Abstract

Is the Spanish economy positioned at its optimal progressivity level in personal income tax? This article quantifies the aggregate, distributional, and welfare consequences of moving toward such an optimal level. A heterogeneous households general equilibrium model featuring both life cycle and dynastic elements is calibrated to replicate some characteristics of the Spanish economy and used to evaluate potential reforms of the tax system. The findings suggest that increasing progressivity would be optimal, even though it would involve an efficiency loss. The optimal reform of the tax schedule would reduce wealth and income inequality at the cost of negative effects on capital, labor, and output. Finally, these theoretical results are evaluated using tax microdata and describe a current scenario where the income-top households typically face suboptimal effective average tax rates.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Many modern governments implement a redistributive fiscal policy, where personal income is taxed at an increasingly higher rate, while transfers tend to target the poorest households. The taxation of personal income is not a minor issue, since most of the OECD economies obtain a large proportion of their tax collection through it.Footnote 1 In Spain, there is an intense debate about how to finance the fiscal stimulus recovery plans to alleviate the economic consequences of the COVID-19 crisis and, more precisely, about how to deal with the unavoidable and needed fiscal consolidation process that will surely follow the enormous government fiscal effort. In particular, this growing political debate is taking up many headlines on the so-called “fiscal justice,” which is putting on the table a tax rate increase for the high-income earners, i.e., an increase in the progressivity of the personal income tax. These policies are initially developed to produce a more egalitarian distribution of income and, consequently, to provide social insurance for both currently living households that suffer from large income fluctuations, and for future generations that face uncertainty about what their initial state will be.

Raising taxes on higher incomes may be potentially justified by the increase in income and wealth inequality in recent years, especially after the 2007 crisis. These concerns over rising economic inequalities have resulted in a huge body of literature. One of the clearest examples is the paper by Piketty (2015), which triggered a widespread discussion on the nature and evolution of wealth inequalities worldwide. A recent study by Anghel et al. (2018) provides an overview of the inequality levels in Spain and their evolution. They show that the wave of unemployment caused by the 2007 crisis resulted in an inequality increase in per capita income. As for the wealth inequality in Spain, they show that it exceeds income inequality and it increased after the crisis, which may be due to financial assets outperforming real assets according to their vision. By international standards, Spain’s wealth inequality is moderate, as the ownership of real assets is more widespread than in other countries. Beforehand, one is likely to consider that raising taxes on the income-rich households could reverse the growing concentration at the top. However, this type of policy could be very costly in terms of efficiency in advanced market economies.

The optimal design of a redistributive tax system is subject to many constraints. Bakis et al. (2015) emphasize three of them in their study about the transitional dynamics of setting an optimal progressivity level. First, agents may have access to self-insurance through savings or bequests, and then, increasing the redistributiveness of the fiscal policies would alleviate the need for such self-insurance and would crowd out capital accumulation, leading to reduced investment and output. Second, misinformation may prevent government from observing individual productivity and, by raising taxes on certain agents, it could provoke incentive problems that discourage labor and thereby reduce output. Third, large-scale shifts in labor and capital supply (savings) alter the wage rate and the interest rate, which may have unexpected repercussions for income redistribution.

This is why having a quantitative theory that accounts accurately for the observed income and wealth inequality is crucial when assessing the aggregate, distributional, and welfare implications of certain policies. For that purpose, a heterogeneous households general equilibrium model is here calibrated to replicate some characteristics of the Spanish economy and used to compare the steady-state consequences of setting an optimal progressivity level in the Spanish personal income tax. For the Spanish case, general equilibrium models with heterogeneous agents have already been used to examine the effects of certain reforms.Footnote 2 However, not many studies are encountered to use general equilibrium models with heterogeneous agents to explore the relationship between fiscal policy variables and the endogenous cross-sectional distribution of income and wealth in Spain, in turn the main topic of analysis of this study. The references that we find with respect to this concern are mentioned in the following lines. Pijoan-Mas and González Torrabadella (2006) quantify the aggregate and distributional implications of an array of revenue neutral flat tax reforms for Spain. Viegas and Ribeiro (2015) attempt to characterize the Spanish debt consolidation process in order to assess its effects on economic inequality and welfare. And finally, Guner et al. (2020) uses a life cycle model to evaluate the impact on fiscal revenues of changes in the progressivity of personal income taxes in Spain. The study herein presented is closely related to that research, but the focus in the present work is on the welfare implications of the reforms.

In general, the literature on optimal taxation in a general equilibrium framework is vast, but these pieces of work do not have their focus on the Spanish context. Kindermann and Krueger (2018), Conesa et al. (2009), and Guner et al. (2017) study the effects of taxing higher incomes and particularly assess whether and to what extent capital should be taxed. Moreover, Bakis et al. (2015), Heathcote et al. (2017), and Conesa and Krueger (2006) provide an assessment of the optimal progressivity of personal income tax and how redistributive the government’s fiscal policy should be. Finally, Díaz-Giménez and Pijoan-Mas (2019) evaluate the gains that a progressive consumption tax could have with the same modeling framework that is used in the present analysis. Hence, due to the topic and the underlying methodology, the work contained herein would contribute to this body of literature.

Again, although some previous studies have analyzed the Spanish economy with general equilibrium models devoted to study policy implications for wealth and income inequality, none of them combined the main characteristics of the dynastic and of the life cycle abstractions (hybrid model with retirement and bequests). Contrarily, these models are built in either dynastic or life cycle fashions. This is where this study adds value, as it proposes other methodologies previously used in other contexts to be applied to the Spanish scenario. The theoretical framework is built for Spain following Castañeda et al. (2003), who also rely on a hybrid approach to account for the US earnings and wealth inequality.Footnote 3 Heterogeneity is introduced in this setup via distinct labor market opportunities using an uninsurable process on the endowment of efficiency labor units that features nonlinear dynamics. Given the labor market opportunity, the households choose their work effort. In other words, the labor choice is set here to be endogenous, as in Pijoan-Mas and González Torrabadella (2006). Life cycle characteristics are modeled using aging and retirement, and dynastic links are modeled in a way that households are altruistic toward their descendants. Once the model is properly calibrated to match some empirical statistics of the Spanish economy, these features ensure that households save for precautionary motives (life cycle reasons and altruistic reasons), as argued by Díaz-Giménez and Pijoan-Mas (2019). This model economy replicates the distributions of income and wealth in very much detail. Further, it also works well when replicating the very top tails of those distributions.Footnote 4

Further, once the theoretical framework is defined, a bunch of potential progressivity reforms are assessed through the calculation of many different general equilibria (one equilibrium for each degree of progressivity evaluated). Then a Benthamite social planner, who takes into account all households in the economy by putting the same weight on each of them, discerns the optimal progressivity reform. The findings suggest that aggregate social welfare is maximized when the level of progressivity of the Spanish personal income tax is increased to some extent. More precisely, in the optimally reformed scenario (setting the optimal level of progressivity), welfare gains are equivalent to an average increase of 3.08% of consumption.

By decomposing the aggregate welfare change, it is shown that most of the welfare gains are obtained by direct improvements in the tax system. It means that most of the aggregate welfare gains come from a majority of households facing a lower tax rate, i.e., the poorest households facing lower effective income tax rates and richest households affronting higher effective income tax rates. On the contrary, the general equilibrium effects of the optimal reformed economy (higher interest rate and lower wage) and the effects resulting from changes in the equilibrium distribution of households across income levels (larger mass of households at lower income levels) show a welfare loss, but these losses are so small that together cannot overpass the welfare gains directly coming from the reformed tax system, jointly resulting in positive aggregate welfare changes. These welfare gains are decomposed by household type, where it is observed that the poorest working and non-working households are the ones who benefit the most from the reform. Contrarily, the most efficient working households and the wealthiest ones (either working or non-working) are those who experience the largest trade-off between (i) positive welfare effects derived from higher income (due to an increased interest rate that pushes up capital returns) and (ii) adverse effects emerging from higher tax payments (due to the increase in progressivity of the income tax that discourages labor and savings). The losses from this trade-off are particularly high in top parts of the income and wealth distributions and clearly offset the potential welfare gains of the households populating such areas. Therefore, knowing that these agents would be the losers of the reform, despite positive aggregate welfare effects, the consequences on aggregate capital, labor, and output would be negative, which means that the economy would experience an efficiency loss. Moreover, looking at the distributional implications, this reform would reduce income and wealth inequality.

Finally, the theoretical results are evaluated with Spanish tax microdata. From the point of view of a Benthamite social planner, households between the 20th and the 80th percentiles would experience a decrease in their average tax rates under the optimal progressivity reform. For example, the effective average tax rate encountered by a household situated within the 40th and the 60th percentiles of the income distribution would drop from 0.067 to 0.056, which involves a change of 1.1 p.p.. On the other hand, households above the 80th percentile would experience a drastic increment in their effective average tax rate. For instance, the top 1% households of the gross income distribution would go from confronting an average tax rate of 0.284 in the actual scenario to dealing with an average tax rate of 0.330 in the optimal one.

The remainder of the paper is structured as follows. The model is formally introduced in Sect. 2. Section 3 describes how the model has been calibrated to match Spanish aggregate and distributional data. Section 4 presents the optimal reform of the progressivity based on a welfare comparison between steady-states and details aggregate and distributional implications. Finally, Sect. 5 concludes.

2 The model economy

The model economy analyzed in this study strictly follows the setup proposed by Castañeda et al. (2003), which is a modified version of the stochastic neoclassical growth model with uninsured idiosyncratic risk and no aggregate uncertainty. The main features of this theoretical framework can be summarized in as follows: (i) there is a number of households that are ex-ante identical (they all exhibit the same preferences); (ii) these households are differentiated among themselves by the uninsured household-specific shock that they receive in their endowments of efficiency labor units; (iii) households go through the life cycle and can be either workers or retirees (which can be interpreted as households out of the labor market in general); (iv) once households are retired, they face a probability of dying, and if they die, they are replaced by working-age descendants; and (v) households are altruistic toward their descendants.

2.1 Population and endowment dynamics

This particular model economy is inhabited by a measured one continuum of heterogeneous dynastic households. The households can be either of working-age or retired, and they are all endowed with \(\ell \) units of disposable time each period. Workers face an uninsured idiosyncratic stochastic process that determines their endowment of efficiency labor units. They also face an exogenous positive probability of retiring. Retired households are endowed with zero efficiency labor units and face an exogenous positive probability of dying. When a retired household dies, it is replaced by a working-age descendant that inherits the deceased household estate and, possibly, some of its earnings abilities. To denote the household’s random age and random endowment efficiency labor units jointly, a one-dimensional shock, s, is used. This process is assumed to be i.i.d. across households and follows a finite state Markov chain with conditional transition probabilities given by \(\Gamma _{{\mathcal {S}}\mathcal {S'}}=\Gamma \left( s'|s\right) =Pr\left\{ s_{t+1}=s'|s_{t}=s\right\} \), where s and \(s'\in {\mathcal {S}}=\{1,2,\ldots ,n\}\).

It is assumed that s takes values in one of two possible J-dimensional sets, \(s\in {\mathcal {S}}={\mathcal {E}}\cup {\mathcal {R}}={1,2,\ldots ,J}\cup {J+1,J+2,\ldots ,2J}\). When a household draws shock \(s\in {\mathcal {E}}\), it is of working-age and endowed with \(e(s)>0\) efficiency labor units. When a household draws shock \(s\in {\mathcal {R}}\), it is retired and endowed with zero efficiency labor units. When a household’s shock changes from \(s\in {\mathcal {E}}\) to \(s' \in {\mathcal {R}}\), the household has retired. When it changes from \(s\in {\mathcal {R}}\) to \(s'\in {\mathcal {E}}\), the retired household dies and is replaced by a working-age descendant that inherits the estate, \(a_{t}\), that the deceased household had at the end of period t. Therefore, the joint age and endowment process imply that the transition probability matrix \(\Gamma _{{\mathcal {S}}\mathcal {S'}}\) controls (i) the demographics of the model economy by determining the expected durations of the households’ working lives and retirements, (ii) the lifetime persistence of earnings by determining the mobility of households between states in \({\mathcal {E}}\), (iii) the life cycle pattern of earnings by determining how the endowments of efficiency labor units of new entrants differ from those of senior workers, and (iv) the intergenerational persistence of earnings by determining the correlation between the states in \({\mathcal {E}}\) for consecutive members of the same dynasty.

Since it is assumed that the presented joint age and endowment process takes values in two J-dimensional sets, the number of realizations of such process is 2J. Therefore, to specify the process on s, the values of \((2J)^2+J\) parameters must be chosen. \((2J)^2\) of these parameters are the conditional transition probabilities and the remaining J are the values of the endowment of efficiency labor units. However, some assumptions about the nature of the joint age and endowment process impose some additional structure/restrictions on the transition probability matrix, \(\Gamma _{{\mathcal {S}}\mathcal {S'}}\), which reduce the large number of parameters. In order to understand these restrictions better, it helps to consider the following partition of this matrix:

Submatrix \(\Gamma _{{\mathcal {E}}{\mathcal {E}}}\) describes the changes in the endowments of efficiency labor units of working-age households that are still of working age one period later, and no restrictions are placed on it so the values of \(J^2\) parameters must be chosen. Submatrix \(\Gamma _{{\mathcal {E}}{\mathcal {R}}}\) describes the transitions from the working-age states into the retirement states. This submatrix is defined by \(\Gamma _{\mathcal {ER}}:=p_{r} {\mathbf {I}}\), where \(p_{r}\) is the probability of retiring and \({\mathbf {I}}\) is the identity matrix. This is because every working-age household faces the same probability of retiring and because only the last realization of the working-age shock is used to keep track of the earnings ability of the retirees. Consequently, the value of only one parameter must be chosen. Submatrix \(\Gamma _{\mathcal {RR}}\) describes the changes in the retirement states of retired households that are still retired one period later. This submatrix is defined by \(\Gamma _{{\mathcal {R}}{\mathcal {R}}}:=p_{s} {\mathbf {I}}\), where \((1-p_{s})\) is the probability of dying or exiting the economy. This is because the type of retired households never changes, because every retiree faces the same probability of dying or exiting the economy. Therefore, the value of only one parameter is needed to identify this submatrix. Finally, submatrix \(\Gamma _{{\mathcal {R}}{\mathcal {E}}}\) describes the transitions from the retirement states into the working-age states that take place when a retired household dies and is replaced by its working-age descendant. The rows of this submatrix contain a two-parameter transformation of the stationary distribution of \(s\in {\mathcal {E}}\), which is denoted by \(\gamma ^{*}_{{\mathcal {E}}}\). Intuitively, the transformation amounts to shifting the probability mass from \(\gamma ^{*}_{{\mathcal {E}}}\) toward both the first row of \(\Gamma _{{\mathcal {R}}{\mathcal {E}}}\) and toward its diagonal. This particular transformation is aimed to control for both the life cycle profile of earnings and its intergenerational correlation. In short, to characterize \(\Gamma _{{\mathcal {R}}{\mathcal {E}}}\), one must choose the value of the two shifting parameters, as it will explained in what follows.

Intergenerational transmission of earnings ability The process driving the transition between retirement and working-age states, i.e., transition submatrix \(\Gamma _{{\mathcal {R}}{\mathcal {E}}}\), must reflects somehow the correlation between the average income of one generation and the average income of its immediate descendants. In this way, the working-age descendant that will replace a deceased retired household will inherit some earnings ability from its predecessor. It implies that the model economy here presented will capture the intergenerational persistence of earnings. Following the procedure presented in Castañeda et al. (2003), in order to determine such intergenerational persistence, the distribution from which households draw the first shock of their working lives must be chosen. If this first shock is assumed to be drawn from the stationary distribution of \(s \in {\mathcal {E}}\), which is denoted by \(\gamma ^{*}_{{\mathcal {E}}}\), then the intergenerational correlation of earnings will be very small. In contrast, if it is assumed that every working-age household inherits the endowment of efficiency labor units that its predecessor had at the end of its working life, then the intergenerational correlation of earnings will be relatively large. Since this correlation between generations usually lies between these two extremes, an additional parameter, \(\phi _1\), is needed to act as a weight that averages between a matrix with \(\gamma ^{*}_{{\mathcal {E}}}\) in every row, denoted by \(\Gamma ^{*}_{{\mathcal {R}}{\mathcal {E}}}\), and the identity matrix, \({\mathbf {I}}\). Intuitively, the role played by this parameter is to shift the probability mass of \(\Gamma ^{*}_{{\mathcal {R}}{\mathcal {E}}}\) toward its diagonal.

Life cycle profile of income The process driving the transition between retirement and working-age states, i.e., transition submatrix \(\Gamma _{{\mathcal {R}}{\mathcal {E}}}\), should also reflect the existing earnings ability gap between new entrants and senior workers. Following the procedure presented in Castañeda et al. (2003), in order to determine such differential, the distribution from which households draw the first shock of their working lives must be chosen. If it is assumed that every new entrant starts its working stage with a shock drawn from \(\gamma ^{*}_{{\mathcal {E}}}\), then the household earnings will be independent of household age. In contrast, if every household starts its working life with the smallest endowment of efficiency labor units, then the household earnings will grow too fast with household age. Since the earnings ability is parsimoniously increasing in household age, i.e., the earnings ability depends on household age, an additional parameter, \(\phi _2\), is needed to act as a weight that averages between \(\Gamma ^{*}_{{\mathcal {R}}{\mathcal {E}}}\) and a matrix with a unity vector in its first column and zeros elsewhere. Intuitively, the role played by this second parameter is to shift the probability mass of \(\Gamma ^{*}_{{\mathcal {R}}{\mathcal {E}}}\) toward its first column.

A detailed description of the mass shifting procedure can be found in Sect. A.1 of “Appendix.” Unfortunately, the effects of \(\phi _1\) and \(\phi _2\) on the two magnitudes of interest previously mentioned are of opposite sign. Consequently, the modeling strategy to attain a pair of values for these parameters that induces magnitudes similar to those observed in the Spanish economy may be very parsimonious.

To keep the dimension of the process s as small as possible while still being able to achieve the calibration targets, a value of \(J=4\) is chosen. This means that \(J^2+J+4=24\) parameters need to be chosen. Note that \(\Gamma _{{\mathcal {S}}\mathcal {S'}}\) has not yet been imposed to be a Markov matrix. When this is done, the number of free parameters is reduced to 20.

2.2 Preferences and production possibilities

Households are assumed to derive utility from consumption, \(c_t\ge 0\), and from non-market uses of their disposable time. They also care about utility of their descendents as if it were their own utility. Consequently, households’ preferences can be characterized by the following standard expected utility function:

where the function u is continuous and strictly concave in both arguments, \(0<\beta <1\) is the subjective-time discount factor, \(\ell \) is the endowment of productive disposable time, and \(0\le h_t\le \ell \) is the labor choice. Consequently, \(\ell -h_t\) is the amount of time allocated to non-market activities by the households. Note that retirees do not work, and consequently, they derive a constant utility from non-market activities.

The functional form chosen for the households’ common utility function is given by the following expression:

where \(\sigma \) denotes the curvature of consumption, \(\varphi \) stands for the curvature of leisure (indirectly, the curvature of work) and the parameter \(\chi \) controls the disutility from work. With this utility function, the intertemporal elasticity of substitution of consumption is given by \(\frac{1}{\sigma }\), the intertemporal elasticity of substitution of leisure by \(\frac{1}{\varphi }\) and the intertemporal elasticity of substitution of labor (i.e., the Frisch elasticity of labor supply) by \(\frac{(\ell -h)}{\varphi \cdot h}\). This particular choice is widely used in this literature framework and is made because, as argued in Castañeda et al. (2003), the households in the model economy face very large changes in productivity, which, under standard nonseparable preferences, would result in extremely large variations of hours allocated to market activities. Aiming to avoid this, a more flexible functional form that is additively separable in consumption and leisure and that allows for different curvatures on these two variables is chosen. It implies that, to identify the households’ preferences, five parameters (the four that identify the utility function and the subjective time discount factor) must be chosen.

On the other hand, as far as production possibilities are concerned, an aggregate product definition, \(Y_t\), that depends on aggregate capital, \(K_t\), and aggregate labor, \(L_t\), is chosen. Note that aggregate capital is obtained by aggregating the wealth (asset position) of every household, and aggregate labor input is obtained by aggregating the efficiency labor units supplied by every household. The aggregate production function, \(Y_t=f(K_t,L_t)\), exhibits constant returns to scale. Therefore, the choice for the particular functional form here is the Cobb–Douglas production function \(Y_t=A_t K^{\alpha }_t L^{1-\alpha }_t\), where \(\alpha \) is the capital share and the total factor productivity, \(A_t\), is normalized to 1. Further, capital is assumed to depreciate geometrically at a constant rate, \(\delta \), and r and w are used to denote the prices of capital and of the efficiency units of labor before all taxes.Footnote 5 Therefore, to depict the aggregate technology, the values of two parameters, \(\alpha \) and \(\delta \), must be chosen.

2.3 Government sector

The government in the model economy taxes household income (from capital and from labor) and it uses the proceeds of taxation to make real transfers to retirees and to finance its consumption. Income taxes are described by the function \(\tau (y_t)\), where \(y_t\) denotes the household income. Public transfers to retirees are described by the function \(\omega (s_t)\).

Social security in this model economy takes the form of transfers to retirees that do not depend on past contributions made by households, i.e., pensions are assumed to be fully redistributive.Footnote 6 This is done out of computational convenience. These public pensions provide the non-working households with an insurance mechanism against the risk of living for too long; therefore, it reduces their incentives to save or accumulate assets for precautionary motives, which makes it easier to replicate the fraction of households that own very few or zero assets. This setup allows for matching the size of average public retirement pensions paid in Spain, but it qualifies the precision of the analysis in two ways. First, the overall amount of idiosyncratic risk in the model economy diminishes because the labor market history does not condition the retirement benefits. Second, it abstracts from a potentially important reason to work, since in real-world economies increasing the labor effort entitles the households to receive larger pension benefits.Footnote 7

Therefore, a government policy rule in this model economy is a specification of \(\{\tau (y_t),\,\omega (s_t)\}\) and of a process on government consumption, \({G_t}\). Since the government is running a budget balance scheme in every period, these policies must satisfy the condition \(G_t+Tr_t=T_t\), where \(Tr_t\) and \(T_t\) denote aggregate transfers and aggregate tax revenues, respectively.

The household income taxes in the model economy are described by the function:

The term within brackets is the tax function chosen by Heathcote et al. (2017) (HSV hereafter) to analyze the optimal progressivity of the tax system. Since this is the main purpose of this study, it justifies the election of such tax function for the model economy. More precisely, in this specification, \(\lambda \) determines the average taxes while \(\tau \) determines the progressivity. When \(\tau =0\), taxes are flat and equal to \((1-\lambda )y\). When \(\tau >0\), taxes are positive, and higher levels of \(\tau \) imply a greater degree of progressivity (the marginal rates exceed the average rates). When \(\tau <0\), the tax system is regressive (households with a nonnegative income would obtain a net transfer from the government). This specification has been already used by García-Miralles et al. (2019) to replicate the Spanish income tax system, and they show that the HSV specification matches almost exactly the effective average tax rates for the Spanish households.

The last term, \(\kappa y\) is added to this tax function because the Spanish government obtains tax revenues from many other sources (property, estate, consumption, and excise taxes, among others), and this model economy abstracts from these tax sources. This choice implies that, in the model economy, it is assumed that all sources of tax revenues are proportional to income, which is equivalent to say that the government uses a proportional income tax to collect all the non-income tax revenues levied by the Spanish government. This type of augment of the tax function with a proportional term is widely used in the literature (e.g., see Castañeda et al. (2003) and Díaz-Giménez and Pijoan-Mas (2019)). Including this linear specification for remaining taxes could act as a consumption tax. This makes the choice of optimal progressivity more robust, since if consumption tax is not taken into account the optimal progressivity that the model finds can vary significantly, as argued by Guner et al. (2020). Therefore, to specify the model economy household income tax function, a total of three parameter values must be chosen.

2.4 Market arrangements

In this model economy, there are no insurance markets for the household-specific shock. If insurance markets were allowed to operate this economy, the model economy would collapse to a standard representative agent model. Instead, to buffer their streams of consumption against the shocks, households in the model economy can accumulate wealth in the form of real capital, \(a_t\in {\mathcal {A}}\). The lower bound of the compact set \({\mathcal {A}}\) can be interpreted as a form of liquidity constraints, or as a solvency requirement (preventing households that derive utility from leisure from going bankrupt).Footnote 8 Finally, firms are assumed to rent factors of production from households in competitive spot markets, which implies that factor prices are given by the corresponding marginal productivities. This means that the interest rate, r, is equal to \(\alpha K^{\alpha -1}L^{1-\alpha }-\delta \), and the wage, w, is equal to \((1-\alpha )(\frac{r+\delta }{\alpha })^{\frac{\alpha }{\alpha -1}}\).

2.5 Households’ decision problem

The individual state variables are the realization of the household-specific shock, s, and the value of the asset holdings, a. The Bellman equation of the household decision problem is as follows:Footnote 9

where v is the households’ common value function. Note that household income, y, includes three terms: capital income, ar, which can be earned by every household, labor income, e(s)hw, and retirement pensions, \(\omega (s)\). Recall that \(e(s)=0\) when \(s\in {\mathcal {R}}\) and \(\omega (s)=0\) when \(s\in {\mathcal {E}}\). It is assumed that every household inherits the estate of the previous member of its dynasty at the beginning of the first period of its working life. More precisely, it is assumed that when a retiree exits the economy, it does so after that period’s consumption and savings have taken place. Then, at the beginning of the next period, the deceased household’s estate is liquidated and transmitted to the offspring.Footnote 10 Here is the key that the asset choice for next period, \(a'\), that an agent makes at t is the household’s stock wealth of its predecessor at the end of period t in the case that the predecessor is not going to be in the economy at period \(t+1\). The household policy that solves this problem is a set of functions that map the individual state into the optimal choices for consumption, end-of-period savings, and labor hours. This policy is denoted by \(\{c(a,s),\, a'(a,s),\, h(a,s)\}\).

2.6 Equilibrium

Each period the economy-wide state is a probability measure of households, \(x_t\), defined over an appropriate family of subsets of \(\{{\mathcal {S}} \times {\mathcal {A}}\}\) that counts the households of each type, and that is denoted by \({\mathcal {B}}\). In the steady state, this measure is time-invariant, even though the individual state variables and the decisions of the individual households change from one period to the next one, as shown by Huggett (1993).

Definition A steady-state equilibrium for this economy is a household value function, v(a, s); a household policy, \(\{c(a,s),\, a'(a,s),\, h(a,s)\}\); a government policy, \(\{\tau (y),\,\omega (s),\,G\}\); a stationary probability measure of households, x; factor prices, (r, w); and macroeconomic aggregates, \(\{K,\,L,\,T,\,Tr\}\), such that:

-

(i)

Given factor prices and the government policy, the household value function and the household policy solve the households’ decision problem described in Eqs. (5)–(9).

-

(ii)

Firms behave as competitive maximizers. That is, their decisions imply that factor prices are factor marginal productivities \(r=f_K(K,L)-\delta \) and \(w=f_L(K,L)\).

-

(iii)

Factor inputs, tax revenues, and transfers are obtained by aggregating over households:

$$\begin{aligned} K=\int \,a\,\mathrm {d}x;\;\;\; L=\int \,h(a,s)\,e(s)\,\mathrm {d}x;\;\;\; Tr=\int \,\omega (s)\,\mathrm {d}x;\;\;\; T=\int \,\tau (y)\,\mathrm {d}x \end{aligned}$$Every integral in the four definitions above is defined over the state space \(\{{\mathcal {S}} \times {\mathcal {A}}\}\).

-

(iv)

The goods market clears:

$$\begin{aligned} \int \,\bigg \{c(a,s)+a'(a,s)\bigg \}\,\mathrm {d}x+G=f(K,L)+(1-\delta )K \end{aligned}$$ -

(v)

The government budget constraint is satisfied: \(G+Tr=T\).

-

(vi)

The measure of households (i.e., the aggregate state variable) is stationary:

$$\begin{aligned} x(B)=\int _{B}\,\bigg \{\int _{{\mathcal {S}} \times {\mathcal {A}}}\,[\xi _{_{a'(a,s)\in {\mathcal {A}}}}\xi _{_{s\in {\mathcal {S}}}}]\,\Gamma _{{\mathcal {S}}\mathcal {S'}}\,\mathrm {d}x\bigg \}\,\mathrm {d}a'\mathrm {d}s' \end{aligned}$$for all \(B\in {\mathcal {B}}\), where \(\xi \) is the indicator function that takes value 1 if some households choose certain level of assets and belong to certain shock group and 0 otherwise. This equation is aimed to count the households and to observe whether their asset holdings distribution is stationary. The procedure used to compute this equilibrium is in Sect. C.4 of “Appendix.”

3 Calibration

The model economy is characterized by 36 parameters: 5 for preferences, 2 for production technology, 4 for government policy, and 25 for the joint process on the age of the households and on the endowments of efficiency labor units (implied by the choice of \(J=4\) possible states during the working-age or the retiree phase of the life cycle). A full list of the parameters can be shown in Sect. B of “Appendix.”

To depict the values of these parameters, 37 calibration targets (T henceforth) are needed. Of these targets, 7 are normalization conditions (NC henceforth) that identify 7 parameters, and the remaining 30 are statistics that describe relevant features of the Spanish economy. Therefore, 30 target values describing the Spanish economy are needed to identify 29 parameters. Eight of these 30 calibration targets uniquely determine the value of 8 model economy parameters. These targets will be noted as direct identification (DI henceforth). To determine the values of the remaining 21 parameters, a system of 22 nonlinear equations must be solved. This system results from equating the values of 22 model economy statistics to their empirical analogues in the Spanish economy. The method of simulated moments (MSM henceforth) is proposed to solve this system. With respect to this method, it is important to recall that each parameter being calibrated by the MSM is intended to match one target of the remaining 22, but in practice a change in one parameter could induce changes in each of the 22 targeted model statistics. It means that there is necessarily no one-to-one correspondence between parameters and targets in the MSM system. In this sense, 22 target values are intended to calibrate 21 parameters. The remainder of this section is devoted to explain in a detailed way how each parameter of the model is identified and which parameters being calibrated by the MSM are intended to match which targets. The details of the procedure used to solve this system can be found in Sect. C.3 of “Appendix.”

Model period One important decision to be made is the length of the model period. It is set to be equal to one year since this is also the length of a tax period in Spain. Further, one year is also the length of the data collection period of the administrative panel dataset of tax returns used in this analysis. Finally, 2015 is chosen as the calibration year, as it is the last year with data availability of this particular data source. This means that the most updated estimate of the progressivity of the personal income tax at the household level depicts the situation in 2015.

Normalization conditions The household endowment of disposable time is an arbitrary constant and is chosen to be \(\ell = 3.2\) [T1-NC (Target 1, Normalization Condition)], as standard in the related literature.Footnote 11 The possible states in which a household can stay during its working-life or retirement are \(J=4\) [T2-NC]. It means that the possible states of endowment of efficiency labor units will be 8: \(\left[ e(1),e(2),e(4),e(5),e(6),e(7),e(8)\right] \). Recall that the endowment of efficiency labor units is zero for retired households, i.e., \(e(s)=0\) for \(s\in {5,6,7,8}\). This basically implies that the endowment vector of 8 possible states is characterized by 4 parameters (those related to working-age agents). In addition, the endowment of efficiency labor units of the least productive households is normalized to be \(e(1)=1\) [T3-NC]. Finally, since matrix \(\Gamma \) is a Markov matrix, its rows must add up to one. This property imposes four additional normalization conditions on the rows of \(\Gamma _{\mathcal {EE}}\) [T4-NC to T7-NC]. The assumptions about the structure of the matrix \(\Gamma \) imply that once submatrix \(\Gamma _{\mathcal {EE}}\) has been appropriately normalized, every row of \(\Gamma \) adds up to one without imposing additional restrictions. In this regard, the calibration algorithm normalizes the diagonal elements of \(\Gamma _{\mathcal {EE}}\), i.e., \(\Gamma _{\mathcal {EE}_{1,1}}\), \(\Gamma _{\mathcal {EE}_{2,2}}\), \(\Gamma _{\mathcal {EE}_{3,3}}\), and \(\Gamma _{\mathcal {EE}_{4,4}}\). For instance, the calibration algorithm calculates the first diagonal element of \(\Gamma _{\mathcal {EE}}\) as \(\Gamma _{\mathcal {EE}_{1,1}}=1-\Gamma _{\mathcal {EE}_{1,2}}-\Gamma _{\mathcal {EE}_{1,3}}-\Gamma _{\mathcal {EE}_{1,4}}-p_{r}\), and analogously for each of the first four rows of \(\Gamma \). The normalization condition could be placed in a different element of each row of the submatrix \(\Gamma _{\mathcal {EE}}\), but the diagonal elements are chosen to be normalized out of computational convenience since it is known beforehand that most of the weight of the transition submatrix between working states is on the diagonal. Note that normalizing the diagonal element of \(\Gamma _{\mathcal {EE}}\) the algorithm is less likely to deliver a negative value of it, since the rest of parameters involved in the normalization of the row (\(\Gamma _{\mathcal {EE}_{1,2}}\), \(\Gamma _{\mathcal {EE}_{1,3}}\), \(\Gamma _{\mathcal {EE}_{1,4}}\), and \(p_{r}\)) normally take values close to zero. Thus in terms of maintaining the constraints on \(\Gamma _{\mathcal {EE}}\) (all elements being between zero and one and rows summing up to one) required for it to be a transition matrix, the algorithm is less likely to be throwing out parameter vectors when estimating the calibrated values because they failed to meet these constraints.

3.1 Macroeconomic aggregates and demographic targets

Ratios The target value for the capital-to-output ratio, K/Y, is 4.25 [T16-MSM], the capital income share, \(\alpha \), is 0.48 [T8-DI], and the target value for the investment-to-output ratio, I/Y, is \(21.94\%\) [T9-DI]. The target value for the capital- to-output ratio is obtained by dividing 247,523€, which was the average household net wealth in Spain in the calibration reference year according to the Bank of Spain (2017, 2019), by 58,230€, which was per household gross domestic product in Spain in the calibration reference year according to Eurostat (2020b, 2020c) and the Spanish National Institute of Statistics (2016) (INE, its acronym in Spanish).Footnote 12 The parameter controlling for the subjective time discount factor, \(\beta \), is calibrated to match this capital-to output-ratio. The target value for the capital income share is obtained by subtracting the labor income share from a total measure of 1. The value for the labor income share was 0.52 in Spain in the calibration reference year, according to data from EU KLEMS (2020). Thus the capital income share is directly identified as \(\alpha =0.48\). To calculate the value of the target for I/Y, investment is defined as the sum of gross private fixed domestic investment, change in business inventories, and 75% of the private consumption expenditures in consumer durables using data for the calibration reference year from the Spanish National Institute of Statistics (2020).Footnote 13 Further, note that the rate of depreciation of capital, \(\delta \), follows immediately from \(\delta =I/K\) in stationary general equilibrium, hence it is directly identified as \(\delta =(I/Y)/(K/Y)=0.0516 \). These choices amount to 3 targets.

Allocation of time and consumption General equilibrium heterogeneous agents models are built to asses counterfactual economies from both aggregate and individual perspective. To calibrate the model economy in the individual perspective, the intertemporal elasticity of substitution of consumption, determined by \(\sigma \), the disutility from work, determined by \(\chi \), and the Frisch elasticity of labor supply, determined by \(\varphi \), are crucial parameters.

For the curvature of consumption, as usual in many papers, a value of \(\sigma =1.5\) is chosen [T10-DI]. It induces a elasticity of intertemporal substitution of consumption of \(\frac{1}{\sigma }=\frac{1}{1.5}=0,66\).Footnote 14 The value chosen for \(\sigma \) falls within the range (1-3) that is standard in the literature for the curvature of consumption. For example, the calibration–estimation exercise by Pijoan-Mas (2006) reports a value of 1.46, Pijoan-Mas and González Torrabadella (2006) encounter a value of 1.23, and Heathcote et al. (2010) finds a value of 1.44. In addition, Castañeda et al. (2003) and Díaz-Giménez and Pijoan-Mas (2019), research works that employ an utility function similar to the one herein presented, also identify directly the curvature of consumption, \(\sigma \), as 1.5. This choice gives one additional target.

The parameter of the utility function controlling for the relative share of consumption and leisure, \(\chi \), is calibrated by the MSM so as to match average share of disposable time allocated to market activities by the households. This statistic is targeted to be \(H/\ell =30.83\) percent [T17-MSM]. The choice is based on the average daily length of time devoted to paid work by working agents in Spain in the calibration reference year according to the Spanish National Institute of Statistics (2011). It gives one more target. On the other hand, as it will be explained below, the parameter of the curvature of leisure (implying the Frisch elasticity of labor supply), \(\varphi \), is selected within the range of values considered in the literature [T11-DI]. In this sense, some restrictions are placed in the values that the curvature of leisure, \(\varphi \), could take, which accounts for one additional target. The parameter \(\varphi \) is particularly important in the model, as it determines the elasticity of the labor supply and thus shapes the response of the labor supply to tax changes. A higher (lower) Frisch elasticity of labor supply will make the households react more (less) to tax changes. But there is still a lot of controversy in the literature about how large this elasticity should be. The early estimates of MaCurdy (1981), Altonji (1986), and Blundell and MaCurdy (1999) indicated that the labor supply elasticity was very small (much smaller than 0.5). However, these estimates are typically obtained for prime aged male actively engaged in the labor market, while elasticities for females are much larger, as shown by Kumar (2005). Furthermore, as pointed out by Pijoan-Mas and González Torrabadella (2006), once one also considers the extensive margin the estimates for the elasticity might even be larger. For example, Nobel laureate Prescott (2004) defends a Frisch elasticity of 1.50 for the labor supply. More specifically, by focusing on research works that are similar to the one presented in this paper and that try to evaluate fiscal reforms in the Spanish economy through macro- and micro-models, one can observe that the disparity in the values of the Frisch elasticity of labor supply is also a common element. For instance, Guner et al. (2020) set the Frisch elasticity of labor supply to 0.5, which implies a curvature of leisure, \(\varphi \), equal to 4.25 (when measured at the average amount of hours worked). On the other hand, Pijoan-Mas and González Torrabadella (2006) and Díaz-Giménez and Pijoan-Mas (2019) estimate in their model economies that the elasticity of the intertemporal substitution of labor is around 1.8, which would translate into curvatures of consumption of \(\varphi =1.15\). Therefore, the parameter \(\varphi \) will be calibrated in the model economy such that it falls within the range observed in the literature applied to the Spanish economy, i.e., Frisch elasticities of labor supply ranging from 0.5 up to 1.8. Making use of this strategy, as it will be shown in Table 2 of Sect. 3.4, the value of the curvature of leisure will be given by \(\varphi =2.65\). It would imply that the model economy would present a Frisch elasticity of labor supply equal to \(\frac{(\ell -h)}{\varphi \cdot h}=\frac{(3.2-0.99)}{2.65 \cdot 0.99}=0.85\) (when evaluated at its average). This value is in line with Imai and Keane (2004), Domeij and Flodén (2006) and Chetty (2012), who argue that a value slightly greater than 0.5 is reasonable. In addition, the labor supply of the model economy will be very similar to the one encountered by Pijoan-Mas (2006). It should be also noted that a labor supply elasticity of 0.85 falls in the middle of the value spectrum found in the literature devoted to the Spanish economy, which reinforces the strategy chosen to calibrate the parameter \(\varphi \).

Age structure of the population The expected duration of working-lives in Spain is targeted to be 35 years [T12-DI], according to Eurostat (2020a). The expected duration of retirement in Spain is targeted to be 22.8 years [T13-DI], according to the OECD (2015, 2017).Footnote 15 These values serve as two more targets that directly identify the probability of retiring, \(p_{r}=\frac{1}{35}=0.0286\), and the probability of surviving, \(p_{s}=1-\frac{1}{22.8}=0.9561\), respectively.

Life cycle profile of income To replicate the life cycle profile of income in Spain in the model economy, the ratio of the average annual wage of agents between ages 45 and 49 to that of agents between ages 25 and 29 is the target value [T18-MSM]. The transition process between retirement and working-age states will be therefore calibrated in such a way that will reflect the observed differences in earnings ability between new entrants and senior workers. In 2015, the value of this statistic in Spain was 1.56, according to the Spanish National Institute of Statistics (2017). This provides an additional target which is intended to calibrate by the MSM the controller of the life cycle earnings profile, i.e., the parameter \(\phi _1\).

Intergenerational transmission of earnings ability To replicate the intergenerational correlation of income encountered in Spain in the model economy, the target is the correlation between the average income of one generation and the average income of its immediate descendents. Llaneras et al. (2020), in their Atlas de Oportunidades project, developed a database at the household and individual level originating from the Spanish State Agency of Tax Administration (AEAT, its Spanish acronym). In this database, 2.7 million young people in 2016 can be followed and for each of them their current income and the income of their parents’ home (in the period 1980–1990) can be obtained. This database is the most updated attempt to study the social mobility in Spain and the intergenerational income correlation between sons and daughters with respect to their parents’ income. Making use of such prominent database, the intergenerational correlation of income at the household level in Spain is estimated to be 0.50 [T19-MSM].Footnote 16 This translates into one more target value which is intended to calibrate by the MSM the controller of the intergenerational persistence of earnings, i.e., the parameter \(\phi _2\).

3.2 Government policy

The parameters of the model economy household income tax are chosen so that the government collect the total tax revenues observed in the Spanish economy, which were 33.63% of the GDP in Spain in the calibration reference year, according to the OECD (2020). In the model economy, these revenues must be entirely spent by the government, i.e., the government of the model economy must balance its budget. This means that the output shares of government consumption, G/Y, and government transfers, Tr/Y (the two government expenditure items in this model economy), are required to add up to 33.63%, which was the GDP share of total tax revenues, T/Y, in Spain in the calibration reference year, as previously mentioned. The target value for the transfers-to-output ratio in the model economy is 11.36% [T20-MSM], which corresponds to the GDP share accounted for by social security contributions in Spain in the calibration reference year, according to the OECD (2020). This value is chosen so because the retired agents in the model economy receive a lump-sum transfer that, once it is aggregated, must be the same as the social security contributions that were paid by the working-age households. This choice means that the residual share for government expenditures to GDP amounts to 22.27% (\(=33.63\%-11.36\%\)) [T21-MSM], which is the target for the G/Y ratio in the model economy. This is consistent with World Bank (2020b) data for Spain for the calibration reference year, which present a general government final consumption expenditure (as % of GDP) of 22%.

The personal income tax function of the model economy is aimed to mimic the progressivity of the Spanish effective personal income taxes. This objective is achieved by shaping the tax function with an augmented version of the HSV specification, as it was similarly done by García-Miralles et al. (2019). The specification used in the present analysis was introduced in Eq. 4. To identify it, the values of parameters \(\lambda \), \(\tau \), and \(\kappa \) must be chosen.

Following the estimation strategy proposed by García-Miralles et al. (2019), the parameters \(\lambda \) and \(\tau \) can be directly estimated using an administrative panel dataset containing a (stratified) random sample of tax returns.Footnote 17 This dataset is provided by the Spanish State Agency of Tax Administration (2019) and contains a very detailed account of income from different sources, tax benefits, tax liabilities, and sociodemographic characteristics for a sample that accounts for a 14% of the population.Footnote 18 The last update of this panel dataset at the household level covers the tax returns in 2015. Hence, the estimated progressivity of the tax system depicts the situation in that year. The estimation results in parameters \(\lambda \) and \(\tau \) taking values 0.8924 and 0.1146 [T14-DI and T15-DI], respectively. These two targets result from directly imposing that the shape of the model economy’s tax function coincides with the shape of the estimated HSV specification. As it can be shown in Fig. 1, the fitting of the estimated HSV tax function to the 2015 household data is very precise, which justifies the choice of this specification for the model economy.

Fitting of the HSV specification to the data

Finally, we just need to choose the values of the parameter \(\omega \), which stands for the lump-sum transfers to retirees, and the remaining parameter of the households’ income tax function of this model economy that has not been already chosen, \(\kappa \). More precisely, \(\omega \) is chosen so as to achieve that the model economy transfers-to-output ratio, Tr/Y, mimics the value observed in the Spanish economy. On the other hand, the value of \(\kappa \) is chosen so that the government expenditures-to-output ratio in the model economy, G/Y, matches that observed amount in the Spanish economy. Note that the government in this model economy only allocates its spending on social security transfers and government spending. Then, because the two above parameters are chosen to match these two targets, it can also be said that the parameter \(\kappa \) is chosen so as to match the ratio of total tax revenues to output, T/Y, observed in the Spanish economy. This is equivalent to stating that the value of \(\kappa \) is selected such that the government in the model economy runs a budget balance policy in equilibrium, i.e., \(G+Tr=T\). Indeed, the value of \(\kappa \) is only completely calibrated when the general equilibrium of the economy is found, since such parameter acts as price solver of the general equilibrium by ensuring that the government runs a budget balance policy. These choices, in conjunction with those that mimic the shape of the model economy’s tax function, represent 4 more targets.

3.3 Distributions of income and wealth

The aforementioned conditions specify a total of 21 targets (7 normalizations and 14 target values observed in the Spanish economy) out of a total of 37 targets. To solve this model economy, one must choose the value of 36 parameters. Therefore, 15 additional parameters must be identified. These parameters will be calibrated by the MSM (jointly with the previously mentioned ones that will also enter the MSM calibration strategy) so as to match 16 additional targets covering the Spanish distributions of income and wealth are added: (i) the Gini coefficients [T22-MSM and T23-MSM]; (ii) the income and wealth shares of the households concentrated between percentiles 1 to 40, 40 to 60, 60 to 80, and 80 to 100 [T24-MSM to T31-MSM]; and (iii) the income and wealth shares of the households concentrated between percentiles 90 to 95, 95 to 99, and the top 1% [T32-MSM to T-37-MSM]. The same calibration procedure can be found in Castañeda et al. (2003) and Díaz-Giménez and Pijoan-Mas (2019). These 16 calibration targets related to the wealth and income distributions are intended to estimate by means of the MSM 3 out of 4 endowments of efficiency labor units (e(1), e(2), and e(3), since e(1) is normalized to be 1) and the off-diagonal elements (12 elements) of the submatrix driving the transition between working states, \(\Gamma _{\mathcal {EE}}\). (The diagonal elements originate from a normalization procedure, as explained before.)

For wealth distributional statistics, the 2015 household data to get the target statistics come from a linear interpolation between statistics derived from the 2014 and the 2017 waves of the Spanish Survey of Household Finances, a very influential survey conducted by the Bank of Spain (2017, 2019) detailing the household balance sheets and their wealth positions. Since the 2017 wave of the Spanish Survey of Household Finances is not completely available yet, some information for such year is directly extracted from the 2017 wave of European version of it, the Household Finance and Consumption Survey, which is conducted by the European Central Bank (2020). As for the income distributional statistics, the 2015 household data to get the target statistics come from the aforementioned administrative tax data provided by the Spanish State Agency of Tax Administration (2019).

3.4 Calibration outcomes

This subsection presents the complete parametrization of the model economy. The values of the 36 parameters are presented here in two tables. The calibrated parameters characterizing the stochastic process of the endowment of efficiency labor units are reported in Table 1, while the rest of the calibrated parameters characterizing the model economy are shown in Table 2. Finally, Table 3 displays the fitness of the model economy, where the success of the parametrization to replicate key selected characteristics of the Spanish economy can be observed.

Stochastic process of endowment of efficiency labor units With the exception of the first endowment, e(1), and the diagonal elements of the submatrix \(\Gamma _{\mathcal {EE}}\), which are determined by normalization, the parameters presented here are estimated/calibrated by means of the MSM in order to match the targets related to the wealth and income distributions presented in the previous Subsection. This means that, of the 20 parameters that this process has, 5 are identified through normalization and 15 through MSM estimation jointly with the rest of the model economy parameters that are also estimated by this procedure.

The process, as shown in Table 1, presents strong skewness, persistence of the shocks, fat right tail, and nonlinear dynamics. It is important not to take this process literally, since it is an approximation that represents everything that is not known about the model economy. The relative endowments of efficiency labor units are reported in the second column of Table 1 and the invariant measures of each type of working-age households are in the third column. The endowments of workers are calibrated such that the endowment of the least lucky (in terms of endowments of efficiency labor units) household is 1 (normalization). Then, it can be observed that the luckiest workers in the model economy are 90 times as lucky as the unluckiest ones. The stationary distribution shows that each period 15% of the workers are very unlucky and draw state \(s=1\). The working agents are mainly concentrated around state \(s=2\), with two out of three workers receiving this productivity shock each period. The transition probabilities between the working-age states are reported in the last four columns of the table. Here it can be noted that agents in states \(s=3\), \(s=4\), and especially \(s=1\) have higher probability of moving to \(s=2\) than to other possible working states. However, each period only one out of every 100 workers is extremely lucky and draws state \(s=4\). Only very rarely workers whose current state is \(s\ne 4\) will make a transition to state \(s=4\). Finally, there is a group of households that are not that lucky in comparison with those households that draw state \(s=4\), but they are not as unlucky as the ones who draw states \(s=1\) or \(s=2\). This group of households accounts for 18% of the workers drawing state \(s=3\) each period. The concentration of the invariant distribution of working households in the first two states is typically higher in the literature devoted to match the characteristics of the US economy with this type of models, as it can be shown in Castañeda et al. (2003) and Díaz-Giménez and Pijoan-Mas (2019). Nevertheless, since the level of income inequality in Spain is much lower, this weight decreases in order to generate an income distribution with higher income-shares in the not-top percentiles.

Note that Table 1 only represents the submatrix \(\Gamma _{\mathcal {EE}}\). This submatrix drives the transition of working households between working states. Recall from expression (1) that this particular submatrix is only the upper-left part of the overall transition matrix \(\Gamma \), but there are many other possible transitions between working to non-working states and vice versa. The complete transition matrix between all possible states of the model economy, \(\Gamma \), and the complete invariant distribution of households, \(\gamma ^{*}\), are presented in Table 8, in Sect. A.2 of “Appendix.” This complete Markov Chain transition matrix is what features the stochastic process that jointly defines the age and the endowment of labor efficiency units of each household.

Other parameter values Every other parameter of the model economy is presented in Table 2. Jointly with the calibrated values for the parameters, it can be observed which calibration strategy was used to identify each of them. Among these parameters, 8 are directly identified to match some targets, 2 are normalization conditions, and 6 parameters were calibrated by solving a system of 22 nonlinear equations (by the MSM) jointly with those calibrated by the same method in the stochastic process of endowment of efficiency labor units. In addition, in case that a parameter would have been calibrated to match some target statistic of the Spanish economy, it is also shown in the last columns of the table. These last columns indicate to which target statistic each parameter points out.

Fitness of the model economy The statistics that describe the main aggregate and distributional features of the Spanish and the baseline model economies are reported in Table 3. In this table, it can be noticed how well the selected parametrization matches the calibration targets. These results confirm that overall the model economy succeeds in replicating the most relevant features of the Spanish economy in much detail. This result is particularly promising since it delivers a very well suited benchmark model to evaluate several potential reforms of the tax and transfers system.

4 Optimal progressivity

This study aims to analyze what the optimal progressivity level of the personal income tax in Spain would be. Namely, it makes a comparison between the calibrated baseline model economy with the current estimated level of progressivity (\(\tau =0.1146\)) and a grid of several alternative economies exhibiting different progressivity levels. In every alternative scenario, the progressivity parameter \(\tau \) is updated to a different value and a new general equilibrium for each reformed model economy is calculated.

But how should the reform be designed? The literature has conventionally employed two types of criteria when evaluating potential tax reforms through theoretical models. On the one hand, the most common choice within this type of research has been to assess reforms that are revenue-neutral. That is, reforms in which a change in taxation leaves the government’s tax revenue levels unchanged, and therefore, the levels of government expenditure, G, and transfers, Tr. In contrast, another body of academic literature in this area has focused on tax reforms that maintain the same level of tax burden on the economy (i.e., on the income-average household). That is, the government must design a tax reform in such a way that the ratio of tax revenues to GDP, T/Y, remains constant. This is the approach chosen in the study herein presented. In this sense, this paper evaluates tax reforms that change the level of tax progressivity without changing the average tax rate (as measured from aggregate data). In addition, the design of the reform must respect the government’s spending structure. In other words, the reform must hold not only the T/Y ratio unchanged, but also the output shares of the transfers, Tr/Y, and of the government expenditure, G/Y. Being output, Y, a measure of the size of the economy, it would imply that for each potential size of the economy the government would offer the same relative amount of education, health, coverage to non-workers, pensions to retirees, etc.

In practice, it translates into every reformed economy being designed such that several conditions are satisfied: (i) the markets clear and (ii) the government runs a balanced-budget policy (iii) while keeping pensions and government expenditure shares of output fixed at baseline levels. Each reformed economy with a different progressivity level exhibits a new interest rate, r, and new wage, w, such that the goods and assets markets clear. This particular reform design implies that the government must choose in each reformed economy a new average level of taxes, \(\lambda \), such that, with a certain progressivity level, \(\tau \), it balances its budget and leaves the ratios \(Tr/Y=11.24\%\) (varying transfers to retirees, \(\omega \), so as to match this level) and \(G/Y=22.27\%\) fixed at their baseline levels. It means that in every reformed economy, the combination of \(\lambda \), \(\tau \), and \(\omega \) chosen by the government must induce the same output-share accounted for by personal income tax revenues as in the baseline economy, i.e., \(T/Y=33.51\%\). A more involved explanation of the general equilibrium calculation in a reformed economy can be accessed in Sect. C.4.1 of “Appendix.”

After calculating a grid of several alternative economies exhibiting different progressivity levels, \(\tau \), ranging from 0.00 to 0.50, the optimal reform of the personal income tax progressivity would be the one that maximizes the aggregate welfare gains. Note that economies with negative progressivity, \(\tau <0\), are not here considered as they would induce a regressive income tax system, which exceeds the scope of the analysis. Further, economies with progressivity \(\tau >0.5\) are not here reported because they always present enormous aggregate welfare losses and the focus of the analysis should be put in the reformed economies that are closer to the baseline economy and to the optimal one.

4.1 Welfare changes and optimal progressivity level

Which economy with level of progressivity from \(\tau =0.00\) to \(\tau =0.50\) results in a steady state with higher aggregate welfare?Footnote 19 Are these aggregate welfare changes mainly driven by the change in the tax scheme? Or do they principally arise from induced shifts in the distribution of households (distributional effects) or in the prices of the economy (general equilibrium effects)? How are these welfare changes distributed across households? A Benthamite social welfare function is used to answer these sort of concerns. The Benthamite social planner maximizes a welfare function that gives identical weights to every household in the economy. Consequently, when the utility function is concave, equal sharing is the welfare-maximizing allocation. It should be noted that the welfare outcomes here presented emerge from a comparison between the welfare derived from different steady state allocations. The present work remains silent about the transitions between these steady states.

4.1.1 Aggregate welfare changes and selection of the optimal progressivity level

To carry out the welfare comparisons, let \(v_{BE}(a,s,\bigtriangleup )\) be the equilibrium value function of a household of type (a, s) in the baseline model economy, whose equilibrium consumption allocation is changed by a fraction \(\bigtriangleup \) every period and whose leisure remains unchanged. Formally,

where \(c_{BE}(a,s)\), \(h_{BE}(a,s)\), and \(a'_{BE}(a,s)\) are the solutions to the households’ decision problem defined in expressions (5) to (9). Next, the welfare gain of living in the steady state of a reformed economy, \(E_{\tau }\), for \(\tau =\{0.00,\ldots , 0.50\}\), is defined as the fraction of additional consumption, \(\bigtriangleup _{\tau }\), that must be given to, or taken away from, the households of the baseline economy so that the aggregate steady-state welfare in the reformed economy \(E_{\tau }\) is the same as in the baseline economy \(E_{BE}\). Formally, \(\bigtriangleup _{\tau }\) is the solution to the following equation:

where \(v_{\tau }\) and \(x_{\tau }\) are the equilibrium value function and the equilibrium stationary distribution of households in the reformed economy, \(E_{\tau }\).

Aggregate welfare change

The aggregate welfare gains or losses associated with each progressivity level are depicted in Fig. 2. It can be here observed that any reform that increases the progressivity level from the current level (current level, baseline level, or “actual level” are used interchangeably), \(\tau =0.1146\), up to levels of \(\tau =0.37\) would result in aggregate welfare gains measured in percent changes of average household consumption. In this regard, the optimal reform of the progressivity level of the Spanish personal income tax would be encountered for \(\tau =0.23\). An equivalent variation in consumption of 3.08% would be found in such optimal case. This means that, from a Benthamite perspective, the steady state generated by a reform of implementing a progressivity level of \(\tau =0.23\) and increasing the average level of taxes accordingly up to \(\lambda =1.18\) would be largely preferred to the steady state under the actual scenario (i.e., \(\tau =0.1146\) and \(\lambda =0.8924\)). Indeed, the consumption of the average household of the model economy would need to be increased by 3.08% in every period and in every state for the social planner to be indifferent between the steady-state allocation implied by the actual progressivity level and the steady-state allocation that results from establishing a progressivity level of \(\tau =0.23\) and increasing the average level of taxes accordingly up to \(\lambda =1.18\).Footnote 20 Therefore, it can be deduced that implementing levels of progressivity lower than \(\tau =0.1146\) or higher than \(\tau =0.37\) would generate losses of aggregate welfare according to this setup.

4.1.2 A decomposition of the aggregate welfare changes

To improve the understanding of the results from an aggregate welfare change perspective, it is useful to decompose the aggregate equivalent variation in consumption previously presented. In order to do so, two additional measures of equivalent variations in consumption are defined. First, a particular equivalent variation in consumption is computed so that it makes the households indifferent between the baseline economy, \(E_{BE}\), and the optimally reformed economy, \(E_{0.23}\), ignoring changes in the equilibrium distribution of households across value function levels. Let \(\bigtriangleup _{0.23}^{a}\) be such variation, which is defined as follows:

Note that the aggregate welfare of such hypothetical economy is calculated using the equilibrium price vector of the optimally reformed economy, \((r_{0.23},w_{0.23})\), while the equilibrium stationary distribution is calculated using that of the baseline model economy, \(x_{BE}\).

Second, another particular equivalent variation in consumption is computed so that it makes the households indifferent between the baseline model economy, \(E_{BE}\), and the optimally reformed economy, \(E_{0.23}\), ignoring both changes in the equilibrium distributions of households across value function levels and changes in the size of the economy. Let \(\bigtriangleup _{0.23}^{b}\) be such variation, which is defined as follows:

Note that the aggregate welfare of such hypothetical economy is now calculated using both the equilibrium stationary distribution, \(x_{BE}\), and the equilibrium price vector, \((r_{BE},w_{BE})\), of the baseline model economy.

These two additional equivalent variations in consumption allow for decomposing the total equivalent variation in consumption defined in expression (11) as follows:

The first term (1) of the right-hand side in Eq. (14) measures the aggregate welfare changes that are due to the reshuffling of resources between the households and ignores both general equilibrium effects of the optimal reform and changes in the distribution of households, i.e., it measures the welfare changes stemming from pure changes in the tax system. The second term (2) shows the added aggregate welfare change triggered by changes in equilibrium prices, i.e., it measures the general equilibrium effects of the optimal reform. The last term (3) measures the additional aggregate welfare change associated with changes in the equilibrium distribution of households across value function levels.

The decomposition results are presented in Table 4. It is certainly interesting that most of the welfare gains are obtained by direct improvements in the tax system. It means that most of the aggregate welfare gains come from poorest households facing lower effective income tax rates and richest households affronting higher effective income tax rates. In contrast, general equilibrium effects of setting the optimally reformed economy and effects resulting from shifts in the equilibrium distribution of households across income levels show a welfare loss, but these losses are that small that together cannot overpass the welfare gains coming from the pure reform of the tax and transfers system, jointly resulting in aggregate welfare gains. The reform provokes a shrinkage in wages (w declining from 1.95 to 1.77 in the model) and an increment in the interest rate (r rising from 5.99 to 7.20% in the model), both reactions making the aggregate welfare change associated with equilibrium prices be negative. When it comes to welfare changes resulting from changes in the equilibrium distribution of households across income levels, these changes are negative, although they are almost zero. It means that there will be a larger mass of households at lower income levels. However, despite these effects, the change in aggregate welfare is largely positive, showing how powerful such reform of the tax system is. This shows and reinforces the optimality of raising the progressivity level of the personal income tax in terms of aggregate welfare.

4.1.3 Welfare changes by household types

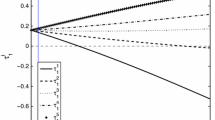

The welfare gains and losses resulting from comparing the baseline model economy, \(E_{BE}\), and the optimally reformed economy, \(E_{0.23}\), are decomposed for different types of households in the spirit of Díaz-Giménez and Pijoan-Mas (2019). In the model economy, there are as many households as there are \(\{a,s\}\) pairs in the individual state space. To calculate the welfare changes at each point in the state space, \(\bigtriangleup _{0.23}(a,s)\), the following equation is solved.

The average of these individual welfare changes for various decile groups of households are reported in Fig. 3.

Sorting by wealth The households are here sorted by their asset holding positions and the welfare gains are computed as an average over every household (i.e., over every pair of states \(\{a,s\}\)) belonging to a certain group. The division of the wealth distribution in ten deciles leaves groups of households accounting for ten percentile points each. Looking at Panel A, ranking every household by wealth, it can be seen that households within percentile 10 and percentile 70 are those that benefit from the reform, being these welfare gains decreasing in wealth. Contrarily, households in the two top wealth deciles and, curiously, households in the lowest wealth decile are the ones that would experience welfare losses with the reform. But what are the driving forces behind these welfare changes by wealth decile? A deeper understanding of it could be learned from observing Panels B and C.

First, the positive welfare variation within the 2nd and the 7th wealth deciles could be mainly explained by the welfare gains experienced by (ii) non-working households and (ii) the least productive working households populating those deciles of the wealth distribution. The welfare changes of retired households (those receiving shocks \(s=5\) to \(s=8\)) are reported in Panel C. Here it can be noticed that every non-working household located within percentiles 10 and 80 of the wealth distribution experiences welfare gains, with these gains decreasing when the household becomes wealthier. These retired households in this part of the wealth distribution benefit from the reform because their income (who is compounded by transfers, \(\omega \), and returns from capital) is so low that is taxed at a lower rate due to a higher progressivity level. In addition, working households located within percentiles 10 and 80 of the wealth distribution and receiving the lowest endowments of efficiency labor units (\(s=1\) and \(s=2\)) also experience welfare gains from the reform, as shown in Panel B. They particularly benefit from a more progressive tax system that levies less taxes on the lowest earnings. Although it is observed that working households receiving a large productivity shock (\(s=3\) and especially \(s=4\)) are those who are most negatively affected by the reform (since they face a higher income tax rate due to a more progressive tax system), they only account for a small fraction of the household stationary distribution, thus resulting in aggregate positive welfare changes of working households populating the wealth distribution within its 10th and 80th percentiles.