Abstract

Using the Heterogeneous Agent Model framework, we incorporate an extension based on Prospect Theory into a popular agent-based asset pricing model. This extension covers the phenomenon of loss aversion manifested in risk aversion and asymmetric treatment of gains and losses. Using Monte Carlo methods, we investigate behavior and statistical properties of the extended model and assess how our extension is manifested in different strategies. We show that, on the one hand, the Prospect Theory extension keeps the essential underlying mechanics of the model intact, but on the other hand it considerably changes the model dynamics. Stability of the model is increased and fundamentalists may be able to survive in the market more easily. When only the fundamentalists are loss-averse, other strategies profit more.

Similar content being viewed by others

Notes

According to Ehrentreich (2007, p. 56), at the time when the foundations of the EMH were laid, logarithmic asset returns were assumed to be distributed normally and the prices therefore followed the log-normal distribution.

The ‘irrationality’ is meant within the expected utility theory.

PT is descriptive in the sense that it tries to capture the real-world decision-making whereas the expected utility theory is de facto normative—it models how people are supposed to decide.

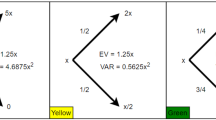

Regular prospect is a prospect such that either \(p + q < 1\), \(x \geqslant 0 \geqslant y\), or \(x \leqslant 0 \leqslant y\). Evaluation of prospects which are not regular follows a different rule—details are provided in Kahneman and Tversky (1979, p. 276).

The equity premium puzzle is a phenomenon that the average return on equity is far greater than return on a risk-free asset. Such a characteristic has been observed in many markets. The term was first coined by Mehra and Prescott (1985).

We run another ‘benchmark’ simulation of the model without the proposed extensions, that is, for the K–W test, we use a different benchmark than that examined in Sect. 5.3.1.

References

Anufriev M, Hommes C (2012) Evolutionary selection of individual expectations and aggregate outcomes in asset pricing experiments. Am Econ J Microecon 4(4):35–64

Barberis N, Huang M, Santos T (2001) Prospect theory and asset prices. Q J Econ 116(1):1–53

Barunik J, Vacha L, Vosvrda M (2009) Smart predictors in the heterogeneous agent model. J Econ Interact Coord 4(2):163–172

Belsky G, Gilovich T (2010) Why smart people make big money mistakes and how to correct them: lessons from the life-changing science of behavioral economics. Simon and Schuster, New York City

Benartzi S, Thaler RH (1993) Myopic loss aversion and the equity premium puzzle. Technical report, National Bureau of Economic Research

Branch WA (2004) The theory of rationally heterogeneous expectations: evidence from survey data on inflation expectations. Econ J 114(497):592–621

Brock WA, Hommes CH (1997) A rational route to randomness. Econom J Econom Soc 65(5):1059–1095

Brock WA, Hommes CH (1998) Heterogeneous beliefs and routes to chaos in a simple asset pricing model. J Econ Dyn Control 22:1235–1274

Cao S-N, Deng J, Li H (2010) Prospect theory and risk appetite: an application to traders’ strategies in the financial market. J Econ Interact Coord 5(2):249–259

Castro PAL, Parsons S (2014) Modeling agent’s preferences based on prospect theory. In: Papers from the AAAI-14 workshop, multidisciplinary workshop on advances in preference handling

Chang C-L, McAleer M, Oxley L (2011) Great expectatrics: great papers, great journals, great econometrics. Econom Rev 30(6):583–619

Chen S-H, Chang C-L, Du Y-R (2012) Agent-based economic models and econometrics. Knowl Eng Rev 27:187–219

Chiarella C, Iori G, Perelló J (2009) The impact of heterogeneous trading rules on the limit order book and order flows. J Econ Dyn Control 33(3):525–537

Cont R (2001) Empirical properties of asset returns: stylized facts and statistical issues. Quant Finance 1(2):223–236

Cont R (2007) Volatility clustering in financial markets: empirical facts and agent-based models. In: Teyssiere G, Kirman A (eds) Long memory in economics. Springer, Berlin, pp 289–309

Ehrentreich N (2007) Agent-based modeling: The Santa Fe Institute artificial stock market model revisited, vol 602. Springer, Berlin

Evans G W, Honkapohja S (2001) Learning and expectations in macroeconomics. Princeton University Press, Princeton

Fama EF (1970) Efficient capital markets: a review of theory and empirical work. J Finance 25(2):383–417

Frankel JA, Froot KA (1990) Chartists, fundamentalists, and trading in the foreign exchange market. Am Econ Rev 80(2):181–185

Giorgi EGD, Legg S (2012) Dynamic portfolio choice and asset pricing with narrow framing and probability weighting. J Econ Dyn Control 36(7):951–972

Giorgi ED, Hens T, Rieger MO (2010) Financial market equilibria with cumulative prospect theory. J Math Econ 46(5):633–651

Grüne L, Semmler W (2008) Asset pricing with loss aversion. J Econ Dyn Control 32(10):3253–3274

Haas M, Pigorsch C (2009) Financial economics, fat-tailed distributions. In: Meyers RA (ed) Encyclopedia of complexity and systems science. Springer, Berlin, pp 3404–3435

Hansen LP, Heckman JJ (1996) The empirical foundations of calibration. J Econ Perspect 10(1):87–104

Harrison GW, Rutström EE (2009) Expected utility theory and prospect theory: one wedding and a decent funeral. Exp Econ 12(2):133–158

Hommes CH (2006) Handbook of computational economics, agent-based computational economics. In: Tesfatsion L, Judd KL (eds) Heterogeneous agent models in economics and finance. Elsevier, Amsterdam, pp 1109–1186

Hommes C (2011) The heterogeneous expectations hypothesis: some evidence from the lab. J Econ Dyn Control 35(1):1–24

Hommes C (2013) Behavioral rationality and heterogeneous expectations in complex economic systems. Cambridge University Press, Cambridge

Kahneman D, Tversky A (1979) Prospect theory: an analysis of decision under risk. Econometrica 47(2):263–291

Kukacka J, Barunik J (2013) Behavioural breaks in the heterogeneous agent model: the impact of herding, overconfidence, and market sentiment. Physica A 392(23):5920–5938

Kukacka J, Barunik J (2017) Estimation of financial agent-based models with simulated maximum likelihood. J Econ Dyn Control 85:21–45

Li Y, Yang L (2013) Prospect theory, the disposition effect, and asset prices. J Financ Econ 107(3):715–739

Mankiw NG, Reis R, Wolfers J (2004) Disagreement about inflation expectations. In: NBER macroeconomics annual 2003, vol 18. The MIT Press, Cambridge, pp 209–270

Mehra R, Prescott EC (1985) The equity premium: a puzzle. J Monet Econ 15(2):145–161

Shefrin H, Statman M (1985) The disposition to sell winners too early and ride losers too long: theory and evidence. J Finance 40(3):777–790

Shimokawa T, Suzuki K, Misawa T (2007) An agent-based approach to financial stylized facts. Physica A 379(1):207–225

Tedeschi G, Iori G, Gallegati M (2012) Herding effects in order driven markets: the rise and fall of gurus. J Econ Behav Organ 81(1):82–96

Tu Q (2005) Empirical analysis of time preferences and risk aversion. Technical report, School of Economics and Management

Tversky A, Kahneman D (1992) Advances in prospect theory: cumulative representation of uncertainty. J Risk Uncertainty 5(4):297–323

Vacha L, Barunik J, Vosvrda M (2012) How do skilled traders change the structure of the market. Int Rev Financ Anal 23:66–71

van Kersbergen K, Vis B (2014) Comparative welfare state politics: development, opportunities, and reform. Cambridge University Press, Cambridge

Vissing-Jorgensen A (2004) Perspectives on behavioral finance: does “irrationality” disappear with wealth? Evidence from expectations and actions. In: NBER macroeconomics annual 2003, vol 18, NBER Chapters. National Bureau of Economic Research, Inc, pp 139–208

West KD (1988) Bubbles, fads, and stock price volatility tests: a partial evaluation. Working paper 2574, National Bureau of Economic Research

Yao J, Li D (2013) Prospect theory and trading patterns. J Bank Finance 37(8):2793–2805

Zhang W, Semmler W (2009) Prospect theory for stock markets: empirical evidence with time-series data. J Econ Behav Organ 72(3):835–849

Author information

Authors and Affiliations

Corresponding authors

Additional information

The views expressed in this article are those of the authors and do not necessarily reflect the position of Moody’s Analytics, Moody’s Investors Service, or Moody’s Corporation. J. Kukacka gratefully acknowledges financial support from the Czech Science Foundation under the P402/12/G097 DYME—‘Dynamic Models in Economics’ project.

Rights and permissions

About this article

Cite this article

Polach, J., Kukacka, J. Prospect Theory in the Heterogeneous Agent Model. J Econ Interact Coord 14, 147–174 (2019). https://doi.org/10.1007/s11403-018-0219-6

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11403-018-0219-6