Abstract

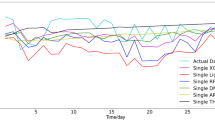

Forecasting China’s carbon price accurately can encourage investors and manufacturing industries to take quantitative investments and emission reduction decisions effectively. The inspiration for this paper is developing an error-corrected carbon price forecasting model integrated fuzzy dispersion entropy and deep learning paradigm, named ICEEMDAN-FDE-VMD-PSO-LSTM-EC. Initially, the improved complete ensemble empirical mode decomposition with adaptive noise (ICEEMDAN) is used to primary decompose the original carbon price. Subsequently, the fuzzy dispersion entropy (FDE) is conducted to identify the high-complexity signals. Thirdly, the variational mode decomposition (VMD) and deep learning paradigm of particle swarm optimized long short-term memory (PSO-LSTM) models are employed to secondary decompose the high-complexity signals and perform out-of-sample forecasting. Finally, the error-corrected (EC) method is conducted to re-modify and strengthen the above-predicted accuracy. The results conclude that the forecasting performance of ICEEMDAN-type secondary decomposition models is significantly better than the primary decomposition models, the deep learning PSO-LSTM-type models have superiority in forecasting China carbon price, and the EC method for improving the forecasting accuracy has been proved. Noteworthy, the proposed model presents the best forecasting accuracy, with the forecasting errors RMSE, MAE, MAPE, and Pearson’s correlation are 0.0877, 0.0407, 0.0009, and 0.9998, respectively. Especially, the long-term forecasting ability for 750 consecutive trading prices is outstanding. Those conclusions contribute to judging the carbon price characteristics and formulating market regulations.

Similar content being viewed by others

Data availability

The data can be available from the corresponding author upon reasonable request.

References

Bengio Y, Courville A, Vincent P (2013) Representation learning: a review and new perspectives. IEEE T Pattern Anal 35(8):1798–1828. https://doi.org/10.1109/TPAMI.2013.50

Byun SJ, Cho H (2013) Forecasting carbon futures volatility using GARCH models with energy volatilities. Energy Econ 40:207–221. https://doi.org/10.1016/j.eneco.2013.06.017

Chevallier J (2009) Carbon futures and macroeconomic risk factors: a view from the EU ETS. Energy Econ 31:614–625. https://doi.org/10.1016/j.eneco.2009.02.008

Colominas MA, Schlotthauer G, Torres ME (2014) Improved complete ensemble EMD: a suitable tool for biomedical signal processing. Biomed Signal Process 14:19–29. https://doi.org/10.1016/j.bspc.2014.06.009

Dragomiretskiy K, Zosso D (2013) Variational mode decomposition. IEEE T Signal Process 62(3):531–544. https://doi.org/10.1109/TSP.2013.2288675

Guo W, Liu Q, Luo Z, Tse Y (2022) Forecasts for international financial series with VMD algorithms. J Asian Econ 80:101458. https://doi.org/10.1016/j.asieco.2022.101458

Hao Y, Tian C, Wu C (2020) Modelling of carbon price in two real carbon trading markets. J Clean Prod 244:118556. https://doi.org/10.1016/j.jclepro.2019.118556

Hochreiter S, Schmidhuber J (1997) Long short-term memory. Neural Comput 9(8):1735–1780. https://doi.org/10.1162/neco.1997.9.8.1735

Huang Y, Dai X, Wang Q, Zhou D (2021) A hybrid model for carbon price forecasting using GARCH and long short-term memory network. Appl Energ 285:116485. https://doi.org/10.1016/j.apenergy.2021.116485

Hubert M, Vandervieren E (2008) An adjusted boxplot for skewed distributions. Comput Stat Data An 52(12):5186–5520. https://doi.org/10.1016/j.csda.2007.11.008

Jianwei E, Ye J, He L, Jin H (2021) A denoising carbon price forecasting method based on the integration of kernel independent component analysis and least squares support vector regression. Neurocomputing 434:67–79. https://doi.org/10.1016/j.neucom.2020.12.086

Junior PO, Tiwari AK, Padhan H, Alagidede I (2020) Analysis of EEMD-based quantile-in-quantile approach on spot-futures prices of energy and precious metals in India. Resour Policy 68:101731. https://doi.org/10.1016/j.resourpol.2020.101731

Kong F, Song J, Yang Z (2022) A novel short-term carbon emission prediction model based on secondary decomposition method and long short-term memory network. Environ Sci Pollut Res 29(43):64983–64998. https://doi.org/10.1007/s11356-022-20393-w

Li G, Yin S, Yang H (2022) A novel crude oil prices forecasting model based on secondary decomposition. Energy 257:124684. https://doi.org/10.1016/j.energy.2022.124684

Li H, Jin F, Sun S, Li Y (2021) A new secondary decomposition ensemble learning approach for carbon price forecasting. Knowl-Based Syst 214:106686. https://doi.org/10.1016/j.knosys.2020.106686

Li J, Liu D (2023) Carbon price forecasting based on secondary decomposition and feature screening. Energy 278:127783. https://doi.org/10.1016/j.energy.2023.127783

Liu YL, Zhang JJ, Fang Y (2023) The driving factors of China’s carbon prices: evidence from using ICEEMDAN-HC method and quantile regression. Financ Res Lett 54:103756. https://doi.org/10.1016/j.frl.2023.103756

Mao S, Zeng XJ (2023) SimVGNets: similarity-based visibility graph networks for carbon price forecasting. Expert Syst Appl:120647. https://doi.org/10.1016/j.eswa.2023.120647

Nazifi F, Milunovich G (2010) Measuring the impact of carbon allowance trading on energy prices. Energy Environ 21(5):367–383. https://doi.org/10.1260/0958-305X.21.5.367

Nguyen THT, Phan QB (2022) Hourly day ahead wind speed forecasting based on a hybrid model of EEMD, CNN-Bi-LSTM embedded with GA optimization. Energy Rep 8:53–60. https://doi.org/10.1016/j.egyr.2022.05.110

Pan D, Zhang C, Zhu D, Hu S (2023) Carbon price forecasting based on news text mining considering investor attention. Environ Sci Pollut Res 30(11):28704–28717. https://doi.org/10.1007/s11356-022-24186-z

Qin Q, He H, Li L, He LY (2020) A novel decomposition-ensemble based carbon price forecasting model integrated with local polynomial prediction. Comput Econ 55:1249–1273. https://doi.org/10.1007/s10614-018-9862-1

Rostaghi M, Khatibi MM, Ashory M, Azami H (2021) Fuzzy dispersion entropy: a nonlinear measure for signal analysis. IEEE T Fuzzy Syst 30(9):3785–3796. https://doi.org/10.1109/TFUZZ.2021.3128957

Schneider L, Hoz L, Theuer S (2019) Environmental integrity of international carbon market mechanisms under the Paris Agreement. Clim Policy 19(3):386–400. https://doi.org/10.1080/14693062.2018.1521332

Shen F, Chao J, Zhao J (2015) Forecasting exchange rate using deep belief networks and conjugate gradient method. Neurocomputing 167:243–253. https://doi.org/10.1016/j.neucom.2015.04.071

Sun J, Zhao P, Sun S (2022) A new secondary decomposition-reconstruction-ensemble approach for crude oil price forecasting. Resour Policy 77:102762. https://doi.org/10.1016/j.resourpol.2022.102762

Sun W, Huang C (2020) A carbon price prediction model based on secondary decomposition algorithm and optimized back propagation neural network. J Clean Prod 243:118671. https://doi.org/10.1016/j.jclepro.2019.118671

Sun W, Zhang C (2018) Analysis and forecasting of the carbon price using multi—resolution singular value decomposition and extreme learning machine optimized by adaptive whale optimization algorithm. Appl Energ 231:1354–1371. https://doi.org/10.1016/j.apenergy.2018.09.118

Tang BJ, Gong PQ, Shen C (2017) Factors of carbon price volatility in a comparative analysis of the EUA and sCER. Ann Oper Res 255:157–168. https://doi.org/10.1007/s10479-015-1864-y

Wang D, Tan D, Liu L (2018) Particle swarm optimization algorithm: an overview. Soft Comput 22:387–408. https://doi.org/10.1007/s00500-016-2474-6

Wang J, Cheng Q, Sun X (2022) Carbon price forecasting using multiscale nonlinear integration model coupled optimal feature reconstruction with biphasic deep learning. Environ Sci Pollut Res 29(57):85988–86004. https://doi.org/10.1007/s11356-021-16089-2

Wang J, Sun X, Cheng Q, Cui Q (2021) An innovative random forest-based nonlinear ensemble paradigm of improved feature extraction and deep learning for carbon price forecasting. Sci Total Environ 762:143099. https://doi.org/10.1016/j.scitotenv.2020.143099

Wu Q, Liu Z (2020) Forecasting the carbon price sequence in the Hubei emissions exchange using a hybrid model based on ensemble empirical mode decomposition. Energy Sci Eng 8(8):2708–2721. https://doi.org/10.1002/ese3.703

Wu Y, Zhang C, Yun P et al (2021) Time-frequency analysis of the interaction mechanism between European carbon and crude oil markets. Energy Environ 32(7):1331–1357. https://doi.org/10.1177/0958305X211002457

Wu Z, Huang NE (2009) Ensemble empirical mode decomposition: a noise-assisted data analysis method. Adv Data Sci Adapt 1(1):1–41. https://doi.org/10.1142/S1793536909000047

Yang H, Yang X, Li G (2023a) Forecasting carbon price in China using a novel hybrid model based on secondary decomposition, multi-complexity and error correction. J Clean Prod 401:136701. https://doi.org/10.1016/j.jclepro.2023.136701

Yang R, Liu H, Li Y (2023b) An ensemble self-learning framework combined with dynamic model selection and divide-conquer strategies for carbon emissions trading price forecasting. Chaos Soliton Fract 173:113692. https://doi.org/10.1016/j.chaos.2023.113692

Yang S, Chen D, Li S, Wang W (2020) Carbon price forecasting based on modified ensemble empirical mode decomposition and long short-term memory optimized by improved whale optimization algorithm. Sci Total Environ 716:137117. https://doi.org/10.1016/j.scitotenv.2020.137117

Yue W, Zhong W, Xiaoyi W, Xinyu K (2023) Multi-step-ahead and interval carbon price forecasting using transformer-based hybrid model. Environ Sci Pollut Res 30:95692–95719. https://doi.org/10.1007/s11356-023-29196-z

Yun P, Huang X, Wu Y, Yang X (2023) Forecasting carbon dioxide emission price using a novel mode decomposition machine learning hybrid model of CEEMDAN-LSTM. Energy Sci Eng 11(1):79–96. https://doi.org/10.1002/ese3.1304

Zhang C, Yun P, Wagan ZA (2019) Study on the wandering weekday effect of the international carbon market based on trend moderation effect. Financ Res Lett 28:319–327. https://doi.org/10.1016/j.frl.2018.05.014

Zhang J, Li D, Hao Y, Tan Z (2018) A hybrid model using signal processing technology, econometric models and neural network for carbon spot price forecasting. J Clean Prod 204:958–964. https://doi.org/10.1016/j.jclepro.2018.09.071

Zhang K, Yang X, Wang T, Thé J, Tan Z, Yu H (2023) Multi-step carbon price forecasting using a hybrid model based on multivariate decomposition strategy and deep learning algorithms. J Clean Prod 405:136959. https://doi.org/10.1016/j.jclepro.2023.136959

Zhang W, Li J, Li G, Guo S (2020) Emission reduction effect and carbon market efficiency of carbon emissions trading policy in China. Energy 196:117117. https://doi.org/10.1016/j.energy.2020.117117

Zhang W, Wu Z (2022) Optimal hybrid framework for carbon price forecasting using time series analysis and least squares support vector machine. J Forecasting 41(3):615–632. https://doi.org/10.1002/for.2831

Zhou F, Huang Z, Zhang C (2022) Carbon price forecasting based on CEEMDAN and LSTM. Appl Energ 311:118601. https://doi.org/10.1016/j.apenergy.2022.118601

Zhou J, Wang Q (2021) Forecasting carbon price with secondary decomposition algorithm and optimized extreme learning machine. Sustainability 13:8413. https://doi.org/10.3390/su13158413

Zhou K, Li Y (2019) Carbon finance and carbon market in China: progress and challenges. J Clean Prod 214:536–549. https://doi.org/10.1016/j.jclepro.2018.12.298

Zhu B, Wang P, Chevallier J, Wei YM (2015) Carbon price analysis using empirical mode decomposition. Comput Econ 45:195–206. https://doi.org/10.1007/s10614-013-9417-4

Zhu B, Ye S, Wang P, He K, Zhang T, Wei YM (2018) A novel multiscale nonlinear ensemble leaning paradigm for carbon price forecasting. Energy Econ 70:143–157. https://doi.org/10.1016/j.eneco.2017.12.030

Zhu J, Wu P, Chen H, Liu J, Zhou L (2019) Carbon price forecasting with variational mode decomposition and optimal combined model. Physica A 519:140–158. https://doi.org/10.1016/j.physa.2018.12.017

Zhu T, Wang W, Yu M (2023) A novel hybrid scheme for remaining useful life prognostic based on secondary decomposition, BiGRU and error correction. Energy 276:127565. https://doi.org/10.1016/j.energy.2023.127565

Acknowledgements

The authors acknowledge the valuable comments from the anonymous reviewers and the editor that have significantly improved the quality of this manuscript.

Funding

This work was supported by the Youth Fund Project for Humanities and Social Sciences of the Ministry of Education of China (Grant No. 21YJC790152), the National Natural Science Foundation of China (Grant Nos. 71971071 and 72101006), and the Youth Fund Project for Philosophy and Social Science Research of Anhui Province of China (Grant No. AHSKQ2022D040).

Author information

Authors and Affiliations

Contributions

All authors contributed to the manuscript design. Conceptualization, methodology, and Python code were performed by Po Yun. The original draft preparation was written by Yingtong Zhou and Chenghui Liu. Review and editing was conducted by Po Yun and Yaqi Wu. Formal analysis was performed by Di Pan. All authors read and approved the final manuscript.

Corresponding author

Ethics declarations

Ethics approval

This study follows all ethical practices during writing.

Consent to participate

Not applicable

Consent for publication

Not applicable

Competing interests

The authors declare no competing interests.

Additional information

Responsible Editor: Ilhan Ozturk

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

Appendix 1. Primary decomposition of the carbon price signals based on the EMD-type technologies

The primary decomposition of carbon price based on the CEEMDAN model

The primary decomposition of carbon price based on the EEMD model

The primary decomposition of carbon price based on the EMD model

Appendix 2. The mode statistic of carbon price signal after the primary decomposition

Appendix 3. The VMD secondary mode decomposition process of the high-complexity signals that recognized by the primary decomposition

The VMD secondary mode decomposition after the CEEMDAN primary decomposition (IMF0 means the high complexity mode signal that needs to be decomposed)

The VMD secondary mode decomposition after the EEMD primary decomposition (IMF0 means the high complexity mode signal that needs to be decomposed)

The VMD secondary mode decomposition after the EMD primary decomposition (IMF0 means the high complexity mode signal that needs to be decomposed)

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Yun, P., Zhou, Y., Liu, C. et al. Forecasting China carbon price using an error-corrected secondary decomposition hybrid model integrated fuzzy dispersion entropy and deep learning paradigm. Environ Sci Pollut Res 31, 16530–16553 (2024). https://doi.org/10.1007/s11356-024-32169-5

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11356-024-32169-5