Abstract

Carbon trading price (CTP) prediction accuracy is critical for both market participants and policymakers. As things stand, most previous studies have only focused on one or a few carbon trading markets, implying that the models’ universality is insufficient to be validated. By employing a case study of all carbon trading markets in China, this study proposes a hybrid point and interval CTP forecasting model. First, the Pearson correlation method is used to identify the key influencing factors of CTP. The original CTP data is then decomposed into multiple series using complete ensemble empirical mode decomposition with adaptive noise. Following that, the sample entropy method is used to reconstruct the series to reduce computational time and avoid overdecomposition. Following that, a long short-term memory method optimized by the Adam algorithm is established to achieve the point forecasting of CTP. Finally, the kernel density estimation method is used to predict CTP intervals. On the one hand, the results demonstrate the proposed model’s validity and superiority. The interval prediction model, on the other hand, reflects the uncertainty of market participants’ behavior, which is more practical in the operation of carbon trading markets.

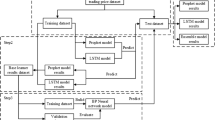

Graphical abstract

Similar content being viewed by others

Abbreviations

- CTP:

-

Carbon trading price

- EU ETS:

-

European Union emissions trading system

- PACF:

-

Partial autocorrelation function

- mRMR:

-

Max-relevance min-redundancy

- GRA:

-

Gray relation analysis

- KICA:

-

Kernel independent component analysis

- LASSO:

-

Least absolute shrinkage and selection operator

- EMD:

-

Empirical mode decomposition

- EEMD:

-

Ensemble empirical mode decomposition

- CEEMD:

-

Complete ensemble empirical mode decomposition

- CEEMDAN:

-

Complete ensemble empirical mode decomposition with adaptive noise

- ICEEMDAN:

-

Improved complete ensemble empirical mode decomposition with adaptive noise

- MOEMD:

-

Empirical mode decomposition algorithm for mean value optimization

- MEEMD:

-

Modified ensemble empirical mode decomposition

- ESMD:

-

Extreme-point symmetric model decomposition

- VMD:

-

Variational model decomposition

- MRSVD:

-

Multi-resolution singular value decomposition

- CCI:

-

Comprehensive contribution index

- ApEn:

-

Approximate entropy

- SE:

-

Sample entropy

- RF:

-

Random forest

- CIM:

-

Cointegration model

- GARCH:

-

Generalized autoregressive conditional heteroskedasticity

- CPN:

-

Carbon price network

- LSSVR:

-

Least squares support vector regression

- ELM:

-

Extreme learning machine

- KELM:

-

Kernel-based extreme learning machine

- WRELM:

-

Weighted regularized extreme learning machine

- KNEA:

-

Kernel-based nonlinear extension of the Arps decline model

- ANFIS:

-

Adaptive network–based fuzzy inference system

- CNN:

-

Convolution neural network

- DBN:

-

Deep belief network

- RNN:

-

Recurrent neural network

- GNN:

-

Gray neural network

- RBFNN:

-

Radial basis function neural network

- NARNN:

-

Nonlinear autoregressive neural network

- LSTM:

-

Long short-term memory

- PSO:

-

Particle swarm optimization

- CKA:

-

Kidney algorithm with scaling factor and cooperation factor

- ACA:

-

Ant colony algorithm

- GWO:

-

Gray wolf optimizer

- AWOA:

-

Adaptive whale optimization algorithm

- IWOA:

-

Improved whale optimization algorithm

- MOGOA:

-

Multiobjective grasshopper optimization algorithm

- MOCSCA:

-

Multiobjective chaotic sine cosine algorithm

- SGD:

-

Stochastic gradient descent

- AdaGrad:

-

Adaptive gradient algorithm

- RMSprop:

-

Root mean square prop

- KDE:

-

Kernel density estimation

- NDE:

-

Normal distribution estimation

- IMF:

-

Intrinsic mode function

- MB:

-

Memory blocks

- MAE:

-

Mean absolute error

- MAPE:

-

Mean absolute percentage error

- RMSE:

-

Root mean square error

- U1:

-

Theil U statistic 1

- PICP:

-

Prediction interval coverage probability

- PINAW:

-

Prediction interval normalized average width

- PIECE:

-

Prediction interval comprehensive evaluation criteria

- AQI:

-

Air quality index

- EUAP:

-

European Union carbon emission allowances price

- BOP:

-

Brent oil price

- NGP:

-

Nature gas price

- ER (EUR–CNY):

-

Exchange rate between EUR and CNY

- CEA:

-

Carbon emission allowances

References

Batten JA, Maddox GE, Young, m.r. (2021) Does weather, or energy prices, affect carbon prices? Energy Econ 96:105016

Chang Z, Zhang Y, Chen W (2019) Electricity price prediction based on hybrid model of Adam optimized LSTM neural network and wavelet transform. Energy 187:115804

Chen P, Vivian A, Ye C (2022a) Forecasting carbon futures price: a hybrid method incorporating fuzzy entropy and extreme learning machine. Ann Oper Res 313:559–601

Chen J, Ma S, Wu Y (2022b) International carbon financial market prediction using particle swarm optimization and support vector machine. J Ambient Intell Humanized Comput 13:5699–5713

Cheridito P, Jentzen A, Rossmannek F (2020) Non-convergence of stochastic gradient descent in the training of deep neural networks. J Complexity 64:101540

Ding W, Meng F (2020) Point and interval forecasting for wind speed based on linear component extraction. Appl Soft Comput 93:106350

Ding G, Deng Y, Lin S (2019) A study on the classification of China’s provincial carbon emissions trading policy instruments: taking Fujian province as an example. Energy Rep 5:1543–1550

Du P, Wang J, Yang W, Niu T (2020) Point and interval forecasting for metal prices based on variational mode decomposition and an optimized outlier-robust extreme learning machine. Resour Policy 69:101881

Duan J, Zuo H, Bai Y, Duan J, Chang M, Chen B (2021) Short-term wind speed forecasting using recurrent neural networks with error correction. Energy 217:119397

E J, Ye J, He L, Jin H (2021) A denoising carbon price forecasting method based on the integration of kernel independent component analysis and least squares support vector regression. Neurocomputing 434:67–69

Fekri MN, Patel H, Grolinger K, Sharma V (2021) Deep learning for load forecasting with smart meter data: online adaptive recurrent neural network. Appl Energy 282:116177

Gao B, Huang X, Shi J, Tai Y, Zhang J (2020) Hourly forecasting of solar irradiance based on CEEMDAN and multi-strategy CNN-LSTM neural networks. Renew Energy 162:1665–1683

Gong X, Shi R, Xu J, Lin B (2021) Analyzing spillover effects between carbon and fossil energy markets from a time-varying perspective. Appl Energy 285:116384

Hamilton J (2017) Why you should never use the Hodrick-Prescott filter. Rev. Econ. Stat. 100:831–843

Han H, Lin Z, Qiao J (2017) Modeling of nonlinear systems using the self-organizing fuzzy neural network with adaptive gradient algorithm. Neurocomputing 266:566–578

Hao Y, Tian C (2020) A hybrid framework for carbon trading price forecasting: the role of multiple influence factor. J Cleaner Prod 262:120378

He Y, Zheng Y (2018) Short-term power load probability density forecasting based on Yeo-Johnson transformation quantile regression and Gaussian kernel function. Energy 154:143–156

He Q, Wu C, Si Y (2022) LSTM with particle Swam optimization for sales forecasting. Electron Commerce Res Appl 51:101118

Huang Y, He Z (2020) Carbon price forecasting with optimization prediction method based on unstructured combination. Sci Total Environ 725:138350

Huang W, Wang H, Qin H, Wei Y, Chevallier J (2022) Convolutional neural network forecasting of European Union allowances futures using a novel unconstrained transformation method. Energy Econ 110:106049

Jebli I, Belouadha FZ, Kabbaj MI, Tilioua A (2021) Prediction of solar energy guided by pearson correlation using machine learning. Energy 224:120109

Jia Y, Li G, Dong X, He K (2021) A novel denoising method for vibration signal of hob spindle based on EEMD and grey theory. Measurement 169:108490

Jianwei E, Ye J, He L, Jin H (2021) A denoising carbon price forecasting method based on the integration of kernel independent component analysis and least squares support vector regression. Neurocomputing 434:67–69

Khalfaoui R, Jabeur SB, Dogan B (2022) The spillover effects and connectedness among green commodities, bitcoins, and US stock markets: evidence from the quantile VAR network. J Environ Manage 306:114493

Khosravi A, Nahavandi S, Creighton D, Atiya AF (2011) Lower upper bound estimation method for construction of neural network-based prediction intervals. IEEE Trans Neural Netw 22(3):337–346

Kim W, Han Y, Kim K, Song K (2020) Electricity load forecasting using advanced feature selection and optimal deep learning model for the variable refrigerant flow systems. Energy Rep 6:2604–2618

Kingma D, Ba J (2014) Adam: a method for stochastic optimization. In: Proceedings of the International Conference on Learning. The initial address is as follows: https://arxiv.org/abs/1412.6980

Lecun Y, Bengio Y, Hinton G (2015) Deep learning. Nature 521(7553):436

Lee SK, Lee H, Back J, An K, Yoon Y, Yum K, Kim S, Hwang S (2021) Prediction of tire pattern noise in early design stage based on convolutional neural network. Appl Acoust 172:107617

Li H, Wang J, Li R, Lu H (2019) Novel analysis-forecast system based on multi-objective optimization for air quality index. J Cleaner Prod 208:1365–1383

Li L, Chang Y, Tseng ML, Liu J, Lim M (2020) Wind power prediction using a novel model on wavelet decomposition-support vector machines-improved atomic search algorithm. J Cleaner Prod 270:121817

Lin G, Lin A, Cao J (2020) Multidimensional KNN algorithm based on EEMD and complexity measures in financial time series forecasting. Expert Syst with Appl 168:114443

Lin Y, Yan Y, Xu J, Liao Y, Ma F (2021) Forecasting stock index price using the CEEMDAN-LSTM model. N Am J Econ Finance 57:101421

Lu H, Ma X, Huang K, Azimi M (2020) Carbon trading volume and price forecasting in China using multiple machine learning models. J Cleaner Prod 249:119386

Perera I, Silvapulle MJ (2020) Bootstrap based probability forecasting in multiplicative error models. J Econ 221(1):1–24

Pincus SM (1991) Approximate entropy as a measure of system complexity. Proc Nat Acad Sci USA 88(6):2297–2301

Qiao D, Li P, Ma G, Qi X, Yan J, Ning D, Li B (2020) Realtime prediction of dynamic mooring lines responses with LSTM neural network model. Ocean Eng 219:108368

Richman J, Moorman J (2000) Physiological time-series analysis using approximate entropy and sample entropy. Am J Physiol - Heart Circ Physiol 278(6):H2039–H2049

Sun W, Wang Y (2018) Short-term wind speed forecasting based on fast ensemble empirical mode decomposition, phase space reconstruction, sample entropy and improved back-propagation neural network. Energy Conversion Manage 157:1–12

Sun W, Zhang C (2018) Analysis and forecasting of the carbon price using multi—resolution singular value decomposition and extreme learning machine optimized by adaptive whale optimization algorithm. Appl Energy 231:1354–1371

Sun S, Sun Y, Wang S, Wei Y (2018) Interval decomposition ensemble approach for crude oil price forecasting. Energy Econ 76:274–287

Torres ME, Colominas MA, Schlotthauer G, Flandrin P (2011) A complete ensemble empirical mode decomposition with adaptive noise. In: 2011 IEEE International Conference on Acoustics, Speech and Signal Processing (ICASSP). IEEE, Prague, Czech Republic, pp 4144–4147

Wang S, Wang S, Wang D (2019) Combined probability density model for medium term load forecasting based on quantile regression and kernel density estimation. Energy Procedia 158:6446–6451

Wu Q, Lin H (2019) Daily urban air quality index forecasting based on variational mode decomposition, sample entropy and LSTM neural network. Sustainable Cities Soc 50:101657

Xu H, Wang M, Jiang S, Yang W (2020) Carbon price forecasting with complex network and extreme learning machine. Phys A: Stat Mech Appl 545:122830

Yang S, Chen D, Li S, Wang W (2020) Carbon price forecasting based on modified ensemble empirical mode decomposition and long short-term memory optimized by improved whale optimization algorithm. Sci Total Environ 716:137117

Zeng S, Jia J, Su B, Jiang C, Zeng G (2021) The volatility spillover effect of the European Union (EU) carbon financial market. J Cleaner Prod 282:124394

Zhang C, Zhao Y, Zhao H (2022) A novel hybrid price prediction model for multimodal carbon emission trading market based on CEEMDAN algorithm and window-based XGBoost approach. Mathematics 10(21):4072

Zhao L, Hu C (2016) Research on influencing factors of China's carbon emissions trading price. An empirical analysis based on structural equation model. Price:Theory Pract 7:101–104

Zhao H, Zhao Y, Guo S (2020) Short-term load forecasting based on complementary ensemble empirical mode decomposition and long-short term memory. Electric Power 53(6):48–55

Zhao L, Miao J, Qu S, Chen X (2021) A multi-factor integrated model for carbon price forecasting: market interaction promoting carbon emission reduction. Sci Total Environ 796:149110

Zhao Y, Su Q, Li B, Zhang Y, Wang X, Zhao H, Guo S (2022) Have those countries declaring “zero carbon” or “carbon neutral” climate goals achieved carbon emissions-economic growth decoupling? J Cleaner Prod 363:132450

Zhao Y, Zhou Z, Zhang K, Huo Y, Sun D, Zhao H, Sun J, Guo S (2023) Research on spillover effect between carbon market and electricity market: Evidence from Northern Europe. Energy 263:126107

Zheng J, Mi Z, Coffman D, Milcheva S, Shan Y, Guan D, Wang S (2019) Regional development and carbon emissions in China. Energy Econ 81:25–36

Zhou K, Li Y (2019) Influencing factors and fluctuation characteristics of China's carbon emission trading price. Phys A: Stat Mech Appl 524:459–474

Zhou Q, Sun W, Zhang Y, Ren H, Sun C, Deng J (2011) A new method to obtain load density based on improved ANFIS. Power Syst Prot Control 39(1):29–34+39

Zhou X, Gao Y, Wang P, Zhu B, Wu Z (2022) Does herding behavior exist in China’s carbon markets? Appl Energy 308:118313

Zhu B, Han D, Wang P, Wu Z, Zhang T, Wei Y (2017) Forecasting carbon price using empirical mode decomposition and evolutionary least squares support vector regression. Appl Energy 191:521–530

Zhu J, Wu P, Chen H, Liu J, Zhou L (2019) Carbon price forecasting with variational mode decomposition and optimal combined model. Phys A: Stat Mech Appl 519:140–158

Acknowledgements

The authors are grateful to the editor and anonymous reviewers for their work.

Availability of data and materials

The [carbon price and influencing factors] data used to support the findings of this study are included in Supplementary information. For more details, please consult the corresponding author on reasonable request.

Funding

This study is supported by the Natural Science Foundation of China under Grant No. 71973043.

Author information

Authors and Affiliations

Contributions

Yihang Zhao: writing, visualization, software. Huiru Zhao: conceptualization, reviewing. Bingkang Li: data curation, supervision. Boxiang Wu: data curation. Sen Guo: reviewing and editing.

Corresponding author

Ethics declarations

Ethics approval and consent to participate

Not applicable.

Consent for publication

Not applicable.

Competing interests

The authors declare no competing interests.

Additional information

Responsible Editor: Nicholas Apergis

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Highlights

• A hybrid point and interval forecasting model for carbon trading price is proposed.

• The efficacy is tested in all the carbon trading markets in China.

• The proposed model can greatly enhance the prediction performance.

• The interval prediction for carbon trading price has more practical application value.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Zhao, Y., Zhao, H., Li, B. et al. Point and interval forecasting for carbon trading price: a case of 8 carbon trading markets in China. Environ Sci Pollut Res 30, 49075–49096 (2023). https://doi.org/10.1007/s11356-023-25151-0

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11356-023-25151-0