Abstract

The rising trend in the capital-output ratio and the productivity slowdown have put capital back in the economist’s agenda. This paper contributes to the debate by providing new estimates of net capital stock and services for Spain over the last 170 years. The net capital (wealth) stock-GDP ratio rose over time and doubled in the last half a century. Capital services grew fast over the long run accelerating in the 1920s and from the mid-1950s to 2007. Until 1975, its acceleration was helped by an increase in the “quality” of capital. Capital deepening proceeded steadily, accelerating during 1955–1985 and slowing down thereafter for expanding sectors attracted less investment-specific technological progress. Although capital consumption rose over time, the rate of depreciation fell from 1970 to 2007 as new capital goods’ relative prices declined due to embodied technological change.

Similar content being viewed by others

Notes

By consistent and integrated estimates, Oulton and Wallis (2016) mean a common dataset and a common set of assumptions in the construction of long-run estimates of capital stock and capital services.

Conference Board (2020) follows the same practice. As a sensitivity test, we have replicated the estimates of net capital stock using six, rather than four, types of assets (that is, considering, biological resources and intellectual property products separately) from 1980 onwards. No trend discrepancies are found between the two set of estimates even though the 6 asset estimates exhibit a slightly lower level (see Figures A5 and A10 in Online Appendix C).

The CFM approach is widely used to reconstruct GFCF series in present-day developing countries (Conference Board, 2017). Also, in the Penn World Tables 9.1, in the absence of direct estimates, investment in an asset is assumed to vary with the economy-wide supply (production + imports − exports) (Feenstra et al. 2015, updated).

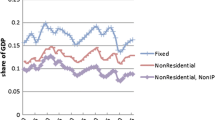

Alternative estimates using the private consumption deflator provide similar results.

These service lives are in line with those used by Pérez et al. (2019). Alternative estimates have been computed with another set of longer average service lives: 70 years (dwellings), 50 years (other construction), and 20 years (transport equipment and machinery). Although longer service lives increase the gross stock and reduce depreciation, and hence, deliver a larger net capital stock, the comparison between the two set of estimates reveals minor differences over time. A third set of estimates has been derived by combining the longer average lives set for 1850-1958 and the shorter average lives set for 1959–2019. Interestingly, the result is lower growth of aggregate capital stock than when the shorter lives set is employed for the entire time span. This finding may be attributed to the fact that the set of average assets lives for the pre-1958 period assigns larger weight to slower growing assets and, consequently, result in lower net capital stock. (See the resulting alternative Net Capital Stock/GDP ratios in Figure A11 in Online Appendix C).

Hulten and Wykoff’s (1981) implicit R values were also used in Prados de la Escosura and Rosés (2010). Alternative estimates have been obtained using a double declining balance (T = 2) and the same average service lives, with the resulting depreciation rates of 3.3%, 5.0%, 13.3%, and 13.3% for each of the four asset types. Figure A12 in Online Appendix C compares the net capital stock derived alternatively with the double declining balance and Hulten and Wykoff’s R values, revealing that the net capital stock derived with the double declining balance is lower as the depreciation rates are larger for the same average lives of assets, and so is the consumption of fixed capital (Figure A13).

The OLS regression results are (with standard error in parentheses),

$$\begin{aligned} { \ln }({\text{Dwellings}}) & = - 5. 7 5+ 1. 2 3\;{ \ln }({\text{GDP}}) \\ & \quad (0. 9 9 5)\;(0.0 9 5)\quad {\text{Adj}}.\;R^{ 2} = 0. 70 \\ \end{aligned}$$$$\begin{aligned} { \ln }({\text{Other}}\;{\text{Construction}}) & = - 1 1. 2 3+ 1. 70{ \ln }({\text{GDP}}) \\ & \quad ( 1. 2 7 1)\;(0. 1 2 1) \quad {\text{Adj}}.\;R^{ 2} = 0. 7 4\\ \end{aligned}$$$$\begin{aligned} { \ln }({\text{Machinery}}) & = - 2 9.0 7+ 3. 1 9 {\text{ ln}}({\text{GDP}}) \\ & \quad ( 1.0 6 2)\;(0. 10 1) \quad {\text{Adj}}.\;R^{ 2} = 0. 9 3\\ \end{aligned}$$$$\begin{aligned} { \ln }({\text{Transport}}\;{\text{Equipment}}) & = - 1 7. 1 8+ 2.0 7 {\text{ ln}}({\text{GDP}}) \\ & \quad ( 2. 7 5 5)\;(0. 2 6 3)\quad {\text{Adj}}.\;R^{ 2} = 0. 4 7\\ \end{aligned}$$The yearly rates assumed are −2.75% for other construction and −5.8% for machinery, following Prados de la Escosura and Rosés (2010). Although the destruction, as a share of net capital stock, is lower in the new estimates, 5% versus 7%, a fact that derives from the use of different asset average service lives and from methodological differences in the computation of the capital stock.

The formula used is 100 * (natural log X − natural log Y), being X the new estimates and Y, Ivie and INE figures, alternatively.

Cf. Young (1995: 650-1) for similar results in the cases of South Korea and Taiwan.

Thus, the endogenous, ex-post rate of return for every period is computed by equating capital compensation Gt plus capital-related taxes on production T tK to the total user costs of capital Ut

$$G^{t} + T_{K}^{t} = U^{t} = \sum\limits_{k = 1}^{N} {P_{0}^{{k,{\text{tB}}}} } (1 + \rho^{t} )\;[r^{t*} + \delta^{k} (1 + i^{k,t*} ){-}i^{k;t*} ]K^{k,t}$$(7)From which the ex-post endogenous real rate of return can be derived,

$$r^{t*} = {{\left\{ {(G^{t} + T_{K}^{t} )\;(1 + \rho^{t} ) - \sum\limits_{k = 1}^{N} {P_{0}^{{k,{\text{tB}}}} [\delta_{0}^{k} (1 + i^{k,t*} ){-}i^{k;t*} ]K^{k,t} } } \right\}} \mathord{\left/ {\vphantom {{\left\{ {(G^{t} + T_{K}^{t} )\;(1 + \rho^{t} ) - \sum\limits_{k = 1}^{N} {P_{0}^{{k,{\text{tB}}}} [\delta_{0}^{k} (1 + i^{k,t*} ){-}i^{k;t*} ]K^{k,t} } } \right\}} {\left\{ {\sum\limits_{k = 1}^{N} {P_{0}^{{k,{\text{tB}}}} K^{k,t} } } \right\}}}} \right. \kern-0pt} {\left\{ {\sum\limits_{k = 1}^{N} {P_{0}^{{k,{\text{tB}}}} K^{k,t} } } \right\}}}$$(8)Then, the ex-post user cost per unit of capital services for a particular type of asset is obtained as

$$F_{0}^{t} = P_{0}^{{k,{\text{tB}}}} (1 + \rho^{t} )\;[r^{t*} + \delta_{0}^{k} (1 + i^{k,t*} ){-}i^{k,t*} ]$$(9)where Gt Non-labour income consists of gross operating surplus and the part of mixed income that can be attributed to capital; T tK taxes on production; P k,tB0 is the purchase price of a new asset at the beginning (B) of year t; ρt is the rate of change of the consumer price index at the beginning of period t; rt* is the real rate of return that applies at the beginning of period t; δk is the rate of depreciation for a new asset k; ik,t* is the ex-post, real rate of asset price inflation for asset k during period t; Kk,t is the productive capital stock of asset k during period t.

Upwards biased if coverage is incomplete, since capital income will be compared to an under-valued capital stock and downwards biased if no clear distinction is made between market and government sectors since, probably, only market capital income will be compared to the value of the total capital stock.

Nonetheless, capital services have also been derived using an ex-post endogenous rate of return in order to provide a contrast to the ex-ante exogenous estimates. See Online Appendix C.

Actually, in Ivie’s estimates 4% real rate of return is chosen for the market sector and 3.5% rate for the non-market sector. The average real rate of return of bank deposits in Spain since 1850 is 4.5% (computed from underlying data in Prados de la Escosura and Rosés (2010), updated to 2019.

Similar trends, although less marked, and machinery and equipment never matches other construction, are observed when the ex-post endogenous rate of return is used (Figure A1).

Similar results are obtained using the private consumption deflator.

The gap is narrower gap when VICS is obtained with an ex-post endogenous, rather than an ex-ante exogenous rate of return. This finding is consistent with the presumed underestimate of capital services derived with an ex-post endogenous rate of return when information on capital assets is incomplete as it is our case (Figure A3).

Although the evolution of “quality” of capital using alternatively ex-ante exogenous and ex-post endogenous rates of return share the same tendencies, the level of capital “quality” is lower for the latter as could be anticipated due to the possible underestimate of capital services when they are computed with incomplete information (Figure A6a).

See Figure A7 for a comparison that included the new estimates derived with both ex-ante exogenous and ex-post endogenous rate of return.

Figure A9 adds up the new estimates of capital quality derived with ex-post endogenous rate of return that exhibits milder gains than when obtained with the ex-ante exogenous rate of return.

It is worth stressing that the described patterns for the capital-output ratio and the consumption of fixed capital are confirmed for alternative estimates derived using different average service lives and depreciation rates. Longer lives, by reducing depreciation, increase the level of net capital stock (Figure A11), and the use of the double declining balance implies higher depreciation rates, which increases capital consumption and, hence, reduces the level of net capital stock (Figure A12), while increases the ratio of the consumption of fixed capital ratio to GDP and net capital stock, respectively (Figure A13).

References

Artola-Blanco M, Bauluz LE, Martínez-Toledano C (2018) Wealth in Spain, 1900-2014: a country of two lands, World Inequality Lab Working Papers 2018/5. https://hal-pse.archives-ouvertes.fr/hal-02878216. Accessed 6 Sept 2020

Christensen LR, Cummings D, Jorgenson DW (1980) Economic growth, 1947-1973: an international comparison. In: Kendrick JW, Vaccara BN (eds) New developments in productivity measurement and analysis. University of Chicago Press/NBER, Chicago, pp 595–698

Conference Board (2020) Total economy database. Growth accounting and total factor productivity, 1990-2019. https://www.conference-board.org/data/economydatabase/total-economy-database-productivity. Accessed 19 Sept 2020

Elías VJ (1978) Sources of economic growth in Latin American countries. Rev Econ Stat 60(3):362–370

Feenstra RC, Inklaar R, Timmer MP (2015) The next generation of the Penn World Table. Am Econ Rev 105(10):3150–3182

Feinstein CH (1988) Sources and methods of estimation for domestic reproducible fixed assets, stocks and works in progress, overseas assets, and land. In: Feinstein CH, Pollard S (eds) Studies in capital formation in the United Kingdom 1750-1920. Clarendon Press, Oxford, pp 257–471

Fraumeni BM (1997) The measurement of depreciation in the U.S. national income and product accounts. Surv Curr Bus 77:7–23

Gallardo-Albarrán D, Inklaar R (2020) The role of capital and productivity in accounting for income differences since 1913. J Econ Surv. https://doi.org/10.1111/joes.12374

Hall R, Jorgenson DW (1967) Tax policy and investment behavior. Am Econ Rev 57(3):391–414

Harberger A (1978) Perspectives on capital and technology in less developed countries. In: Artis MJ, Nobay AR (eds) Contemporary economic analysis. Croom Helm, London, pp 15–40

Hulten Ch (1990) The measurement of capital. In: Berndt E, Tripplett J (eds) Fifty years of economic measurement. The Jubilee of the conference on research in income and wealth. University of Chicago Press, NBER, Chicago, pp 119–152

Hulten Ch, Wykoff F (1981) The estimation of economic depreciation using vintage asset prices. J Econ 15:367–396

Jorgenson DW (1963) Capital theory and investment behavior. Am Econ Rev 53(2):247–259

Jorgenson DW (1989) Capital as a factor of production. In: Jorgenson DJ, Landau R (eds) Technology and capital formation. MIT Press, Cambridge, pp 1–35

Jorgenson DW (1990) Productivity and economic growth. In: Berndt E, Tripplett J (eds) Fifty years of economic measurement. The jubilee of the conference on research in income and wealth. University of Chicago Press, NBER, Chicago, pp 19–118

Jorgenson DW, Griliches Z (1967) The explanation of productivity change. Rev Econ Stud 39(3):249–282

Jorgenson DW, Gollop F, Fraumeni B (1987) Productivity and US economic growth. Harvard University Press, Cambridge

Kaldor N (1957) A model of economic growth. Econ J 67(268):591–624

Maddison A (1995) Standardised estimates of fixed capital stock: a six country comparison. In: Maddison A (ed) Explaining the economic performance of nations. Essays in time and space. Edward Elgar, Aldershot, pp 137–166

Mas M, Pérez F, Uriel E (2000) Estimation of the stock of capital in Spain. Rev Income Wealth 46(1):103–116

Myro R (1983) La evolución de la productividad global de la economía española en el período 1965-1981. Inf Comer Esp 594:115–127

OECD (1993) Methods used by OECD countries to measure stocks of fixed capital. National accounts: sources and methods no. 2. OECD, Paris

OECD (2001) Measuring capital: measurement of capital stock, consumption of

OECD (2009) Measuring capital: OECD manual. OECD, Paris

Oulton N, Wallis G (2016) Capital stocks and capital services: integrated and consistent estimates for the United Kingdom, 1950–2013. Econ Model 54:117–125

Pérez F, Mas M, Serrano L, Uriel E (2019) El stock de capital en España y sus comunidades autónomas, Fundación BBVA, Documentos de Trabajo 1

Piketty T (2014) Capital in the twenty-first century. Harvard University Press, Cambridge

Piketty T, Zucman G (2014) Capital is back: wealth-income ratios in rich countries 1700–2010. Q J Econ 129(3):1255–1310

Prados de la Escosura L (2016) Mismeasuring long run growth. The bias from spliced national accounts: the case of Spain. Cliometrica 10(3):251–275

Prados de la Escosura L (2017) Spanish economic growth, 1850-2015. Palgrave Macmillan, London. https://www.palgrave.com/la/book/9783319580418. Updated data accessible at https://frdelpino.es/investigacion/en/category/01_social-sciences/01_spanish-economy/04_historical-perspective-1850-2018-spanish-economy/

Prados de la Escosura L, Rosés JR (2010) Capital accumulation in the long-run: the case of Spain, 1850-2000. Res Econ Hist 27:141–200

Universidad Comercial de Deusto (1968–1972), Riqueza nacional de España, 5 vol. Universidad Comercial de Deusto, Bilbao

Young A (1995) The Tyranny of numbers: confronting the statistical realities of the East Asian growth experience. Q J Econ 90(2):641–680

Acknowledgements

Thanks to Eva Benages, Juan Carlos Robledo, Ezequiel Uriel, and, especially, Matilde Mas and Ilya Voskoboynikov for their most valuable comments and to Juan Carlos Robledo and Eva Benages who kindly provided Ivie’s detailed capital stock and capital services series. A research grant from Fundación Rafael del Pino is gratefully acknowledged.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Electronic supplementary material

Below is the link to the electronic supplementary material.

Rights and permissions

About this article

Cite this article

Prados de la Escosura, L. Capital in Spain, 1850–2019. Cliometrica 16, 1–28 (2022). https://doi.org/10.1007/s11698-020-00221-2

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11698-020-00221-2