manera, M. (2009). The asymmetric effects of oil shocks on output growth: A Markov-Switching analysis for the G-7 countries. Economic Modelling, 26(1), 1–29.

Dahl, C. A. (2011). A global survey of electricity demand elasticities. Paper presented at the 34th IAEE International Conference: Institutions, Efficiency and Evolving Energy Technologies, Sweden.

Diabi, A. (1998). The demand for electric energy in Saudi Arabia: An empirical investigation. OPEC Review, 22(1), 13–29. doi:10.1111/1468-0076.00039.

Elder, J., & Serletis, A. (2010). Oil price uncertainty. Journal of Money, Credit and Banking, 42(6), 1137–1159.

Fisher, F. M., Fox-Penner, P. S., Greenwood, J. E., Moss, W. G., & Phillips, A. (1992). Due diligence and the demand for electricity: A cautionary tale. Review of Industrial Organization, 7, 117–149.

Grier, K. B., & Perry, M. J. (2000). The effects of real and nominal uncertainty on inflation and output growth: Some GARCH-M evidence. Journal of Applied Econometrics, 15(1), 45–58. doi:10.1002/(SICI)1099-1255(200001/02)15:1<45:AID-JAE542>3.0.CO;2-K.

Guo, H., & Kliesen, K. L. (2005). Oil price volatility and U.S. macroeconomic activity. Federal Reserve Bank of St. Louis Review, 87(6), 669–683.

Harris, M., Matyas, L., & Sevestre, P. (2008). Dynamic models for short panels. In L. Mátyás & P. Sevestre (Eds.), Econometrics of panel data (3rd ed., pp. 249–278). Berlin: Springer.

Henriques, I., & Sadorsky, P. (2011). The effect of oil price volatility on strategic investment. Energy Economics, 33(1), 79–87. doi:10.1016/j.eneco.2010.09.001.

Heshmati, A. (2012). Survey of models on demand, customer base-line and demand response and their relationships in the power market. IZA Discussion paper No. 6637.

Holtedahl, P., & Joutz, F. L. (2004). Residential electricity demand in Taiwan. Energy Economics, 26(2), 201–224. doi:10.1016/j.eneco.2003.11.001.

Houthakker, H. S. (1951). Some calculations of electricity consumption in Great Britain. Journal of the Royal Statistical Society, 114, 351–371.

Hsiao, C. (2003). Analysis of panel data. Cambridge: Cambridge University Press.

Hsiao, C., Mountain, D. C., Chan, M. W. L., & Tsui, K. Y. (1989). Modeling Ontario regional electricity system demand using a mixed fixed and random coefficients approach. Regional Science and Urban Economics, 19(4), 565–587. doi:10.1016/0166-0462(89)90020-3.

IEA. (2011). World energy outlook 2011. Paris: IEA.

Khanna, M., & Rao, N. D. (2009). Supply and demand of electricity in the developing world. Annual Review of Resource Economics, 1, 567–595.

Kirschen, D. S. (2003). Demand-side view of electricity markets. IEEE Transactions on Power Systems, 18(2), 520–527. doi:10.1109/TPWRS.2003.810692.

Kuper, G. H., & van Soest, D. P. (2006). Does oil price uncertainty affect energy use? Energy Journal, 27(1), 55–78.

Ma, H. Y., Oxley, L., Gibson, J., & Kim, B. (2008). China’s energy economy: Technical change, factor demand and interfactor/interfuel substitution. Energy Economics, 30(5), 2167–2183.

Madlener, R. (1996). Econometric analysis of residential energy demand: A survey. Journal of Energy Literature, 2(2), 3–32.

Murray, M. P., Spann, R., Pulley, L., & Beauvais, E. (1978). The demand for electricity in Virginia. The Review of Economics and Statistics, 60(4), 585–600. doi:10.2307/1924252.

Narayan, P. K., & Smyth, R. (2005). The residential demand for electricity in Australia: An application of the bounds testing approach to cointegration. Energy Policy, 33(4), 467–474.

Olsen, Ø., & Roland, K. (1988). Modeling demand for natural gas: A review of various approaches. Oslo, Kongsvinger: Central Bureau of Statistics of Norway.

Özer, M., & Türkyılmaz, S. (2005). Türkiye’de Enflasyon ile Enflasyon Belirsizliği Arasındaki İlişkinin Zaman Serisi Analizi [Time Series Analysis of the Relation between Inflation and Inflation Uncertainty in Turkey]. İktisat İşletme ve Finans Dergisi, 229, 93–104. doi:10.3848/iif.2005.229.6260.

Pesaran, M. H. (2004). General diagnostic tests for cross section dependence in panels. CESifo working paper No. 1229.

Plante, M., & Traum, N. (2012). Time-Varying oil price volatility and macroeconomic aggregates center for applied economics and policy research working paper No. 2012-002.

Pouris, A. (1987). The price elasticity of electricity demand in South-Africa. Applied Economics, 19(9), 1269–1277.

Pourshahabi, F., Sattari, Y., & Shirazi, A. (2012). Petroleum consumption—Oil price uncertainty nexus in OECD countries: Application of EGARCH models and panel cointegration. OPEC Energy Review, 36(2), 204–214. doi:10.1111/j.1753-0237.2011.00209.x.

Rzayeva, G. (2014). Natural gas in the Turkish domestic energy market: Policies and challenges. OIES Paper: NG 82. England: University of Oxford, Oxford Institute for Energy Studies.

TP (2016). Ham petrol ve doğal gaz sektör raporu Mayıs2016. Ankara: Türkiye Petrolleri.

Van Robays, I. (2016). Macroeconomic uncertainty and oil price volatility. Oxford Bulletin of Economics and Statistics, 78(5), 671–693.

Weiner, R. J. (2005). Speculation in international crises: Report from the Gulf. Journal of International Business Studies, 36(5), 576–587.

Weller, C., & Fields, W. (2011). Roller coaster economics: Why energy price volatility hurts families, businesses, and the economy. Challenge, 54(5), 99–117.

Windmeijer, F. (2005). A finite sample correction for the variance of linear efficient two-step GMM estimators. Journal of Econometrics, 126(1), 25–51.

Yépez-García, R. A., Johnson, T. M., & Andrés, L. A. (2011). Meeting the balance of electricity supply and demand in Latin America and the Caribbean (directions in development). Washington, D.C.: World Bank Publications.

Author information

Authors and Affiliations

Corresponding author

Additional information

This article is part of Ph.D. thesis of the author. I would like to thank to anonymous referees for their valuable comments.

Rights and permissions

About this article

Cite this article

Akarsu, G. Analyzing the impact of oil price volatility on electricity demand: the case of Turkey. Eurasian Econ Rev 7, 371–388 (2017). https://doi.org/10.1007/s40822-017-0079-8

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s40822-017-0079-8