Abstract

This paper explores the influence of economic policy uncertainty on environmental quality in selected MENA countries depending on an augmented STIRPAT model over the period 1970–2020. ARDL model and its extensions like augmented ARDL, augmented NARDL, and MTNARDL models are applied to detect any possible effect from uncertainty index to carbon dioxide (CO2) emissions. The empirical results reveal the validity of environmental Kuznet curve (EKC) curve in all the countries. Moreover, the results show that the uncertainty index enhances environmental degradation, especially in extremely large changes in Morocco, Turkey, and Iran. Besides, the findings reveal that energy consumption and population in the entire sample escalates CO2 emissions over the study period. Consequently, policymakers in MENA countries should consider the economic uncertainty index, particularly in light of its recent rise, when developing any strategies and plans aimed at improving environmental standards, as well as the need to encourage the use of renewable energies in order to increase the percentage of their contribution to total energy consumption.

Similar content being viewed by others

Introduction

Climate change and global warming have become one of humanity’s most significant challenges in recent years (Jahanger et al. 2022a). The carbon dioxide (CO2) levels in the atmosphere have risen in recent decades, coinciding with an increase in global average temperature (Jahanger et al. 2021a). In actual digit, the CO2 levels in the atmosphere have increased by around 40% since the mid-nineteenth century, and our world is warming at a rate of 0.2° per decade (Cramer et al. 2018; Ahmad et al. 2022; Yang et al. 2022). Relayed to Solomon et al. (2007), increased greenhouse gas concentrations result in a 2 °C increase in global average temperature, as they suggest that our planet’s average temperature could be between 2 and 9.7°F (1.1 to 5.4 °C) warmer in 2100 than it is today. It demonstrates that the Earth’s climate warmed between 1880 and 2012 and that human activities that alter the atmosphere are likely to have played a pivotal role (Al-Ghussain 2019; Jahanger et al. 2021b; Khalid et al. 2021).

It is observed that the biodiversity damage was noticed at the level of ecosystems by the deforestation that has led to the loss of six million hectares per year of forest since 2000 (Laurent and Le Cacheaux 2012). This loss can provide a high cost for human development and the environment. In the past, this deterioration was mostly caused by natural phenomena, but now they are caused by anthropogenic factors (the result of human actions), such as the destruction of the environment of the species by the overexploitation of the resources, such as oil, coal, gold, and others (Sharif et al. 2019; Usman et al. 2021, 2022). Despite the fact that the conventions have been signed by the United Nations for environmental protection and against poverty in the world, the ruin of natural biodiversity and ecosystems continues its degradation and that getting worse and worse (Ramzan et al. 2022; Sharif et al. 2020a; Huang et al. 2022). According to Friedlingstein et al. (2010), they noticed that before 2100, the quantity of carbon will increase by 9 times than now and it is going to reach an unbelievable quantity of carbon that the atmosphere would not be able to support. Therefore, such outcomes push policymakers to search for solutions to the coming environmental disaster (Ke et al. 2022; Sari-Hassoun et al. 2019). The depletion of natural resources and pollution has become a severe issue that necessitates a rethinking of current government policy (Sharif et al. 2020b; Jahanger et al. 2022b; Usman and Balsalobre-Lorente 2022; Sari-Hassoun and Ayad 2020). Governments all across the world acknowledge that the existing growth model is unsustainable, and they are advocating for the environmental impact of economic expansion to be taken into account by proposing and implementing sustainable development as an integrated policy (Yang et al. 2021; Usman et al. 2020; Ramzan et al. 2021; Kamal et al. 2021).

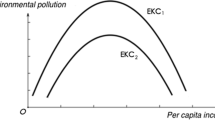

Today’s scholars admit that humans have a significant impact on the climate system, and the debate is whether the economic expansion will automatically result in increased carbon emissions or not. Thus, several researchers (Qader et al. 2021; Destek and Sarkodie 2019; Sadiq et al. 2022) pointed out that the investigation of the environmental Kuznets curve (EKC) hypothesis can give a holistic view of the link between economic growth and pollution. Kuznets (1955) studied several graphs of the economic inequality against per capita income over the economic development, but since then, Grossman and Krueger (1991) and Nemat (1994) have transferred the curve of Kuznets into a new model and new hypothesis, which is called the EKC. This hypothesis examines the association between pollution and economic growth (Sari-Hassoun et al. 2019). In the first period, the economic growth can escalate the rate of pollution the way of industry and chemical production, especially for the nations, which rely on fossil fuel production (Chen and Taylor 2020). In the second period, when the countries depend on cleaner industry and green production, the economic factor can decrease the level of pollution (Dogan and Ozturk 2017; Usman and Radulescu 2022). Akalpler and Hove (2019) claimed that further economic expansion would degrade the ecology and ecosystem due to technological advances and the development of new unsafe products, resulting in demographic, social, and ecological concerns.

The last three decades have been marked by research into how different economic and social factors affect greenhouse gas emissions in all nations of the world in order to pinpoint the main reasons why environmental pollution has become a pressing issue that has to be addressed. Li et al. (2022) in the context of China as one of the top three emitter countries revealed that natural resources rent, financial development, and energy investment play a pivotal role in CO2 emissions in all China provinces over the period of 1995–2017. Additionally, the authors showed that green investments could be effective in improving the environmental quality against the other determinants of CO2 emissions, but these investments are still very limited. In addition, Liu et al. (2021) revealed that household consumption significantly increases carbon emissions, but that by using renewable energy sources, this consumption can become a key component in enhancing environmental circumstances. This finding is consistent with the study of Chica-Olmo et al. (2020) for the case of 26 European countries. Besides, Khan et al. (2022) exposed that energy efficiency and renewable electricity decrease the CO2 emissions in the Next Eleven countries. In the long term, however, economic growth, financial inclusion, and trade openness are major factors influencing CO2 emissions. Murshed et al. (2022) revealed that the G-7 countries’ use of nuclear power has the potential to cut CO2 emissions over the long term, whereas their use of renewable energy has the opposite effect. Besides, the economic complexity could be an important solution to reducing carbon footprint levels.

The classical study of decisions under uncertainty, on the other hand, stretches back to Savage (1954), but recent research began with Ellsberg’s behavioral paradoxes (1961). Following that, this argument is expanded upon using Schmeidler’s (1989) theoretical analysis, with some crucial ideas dating back to Keynes (1921, 1936). Arrow and Fisher (1974) and Henry (1974) developed new rational decision-making models for environmental economics, and several scholars followed suit with surveys of uncertainty in environmental economics. (Mäler and Fisher 2005; Pindyck 2007; Aldy and Viscusi 2014; Usman et al. 2022). However, the COVID-19 pandemic that occurred in 2019 has generated huge economic policy uncertainty. Therefore, our focus here is on economic policy uncertainty (EPU), which is defined as the unpredictability of government regulatory, monetary, and fiscal policies that affect the economic agents’ outputs and the environment in which they function. It may also have environmental concerns with its economic ones (Wang et al. 2020; Li et al. 2022; Hussain et al. 2022). The EPU may encourage producers to use conventional, environmentally unfriendly procedures of manufacturing, resulting in higher carbon dioxide outputs (Anser et al. 2021a). On the other hand, EPU may have an impact on consumption and investment, resulting in lower CO2 emissions (Liu and Zhang 2021). Furthermore, due to high EPU, reductions in R&D, innovation, and renewable energy usage could result in increased CO2 emissions. As a result, the link between EPU and carbon emissions must be investigated to develop any environmental measures (Adedoyin and Zakari, 2020; Anser et al. 2021b; Balsalobre-Lorente et al. 2022).

The main contributions of this paper can be summarized as follows. First, this paper is an attempt to compare the effects of economic uncertainty on CO2 emissions in the Middle East and North Africa (MENA) countries, particularly those with very high carbon emissions from oil production (Algeria, Iran, and Saudi Arabia), as well as non-oil producer (Morocco, Egypt, and Turkey) countries. Second, this novel work adds to the body of literature by utilizing several autoregressive distributed lags (ARDL) methods to identify any potential impacts of uncertainty on carbon emissions. This study employs the augmented ARDL model to deal with the original series, in addition to nonlinear autoregressive distributed lags (augmented NARDL) presented by Sam et al. (2019) to detect the possible hidden co-integration proposed by Granger and Yoon (2002). Furthermore, as declared by Li and Guo (2022), the NARDL model with only one threshold is not flexible in detecting the different kinds of changes in the independent variable. In the light of this statement, this paper uses the multiple threshold nonlinear autoregressive distributed lag (MTNARDL) models, which allows us to use more than one threshold. The key improvement of such a model is when we are aware that changes in the uncertainty index are accompanied by various responses from other variables, as the rise or fall of uncertainty in tiny percentages does not have the same impact as the rise or fall in uncertainty in big percentages (Anser et al. 2021a). Hence, this study employs the modern ARDL model with multiple thresholds presented by Pal and Mitra (2015) to examine and even the extremely small and large changes effects of uncertainty on carbon emissions. Moreover, the most significant additional benefit of this methodology is that it enables decision-makers to deal with any type of shocks or changes that occur in economic uncertainty, allowing them to create different and flexible policies that can deal with different levels of uncertainty and avoid using conventional methods to deal with economic variables. In other words, decision-makers can select from a range of tactics and techniques to manage any potential imbalance by applying different thresholds when using the MTNARDL model estimation. Thirdly, this study compares these nations in the context of the environmental Kuznets curve to investigate the relationship between economic growth and environmental quality and to determine whether a turning point exists in order to calculate the ideal rates of economic growth to reduce carbon emissions.

The paper is structured into five sections: the introduction, which covers a basic overview of climate change, economic growth, energy, and uncertainty, is the first section. The second section includes a review of the literature, and the third section includes data and methods. The model and empirical results are presented in the fourth section, while discussion and policy implications are presented in the fifth section.

Literature review

Literature on EKC hypothesis

The environmental Kuznets curve (EKC) hypothesis is based on the finding that economic development is linked to an increase in environmental destruction up to a certain level, after which environmental quality starts to recover. Several empirical investigations looking into the EKC hypothesis employed polynomial regression (inverted U-shape, N-shape, and M-shaped EKC) (Ozokcu and Özdemir 2017; Balsalobre-Lorente et al. 2022). These shapes (U with one turning point, N with two points, and M with three points) may be analyzed sequentially in determining the best-fit curve to see if an inverse trend suggesting less environmental deterioration emerges when wealth rises above a specific level. It is possible for a cubic function to increase quicker than falls or vice versa (Lieb 2003).

Jalil and Mahmud (2009) studied the relationship between gross domestic product (GDP) and CO2 emissions in China over the period from 1975 to 2005. They suggest that CO2 emissions and economic growth association take the inverted U shape under the EKC hypothesis. Shahbaz et al. (2014) analyzed the EKC hypothesis in addition to a causality analysis among CO2 emission, GDP per capita, energy use, and trade openness in Tunisia using ARDL procedure and innovative accounting approach over the period of 1971–2010. They found evidence of the EKC hypothesis with an inverted U shape. Dogan and Ozturk (2017) examined the EKC hypothesis in the USA over the period from 1980 to 2014. They used the variables of CO2 emissions, GDP, square of GDP (GDPsq), renewable, and non-renewable energy consumption. They established that the EKC hypothesis is not valid, because the expansion in production level will not stop the USA’s growth and will create a collapse in the environment. Sari-Hassoun et al. (2019) investigated the link between fossil energy, renewable energy, carbon dioxide emissions, and economic growth in Algeria during the period of 1995–2016. To analyze the influence in the short and long term, they used Granger causality and the vector error correction model (VECM). The authors concluded that an increase in economic growth, fossil energy production, and consumption will result in an increase in carbon dioxide emissions, but an increase in renewable energy consumption will result in a decrease in income growth and carbon dioxide emissions, confirming that the EKC hypothesis is not supported in Algeria. They came to the conclusion that there is short-term unidirectional causation going from renewable energy use to carbon dioxide emissions and bidirectional causality between carbon dioxide emissions and economic growth. Moreover, Murshed et al. (2021) examined the EKC hypothesis in Bangladesh using Maki co-integration and ARDL framework over the period 1980–2015. Clearly, the results exposed the existence of the EKC hypothesis showing that Bangladesh is still in the development phase of the relationship between economic growth and CO2 emissions. Finally, In South Asia countries, Murshed (2021) revealed the presence of the EKC hypothesis in India, Bhutan, Bangladesh, and Sri Lanka.

Economic policy uncertainty

Existing literature attempts to characterize uncertainty by pointing to several measurements of uncertainty, but in this study, we shall focus on economic policy uncertainty only. Tiwari, Jana, and Roubaud (2019) said that the economic policy uncertainty affects the economic agents’ behavior such as consumption and investment decisions, and it is relating to monetary, fiscal, trade, and other interrelated policies. Moreover, the worldwide financial issues caused by the global financial crisis of 2007–2009, US and European taxation, the European debt crisis, the US–China trade war, Brexit, and other events have made the economic policy uncertainty gain more attention, according to Al-Thaqeb and Algharabali (2019). The EPU influences the government’s regulatory, monetary, and fiscal policies that change the situation in which people and businesses function. Higher EPU could affect several macroeconomic indicators (economic growth, investment, financial development, trade, tourism, oil prices, and innovation) at the company levels such as national and international markets and activities (Pirgaip and Dinçergök, 2020).

Using the dynamic ARDL simulations model, Bhowmik et al. (2022) examined the environmental Phillips curve (EPC) hypothesis between unemployment and CO2 emissions in the USA as well as the impact of several uncertainty indexes (monetary, fiscal, and trade uncertainties) on environmental degradation. The findings demonstrated the long-term validity of the EPC hypothesis. Additionally, the findings revealed a positive association between monetary policy uncertainty and CO2 emissions, whereas fiscal policy uncertainty causes emissions to decline. Contrarily, the results showed that trade policy uncertainty might not have any effect at all on emissions. Similarly, depending on the bootstrap ARDL model, Syed and Bouri (2021) investigated the impact of EPU on CO2 emissions in the USA from January 1985 to December 2019. The results showed diverse outcomes in the short and long term. On the one hand, it is evident that EPU increases CO2 emissions in the short run, which causes more environmental damage. On the other hand, EPU decreases emissions, which improves the quality of the environment. Moreover, Syed et al. (2022) studied the impact of EPU and geopolitical risk on CO2 emissions in BRICST countries (Brazil, Russia, India, China, South Africa, and Turkey) over the period 1990–2015 using quantile regressions. The results revealed that EPU decreases CO2 emissions in both lower and middle quantiles in contrast to higher quantiles where the EPU increases the emissions. Conversely, the geopolitical risk upsurges the emissions in the lower quantiles and drops the emissions in both middle and higher quantiles. In the same frame, Anser et al. (2021a, b) dealt with the same topic as Syed et al. (2022), but in a group of emerging countries (Mexico, China, Brazil, and Colombia) over the period 1995–2015. The findings showed clearly that EPU and energy use escalate CO2 emissions in contrary to geopolitical risk and renewable energy use.

Jiang et al. (2019) used the Granger causality in quantiles to analyze the causal link between EPU and CO2 emissions (both its growth rate and uncertainty index) on both aggregate and sectoral levels in the USA for the period from January 1985 to August 2017. They established that there is a unidirectional causal link running from EPU to CO2 emissions in both high and low quintiles. Adedoyin and Zakari (2020) used ARDL and Granger causality to examine the contribution of EPU in the relationship between CO2 emissions, GDP, and energy use in the UK for the period 1985–2017. They found that the economic policy uncertainties reduce the level of CO2 emissions in the short run, however, in the long run; it needs relevant policies to reduce the rise of carbon emissions according to the positive effect of EPU on CO2 emissions. The causality results show the existence of unidirectional causality running from energy use to CO2 emissions, from CO2 emissions to EPU, and from energy use to EPU as well. Pirgaip and Dinçergök (2020) studied the causal link between EPU, energy consumption, and carbon emissions using Konya’s panel causality in the context of G-7 countries from 1998 to 2018. The results revealed the existence of Granger causal link from EPU to CO2 emissions in the USA, Germany, and Canada; however, there is a unidirectional causality running from CO2 emissions to EPU in Italy. Furthermore, their findings explore that policies promoting reduced energy consumption and CO2 emissions, as well as the use of alternative energy sources, should be implemented in G-7 countries to help mitigate the impact of EPU to improve the environment quality. Danish et al. (2020) analyzed the role of EPU on CO2 emissions in the USA over the period from 1985 to 2017. They concluded with dynamic ARDL simulations that EPU increases the level of carbon dioxide with a fundamental role in environmental humiliation. Amin and Dogan (2021) investigated the impact of EPU on the energy-CO2 emissions connection in China from 1980 to 2016. They used the recent ARDL model presented by Jordan and Philips (2018) examined the effect of EPU shocks on energy use and CO2 emissions depending on dynamic simulations, the results showed that EPU has a significant and positive impact on CO2 emissions, showing that high economic policy uncertainty, real income growth, and energy intensity increase highly the emissions of carbon. However, renewable energies play an important role in mitigating CO2 emissions that can be a determinant solution to avoid environmental degradation in the long run.

Furthermore, Abbasi and Adedoyin (2021) employed a dynamic ARDL simulation approach to examine the shocks of energy use, EPU, and real income growth, on carbon dioxide emissions during the period from 1970 to 2018 in China. The findings show that both energy use and real income growth have positive and significant coefficients, while the sign EPU coefficient was positive but insignificant. Zakari et al. (2021) examined the influence of real income growth, energy use, and EPU on carbon dioxide emissions in 22 Organisation for Economic Co-operation and Development (OECD) countries during the period of 1985–2017. They employed the methodology of PMG-ARDL (Pooled Mean Group ARDL) and they found that EPU, real income growth, and energy use have a positive and statistically accept coefficient, leading to an increase in the level of CO2 emissions in such countries.

EKC hypothesis and economic policy uncertainty

Several studies examine the hypothesis of EKC under the effect of the EPU on the energy use CO2 emissions nexus. Adams et al. (2020) considered the relationship between EPU and CO2 emissions in the presence of both energy consumption, and geopolitical risk for 10 resource-rich countries over the period of 1996—2017. They found with the PMG-ARDL model that EPU, income growth, and energy use contribute positively and significantly to the raised CO2 emissions, in the long run, this result, therefore, stimulates the environmental pollution in such countries. Furthermore, the results demonstrated the existence of U shapes EKC in the short run, but on the other hand, they proved that EKC is constant in the long run. Wang et al. (2020) studied the impact of real income growth, energy prices, and the World Uncertainty index on CO2 emissions in the USA spanning the period 1960–2016 depending on the ARDL model. The results explored a positive effect from EPU on CO2 emissions through two channels, which are the consumption, and the investment effects. The first suggests that EPU can decrease energy consumption as a response to a rise in EPU, thus CO2 emissions decline. The second effect suggests that high EPU can harm renewable energy investments; thus, CO2 emissions increase automatically using non-renewable energies. Therefore, they proposed developing stable and transparent policies in order to minimize these effects and improve environmental quality. Furthermore, they validated also the EKC hypothesis in the USA. Anser et al. (2021a) employed the CO2 and Anser et al. (2021b) emissions, real income growth, energy consumption, total population, and the world uncertainty index (as a proxy of Economic Policy Uncertainty) to analyze the influence of economic policy uncertainty on CO2 emissions. The authors used PMG-ARDL modeling for the top 10 carbon emitter countries, which are China, the USA, India, Russia, Japan, Germany, Iran, Saudi Arabia, South Korea, and Canada during the period 1990–2015. They found that the world uncertainty index influence positively and significantly the emissions of CO2, and there is evidence of the EKC hypothesis for these countries.

Moreover, Liu and Zhang (2021) analyzed the instruments of how EPU influences carbons emissions and its role in controlling the environmental regulation–CO2 emissions nexus for 30 provinces of China during the period from 2003 to 2017. The authors employed a fixed-effects panel model and linear regression with Driscoll-Kraay standard errors. They used CO2 emissions as a dependent variable, followed by independent variables GDP, GDPsq, energy consumption, environment regulation (ER), economic policy uncertainty (EPU), and they introduced the concept of (EPU*ER) to establish the moderating role of EPU on the environmental regulation–carbon emissions nexus. The findings show that there is a negative impact of EPU on carbon emissions, while the other variables have a positive influence on carbon emissions. Also, the interactive term (EPU*ER) has a positive and significant coefficient, confirming that environmental regulations have significantly promoted carbon emissions (evidence of green paradox), and it implies that EPU has a positive impact on the environment regulation-carbon emissions nexus. This study confirmed the evidence of the EKC hypothesis in the eastern and central regions.

Data, model construction, and methodological framework

Data and model construction

Our analysis is mainly based on Dietz and Rosa (1994) model named STIRPAT (Stochastic Impacts by Regression on Population, Affluence and Technology) model which examines the effect of socioeconomic factors on environmental quality including technology, affluence, and population. Thus, our STIRPAT model can be written as follows:

where CO2 shows the carbon dioxide emissions, POP illustrates the population growth, GDP denotes the gross domestic product per capita, and ENE represents energy consumption. Moreover, to avoid the issue of heterogeneity, we transform our STIPRAT model into logarithmic form following Usman and Hammar (2021) and Yang et al. (2022) as follows:

As stated previously, we aim in this paper to investigate the effect of uncertainty on CO2 emissions using the World Uncertainty Index (WUI) presented by Ahir et al. (2022); therefore, we introduce the WUI variable into our STIRPAT model. In addition, the authors incorporate the GDP square (GDPsq) variable into the model with the GDP variable to test the EKC hypothesis with the expectation of positive and negative effects of GDP and GDPsq on CO2 emissions respectively, following Apergis and Ozturk (2015). Finally, our empirical model used is as follows:

Moreover, our analysis uses annual data for six selected MENA countries depending on availability data (Algeria, Egypt, Iran, Morocco, Saudi Arabia, and Turkey) spanning the period 1970–2020. Noteworthy, the WUI index is available only on quarterly bases, for this reason, and following Anser et al. (2021a), we convert the quarterly data into yearly data by calculating the average of four quarters for each year. The descriptions of all variables are reported in Table 1.

Descriptive statistics of the variables are presented in Table 2. Remarkably, all the series in most cases are normally distributed except WUI and GDP for Algeria and Saudi Arabia. Besides, it is important to shed light on maximum and minimum values of GDP, whereas, we will need it in the comment on the threshold of the EKC curve. For the correlations matrix, the energy consumption and CO2 emissions in all countries except Iran are positively and significantly correlated, showing that ENE is a fundamental explanation for CO2 emissions. In juxtaposing, the same result is achieved with population-CO2, and GDP-CO2 emissions relationships (except in Saudi Arabia where there is a negative association).

Methodology

Since Pesaran et al. (2001), the ARDL bounds test approach has become widely used in economic studies. Whereas traditional tests like Engel Granger and Johansen tests require all series to be of type I (1), the ARDL methodology, which allows for a mixture of type I (0), and I (1) variables, is the best option for researchers to study the co-integration relationship between their variables, given that no variable is of type I (2). Furthermore, the typical ARDL model established three key assumptions: first, the independent variables must be exogenous, second, the dependent variable must be integrated into order one I (1), and third, there must be no degenerate cases (McNown et al. 2018). As a result, according to Sam et al. (2019), many papers and researchers have neglected these assumptions, resulting in ambiguous results. Moreover, the ARDL approach suggested two tests to examine the cointegration relationships, one for the lagged level variables (LLV) named the overall F test, and the second for the lagged level of the dependent variable (LLDV) named the t-test. However, in order to avoid the degenerate instances indicated above for the third assumption of the ARDL model, these two tests require the dependent variable to be an I (1) series as a strong assumption. On one hand, the acceptance of the significance of the overall F test means that the lagged level of all variables is together significant; on the other hand, the t-test allows us to avoid the degenerate lagged dependent variable described by McNown et al. (2018). This last suggests that the significance of the overall F test can be due to the significance of LLDV or the lagged level of independent variables (LLIV) solely. Resultantly, if only the LLDV is significant, we get the Dickey-Fuller equation and the dependent variable is the I (0) series.

For all these reasons, McNown et al (2018) proposed a third test to examine the significance of LLIV to eliminate the I (1) assumption for the dependent variable. To get a clear idea about the three hypotheses, we introduce our ARDL model in this study as follows:

where \({\varphi }_{1}\) is the intercept of the model; \({\gamma }_{ji}\) represents the short run estimators; \({\beta }_{j}\) indicates the long run estimators; and \({\varepsilon }_{t}\) is the white noise of estimation while \(\Delta\) represents the first difference operator, in addition. Thus, the three hypotheses are as follows:

Overall F test on LLV is presented as \({H}_{0A}: {\beta }_{1}={\beta }_{2}={\beta }_{3}={\beta }_{4}={\beta }_{5}={\beta }_{6}=0\);

The t-test on LLDV is presented as: \({H}_{0B}: {\beta }_{1}=0\)

F test on LLIV is presented as: \({H}_{0A}: {\beta }_{2}={\beta }_{3}={\beta }_{4}={\beta }_{5}={\beta }_{6}=0\)

As a result, the AARDL model (augmented ARDL model) provides two sets of critical values: I (0) critical values are lower bounds achieved when variables are completely I (0), while I (1) critical values are upper bounds in the case of all variables are purely I (1). Therefore, on the one hand, the null hypothesis will be rejected only if the test statistic exceeds the upper critical value; on the other hand, the null hypothesis cannot be rejected if the test statistic is below the lower bounds. Notably, if the test statistic falls between the upper and lower boundaries, the test will be indecisive; for this reason, they applied a bootstrapping technique to get new critical values to avoid this situation.

On the other extreme, since Granger and Yoon (2002) work, the hidden cointegration concept has become very important in time series analysis. According to Stock and Watson (1988), variables are co-integrated when they respond to the same shocks together and are not co-integrated when they respond to the same shocks separately. Going further, Granger and Yoon (2002) showed that some series could move together only in the case of the positive shock but not with negative ones or vice versa. For this reason, they suggested a new procedure to put a threshold at zero to get positive and negative sums to detect independently both appreciations and depreciations of independent variables’ effects on dependent variables. Therefore, in this paper, we aim to examine the asymmetric effects of uncertainty on CO2 emissions by decomposing the WUI variable into its positive and negative changes as follows:

where \({\mathrm{WUI}}_{t}= {\mathrm{WUI}}_{0}+ {\mathrm{WUI}}_{t}^{+}+{\mathrm{WUI}}_{t}^{-}\). Consequently, the NARDL model following Shin et al. (2014) can be written as follows:

where \({\mathrm{WUI}}_{t}^{+}\) and \({\mathrm{WUI}}_{t}^{-}\) are positive and negative changes of the WUI variable respectively. Thus, the co-integration nexus in Eq. 5 can be verified due to the null hypothesis proposed by Shin et al. (2014) using Pesaran et al. (2001) and Narayan (2005) critical values depending on standard bounds tests, which is\({H}_{0}: {\beta }_{1}={\beta }_{2}={\beta }_{3}={\beta }_{4}={\beta }_{5}={\beta }_{6}={\beta }_{7}=0\). Besides, this allows us to test the asymmetric behavior in the long-run term by setting (\({\beta }_{6}/-{\beta }_{1}= {\beta }_{7}/-{\beta }_{1})\) along with short-run asymmetry by setting (\(\sum_{i=0}^{p-1}{\gamma }_{6i}=\sum_{i=0}^{p-1}{\gamma }_{7i} )\), according to normal Wald test.

Additionally, to confirm the long-term link between the variables, the augmented NARDL model can be examined utilizing the three hypotheses in line with Sam et al. (2019) work on the ARDL model. Furthermore, Pal and Mitra (2015) have introduced the MTNARDL model, which is an extension of the NARDL framework with multiple thresholds instead of a single threshold. Thus, using several partial sums, we can determine the impact of extremely small and large changes in independent variables on the dependent variable. Therefore, in this paper, we will use an MTNARDL model with three thresholds denoted by \({\tau }_{25}\), \({\tau }_{50}\), and \({\tau }_{75}\) to get partial sum series in quintiles 25th, 50th, and 75th respectively given that \({\mathrm{WUI}}_{t}^{i}= {\mathrm{WUI}}_{0}^{i}+ {\mathrm{WUI}}_{t}^{i}\left({\omega }_{1}\right)+{\mathrm{WUI}}_{t}^{i}\left({\omega }_{2}\right)+{\mathrm{WUI}}_{t}^{i}\left({\omega }_{3}\right)+{\mathrm{WUI}}_{t}^{i}\left({\omega }_{4}\right)\) calculated as given:

where \(I\left\{T\right\}\) is an indicator function with the value one if the condition T is satisfied and zero value if not? Hence, our MTNARDL model will be:

where the null hypothesis is \({H}_{0}: {\beta }_{1}={\beta }_{2}={\beta }_{3}={\beta }_{4}={\beta }_{5}={\beta }_{6}={\beta }_{7}={\beta }_{8}={\beta }_{9}={\beta }_{10}=0\), which is tested by standard critical values suggested by Pesaran et al. (2001). Returning to the Sam et al. (2019) publication, it is evident that there are no critical values for more than six independent variables; nevertheless, since our models contain more than seven independent variables, we are unable to apply the Augmented MTNARDL model.

Results and discussion

Unit root tests results

Generally, the first step in time series analysis is the unit root test to detect the integration order of the series to avoid spurious regressions and results. Additionally, the ARDL procedure and its extensions are used in this article, and this procedure demands that all series must be in order I (0) or I (1), with no I (2) series. For this reason, we use three tests to ensure that there is no I (2) series among our variables, the tests are augmented Dickey-Fuller (ADF) and Phillips Perron (PP) tests for traditional unit root tests and Zivot-Andrews (ZA) test to deal with structural breaks in the series. Table 3 demonstrates that all variables, with the exception of WUI, which is stationary at the level, are I (1) series for all of our samples employing the three tests. Resultantly, the study variables have no I (2) series, thus, we can use the ARDL equations to look at the long-run relationship between them, as well as the long-run and short-run impacts.

Augmented ARDL model estimation results

As previously stated, we use the modern augmented ARDL (AARDL) model presented by McNown et al. (2018) instead of the standard ARDL model proposed by Pesaran et al (2001). The results are presented in Table 4, which clearly showed that the three null hypotheses of no co-integration are all rejected at the 1% significance level, with the exception of Iran. Additionally, the results demonstrated that all error correction terms (ECT) are statistically significant at the 1% level, with negative coefficients indicating that all models include a long-run adjustment. As a result, Algeria, Saudi Arabia, and Iran adjust more than 40% of variations from long-run equilibrium each year (the three oil producers). However, when compared to Morocco and Egypt, it is evident from the ECT coefficient that this case’s rate of adjustment is extremely rapid, with an annual adjustment rate of more than 80%. According to Narayan (2005), the ECT coefficient between − 1 and − 2 that shows dampened fluctuations in the equilibrium path; however, the ECT coefficient in Turkey is − 1.082, which is lower than − 1. We suggest relaying to the coefficient (− 1.082) that the error correction process varies around the long-run value in a dampening way rather than monotonically converging to the equilibrium path straight. The convergence to the equilibrium path, however, happens quickly once this process is over. Moreover, the diagnostic tests indicated that there is no problem with estimation models with any autocorrelation of errors, high R-squared, no auto-regressive conditionally heteroscedasticity (ARCH) behavior, and the estimators are stable overtime except in Algeria and Iran. However, the findings revealed clearly that the uncertainty index affects the CO2 emissions neither in long-run nor in the short-run terms with the exception of Saudi Arabia and Turkey but at only a 10% significance level with a positive association.

The environmental Kuznets curve also exists in the cases of Algeria, Saudi Arabia, and Turkey because the GDPsq coefficient is significant and negative while the GDP coefficient is significant and positive. This suggests that an inverse U-shaped curve exists in the relationship between GDP and CO2 emissions in the three countries (return points are 3.98, 4.42, and 4.14, respectively). These findings are in line with the conclusion of earlier studies (Intisar et al. 2022; Wan et al. 2022; Usman and Jahanger 2021; Usman and Hammar 2021; Sadiq et al. 2022). On the other hand, the outcomes exposed that population growth plays a pivotal role in CO2 emissions in Algeria, Saudi Arabia, Morocco, and Turkey in both long-run and short-run terms, especially in Saudi Arabia where a 1% increase in population increases CO2 emissions by 4.67% in the long-run term (2.11% in Algeria, 1.19% in Morocco, and 0.71% in Turkey). Furthermore, the energy coefficient has a positive impact on CO2 emissions in all country’s samples, implying that energy consumption upsurges CO2 emissions in the long and short run.

Augmented NARDL model estimation results

Returning to Granger and Yoon (2002), we see that the concept of hidden co-integration has gained a lot of traction in the economic literature up until Shin et al. (2014) paper, in which they applied the Granger and Yoon methodology to the ARDL equation by dividing the independent variable to its positive and negative partial sums. Additionally, in order to confirm the long-term relationships between the variables, we rely on the augmented NARDL model to test the three hypotheses. Table 5 displays the outcomes of the augmented NARDL calculation, and the conclusions are summarized as follows: we found that all nations except Saudi Arabia accept the null hypothesis that there is no co-integration between negative and positive changes, as well as other factors. Furthermore, in both short- and long-run terms, the Wald test for asymmetric behavior rejects the symmetric impact of WUI on CO2 emissions only in Morocco and Iran, showing that WUI affects CO2 emissions asymmetrically and exclusively the negative changes. Thus, in the long run, a 1% reduction in WUI reduces CO2 emissions by 0.34 and 0.17% in Morocco and Iran, respectively. In juxtaposing, the uncertainty coefficient is significant only in the Turkey equation with negative changes but with a positive association, the decrease in WUI in Turkey by 1% leads to an upsurge in CO2 emissions by 0.06% in the long-run term. Furthermore, the results of the environmental Kuznets curve, population, and energy use are the same for ARDL estimation. Observably, in the case of Iran, the results revealed a U shape curve of the environmental Kuznets curve (the return point is 3.54) with a negative effect from GDP to CO2 emissions and a positive effect from GDPsq, these results indicate that GDP is higher than 3.54 in Iran improves the environmental quality in the long run term.

MTNARDL model estimation results

Table 6 presents the multinomial threshold NARDL (MTNARDL) findings. To obtain more reliable results, we used Pal and Mitra’s (2015) ARDL model with multiple thresholds, by decomposing the WUI variable into four partial sums based on three thresholds at 25, 50, and 75 quintiles. As a result, we can detect the impact of extremely small and large changes in WUI on CO2 emissions using this decomposition. The outcomes show that a co-integration relationship among the partial sums of WUI and other variables exists in the entire sample excluding Saudi Arabia. Besides, the Wald test shows that the asymmetric effect of WUI on CO2 emissions exists only in Morocco, Egypt, Turkey, and Iran. Therefore, in Turkey and Iran, both small and large changes affect positively WUI in both long- and short-run terms. In Iran on one hand, a 1% change in the second quintile (ω2) surges the CO2 emissions by 1.44 and 1.51% in the long run and short run respectively; on the other hand, a 1% change in large changes (fourth quintile ω4) increases CO2 emissions by 0.15% and 0.28% respectively. In the case of Turkey, the results indicate that a 1% change in extremely small changes (first quintile (ω1) rises CO2 emissions by 0.03 and 0.06% in the long run and short run respectively, while a 1% change in extremely large changes (fourth quintile ω4) rises CO2 emissions by 0.05 and 0.09%. In addition, in Morocco, WUI affect CO2 emissions only with large changes (ω3) where any change in large changes by 1% increases CO2 emissions by 0.9 and 0.84% in the long run and short run respectively. In the case of Egypt, at a 10% significance level, the small changes (ω2) negatively affect carbon emissions in the long-run term. Contrariwise, the uncertainty index in Algeria and Saudi Arabia affects CO2 emissions neither in long-run nor in short-run terms.

The inverse U shape of the EKC is consistently present in the whole sample. In contrast, in Iran at 5% and Egypt at 10% significance levels, the results revealed the U-shaped of EKC. Furthermore, the findings show that energy consumption worsens the environment in all countries. Population growth, on the other extreme, is a significant factor in environmental deterioration in Algeria, Saudi Arabia, and Turkey, but not in Morocco, Egypt, or Iran. Noteworthy, GDP is the major factor in CO2 emissions in Saudi Arabia, any rise in GDP of 1% increases CO2 emissions by 24.70% and 15.02% in the long and short run, respectively.

Discussion

Clearly, over the last 50 years, climate change has been a major impediment to economic and social activities. For this reason, we attempted to examine the socioeconomic determinants of CO2 emissions in selected MENA countries from 1970 to 2020 in this paper. We specifically sought to detect the impact of EPU on CO2 emissions as an important key factor of environmental quality over the last 10 years, particularly following the 2008 crisis. As previously discussed, the association between EPU and CO2 emissions must be tested and explored before proposing any climate change policies (Anser et al. 2021b). To achieve this goal, we use various econometric estimation methods to ensure the results. For example, because our dependent variable was integrated with order 0 in some countries (Algeria and Saudi Arabia), we used the augmented ARDL model presented by McNown et al. (2018) instead of the standard ARDL model, which requires that the dependent variable must be an I (1) variable. Furthermore, we use both augmented NARDL and MTNARDL models to detect any possible asymmetric effects from uncertainty to CO2 emissions. On the one hand, based on our findings, we will concentrate our discussions on the augmented ARDL results for Algeria and Saudi Arabia, as there is no evidence of asymmetric effects from WUI on CO2 emissions. On the other hand, due to the asymmetric impacts detected, we will discuss the MTNARDL results for Morocco, Egypt, Turkey, and Iran.

Particularly, the findings led to several disparate conclusions, which can be summarized as follows. First, the uncertainty index WUI has no impact on CO2 emissions in any estimation model for Algeria and Saudi Arabia, two of the major oil producers and carbon emitters in the world. This outcome is consistent with those of the Abbasi and Adedoyin (2021) study, which showed that EPU has no short- or long-term influence on carbon emissions. However, this result can be explained by the two countries’ total reliance on oil exports. Whereas uncertainty in both countries is largely related to global oil prices, and whether prices rise or fall, both countries will continue in the same context and export direction of oil exportation to avoid external shocks, which is what isolates the hydrocarbon sector from economic uncertainty. Consequently, despite external and internal shocks, carbon emissions will not change in the long run due to the stability of their economic situation (Sadiq et al. 2022).

Second, depending on MTNARDL results, the WUI index affects positively the CO2 emissions in Morocco, Turkey, and Iran in the long run confirming the results of Zakari et al. (2021), and Atsu and Adams (2021). In Iran, average (second quantile) and extremely large (fourth quantile) changes in WUI increase CO2 emissions by 1.44% and 0.15%, respectively. Notably, the effect of average changes in WUI is greater than the effect of large changes. Accordingly, the higher Iran’s uncertainty index, the lower the impact on carbon emissions, and vice versa. Therefore, while it is critical for Iran to take advantage of high levels of uncertainty in order to reduce carbon emissions, the Iranian government should tread carefully when uncertainty decreases by limiting non-environmentally friendly activities, for example, by imposing taxes on these activities, to avoid exacerbating long-term carbon emissions. Conversely, it is clear in the Turkish case that the WUI affects CO2 emissions positively in both extremely small (first quantile) and extremely large (fourth quintile). However, the effect of extremely large changes is greater than the effect of extremely small changes. This means that Turkey’s high economic uncertainty index worsens the country’s climatic situation. Thus, this result can be explained by the hustle of Turkish institutions to boost their industrial activities by relying on cheap production methods that depend primarily on oil products to reduce losses caused by uncertainty. Furthermore, in a state of economic uncertainty, these companies and firms largely avoid using renewable energies because of their high costs. In the same line, in the context of Morocco, the rise in the third quantile (average changes) of WUI by a 1% increase will lead to increase the CO2 emissions by 0.90% in the long term. Hence, this result means that Moroccan companies, in light of high economic uncertainty, tend to reduce their losses and mitigate the effects of any expected shocks by reducing production costs this is done by using low-cost methods, and the latter are often unfriendly to the environment. Therefore, this situation increases carbon emissions and exacerbates the climate situation in the long term.

Third, moving to the EKC hypothesis, the findings showed that Algeria, Saudi Arabia, Morocco, and Turkey accomplished the EKC’s inverted U-shape curve. These results are consistent with the investigations of (Amri 2017; Bouznit and Pablo-Romero 2016; Touitou and Langarita 2021) for Algeria. Alshehry and Belloumi (2017) and Samargandi (2017) confirmed the result for Saudi Arabia. Kharbach and Chfadi (2017), Sghaier et al. (2019), and Bouyghrissi et al. (2022) established the outcomes for Morocco, while Bölük and Mert (2015) and Pata (2018) for Turkey. Therefore, this means that economic growth has a positive impact on carbon emissions until a certain threshold is reached, after which the effect becomes negative. Exceeding this threshold of economic growth will allow these countries to implement new economic measures that help improve the quality of the climate, and these thresholds are estimated to be 3.98, 4.42, 2.87, and 4.34 (in logarithmic form), respectively. Nevertheless, both Algeria and Turkey were unable to cross this threshold during the study period, indicating that the effect is positive and economic growth contributes to an increase in environmental deterioration, while Saudi Arabia and Morocco have crossed this threshold on very rare occasions, indicating that economic growth contributes to an increase in carbon emissions most of the time. Contrariwise, the results showed that Iran achieved the U-shape of the EKC curve validating the results of Moghadam and Dehbashi (2018) and Asghari (2012), which means that economic growth has an inverse effect on carbon emissions until a certain threshold is reached, which was estimated to be 3.49. However, Iran never achieved a growth rate below this threshold during the study period, implying that economic growth contributed to an increase in carbon emissions.

Fourth, the results revealed logically that energy consumption is a key factor determinant of environmental degradation in these countries. Whereas, it is clear the biggest effect of ENE on CO2 emissions is in the Saudi Arabia case confirming the results of Raggad (2020) and, Agboola et al. (2021) results, where the increase in ENE by 1% increases CO2 emissions by 1.87% and 0.84% in the long and short run respectively. Hence, Saudi Arabia is one of the top three exporter countries in the world with its huge company ARAMCO. Because the Kingdom’s consumption of energy for oil extraction has increased significantly in recent years, and the use of renewable energies remains very low in comparison to widely accessible and cheaper fuels, energy consumption in Saudi Arabia is regarded as one of the major contributors to rising carbon emissions and environmental deterioration. The same result is held in all other countries, this means that these countries rely heavily on cheap and non-renewable energy sources to boost their economic growth, which exacerbates environmental degradation.

Finally, it is clear that population growth in Algeria, Saudi Arabia, and Turkey contributes significantly to environmental descent as Mahmood et al. (2020) exposed in Algeria and Saudi Arabia respectively, where a 1% increase in population leads to a 4.76% increase in carbon emissions (2.11% in Algeria and 0.84% in Turkey). This result can be explained by stating that population growth puts additional pressure on energy demand and consumption in the long run, resulting in an increase in carbon emissions.

Conclusion and policy implications

In recent years, the concept of economic uncertainty has gained popularity among researchers and policymakers, particularly in the aftermath of the 2008 financial crisis, which resulted in a state of doubt and mistrust in the global economy, as well as the dire consequences for the global economy for several years. For this reason, this paper explored the effect of economic policy uncertainty (measured by the World Uncertainty Index (WUI) proposed by Ahir et al. (2022) on environmental quality (measured by carbon dioxide emissions (CO2) in selected MENA countries (Algeria, Saudi Arabia, Egypt, Morocco, Turkey, and Iran based on data availability) over the period from 1970 to 2020. In juxtaposing, the paper used modern ARDL procedure to deal with any kind of possible effects. First, we used the augmented ARDL (AARDL) model presented by McNown et al. (2018) to avoid the dependent variable integer in order 0 issues. Second, we applied the NARDL model presented by Shin et al. (2014) to deal with the effect of positive and negative changes of WUI on carbon emissions. Third, we used the MTNARDL model proposed by Pal and Mitra (2015) in order to examine the effect of extremely small and large changes in WUI on CO2 emissions. The outcomes revealed that uncertainty affects carbon emissions only in Morocco, Turkey, and Iran with an asymmetric effect from both small and large changes in the long-run term. Conversely, the results showed no evidence of any effect of WUI on environmental pollution in Algeria, Saudi Arabia, and Egypt. Besides, the results showed that population and energy consumption are the key determinant factors of CO2 emissions in these countries. Furthermore, the inversed U shape of EKC is achieved in Algeria, Saudi Arabia, Morocco, and Turkey while the U shape is achieved in Iran and Egypt.

Based on these findings, we can therefore offer some policy recommendations for these governments. It is first necessary to invest in R&D to advance new technologies that use environmentally friendly production methods and products in Algeria and Saudi Arabia in order to decouple economic growth from carbon emissions, as well as to reduce production methods that depend on oil and hydrocarbon sources.

Since the third and fourth thresholds have the greatest effects in Morocco and Turkey, it is crucial to deal with changes in uncertainty. This is because these two countries’ institutions have adopted conventional, unsustainable technologies that heavily rely on hydrocarbons in an effort to cut production costs and prevent shocks brought on by uncertainty. In order to prevent unexpected developments, the governments of these two countries must handle the high levels of uncertainty with caution by providing aid and subsidies to institutions. They must also adopt preventative measures to deal with significant shifts in uncertainty, including clear and transparent laws and policies, special tax exemptions to lower production costs, facilitation of international trade, the provision of raw materials at reasonable prices, partnerships with foreign firms to supply modern technologies, and increased investment in renewable energy innovation.

The MTNARDL results in Iran showed that medium modifications are far more significant in raising CO2 emissions than are high increases. Due to the low levels of uncertainty, the Iranian government should take precautions to prevent its institutions and businesses from using production techniques that worsen the environment. To do this, it should impose additional taxes and fees on the production process, especially for the very affordable oil products that are Iran’s trademark. This calls for a review of the prices of the petroleum materials used in the production process. These findings may encourage such countries to adopt renewable energy to lessen the effects of population increase and climate change, both of which are highly prevalent in the MENA countries. In order to reduce the number of ineffective activities that contribute to environmental degradation, such as deforestation and conventional agricultural and industrial practices, these countries must impose lower taxes and provide assistance for the use of these energies by making them available at affordable prices for individual consumption, and increase national awareness of the economic and social costs of pollution.

Although the importance and sensitivity of uncertainty subject, it has not yet received enough attention to enable the identification of opportunities that can be used to improve environmental conditions and lower greenhouse gas emissions. Therefore, it is crucial to do research on how many categories of uncertainty (commercial, financial, monetary, health care, geopolitical risks, and taxation) affect carbon emissions and identify the primary causes of environmental deterioration in order to regulate carbon emissions in the future. In order to have reliable findings on the specific impacts of each sector of the economy and identify which sectors should be prioritized for the reduction of carbon emissions and other greenhouse gases, it is also necessary to study the impact of uncertainty of all kinds on various sectors of the economy (residential, transportation, commercial, industrial, and power generation).

Data availability

Available upon request.

References

Abbasi KR, Adedoyin FF (2021) Do energy use and economic policy uncertainty affect CO2 emissions in China? Empirical evidence from the dynamic ARDL simulation approach. Environ Sci Pollut Res 28:23323–23335. https://doi.org/10.1007/s11356-020-12217-6

Adams S, Adedoyin F, Olaniran E, Bekun FV (2020) Energy consumption, economic policy uncertainty and carbon emissions; causality evidence from resource rich economies. Econ Anal Pol 68:179–190. https://doi.org/10.1016/j.eap.2020.09.012

Adedoyin FF, Zakari A (2020) Energy consumption, economic expansion, and CO2 emission in the UK: the role of economic policy uncertainty. Sci Total Environ 738. https://doi.org/10.1016/j.scitotenv.2020.140014

Agboola MO, Bekun F, Joshua U (2021) Pathway to environmental sustainability: nexus between economic growth, energy consumption, CO2 emission, oil rent and total natural resources rent in Saudi Arabia. Resour Policy 74:102380. https://doi.org/10.1016/j.resourpol.2021.102380

Ahir H, Bloom N, Furceri D (2022) The world uncertainty index (No. w29763). National Bureau of Economic Research. https://www.nber.org/system/files/working_papers/w29763/w29763.pdf. https://www.policyuncertainty.com/. Accessed 26 Jan 2022

Ahmad US, Usman M, Hussain S, Jahanger A, Abrar M (2022) Determinants of renewable energy sources in Pakistan: an overview. Environ Sci Pollut Res 29:29183–29201. https://doi.org/10.1007/s11356-022-18502-w

Akalpler E, Hove S (2019) Carbon emissions, energy use, real GDP per capita and trade matrix in the Indian economy-an ARDL approach. Energy 168:1081–1093. https://doi.org/10.1016/j.energy.2018.12.012

Aldy JE, Viscusi K (2014) Environmental risk and uncertainty. In: Machina M, Viscusi K (Eds.) Handbook of the economics of risk and uncertainty, vol. 1. North-Holland, pp 601–649

Al-Ghussain L (2019) Global warming: review on driving forces and mitigation. Environ Prog Sustain Energy 38(1):13–21

Alshehry AS, Belloumi M (2017) Study of the environmental Kuznets curve for transport carbon dioxide emissions in Saudi Arabia. Renew Sustain Energy Rev 75:1339–1347. https://doi.org/10.1016/j.rser.2016.11.122

Al-Thaqeb SA, Algharabali BG (2019) Economic policy uncertainty: a literature review. J Econ Asymmetries 20:e00133. https://doi.org/10.1016/j.jeca.2019.e00133

Amin A, Dogan E (2021) The role of economic policy uncertainty in the energy-environment nexus for China: evidence from the novel dynamic simulations method. J Environ Manag 292https://doi.org/10.1016/j.jenvman.2021.112865

Amri F (2017) Carbon dioxide emissions, output, and energy consumption categories in Algeria. Environ Sci Pollut Res 24(17):14567–14578. https://doi.org/10.1007/s11356-017-8984-7

Anser MK, Apergis N, Syed QR (2021a) Impact of economic policy uncertainty on CO2 emissions: evidence from top ten carbon emitter countries. Environ Sci Pollut Res 28:29369–29378. https://doi.org/10.1007/s11356-021-12782-4

Anser MK, Syed QR, Lean HH, Alola AA, Ahmad M (2021b) Do economic policy uncertainty and geopolitical risk lead to environmental degradation? Evidence from emerging economies. Sustainability 13(11):5866. https://doi.org/10.3390/su13115866

Atsu F, Adams S (2021) Energy consumption, finance, and climate change: does policy uncertainty matter? Econ Anal Policy 70:490–501. https://doi.org/10.1016/j.eap.2021.03.013

Apergis N, Ozturk I (2015) Testing environmental Kuznets curve hypothesis in Asian countries. Ecol Ind 52:16–22. https://doi.org/10.1016/j.ecolind.2014.11.026

Arrow KJ, Fisher AC (1974) Environmental preservation, uncertainty, and irreversibility. Q J Econ 88(2):312–319. https://doi.org/10.2307/1883074

Asghari M (2012) Environmental Kuznets curve and growth source in Iran. Panoeconomicus 59(5):609–623. https://doi.org/10.2298/PAN1205609A

Balsalobre-Lorente D, Ibáñez-Luzón L, Usman M, Shahbaz M (2022) The environmental Kuznets curve, based on the economic complexity, and the pollution haven hypothesis in PIIGS countries. Renewable Energy 185:1441–1455. https://doi.org/10.1016/j.renene.2021.10.059

Bhowmik R, Syed QR, Apergis N, Alola AA, Gai Z (2022) Applying a dynamic ARDL approach to the Environmental Phillips Curve (EPC) hypothesis amid monetary, fiscal, and trade policy uncertainty in the USA. Environ Sci Pollut Res 29(10):14914–14928. https://doi.org/10.1007/s11356-021-16716-y

Bölük G, Mert M (2015) The renewable energy, growth and environmental Kuznets curve in Turkey: an ARDL approach. Renew Sustain Energy Rev 52:587–595. https://doi.org/10.1016/j.rser.2015.07.138

Bouyghrissi S, Murshed M, Jindal A, Berjaoui A, Mahmood H, Khanniba M (2022) The importance of facilitating renewable energy transition for abating CO2 emissions in Morocco. Environ Sci Pollut Res 29(14):20752–20767. https://doi.org/10.1007/s11356-021-17179-x

Bouznit M, Pablo-Romero MDP (2016) CO2 emission and economic growth in Algeria. Energy Policy 96:93–104. https://doi.org/10.1016/j.enpol.2016.05.036

Chen Q, Taylor D (2020) Economic development and pollution emissions in Singapore: evidence in support of the Environmental Kuznets Curve hypothesis and its implications for regional sustainability. J Cleaner Prod 243:118637. https://doi.org/10.1016/j.jclepro.2019.118637

Chica-Olmo J, Se S-H, Moya-Fernández P (2020) Spatial relationship between economic growth and renewable energy consumption in 26 European countries. Energy Econ 92:104962. https://doi.org/10.1016/j.eneco.2020.104962

Cramer W, Guiot J, Fader M et al (2018) Climate change and interconnected risks to sustainable development in the Mediterranean. Nat Clim Chang 8(11):972–980. https://doi.org/10.1038/s41558-018-0299-2

Danish, Ulucak R, Khan S (2020) Relationship between energy intensity and CO2 emissions: does economic policy matter? Sustain Dev 28(5):1457–1464. https://doi.org/10.1002/sd.2098

Destek MA, Sarkodie SA (2019) Investigation of environmental Kuznets curve for ecological footprint: the role of energy and financial development. Sci Total Environ 650:2483–2489. https://doi.org/10.1016/j.scitotenv.2018.10.017

Dietz T, Rosa EA (1994) Rethinking the environmental impacts of population, affluence and technology. Hum Ecol Rev 1(2):277–300

Dogan E, Ozturk I (2017) The influence of renewable and non-renewable energy consumption and real income on CO2 emissions in the USA: evidence from structural break tests. Environ Sci Pollut Res 24(11):10846–10854. https://doi.org/10.1007/s11356-017-8786-y

Ellsberg D (1961) Risk, ambiguity, and the savage axioms. Qu J Econ 75:643–669

Friedlingstein P, Houghton RA, Marland G, Hackler J, Boden TA, Conway TJ, Canadell JG, Raupach MR, Ciais P, Le Quere C (2010) Update on CO2 emissions. Nat Geosci 3(12):811–812. https://doi.org/10.1038/ngeo1022

Granger CW, Yoon G (2002) Hidden cointegration. University of California, Economics Working Paper, (2002–02). https://doi.org/10.2139/ssrn.313831

Grossman GM, Krueger AB (1991) Environmental impacts of a North American Free Trade Agreement. National Bureau of Economic Research Working Paper 3914, NBER. https://doi.org/10.3386/w3914

Henry C (1974) Investment decisions under uncertainty: the irreversibility effect. Am Econ Rev 64(6):1006–1012

Huang Y, Haseeb M, Usman M, Ozturk I (2022) Dynamic association between ICT, renewable energy, economic complexity and ecological footprint: is there any difference between E-7 (developing) and G-7 (developed) countries? Technol Soc 68:101853. https://doi.org/10.1016/j.techsoc.2021.101853

Hussain Y, Abbass K, Usman M, Rehan M, Asif M (2022) Exploring the mediating role of environmental strategy, green innovations, and transformational leadership: the impact of corporate social responsibility on environmental performance. Environ Sci Pollut Res, 1-17. https://doi.org/10.1007/s11356-022-20922-7

Intisar RA, Yaseen MR, Kousar R, Usman M, Makhdum MSA (2020) Impact of trade openness and human capital on economic growth: a comparative investigation of Asian countries. Sustainability 12(7):2930. https://doi.org/10.3390/su12072930

Jahanger A, Usman M, Ahmad P (2021a) A step towards sustainable path: the effect of globalization on China’s carbon productivity from panel threshold approach. Environ Sci Pollut Res 29(6):8353–8368. https://doi.org/10.1007/s11356-021-16317-9

Jahanger A, Usman M, Balsalobre‐Lorente D (2022a) Linking institutional quality to environmental sustainability. Sustain Dev. https://doi.org/10.1002/sd.2345

Jahanger A, Usman M, Murshed M, Mahmood H, Balsalobre-Lorente D (2022b) The linkages between natural resources, human capital, globalization, economic growth, financial development, and ecological footprint: the moderating role of technological innovations. Resour Policy 76:102569. https://doi.org/10.1016/j.resourpol.2022.102569

Jahanger A, Usman M, Balsalobre-Lorente D (2021b) Autocracy, democracy, globalization, and environmental pollution in developing world: fresh evidence from STIRPAT model. J Public Aff e2753. https://doi.org/10.1002/pa.2753

Jalil A, Mahmud SF (2009) Environment Kuznets curve for CO2 emissions: a cointegration analysis for China. Energy Policy 37(12):5167–5172. https://doi.org/10.1016/j.enpol.2009.07.044

Jiang Y, Zhou Z, Liu C (2019) Does economic policy uncertainty matter for carbon emission? Evidence from US sector level data. Environ Sci Pollut Res 26(24):24380–24394. https://doi.org/10.1007/s11356-019-05627-8

Jordan S, Philips AQ (2018) Cointegration testing and dynamic simulations of autoregressive distributed lag models. Stata J 18:902–923. https://doi.org/10.1177/1536867X1801800409

Kamal M, Usman M, Jahanger A, Balsalobre-Lorente D (2021) Revisiting the role of fiscal policy, financial development, and foreign direct investment in reducing environmental pollution during globalization mode: evidence from linear and nonlinear panel data approaches. Energies 14(21):6968. https://doi.org/10.3390/en14216968

Ke J, Jahanger A, Yang B, Usman M, Ren F (2022) Digitalization, financial development, trade, and carbon emissions; implication of pollution haven hypothesis during globalization mode. Front Environ Sci 211. https://doi.org/10.3389/fenvs.2022.873880

Keynes JM (1921) A treatise on probability. Macmillan and Co, London

Keynes JM (1936) The general theory of employment, interest, and money. Harcourt, Brace, New York

Khalid K, Usman M, Mehdi MA (2021) The determinants of environmental quality in the SAARC region: a spatial heterogeneous panel data approach. Environ Sci Pollut Res 28(6):6422–6436. https://doi.org/10.1007/s11356-020-10896-9

Khan S, Murshed M, Ozturk I, Khudoykulov K (2022) The roles of energy efficiency improvement, renewable electricity production, and financial inclusion in stimulating environmental sustainability in the Next Eleven countries. Renewable Energy 193:1164–1176. https://doi.org/10.1016/j.renene.2022.05.065

Kharbach M, Chfadi T (2017) CO2 emissions in Moroccan road transport sector: Divisia, Cointegration, and EKC analyses. Sustain Cities Soc 35:396–401. https://doi.org/10.1016/j.scs.2017.08.016

Kuznets S (1955) Economic growth and income inequality. Am Econ Rev 45:1–28

Laurent E, Le Cacheux J (2012) Économie de l’Environnement et Économie Écologique, Paris, Armand Colin, p 214

Lieb CM (2003) The Environmental Kuznets Curve: a survey of the empirical evidence and of possible causes. Discussion Paper Series No. 391. University of Heidelberg, Department of Economics, Heidelberg

Liu J, Murshed M, Chen F, Shahbaz M, Kirikkaleli D, Khan Z (2021) An empirical analysis of the household consumption-induced carbon emissions in China. Sustain Prod Consum 26:943–957. https://doi.org/10.1016/j.spc.2021.01.006

Liu Y, Zhang Z (2021) How does economic policy uncertainty affect CO2 emissions? A regional analysis in China. Environ Sci Pollut Res 29(3):4276–4290. https://doi.org/10.1007/s11356-021-15936-6

Li Y, Guo J (2022) The asymmetric impacts of oil price and shocks on inflation in BRICS: a multiple threshold nonlinear ARDL model. Appl Econ 54(12):1377–1395. https://doi.org/10.1080/00036846.2021.1976386

Li S, Yu Y, Jahanger A, Usman M, Ning Y (2022) The impact of green investment, technological innovation, and globalization on CO2 emissions: evidence from MINT countries. Front Environ Sci 156. https://doi.org/10.3389/fenvs.2022.868704

Mahmood H, Alkhateeb TTY, Furqan M (2020) Industrialization, urbanization and CO2 emissions in Saudi Arabia: asymmetry analysis. Energy Rep 6:1553–1560. https://doi.org/10.1016/j.egyr.2020.06.004

Mäler KG, Fisher A (2005) Environment, uncertainty, and option values. Handb Environ Econ 2:571–620

McNown R, Sam CY, Goh SK (2018) Bootstrapping the autoregressive distributed lag test for cointegration. Appl Econ 50(13):1509–1521. https://doi.org/10.1080/00036846.2017.1366643

Moghadam HE, Dehbashi V (2018) The impact of financial development and trade on environmental quality in Iran. Empir Econ 54(4):1777–1799. https://doi.org/10.1007/s00181-017-1266-x

Murshed M (2021) LPG consumption and environmental Kuznets curve hypothesis in South Asia: a time-series ARDL analysis with multiple structural breaks. Environ Sci Pollut Res 28(7):8337–8372. https://doi.org/10.1007/s11356-020-10701-7

Murshed M, Alam R, Ansarin A (2021) The environmental Kuznets curve hypothesis for Bangladesh: the importance of natural gas, liquefied petroleum gas, and hydropower consumption. Environ Sci Pollut Res 28(14):17208–17227. https://doi.org/10.1007/s11356-020-11976-6

Murshed M, Saboori B, Madaleno M, Wang H, Doğan B (2022) Exploring the nexuses between nuclear energy, renewable energy, and carbon dioxide emissions: the role of economic complexity in the G7 countries. Renewable Energy 190:664–674. https://doi.org/10.1016/j.renene.2022.03.121

Narayan PK (2005) The saving and investment nexus for China: evidence from cointegration tests. Appl Econ 37(17):1979–1990. https://doi.org/10.1080/00036840500278103

Nemat S (1994) Economic development and environmental quality: an econometric analysis. Oxf Econ Pap 46:757–773

Ozokcu S, Özdemir Ö (2017) Economic growth, energy, and environmental Kuznets curve. Renew Sustain Energy Rev 72:639–647. https://doi.org/10.1016/j.rser.2017.01.059

Pal D, Mitra SK (2015) Asymmetric impact of crude price on oil product pricing in the United States: an application of multiple threshold nonlinear autoregressive distributed lag model. Econ Model 51:436–443. https://doi.org/10.1016/j.econmod.2015.08.026

Pata UK (2018) Renewable energy consumption, urbanization, financial development, income and CO2 emissions in Turkey: testing EKC hypothesis with structural breaks. J Clean Prod 187:770–779. https://doi.org/10.1016/j.jclepro.2018.03.236

Pesaran MH, Shin Y, Smith RJ (2001) Bounds testing approaches to the analysis of level relationships. J Appl Economet 16(3):289–326. https://doi.org/10.1002/jae.616

Pindyck RS (2007) Uncertainty in environmental economics. Rev Environ Econ Policy 1(1):45–65

Pirgaip B, Dinçergök B (2020) Economic policy uncertainty, energy consumption and carbon emissions in G7 countries: evidence from a panel Granger causality analysis. Environ Sci Pollut Res 27:30050–30066. https://doi.org/10.1007/s11356-020-08642-2

Qader MR, Khan S, Kamal M, Usman M, Haseeb M (2021) Forecasting carbon emissions due to electricity power generation in Bahrain. Environ Sci Pollut Res, 1-12. https://doi.org/10.1007/s11356-021-16960-2

Raggad B (2020) Economic development, energy consumption, financial development, and carbon dioxide emissions in Saudi Arabia: new evidence from a nonlinear and asymmetric analysis. Environ Sci Pollut Res 27(17):21872–21891. https://doi.org/10.1007/s11356-020-08390-3

Ramzan M, Iqbal HA, Usman M, Ozturk I (2022) Environmental pollution and agricultural productivity in Pakistan: new insights from ARDL and wavelet coherence approaches. Environ Sci Pollut Res 29:28749–28768. https://doi.org/10.1007/s11356-021-17850-3

Ramzan M, Raza SA, Usman M, Sharma GD, Iqbal HA (2021) Environmental cost of non-renewable energy and economic progress: Do ICT and financial development mitigate some burden? J Clean Prod 333:130066. https://doi.org/10.1016/j.jclepro.2021.130066

Sadiq M, Shinwari R, Usman M, Ozturk I, Maghyereh AI (2022) Linking nuclear energy, human development and carbon emission in BRICS region: Do external debt and financial globalization protect the environment? Nucl Eng Technol. https://doi.org/10.1016/j.net.2022.03.024

Sam CY, McNown R, Goh SK (2019) An augmented autoregressive distributed lag bounds test for cointegration. Econ Model 80:130–141. https://doi.org/10.1016/j.econmod.2018.11.001

Samargandi N (2017) Sector value addition, technology and CO2 emissions in Saudi Arabia. Renew Sustain Energy Rev 78:868–877. https://doi.org/10.1016/j.rser.2017.04.056

Sari-Hassoun S, Ayad H (2020) Renewable energy and sustainable development: evidence from 17 OECD countries. Int J Econ, Bus Politics 4(1):41–60

Sari-Hassoun S, Mékidiche M, Guellil MS (2019) Examining the connection amongst renewable energy, economic growth and carbon dioxide emissions in Algeria, Ekoist. J Econom Stat 14(29):199–223. https://doi.org/10.26650/ekoist.2018.14.29.0013

Savage L (1954) The foundations of statistics. J. Wiley, New York, second revised edition, 1972

Sharif A, Raza SA, Ozturk I, Afshan S (2019) The dynamic relationship of renewable and nonrenewable energy consumption with carbon emission: a global study with the application of heterogeneous panel estimations. Renewable Energy 133:685–691. https://doi.org/10.1016/j.renene.2018.10.052

Sharif A, Baris-Tuzemen O, Uzuner G, Ozturk I, Sinha A (2020a) Revisiting the role of renewable and non-renewable energy consumption on Turkey’s ecological footprint: evidence from Quantile ARDL approach. Sustain Cities Soc 57:102138. https://doi.org/10.1016/j.scs.2020.102138

Sharif A, Mishra S, Sinha A, Jiao Z, Shahbaz M, Afshan S (2020b) The renewable energy consumption-environmental degradation nexus in Top-10 polluted countries: fresh insights from quantile-on-quantile regression approach. Renewable Energy 150:670–690. https://doi.org/10.1016/j.renene.2019.12.149

Schmeidler D (1989) Subjective probability and expected utility without additivity. Econometrica 57(3):571–587. https://doi.org/10.2307/1911053

Sghaier A, Guizani A, Ben Jabeur S, Nurunnabi M (2019) Tourism development, energy consumption and environmental quality in Tunisia, Egypt and Morocco: a trivariate analysis. GeoJournal 84(3):593–609. https://doi.org/10.1007/s10708-018-9878-z

Shahbaz M, Khraief N, Uddin GS, Ozturk I (2014) Environmental Kuznets curve in an open economy: a bounds testing and causality analysis for Tunisia. Renew Sustain Energy Rev 34:325–336. https://doi.org/10.1016/j.rser.2014.03.022

Shin Y, Yu B, Greenwood-Nimmo M (2014) Modelling asymmetric cointegration and dynamic multipliers in a nonlinear ARDL framework. Festschrift in honor of Peter Schmidt. Springer, New York, pp 281–314. https://doi.org/10.1007/978-1-4899-8008-3_9

Solomon SD, Qin M, Manning Z, Chen M, Marquis KB, Avery M, Tignor HL, Miller (eds.) (2007) Climate Change 2007: the physical science basis. Contribution of Working Group I to the Fourth Assessment Report of the Intergovernmental Panel on Climate Change. Cambridge University Press, Cambridge, United Kingdom, and New York, NY, USA.

Stock JH, Watson MW (1988) Testing for common trends. J Am Stat Assoc 83(404):1097–1107

Syed QR, Bouri E (2021) Impact of economic policy uncertainty on CO2 emissions in the US: Evidence from bootstrap ARDL approach. J Public Aff e2595. https://doi.org/10.1002/pa.2595

Syed QR, Bhowmik R, Adedoyin FF, Alola AA, Khalid N (2022) Do economic policy uncertainty and geopolitical risk surge CO2 emissions? New insights from panel quantile regression approach. Environ Sci Pollut Res 29(19):27845–27861. https://doi.org/10.1007/s11356-021-17707-9

Tiwari AK, Jana RK, Roubaud D (2019) The policy uncertainty and market volatility puzzle: Evidence from wavelet analysis. Finance Res Lett 31. https://doi.org/10.1016/j.frl.2018.11.016

Touitou M, Langarita R (2021) Environmental Kuznets curve for carbon dioxide emissions and economic growth in Algeria. Margin: J Appl Econ Res 15(4):418–432. https://doi.org/10.1177/09738010211036261

Usman M, Balsalobre-Lorente D (2022) Environmental concern in the era of industrialization: can financial development, renewable energy and natural resources alleviate some load? Energy Policy 162:112780. https://doi.org/10.1016/j.enpol.2022.112780

Usman M, Hammar N (2021) Dynamic relationship between technological innovations, financial development, renewable energy, and ecological footprint: fresh insights based on the STIRPAT model for Asia Pacific Economic Cooperation countries. Environ Sci Pollut Res 28(12):15519–15536. https://doi.org/10.1007/s11356-020-11640-z

Usman M, Jahanger A (2021) Heterogeneous effects of remittances and institutional quality in reducing environmental deficit in the presence of EKC hypothesis: a global study with the application of panel quantile regression. Enviro Sci Pollut Res 28(28):37292–37310. https://doi.org/10.1007/s11356-021-13216-x

Usman M, Radulescu M (2022) Examining the role of nuclear and renewable energy in reducing carbon footprint: does the role of technological innovation really create some difference?. Sci Total Environ, 156662. https://doi.org/10.1016/j.scitotenv.2022.156662

Usman M, Makhdum MSA, Kousar R (2020) Does financial inclusion, renewable and non-renewable energy utilization accelerate ecological footprints and economic growth? Fresh evidence from 15 highest emitting countries. Sustain Cities Soc 65:102590. https://doi.org/10.1016/j.scs.2020.102590

Usman M, Jahanger A, Makhdum MSA, Balsalobre-Lorente D, Bashir A (2021) How do financial development, energy consumption, natural resources, and globalization affect Arctic countries’ economic growth and environmental quality? An advanced panel data simulation. Energy 122515. https://doi.org/10.1016/j.energy.2021.122515

Usman M, Balsalobre-Lorente D, Jahanger A, Ahmad P (2022) Pollution concern during globalization mode in financially resource-rich countries: do financial development, natural resources, and renewable energy consumption matter? Renewable Energy 183:90–102. https://doi.org/10.1016/j.renene.2021.10.067