Abstract

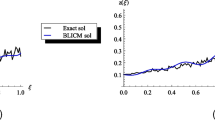

We study the local linear estimator for the drift coefficient of stochastic differential equations driven by α-stable Lévy motions observed at discrete instants. Under regular conditions, we derive the weak consistency and central limit theorem of the estimator. Compared with Nadaraya-Watson estimator, the local linear estimator has a bias reduction whether the kernel function is symmetric or not under different schemes. A simulation study demonstrates that the local linear estimator performs better than Nadaraya-Watson estimator, especially on the boundary.

Similar content being viewed by others

References

Aït-Sahalia Y, Jacod J. Testing for jumps in a discretely observed process. Ann Statist, 2009, 37: 184–222

Aït-Sahalia Y, Jacod J. Estimating the degree of activity of jumps in high frequency data. Ann Statist, 2009, 37: 2202–2224

Allen D M. The relationship between variable and data augmentation and a method of prediction. Technometrics, 1974, 16: 125–127

Andersen T, Benzoni L, Lund J. An empirical investigation of continuous time equity return models. J Finance, 2002, 57: 1239–1284

Bandi F, Nguyen T. On the functional estimation of jump diffusion models. J Econometrics, 2003, 116: 293–328

Bandi F, Phillips P. Fully nonparametric estimation of scalar diffusion models. Econometrica, 2003, 71: 241–283

Bandi F, Phillips P. A simple approach to the parametric estimation of potentially nonstationary diffusions. J Econometrics, 2007, 137: 354–395

Barndorff-Nielsen O E, Mikosch T, Resnick S. Lévy Processes, Theory and Applications. Boston: Birkhäuser, 2001

Baskshi G, Cao Z, Chen Z. Empirical performance of alternative option pricing models. J Finance, 1997, 52: 2003–2049

Bosq D. Nonparametric Statistics for Stochastic Processes. Lecture Notes in Statistics, vol. 110. New York: Springer-Verlag, 1996

Bradley R. Basic properties of strong mixing conditions: A survey and some open questions. Probab Surv, 2005, 2: 107–144

Cleveland W. Robust locally weighted regression and smoothing scatter plots. J Amer Statis Assoc, 1979, 74: 829–836

Duffie D, Pan J, Singleton K. Transform analysis and asset pricing for affine jump-diffusions. Econometrica, 2000, 68: 1343–1376

Fan J. Design-adaptive nonparametric regression. J Amer Statis Assoc, 1992, 87: 998–1004

Fan J, Gijbels I. Variable bandwidth and local linear regression smoothers. Ann Statist, 1992, 20: 2008–2036

Fan J, Gijbels I. Data-driven bandwidth selection in local polynomial fitting: Variable bandwidth and spatial adaptation. J R Stat Soc Ser B, 1995, 57: 371–394

Fan J, Gijbels I. Local Polynomial Modeling and its Applications. New York: Chapman and Hall, 1996

Fan J, Zhang C. A re-examination of diffusion estimators with applications to financial model validation. J Amer Statist Assoc, 2003, 98: 118–134

Gasser T, Müller H G. Kernel estimation of regression functions. In: Smoothing Techniques for Curve Estimation. Lecture Notes in Math, vol. 757. New York: Springer, 1979, 23–68

Hall P, Presnell B. Intentionally biased bootstrap methods. J R Stat Soc Ser B, 1999, 61: 143–158

Hanif M. Local linear estimation of recurrent jump-diffusion models. Comm Statist Theory Methods, 2012, 41: 4142–4163

Hu Y, Long H. Least squares estimator for Ornstein-Uhlenbeck processes driven by α-stable motions. Stochastic Process Appl, 1999, 119: 2465–2480

Jacod J, Kurtz T G, Méléard S, et al. The approximate Euler method for Lévy driven stochastic differential equations. Ann Inst H Poincaré Probab Statist, 2005, 41: 523–558

Jacod J, Li Y, Mykland P A, et al. Microstructure noise in the continuous case: The pre-averaging approach. Stochastic Process Appl, 2009, 119: 2249–2276

Jacod J, Protter P. Discretization of Processes. Heidelberg-New York: Springer-Verlag, 2012

Jacod J, Shiryaev A. Limit Theory for Stochastic Processes. Berlin: Springer, 2003

Janicki A, Weron A. Simulation and Chaotic Behavior of α-Stable Stochastic Processes. New York: Marcel Dekker, 1994

Johannes M S. The economic and statistical role of jumps to interest rates. J Finance, 2004, 59: 227–260

Kyprianou A, Schouten W, Wilmott P. Exotic Option Pricing and Advanced Lévy Models. Hoboken: Wiley, 2005

Long H, Qian L. Nadaraya-Watson estimator for stochastic processes driven by stable Lévy motions. Working paper, http://math.fau.edu/long/QianLongSPA08.pdf

Masuda H. On multi-dimensional Ornstein-Uhlenbeck processes driven by a general Lévy process. Bernoulli, 2004, 10: 1–24

Masuda H. Ergodicity and exponential β-mixing bounds for multidimensional diffusions with jumps. Stochastic Process Appl, 2007, 117: 35–56

Masuda H. Approximate self-weighted LAD estimation of discretely observed ergodic Ornstein-Uhlenbeck processes. Electron J Probab, 2010, 4: 525–565

Moloche G. Local nonparametric estimation of scalar diffusions. Working paper, MIT, 2010

Nicolau J. Nonparametric estimation of second-order stochastic differential equations. Econometric Theory, 2007, 23: 880–898

Prakasa Rao B L S. Estimation of the drift for diffusion process. Statistics, 1985, 16: 263–275

Ruppert D, Wand M P. Multivariate locally weighted least squares regression. Ann Statist, 1994, 22: 1346–1370

Sato K I. Lévy Processes and Infinitely Divisible Distributions. Cambridge: Cambridge University Press, 1999

Schertzer D, Larchevêque M, Duan J, et al. Fractional Fokker-Planck equation for nonlinear stochastic differential equations driven by non-Gaussian Lévy stable noises. J Math Phys, 2001, 42: 200–212

Schoutens W. Lévy Processes in Finance: Pricing Financial Derivatives. Hoboken: Wiley, 2003

Shimizu Y, Yoshida N. Estimation of parameters for diffusion processes with jumps from discrete observation. Stat Inference Stoch Process, 2006, 9: 227–277

Silverman B W. Density Estimation for Statistics and Data Analysis. London: Chapman and Hall, 1986

Stone C. Optimal global rates of convergence for nonparametric regression. Ann Statist, 1982, 10: 1040–1053

Stone M. Cross-validity choice and assesment of statistical predictions (with discussion). J R Stat Soc Ser B, 1974, 36: 111–147

Sun S, Zhang X. Empirical likelihood estimation of discretely sampled processes of OU type. Sci China Ser A, 2009, 52: 908–931

Wand M, Jone C. Kernel Smoothing. London: Chapman and Hall, 1995

Wang H, Lin Z. Local linear estimation of second-order diffusion models. Comm Statist Theory Methods, 2011, 40: 394–407

West B J, Seshadri V. Linear systems with Lévy fluctuations. Physica A, 1982, 113: 203–216

Xu K. Empirical likelihood based inference for nonparametric recurrent diffusions. J Econometrics, 2009, 153: 65–82

Xu K. Re-weighted functional estimation of diffusion models. Econometric Theory, 2010, 26: 541–563

Zhang L, Mykland P A, Aït-Sahalia Y. A tale of two time scales: Determining integrated volatility with noisy high-frequency data. J Amer Statist Assoc, 2005, 100: 1394–1411

Zhao Z, Wu W B. Nonparametric inference of discretely sampled stable Lévy processes. J Econometrics, 2009, 153: 83–92

Zhou Q, Yu J. Asymptotic distributions of the least squares estimator for diffusion process. Working paper, Singapore Management University, 2010

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Lin, Z., Song, Y. & Yi, J. Local linear estimator for stochastic differential equations driven by α-stable Lévy motions. Sci. China Math. 57, 609–626 (2014). https://doi.org/10.1007/s11425-013-4628-7

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11425-013-4628-7

Keywords

- local linear estimator

- stable Lévy motion

- drift coefficient

- bias reduction

- consistency

- central limit theorem