Abstract

Choosing assets for their portfolios is a complex decision, and investors, endowed with limited information processing capacity are influenced by various psychological factors. One such factor is investors’ processing fluency with the firm’s stock. In this paper, we introduce the idea of congruent ticker symbol, defined as whether or not the firm’s ticker symbol is similar to its corporate name (e.g., DELL for Dell, Inc.) Further, we propose that a firm’s congruent ticker symbol, in conjunction with other firm characteristics, will increase investors’ processing fluency with its stock and, therefore, affect its intangible value. We consider the firm’s size, performance, advertising, and distribution presence as firm characteristics that will interact with congruent ticker symbol to affect its intangible value. Data from 181 publicly listed US retailers between 1994 and 2006 strongly support the hypotheses relating the contingent effects of congruent ticker symbols to intangible value. While, firms’ congruent ticker symbols do not independently increase their intangible values, they do so, in conjunction with their performance, advertising, and distribution presence. For marketing theory, congruent ticker symbols emerge as contingent intangible market-based assets that create enduring shareholder value with other firm characteristics. For managerial practice, the findings offer guidance on ticker symbol-naming strategies that can increase shareholder value.

Similar content being viewed by others

1 Introduction

When a public firm lists its stock on a stock exchange, it is assigned a ticker symbol which uniquely identifies its stock to investors (e.g., MO for Altria Inc. and IBM for IBM Corporation). Although, a ticker symbol should have no information content in an efficient market, CEOs appear to view congruent ticker symbols as instruments that increase shareholder value. Consider:

Owen Dukes, CEO of Propalms USA, Inc., which changed its ticker symbol from JLNY to PRPM on March 16, 2007: “The PRPM symbol makes much more sense for us and our potential investors. The symbol change is one of many steps moving forward to bring greater value to our shareholders. As the Propalms USA name grows in the business world, so, too will our presence in the investment community.”

Michael H. Tardugno, President and Chief Executive Officer of Celsion Corporation (CLN), which changed its ticker symbol to CLSN on July 14, 2008: “We are pleased to announce our new ticker symbol, one that we believe will improve our visibility with investors and more closely associate our company with the NASDAQ on which our shares have traded since February 2008. We continue to successfully execute on our strategy and our focus remains on building value for all shareholders.”

We propose that a firm’s congruent ticker symbol, which we define as whether or not its ticker symbol is similar to its name, has the potential to be value-relevant.Footnote 1 Examples of congruent ticker symbols include PALM (Palm One, Inc.) and MMM (3M Corporation), and incongruent ticker symbols include NLAI (Paragon Fund Inc.) and SVWN (Knova Software). We focus on ticker symbols managed by the firm’s finance executives and not directly under the purview of the firm’s marketing function. By studying the value relevance of ticker symbols aimed at investors, we adopt the perspective of “the investor community as a customer,” an idea that has not been explored in the marketing literature.

A study on the shareholder wealth effects of ticker symbols has high managerial relevance. While firms choose their ticker symbols at the time of their initial public offering (IPO), some firms do change their ticker symbols subsequently. For example, 480 firms, listed in US stock exchanges, changed their ticker symbol between January 2005 and August 2008. Pertinent to this study, 127 (25%) of the new ticker symbols were congruent after the change, compared to 78 (16%) ticker symbols before, a 50% increase in the incidence of congruent ticker symbols, suggesting that some firms consider congruent ticker symbols to be value-relevant.

What factors might motivate a firm’s choice of a congruent ticker symbol? From a communications perspective, investors can access information about firms with congruent ticker symbols more easily in the increasingly, cluttered information environment. As Richard Adamonis, a spokesperson for the New York Stock Exchange noted, “They [congruent ticker symbols] are easier to remember and can reinforce what a company stands for” (http://www.reuters.com/articleprint?articleid=USN1036624820070710).

If congruent ticker symbols are value-relevant, then firms with incongruent ticker symbols may be foregoing an opportunity to build shareholder wealth. However, changing ticker symbols is both costly and risky. Firms need to invest in the promotion of the new ticker symbol and risk being overlooked by potential investors, lowering the liquidity of their stocks [27]. Thus, insights on the value relevance of congruent ticker symbols will be useful to senior executives of publicly listed firms.

Non-informative, psychological factors influence investors’ decisions and stock returns [21]. One such psychological factor is processing fluency, the ease with which individuals process information about a stimulus [47]. Developments in the psychology of judgment indicate that, controlling for the stimuli’s contents, individuals’ processing fluency with stimuli increases the favorability of their evaluations of stimuli [37].

In this paper, we address the following questions: Are congruent ticker symbols value-relevant when investors have access to other diagnostic information about the firm? Does the value relevance of congruent ticker symbols vary across firms? If so, what firm characteristics affect this relationship?

To start with, various firm characteristics (e.g., business strategy, profile, and performance) influence the content of the associations of firm’s ticker symbols (e.g., the congruent ticker symbol, KMRT of Kmart Corporation, would have negative associations during Kmart Corporation’s bankruptcy proceedings). Thus, a priori, we do not expect that a firm’s congruent ticker symbol will, independently, influence its intangible value.

Applying contingency theory which proposes complementarities among firms’ characteristics on outcomes [19, 54], we propose interaction effects between a firm’s congruent ticker symbol and its other characteristics on its intangible value. For the contingency model, we identify four characteristics that we hypothesize will interact with a firm’s congruent ticker symbol to affect its intangible value: firm size and performance, and two marketing characteristics: advertising and distribution presence.

We test the hypotheses using a panel data of 181 publicly US listed retailers (1,415 firm years) between 1994 and 2006. Two factors motivate the choice of the US retailing industry as the empirical context. First, ticker symbol-naming strategies vary across retailers providing the variation necessary for the study. Second, most retailers follow corporate branding strategies, enabling a clean test of the effects of congruent ticker symbols.

We define a firm’s congruent ticker symbol as whether or not it is similar to its corporate name (e.g., AMES for Ames Department Stores, and TGT for Target Brands Inc.). We measure the firm’s intangible value by Tobin’s Q, a forward-looking, capital market-based measure [7]. We estimate the model using a random effects regression approach.

As expected, while firms’ congruent ticker symbols do not, independently, increase intangible value, their interaction effects with performance, advertising, and distribution presence increase intangible value. The model predicts a firm’s intangible value well, given its characteristics. Overall, the paper’s findings suggest that congruent ticker symbols are intangible market-based assets, for some, but not all firms.

2 Processing Fluency: an Overview

A key idea in the psychology literature is that in addition to the objective, descriptive content of a stimulus, psychological factors, unrelated to the stimulus content, affect individuals’ processing of a stimulus. Individuals’ processing of stimuli of similar content differ in speed [24] and ease, an idea termed as processing fluency [47, 51].

What factors influence processing fluency? One view [25] suggests that familiar material is easier to process than unfamiliar material, so that increased knowledge about a stimulus will increase individuals’ familiarity with it which, in turn, will increase their processing fluency. An alternative view [52] argues that information about a stimulus is easier to process when observed more frequently and for long rather than short durations. So, multiple exposures to a stimuli increase processing fluency [53].

Individuals evaluate fluent stimuli more positively, considering them to be more frequent [48], more true [36], and more likeable [37] than stimuli that are similar in content, but less fluent. Processing fluency is manifest as a hedonically positive experience which provides diagnostic information for evaluations of stimuli [50]. All things being equal, fluent stimuli are evaluated more favorably than [38] and preferred over less fluent stimuli [38, 41].

A processing fluency signal is most informative for evaluations when little diagnostic information is available about stimuli [38], and it is least informative when the stimuli are meaningful and personally relevant [10]. Moreover, while processing fluency may elicit an initial positive reaction to a stimulus, over time, the stimulus’ features are attended to and the stimulus will be re-evaluated [11]. Thus, subject to some boundary conditions, individuals’ evaluations of and preferences for stimuli are influenced not only by their evaluations of the stimuli’s objective contents but also by their fluency with them.

3 Processing Fluency and Investing

Investors endowed with limited information processing capacity and facing a complex decision-making task when choosing assets for their portfolios are influenced by psychological factors [21]. One such psychological factor is investors’ processing fluency with the firm’s stock, which enables the firm’s stock to stand out from the large number of stocks that they may be considering for investment decisions [1].

Behavioral finance provides evidence of the effects of processing fluency on investors’ behaviors. Investors buy and hold the stocks of firms with regional business presence with which they are familiar, and with which, they have greater processing fluency [49]. Customers of a Regional Bell Operating Company (RBOC) who live in its served area hold disproportionately more of its shares than of other RBOC’s [22]. Investors, who are more familiar with firms from their home country, buy more stock of firms from their country, than is optimal, despite the well-documented gains from international diversification in stock portfolios [13].

Stock returns of firms with simple symbols (e.g., Flinks) are higher than those of firms with complex ticker symbols (e.g., Aegeadux) [1]. Stocks of firms with pronounceable ticker symbols (e.g., KAR) outperformed those with unpronounceable ticker symbols (e.g., RDO) after 1 day of trading on the stock market. However, the effects of pronounceability of ticker symbols on stock returns disappear over the long term (a 14-year period), presumably, when other relevant information about firms is available to investors.

In summary, there is some evidence of the effects of processing fluency on investors’ behaviors. Specifically, investors’ processing fluency of ticker symbols affects firms’ stock returns when relevant, diagnostic information about the firm is not available to them. However, investors do have access to and actively process diagnostic information about the firms in their investment decisions. A related unexamined question is, what is the effect of ticker symbols on investors’ behaviors, when relevant firm information is available? Thus, we examine the effects of congruent ticker symbols, in conjunction with firm characteristics, on shareholder value.

4 Hypotheses

4.1 Definition

The Merriam-Webster dictionary defines “congruence” as the extent to which a stimulus is similar to a focal stimulus. Accordingly, we define a congruent ticker symbol as whether or not the firm’s ticker symbol is to the firm’s corporate name (the focal stimulus). Thus, we view congruent ticker symbol as a dichotomous construct—i.e., a ticker symbol is either congruent or incongruent. Examples of congruent ticker symbols in the US retailing industry include ANN (Ann Taylor Stores Corporation) and JCP (J. C. Penney Company Inc.) and examples of incongruent ticker symbols congruent include CTR (Cato Corporation) and JWN (Nordstrom Inc.). A congruent ticker symbol is distinct from a pronounceable ticker symbol, although some congruent ticker symbols (e.g., ANN of Ann Taylor Inc.) may be pronounceable. To illustrate, MSFT and ADBE are unpronounceable, yet congruent ticker symbols of Microsoft Inc. and Adobe Inc., respectively.

4.2 Hypotheses

Three key ideas underlie the hypotheses relating firms’ congruent ticker symbols to their intangible value. First, investment decisions are personally relevant decisions, so we anticipate that investors will be influenced by more than just their processing fluency with a firm’s stock. In addition, various firm characteristics (e.g., size, performance, and strategy) provide relevant diagnostic information to investors about its stock performance and its prospects, influencing their investment decisions. Thus, we do not anticipate a main effect of congruent ticker symbol on intangible value, a long-term stock performance metric.

Second, the contingency-based approach argues for complementarities between the elements of a firm’s resources and strategy on its performance [19, 54]. Accordingly, we propose that a firm’s congruent ticker symbol will interact with other diagnostic firm information (i.e., its characteristics) to jointly influence investors’ evaluation of its stock. Thus, we develop hypotheses of interaction effects between a firm’s characteristics and its congruent ticker symbol on intangible value.

We seek firm characteristics that satisfy two criteria: (1) that they affect investors’ knowledge of the firm’s business strategy and prospects, increasing their processing fluency with the firm’s stock, and/or (2) that they affect the firm’s future performance, providing investors diagnostic information about the firm’s prospects and therefore its shareholder value. Four firm characteristics satisfy these criteria: its size and performance, and two marketing characteristics, advertising and distribution presence, which we use to develop interaction effects with the firm’s congruent ticker symbol. We note that consistent with the dominant empirical tradition in finance on the effects of psychological factors on stock performance, we do not explicitly measure processing fluency, but argue for its effects on intangible value.

4.3 Congruent Ticker Symbol and Firm Size

Relative to small firms, large firms are seen as worthy of [40] and receive increased media attention [33] which increases investors’ knowledge of them. Large firms, relative to small firms have higher analysts’ following and information acquisition and positive analysts’ reports [3].

In addition, other arguments suggest a performance advantage to large firms. Several theoretical explanations including efficiency theory [14] and market power theory [39] suggest that increasing firm size confers the firm with future performance benefits. Increasing firm size provides scale economies, with attendant demand and supply side advantages including superior product quality and lower manufacturing costs [42]. With respect to stock returns, a firm’s size lowers its current stock returns and cost of capital and increases its market value [15].

When a large firm also has a congruent ticker symbol, the integration of the information about the firm’s size, with its attendant benefits on its future performance, and the increased information reporting on large firms by financial analysts and the media at large will not only increase investors’ processing fluency with the firm’s stock but will also cue its performance advantages arising from its size, raising investors’ expectations about its future cash flows and increasing its intangible value. Thus,

-

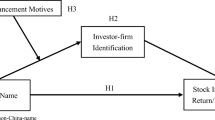

H1 The interaction between a firm’s congruent ticker symbol and its size will increase its intangible value.

4.4 Congruent Ticker Symbol and Firm Performance

Investors use firms’ performance as an indicator of their future performance in their investments decisions. Investors are enthusiastic about the prospects of firms that have performed well—“glamour stocks”, and prefer them, over ill-performing stocks, overpricing glamour stocks [28]. Indeed, they argue (p. 1,575) that “some individuals might just equate well-run firms with good investments, regardless of price.”

As with large firms, firms with superior performance are covered extensively by mass media and analyst community. The analysts’ primary responsibility is to write research reports that recommend stocks to customers. Analysts are under pressure to make buy versus sell recommendations, as a result of which they focus their information acquisition efforts on firms with superior performance, more likely to be “buy” targets. Thus, investors are very familiar with well-performing firms as these firms have greater analyst following and information acquisition [8].

We anticipate that the integration of the firm’s superior performance, a relevant, positive trait of the firm, and the increased information reporting on it, with its congruent ticker symbol, will increase investors’ processing fluency, causing them to assess the firm’s stock favorably, raising their expectations about its future cash flows and increasing its intangible value. Thus,

-

H2 The interaction between a firm’s congruent ticker symbol and its performance will increase its intangible value.

4.5 Congruent Ticker Symbol and Advertising

At a fundamental level, firms’ advertising informs their various stakeholders, including customers and investors, about their strategies, and the range and quality of offerings [30]. Advertising also plays an important informative role [4], informing its various stakeholders, including investors, about their products. The informative view suggests that advertised products (i.e., the firm’s stocks) are of high quality so that firms’ even seemingly uninformative advertising may provide an indirect signal that the quality of their products and stocks are high [45].

The persuasive view of advertising [46] holds that advertising affects demand by changing tastes and creating brand loyalty, so that advertised products face less elastic demand and deter market entry. Consistent with this view, the market-based assets theory [44] argues that advertising creates brands, which are intangible market-based assets that increase cash flows, and lower the risk of these cash flows increasing the firm’s shareholder value. Given the increasing attention to advertising-generated, intangible market-based assets in the accounting literature [2] and their inclusion as assets in financial statements in the UK and Australia [6], there is cognizance among investors that advertising creates intangible assets that are value-relevant. Not surprisingly, firms with increased product market advertising have more investors and better liquidity of their stock [18].

A recent study provides indirect support for a potential positive interaction effect between a firm’s congruent ticker symbol and its advertising on shareholder value. Positive abnormal returns accrue to readily identifiable firms (e.g., Pepsico), presumably, with high processing fluency, for broadcast advertising during the Super Bowl [16]. Thus, when a firm with a congruent ticker symbol also increases its advertising, investors’ processing fluency with the firm’s stock increases and the firm’s stock will also be imbued with positive associations, resultant from the multi-faceted benefits of advertising. As a result, investors will assess the firm’s stock favorably, raise their expectations of its future cash flows and increase its intangible value. Thus,

-

H3 The interaction between a firm’s congruent ticker symbol and its advertising will increase its intangible value.

4.6 Congruent Ticker Symbol and Distribution Presence

Distribution presence is the extent of the firm’s distribution coverage in the market. To start with, distribution presence is created by virtue of the firm’s investments in its distribution channels. A firm’s distribution presence increases first-hand awareness, trial and experience opportunities for both its customers and investors, who are also consumers of the firm’s stocks and products.

On the one hand, as with advertising, a firm’s increasing distribution presence should increase investors’ awareness of its products, and its strategies. Thus, when a firm with a congruent ticker symbol also has increasing distribution presence, investors’ processing fluency with the firm’s stock will increase. More distribution outlets may also signal to investors that the firm is on a trajectory of market growth, raising investors’ expectations of the firm’s future cash flows and increasing the demand for its stocks.

On the other hand, other developments in the psychology literature suggest a potential negative interaction effect between a firm’s congruent ticker symbol and increasing distribution presence on intangible value. There is a cascading effect of dissimilarity on judgments in multiple representations of a stimulus, so that once evidence of dissimilarity is encountered, subsequent information about the stimulus is more likely to be interpreted as further evidence of dissimilarity, lowering preference for it [31]. Unlike centralized advertising that is controlled from corporate headquarters, distribution is a decentralized operation, and investors are exposed to multiple representations of a firm’s distribution outlets. Given this background, increasing distribution poses challenges in managerial control, creating greater variability across distribution outlets. Hence, with a firm’s increasing distribution presence, investors’ average service quality experience with its outlets may decline and the variance may increase, creating dissimilarity cascades and providing negative information to investors.

Thus, when a firm with a congruent ticker symbol also has increasing distribution presence, although investors’ processing fluency with the firm’s stock will increase, investors may incorporate their negative assessments of the firm causing them to view the firm’s stock unfavorably, lowering their expectations about its future cash flow and decreasing its intangible value. Integrating this opposing evidence, we hypothesize opposing interaction effects between a firm’s congruent ticker symbol and its distribution presence on intangible value. Thus,

-

H4a/H4b The interaction between a firm’s congruent ticker symbol and its distribution presence will increase/decrease its intangible value.

4.7 Method

4.7.1 Data

We used data on publicly listed retailers spanning the two-digit Standard Industrial Classification (SIC) codes of 52 to 59, which includes building materials and garden supplies, general merchandise stores, automotive dealers and service stations, furniture and home furnishing stores, and miscellaneous retail stores. We excluded restaurant chains (two-digit code = 58) which have governance mechanisms (e.g., franchising) different from those in retailers.

We collected data on US retailers for the period 1994–2006 from various secondary sources including COMPUSTAT and annual reports. The final data set with all explanatory variables had data on 181 firms for 12 years resulting in 1,415 firm years. Some firms entered the data set after 1994 or exit before 2002, contributing fewer firm years. The average number of firm years is 7.82 (minimum = 1 year; maximum = 12 years).

4.7.2 Variables

We used Tobin’s Q as a measure of the firm’s intangible value. Specifically, we use the method of Chung and Pruitt [12] to calculate Tobin’s Q as follows: \( Q=\frac{\mathrm{MVE}+\mathrm{PS}+\mathrm{DEBT}}{\mathrm{TA}} \), where MVE is the closing price of shares at the end of the financial year × number of common shares outstanding, PS is the liquidation value of the firm’s outstanding preferred stock, DEBT is the sum of book value of inventories, long-term debt and current liabilities less current assets, and TA is the book value of total assets. We used the firm’s year-end stock price and number of shares to compute Tobin’s Q.

We measured the firm’s congruent ticker symbol by whether or not the firm’s ticker symbol cues its corporate name, which can happen in two ways: (1) the ticker symbol contains a part of the corporate name (e.g., ANN for Ann Taylor Stores Corporation) or (2) if the ticker symbol is a phonetic representation of the corporate name (LTD. for Limited Brands Inc). After being briefed on the coding task by one of the authors, two graduate students independently coded firms’ ticker symbols; 43% (n = 78) had congruent ticker symbols. Table 1 contains ten examples—five firms with and without congruent ticker symbol.

We measured the firm’s size by the natural logarithm of its total sales (DATA12 in COMPUSTAT). We measured the firm’s performance by its return on assets, the ratio of its net income (DATA172) to total assets (DATA6). The firm’s advertising was measured by its advertising expenditure (DATA45), and the firm’s distribution presence was measured by the total number of retail outlets, which we obtained from the annual reports.

We also included, in the model, two financial characteristics that affect intangible value. First, we included financial leverage, computed as the ratio of a firm’s long-term debt to its total assets [26]. Second, we included financial liquidity, measured as the ratio of a firm’s cash, marketable securities, notes receivable, and accounts receivables to its current liabilities [9]. Table 2 contains the descriptive statistics and the correlation matrix of the measures. We examined correlations between the explanatory variables and found them to be within acceptable limits (the highest correlation is 0.589 between advertising and its size), suggesting that multicollinearity may not be a problem.

4.7.3 Model

We estimate a random effects regression model that accounts for unobserved heterogeneity relating the interaction effects of the firm’s congruent ticker symbol with firm characteristics on its intangible value [23]. This random effects approach also allows us to model the main effect of congruent ticker symbols on intangible value. We included the main effects of all variables used to construct the interaction terms in the model. A Hausman test of the random effects model versus the fixed effects model fails to reject the null hypothesis (i.e., that random effects would be consistent and efficient) supporting the random effects formulation.

In addition, we included time dummy variables to account for any time-specific effects and five industry dummy variables for the two-digit SIC codes of 52, 53, 54, 56, 57, and 59. We also included two dummy variables to account for retailer characteristics—a brand variable which measured whether the retailer marketed brands under the corporate name (e.g., Gap Inc. sells Gap brand apparel) and a category variable which measured whether or not the retailer was a grocery store (e.g., Weiss Markets Inc. was coded as a grocery store). All explanatory variables were lagged by one year to preclude explanations of reverse causality.

5 Results

5.1 Heckman Sample Correction

Some firms (n = 72) were not observed for the entire period. If the data are not missing randomly and the model is estimated with the observed data, the parameter estimates may be biased [20]. We corrected for potential sample selection bias by including Lee’s λ (inverse Mill’s ratio) obtained from a Heckman selection model in the regression model for Tobin’s Q.

We first estimated the probit selection model including the firm’s sales and its performance as factors influencing its exit from the data set. The results supported the selection model (χ2 = 15.891, degrees of freedom = 1, p < 0.01). The firm’s size (b = −0.123, p < 0.01) and performance (b = −0.483, p < 0.01) had negative effects in the selection model. As might be expected, small and poorly performing firms were more likely to exit the data set.

5.2 Hypotheses Testing

We estimated the model relating the firm’s congruent ticker symbol and its interactions with size, performance, advertising, and distribution presence along with control variables, the year, industry and retailer dummy variables to intangible value using a random effects regression model. Column 1 of Table 3 contains the results of pertaining to the hypothesized model. The data fit the model well (Wald Chi-square, degrees of freedom (30) = 181.70, p < 0.01) and the model’s R 2 is 0.119. Some of the year dummy variables were statistically significant.

As expected, the firm’s congruent ticker symbol does not affect its intangible value (b = 0.421, not significant (ns)). The firm’s size (b = 0.157, p < 0.01) and performance (b = 1.548, p < 0.01) increase intangible value while its advertising (b = −1.548, p < 0.01), somewhat surprisingly, and its financial liquidity (b = −0.073, p < 0.05) decrease intangible value. We discuss the negative effect of advertising on intangible value subsequently. The firm’s distribution presence (b = −0.001, ns), financial leverage (b = 0.028, ns), and Lee’s Lambda for Heckman sample selection correction (b = 0.062, ns) do not affect intangible value. The corporate brand name dummy (e.g., GAP Brands for GAP Inc.) increases intangible value (b = 0.328, p < 0.10) while the grocery store dummy has no effect (b = 0.031, ns).

We next present the results for the hypothesized effects. First, the results do not support the interaction effect, H1, between the firm’s congruent ticker symbol and its size (b = −0.074, ns). However, the results support H2, the interaction effect between the firm’s congruent ticker symbol and its performance (b = 2.885, p < 0.01), and H3, the interaction effect between the firm’s congruent ticker symbol and its advertising (b = 0.141, p < 0.01). Finally, the results support H4a, the positive interaction effect between the firm’s congruent ticker symbol and its distribution presence (b = 0.015, p < 0.05). We next report additional analyses that examine the robustness of the results.

5.3 Additional Analyses

5.3.1 Model Comparisons

First, we compared the proposed model to a model with only the main effects of the firm’s size, performance and accounting data but without the two marketing characteristics of advertising and distribution presence. Based on a Chi-square test, the hypothesized model outperformed this model (p < 0.01). Second, we compared the proposed model to one with all of the explanatory variables and the interaction effects of congruent ticker symbol with firm size and performance but without its interaction effects with the two marketing characteristics of advertising and distribution presence. Again, the proposed model outperformed this model (p < 0.01). Thus, the proposed model explains intangible value better than models with either only accounting data or excluding congruent ticker symbol’s interactions with the firm’s advertising and distribution presence.

5.3.2 Firm Size

We reestimated the model using an alternative measure of firm size, measured by the natural logarithm of its assets instead of its sales. We report these results in column 2 of Table 3, which are consistent with the results in column 1 of Table 3 testifying to the robustness of the model specification.

5.3.3 Alternative Ticker Symbol-Naming Strategies

In this paper, we defined congruent ticker symbol as whether the firm’s ticker symbol is similar to the firm’s corporate name. A perusal of the ticker symbol-naming strategies suggests an alternative ticker symbol strategy, pronounceable ticker symbols. There were 30 firms (17 %) that had a pronounceable ticker symbol (e.g., OATS for Wild Oats Markets Inc.), which increases short-term stock returns, i.e., 1 day after the firm’s listing on the stock exchange [1].

An interesting question that arises is whether pronounceable ticker symbols, which were presumably adopted by these firms to leverage processing fluency among the investment community about their firms’ stocks, affect intangible value? We examine this question by re-estimating the model using the pronounceability of the ticker symbols. The results in Column 2 of Table 4 do not support either main or interaction effects of pronounceable ticker symbol-naming strategies on intangible value. We then re-estimated the model using a symbol which is either pronounceable or congruent. The results reported in Column 3 of Table 4 are similar to those obtained in the hypothesized model (Column 1 of Table 4). Hence, pronounceability of ticker symbols does not appear to be value-relevant for the firms in our study, with respect to their intangible values.

5.3.4 Predictive Validity

We evaluated the model’s predictive ability using a jackknifing technique, holding out a target firm year, re-estimating the model on other firms, and then using the estimated parameters to predict the target firm’s Tobin Q. We computed the mean absolute deviation (MAD), defined as \( =\left(1/ NT\right){\displaystyle \sum_{t_i=1}^{T_i}{\displaystyle \sum_{i=1}^N\left|{T}_{ob}\_{Q}_{oit}-{T}_{ob}\_{Q}_{pit}\right|}} \), where T ob _ Q oit , T ob _ Q pit , N, and T i denote observed and predicted Tobin’s Q for firm i in year t, N the number of firms, and T i the number of years for each firm i, respectively. The proposed model’s MAD was 0.245 compared to MAD of 0.406 obtained with the average values of explanatory variables (improvement of 40%). Thus, the proposed model predicts the firm’s intangible value well.

6 Discussion

The firm’s ticker symbol, an important mnemonic device that uniquely identifies the firm’s stock to the investment community, is extensively used by various stock market participants. In this paper, we introduce the concept of a congruent ticker symbol, which we propose, in conjunction with firm characteristics, has the potential to be a value-relevant market-based asset. The empirical test of the relationship in the US retailing industry indicates that the firm’s congruent ticker symbol, in conjunction with its performance, advertising, and distribution presence, increases its intangible value. We conclude with a discussion of the paper’s theoretical contributions, managerial implications, and limitations and opportunities for future research.

6.1 Theoretical Contributions

6.1.1 Marketing Metrics

This paper is at the intersection of Wall Street and marketing strategy as embodied in its congruent ticker symbol, a representation of the firm’s corporate brand to investors, who are customers of the firm’s stocks. In demonstrating the value relevance of congruent ticker symbols, we find that the ticker symbol, typically not considered as a variable under the purview of the marketing function, can be an intangible market-based asset.

The null main effect of congruent ticker symbols on the firm’s intangible value suggests that congruent ticker symbols are not independently value-relevant, but only in conjunction with the firm’s performance, advertising, and distribution presence. However, it is expected that the null effect of congruent ticker symbols represents a departure from past research in finance [13, 22], which supports, albeit indirectly, a main effect of familiarity on firms’ stock returns. We conjecture that this departure may be arising because we use intangible value, while past research has examined other metrics such as ownership patterns of stocks.

In addition, the null main effect of congruent ticker symbols, combined with their significant positive interaction effects with the firm’s performance, advertising, and distribution presence, suggests that congruent ticker symbols are contingent market-based assets, i.e., for some but not all, retailer firms. Future research that explores other such contingent market-based assets (e.g., corporate logos and audiovisual mnemonics) will be useful.

Although firms’ distribution strategies affect intangible firm values [29, 43], past research relating marketing activities to investors’ responses has studied only the value relevance of advertising. In this paper, we examine the investor response effects of distribution presence, a key marketing mix element.

The negative main effect of advertising on intangible value is surprising and represents a departure from research that reports a main effect of advertising on the pattern of stockholding and liquidity [17, 18], for which we offer the following explanation. First, like other research that uses secondary data sources for firms’ advertising data, we focus on advertising spending, an input-based accounting measure of advertising, which also includes promotional expenditures (see the COMPUSTAT manual) and does not measure the content (e.g., brand building versus sales generation) or the effectiveness of firms’ advertising programs which can vary significantly across firms. Second, promotions constitute a significant component of retailers’ advertising and promotion budgets, and while promotions improve short-term revenues and profits, they lower long-term profits and shareholder value [32]. Moreover, given retailers’ high frequency of promotions and price-based advertising, would investors infer their poor performance? This is a conjecture that we are unable to resolve with the data on hand. Future studies that explore the effectiveness of advertising in retailers, and the boundary conditions of the main and interaction effects of advertising on intangible value in other industry contexts would be useful.

6.1.2 Corporate Branding

This paper’s findings also extend the marketing literature on the wealth effects of corporate branding. There is empirical evidence in the marketing (e.g., Ref. [34]) and accounting [5] literatures that branding strategies of firms increases their shareholder value. However, past research has not examined whether the firms’ branding efforts outside the purview of the firm’s marketing function (e.g., ticker symbols) are value-relevant. Our conceptualization of congruent ticker symbols as representations of firms’ corporate brands to investors and the demonstration of its positive contingent effects on shareholder value address this gap in the literature and opens the door for future work on issues related to corporate branding communications aimed at the investor community (e.g., CEOs’ letters to shareholders).

6.1.3 Behavioral Finance

Our view of congruent ticker symbols as corporate brand representations takes a step toward bridging the gap between the work in behavioral finance that explores “irrational” investor behaviors. Future work that relates aspects of various marketing mix programs [e.g., everyday low price (EDLP) versus Hi-Lo price, humor in advertising, thematic versus promotion-based advertising] to contextual factors that influence investors’ behaviors will be insightful.

6.2 Managerial Implications

The interaction effects of congruent ticker symbol with firm characteristics draw attention to the importance of the firm’s ticker symbol as a branding element for investors, a key constituency for publicly listed firms. Just as the corporate brand represents a source of equity with firm’s customers, the congruent ticker symbol represents brand equity with investors, who are customers of the firm’s shares.

Specifically, the findings suggest that a congruent ticker symbol creates enduring “value-in-use” for some, but not all firms. For practice, the model we propose also has good predictive validity and can be used to value firms’ congruent ticker symbols (contingent on their other characteristics) as part of the valuation process in mergers and acquisitions.

The findings on the contingent effect of congruent ticker symbols and the null effect of pronounceable ticker symbols offer some guidelines for leveraging firms’ congruent ticker symbol. Executives of firms with congruent ticker symbols can highlight their superior performance, advertising, and distribution presence to investors to increase their shareholder value. If firms with incongruent ticker symbols have superior performance, large advertising spending, or significant distribution presence, they consider renaming their ticker symbols to be congruent, which should increase their intangible value.

Further, firms may also be experiencing an opportunity loss in their shareholder value if other firms have ticker symbols similar to their corporate names, because of investor confusion [35]. Indeed, we noticed the potential for such investor confusion for two firms in our data set: GAP Inc. (GPS) and Great Atlantic and Pacific Tea Company (GAP), whose ticker symbol GAP is similar to Gap Inc’s corporate name. We collected daily stock prices, returns, and trading volumes for the two firms from January 1, 1976 to December 31, 2007 (N = 7,979 observations) and found high correlations between their prices (ρ = 0.64, p < 0.01) and volume (ρ = 0.47, p < 0.01). Prima facie, these correlations point to investor confusion and resultant opportunity losses in shareholder value (in this case to Gap Inc., the firm with superior performance). GAP Inc. should consider using GAPS as their ticker symbol (which is already assigned to them) as their ticker symbol to reduce investor confusion and leverage increased intangible value from their superior performance, advertising, and distribution presence. Also, firms considering changing their ticker symbol to a congruent one can use the proposed model to assess their intangible value following this symbol change, given their profiles.

6.3 Limitations and Opportunities for Further Research

We define a congruent ticker symbol based on whether the ticker symbol is similar to its corporate name. Firms use several other ticker symbol-naming strategies including their history (Southwest Airlines’ LUV, whose first flights were out of Love Field airport in Dallas), brands (e.g., Anheuser Busch Inc.’s BUD), customer segments [Harley Davidson Inc.’s (HOG, an acronym for its famed Harley Owners’ Group] and even a muse (Steinway Musical Instruments Inc.’s LVB, acronym for Ludwig van Beethoven, the famous music composer).

We offer processing fluency of the firm’s congruent ticker symbol as the mechanism by which the firm’s intangible value increases. However, in this study, using secondary data, we are unable to explicitly test this mechanism. One alternative explanation for the effects of congruent ticker symbols on intangible value may be that investors may assume that the management of firms which adopt a congruent ticker symbol are “savvy marketers” and may therefore assume superior marketing and management quality, which may be resulting in higher intangible value. Further research that explores this and other alternative explanations would be useful.

Moreover, there may be risks and/or costs to ticker symbol-naming strategies which we do not examine. For example, ticker symbols named after brands may increase the firm’s risk exposure (e.g., does Anheuser Busch Inc.’s stock returns covary with Budweiser’s market shares?). The development of a taxonomy of ticker symbols and their shareholder wealth implications emerges as an interesting area for future research.

We examine the interaction effects of two marketing characteristics pertinent to the retailing industry, advertising, and distribution presence, with congruent ticker symbols, on intangible value. Further, we focus on shareholder value as measured by the firm’s intangible value and do not address whether these effects arise because of trading by institutional investors, day traders, or casual investors. Research exploring ticker symbol strategies using other methods (e.g., in-depth interviews and surveys) that incorporate other marketing characteristics with output-based measures of (e.g., corporate brand awareness and shelf space) and using other metrics including systematic risk, shareholding patterns, and volatility in returns will be useful to further disentangle these effects.

Many high technology firms (e.g., Yahoo, Google, Adobe, and Amazon) use corporate branding strategies and have congruent ticker symbols (YHOO, GOOG, ADB, and AMZN, respectively). We suggest that there is a preponderance of congruent ticker symbols in firms in the high technology sector not only because of a key role for corporate branding in this sector but also because investor relations management is a key mechanism for shareholder wealth creation. Will the widespread prevalence of congruent ticker symbols in an industry affect firms’ intangible value differently? Also, while we included time dummies, we do not examine whether the value relevance of congruent ticker symbols varies by stock market conditions. Studies covering other industries especially the high-technology sector, across bear markets characterized by panic selling, would be useful.

In sum, we believe that this study represents a useful, first step in exploring the shareholder wealth effects of the firm’s ticker symbol, which represents the firm’s corporate brand to its investors. We hope that this paper stimulates further work exploring the effects of corporate branding, in general, and ticker symbols, in particular, on shareholder value.

Notes

In this paper, we use the terms ‘intangible value’ and ‘value’ and ‘intangible firm value’ to denote the firm’s intangible value measured by its Tobin’s Q, and the term ‘stocks’ and ‘shares’ to denote its stocks.

References

Alter AL, Oppenheimer DL (2006) Predicting short-term stock fluctuations by using processing fluency. http://www.pnas.org/cgi doi 10.1073 pnas.0601071103, 9369–9372

Amir E, Lev B (1996) Value relevance of non-financial information: the wireless communications industry. J Account Econ 22(1–3):3–30

Atiase RK (1985) Predisclosure information, firm capitalization, and security price behavior around earnings announcements. J Account Res 23(1):21–36

Bagwell K, Ramey G (1993) Advertising as information: matching products to buyers. The Journal of Economics and Management Strategy 2(summer):199–243

Barth ME, Clement MB, Foster G, Kasznik R (1998) Brand values and capital market evaluation. Rev Acc Stud 3(1–2):41–68

Barth ME, Clinch G (1998) Revalued financial, tangible, and intangible assets: associations with share prices and non-market-based value estimates. J Account Res 36:199–233

Bharadwaj AS, Bharadwaj SG, Konsynski BR (1999) Information technology effects on firm performance as measured by Tobin’s Q. Manag Sci 45(June):1008–1024

Bhushan R (1989) Firm characteristics and analyst following. J Account Econ 11(2/3):255–274

Bond S, Meghir C (1994) Dynamic investment models and the firm’s financial policy. Rev Econ Stud 61:197–207

Bornstein RF, D’Agostino PR (1992) Stimulus recognition and the mere exposure effect. J Pers Soc Psychol 63:545–552

Cacioppo JT, Berntson GG (1994) Relationship between attitudes and evaluative space: a critical review with emphasis on the separability of positive and negative substrates. Psychol Bull 115:401–423

Chung KH, Pruitt SW (1994) A simple approximation of Tobin’s Q. Financial Management 23(autumn):70–74

Coval JD, Moskowitz TJ (1999) Home bias at home: local equity preference in domestic portfolios. J Financ 54(6):2045–2073

Day GS, Montgomery DB (1983) Diagnosing the experience curve. J Mark 47(2):44–58

Fama EF, French KR (1992) The cross-section of expected stock returns. J Financ 47(2):427–465

Fehle F, Tsyplakov S, Zdorovtsov V (2005) Can companies influence investor behavior through advertising? Super bowl commercials and stock returns. Eur FinancManag 11(5):625–647

Frieder L, Subrahmanyam A (2005) Brand perceptions and the market for common stock. J Financial Quantitat Anal 40(1):57–85

Grullon G, Kanatas G, Weston JP (2004) Advertising, breadth of ownership, and liquidity. Rev Financ Stud 17(2):439–461

Hambrick DC (1983) An empirical typology of mature industrial product environments. Acad Manag J 26(2):213–230

Heckman JJ (1979) Sample selection as a specification error. Econometrica 47(1):153–161

Hirshleifer D (2001) Investor psychology and asset pricing. J Financ 56(4):1533–1597

Huberman G (2001) Familiarity breeds investment. Rev Financ Stud 14(3):659–680

Jacobson R (1990) Unobservable effects and business performance. Mark Sci 9(1):74–85

Jacoby LL (1983) Perceptual enhancement: persistent effects of an experience. J Exp Psychol 9:21–38

Jacoby LL, Dallas M (1981) On the relationship between autobiographical memory and perceptual learning. J Exp Psychol 110(3):306–340

Jensen M, Meckling W (1976) Theory of the firm: managerial behavior: agency costs and ownership structure. J Financ Econ 3(4):305–360

Kadapakkam P-R, Misra L (2007) What’s in a nickname?—price and volume impacts of a pure ticker symbol change. J Financ Res 30:53–71

Lakonishok J, Shleifer A, Vishny RW (1994) Contrarian investment, extrapolation, and risk. J Financ 49(5):1541–1578

Lee RP, Grewal R (2004) Strategic responses to new technologies and their impact on firm performance. J Mark 68(4):157–171

MacInnis DJ, Jaworski BJ (1989) Information processing from advertising: toward an integrative framework. J Mark 53(4):1–23

Norton MI, Frost JH, Ariely D (2007) Less is more: the lure of ambiguity, or why familiarity breeds contempt. J Personal Soc Psychol 92(1):97–105

Pauwels K, Silva-Risso J, Srinivasan S, Hanssens DM (2004) New products, sales promotions, and firm value: the case of the automobile industry. J Mark 68(4):142–156

Pollock TG, Rindova VP, Maggitti PG (2008) Market watch: information and availability cascades in the U.S. IPO market. Acad Manag J 51(2):335–358

Rao VR, Agarwal MK, Dahloff D (2004) How is manifest branding strategy related to the intangible value of a corporation? J Mark 68(4):126–141

Rashes MS (2001) Massively confused investors making conspicuously ignorant choices (mci–mcic). J Financ 56(5):1911–1927

Reber R, Schwarz N (1999) Effects of perceptual fluency on judgments of truth. Conscious Cogn 8:338–342

Reber R, Schwarz N, Winkielman P (2004) Processing fluency and aesthetic pleasure: is beauty in the perceiver’s processing experience. Personal Soc Psychol Rev 8(364):382

Reber R, Winkielman P, Schwarz N (1998) Effects of perceptual fluency on affective judgments. Psychol Sci 9:45–48

Schroeter JR (1988) Estimating the degree of market power in the beef packing industry. Rev Econ Stat 70(1):158–162

Schultz M, Mouritsen J, Gabrielson G (2001) Sticky reputation: analyzing a ranking system. Corp Reput Rev 4(1):24–41

Schwarz N (2004) Meta-cognitive experiences in consumer judgment and decision making. J Consum Psychol 14:332–348

Smallwood DE, Conlisk J (1979) Product quality in markets where consumers are imperfectly informed. Q J Econ 93(1):1–23

Srinivasan R (2006) Dual distribution and intangible firm value: franchising in restaurant chains. J Mark 70(3):120–135

Srivastava RK, Shervani TA, Fahey L (1998) Market-based assets and shareholder value: a framework for analysis. J Mark 62(1):2–18

Stigler GJ (1961) The economics of information. J Polit Econ 69(3):213–225

Stigler GJ, Becker GS (1977) De gustibus non est disputandum. Am Econ Rev 67:76–90

Tulving E, Schacter DL (1990) Priming and human memory systems. Science 247:301–306

Tversky A, Kahneman D (1973) Availability: a heuristic for judging frequency and probability. Cogn Psychol 5(2):207–232

Whittlesea BWA, Jacoby LL, Girard K (1990) Illusions of immediate memory: evidence of an attributional basis for feelings of familiarity and perceptual quality. J Mem Lang 2:716–732

Winkielman R, Cacioppo JT (2001) Mind at ease puts a smile on the face: psychophysiological evidence that processing facilitation leads to positive affect. J Pers Soc Psychol 81:989–1000

Winkielman R, Schwarz N, Reber R, Fazendeiro T (2003) Cognitive and affective consequences of visual fluency: when seeing is easy on the mind. In: Scott L, Batra R (eds) Persuasive imagery: a consumer response perspective. Lawrence Erlbaum Associates, Inc., Mahwah, pp 75–89

Witherspoon D, Allan LG (1985) The effects of prior presentation on temporal judgments in a perceptual identification task. Mem Cogn 13:103–111

Zajonc RB (1968) Attitudinal effects of mere exposure. J Pers Soc Psychol 9(2):1–27

Zeithaml VA, Varadarajan RP, Zeithaml CP (1988) The contingency approach: its foundations and relevance to theory building and research in marketing. Eur J Mark 22(7):37–64

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Srinivasan, R., Umashankar, N. There’s Something in a Name: Value Relevance of Congruent Ticker Symbols. Cust. Need. and Solut. 1, 241–252 (2014). https://doi.org/10.1007/s40547-014-0018-8

Published:

Issue Date:

DOI: https://doi.org/10.1007/s40547-014-0018-8