Abstract

In September 2006, the Financial Accounting Standards Board issued Statement of Financial Accounting Standards No. 157, “Fair Value Measurements” (SFAS 157). Later in 2008, U. S. banks were mired in a credit crisis. Many economists and bankers suggested that one cause of the 2008 credit crisis was the requirements of SFAS 157 and a movement began to have its provisions amended or rescinded. The result of this movement was the passage of FSP FAS 157-4. The purposes of this study are to chronicle the events that lead to the release of FSP FAS 157-4, to report on the impact of FSP FAS 157-4 for the quarter ending March 31, 2009 for a sample of banks and to investigate the characteristics of the banks that early adopted FSP FAS 157-4 as compared to the non-adopters. The results did not find the predicted income increasing effect and indicated that total asset size and financial asset size were significant factors in the early adoption decision.

Similar content being viewed by others

Notes

Effective September 15, 2009, all FASB standards are now contained in what is termed the Accounting Standards Codification. The guidance provided originally in SFAS 157 is now contained in Section 820 of the FASB Accounting Standards Codification. For purpose of historical accuracy, we refer to this and subsequent guidance on fair value measurements by the original pronouncement numbers.

We used each company’s Tier 1 capital adequacy ratio to assess capital adequacy.

The Russell 3000 is a stock index that measures the performance of 3,000 publicly held US companies based on total market capitalization. This index represents approximately 98% of the investable US market; consequently, our sample consists of the 73 largest banks according to market capitalization.

Many of the banks in our sample did not disclose capital adequacy information in their 10-Q reports.

The four companies that reported material early adoption results were Capital Bancorp (CBC), Comerica. Inc. (CMA), Valley National Bank (VLY) and Wells Fargo (WFC).

A subsequent review of the June 30, 2009 10Qs for the companies that did not early adopt FAS FASB 157-4 revealed that none of the companies reported a material income effect.

Each of the four companies reporting a material impact from the adoption of FSP FAS 157-4 reported the impact of the adoption in the notes to the financial statements. Additionally, it is possible to determine the potential impact of category Levels 1 and 2 assets measured at fair value on net income and other comprehensive income by reviewing the types of assets held. Changes in the fair value of trading securities will be reported in net income. Changes in the fair value of available for sale securities will be reported in other comprehensive income. Changes in the fair value of fair value hedges are reported in net income while changes in the fair value of cash flow derivatives are reported in other comprehensive income and are later recycled into net income.

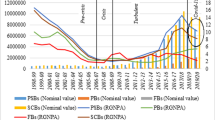

These percentages are distorted by the provisions of FIN No. 39 “Offsetting of Amounts Related to Certain Contracts—an interpretation of APB Opinion No. 10 and FASB Statement No. 105,” allows some derivative assets and liabilities with the same counterparty to be offset (netted). If the effects of netting are eliminated for the four largest banks in our sample, the percentage of financial assets to total assets rises from 21.5% to 55.78%.

The sum of the Level 1, 2 and 3 assets is not equal to the total financial assets for the reason discussed in footnote no. 5.

References

Barr, C. (2008). Accountants in the hotseat, special report issue #1: America’s Money Crisis. CNNMoney.com. (October, 28). http://money.cnn.com/2008/10/27/news/accounting.hotseat.fortune/?section=money_latest. Last accessed January 21, 2010.

Barth, M., Beaver, W., & Landsman, W. (1996). Value-relevance of banks’ fair value disclosures under SFAS No. 107, 71. The Accounting Review, 71(4), 513–537.

Beatty, A., Chamberlain, S. L., & Magliolo, J. (1995). Managing financial reports of commercial banks: the influence of taxes, regulatory capital, and earnings. Journal of Accounting Research, 33(2), 231–261.

Eccher, E., Ramesh, K., & Thiagarajan, R. (1996). Fair value disclosures by bank holding companies. Journal of Accounting and Economics, 22, 79–117.

Financial Accounting Standards Board. (1980). Statement of Financial Accounting Concepts No. No. 2, Qualitative characteristics of accounting information. Stamford: FASB.

Financial Accounting Standards Board. (1985). Statement of Financial Accounting Concepts No. No. 6: Elements of Financial Statements. Stamford: FASB.

Financial Accounting Standards Board. (2006). Statement of Financial Accounting Standards No. 157, Fair value measurements. Norwalk: FASB.

Financial Accounting Standards Board. (2008). FSP FAS 157-3, determining the fair value of a financial asset when the market for that asset is not active. Norwalk: FASB.

Financial Accounting Standards Board. (2009). FASB Staff Position on Statement of Financial Accounting Standards No. 157-4, determining fair value when the volume and level of activity for the assets or liability have significantly decreased and identifying transactions that are not orderly. Norwalk: FASB.

Friedmann, T. J., Zacharski, A. H., Bancroft, M. A., Mulvihill, R., Reading, S. A., Williams, R. J., & Rosenblat, A. (2008). SEC holds round-table on fair value accounting and auditing standards. Journal of Investment Compliance, 9(4), 13–17.

Goh, B. W., Ng, J., Yong, K. O. (2009). Market pricing of banks’ fair value assets reported under SFAS 157 during the 2008 economic crisis. Accessed at SSRN: http://papers.ssrn.com/sol3/papers.cfm?abstract-id=1335848.

Gordon, M., & Bernard, S. (2008). Banks want to suspend accounting rule in bailout. ABC News, Money, October 1. http://www.abcnews.go.com/Business/wireStory?id=5931917. Last accessed June 14, 2009.

Hughes, J., & Chung, J. (2009). IASB to consider changes to fair value rule. Financial Times. (March 18). http://www.ft.com/cms/s/0/ef960754-1353-11de-a170-0000779fd2ac.html?nclick_check=1. Last accessed September 15, 2010.

Katz, I., & Westbrook, J. (2009). Mark-to-market lobby buoys bank profits 20% as FASB may say yes. Financial Times. March 30. http://www.bloomberg.com/apps/news?pid=20601109&sid=awSxPMGzDW38&refer=home. Last accessed January 21, 2010.

Kim, M., & Kross, W. (1998). The impact of the 1989 change in bank capital standards on loan loss provisions and loan write-offs. Journal of Accounting and Economics, 25(1), 69–99.

Kolev, K. (2009). Do investors perceive marking-to-model as marking-to-myth? Early evidence from FAS 157 disclosure. Accessed at SSRN: http://ssrn.com/abstract=1336368.

Kudlow, L. (2009). The aig outrage: The government shouldn’t run anything, because it cannot run anything. National Review Online. (March 17). http://article.nationalreview.com/?q=YjA0ODRlOWIyMjU5ZjUxMTBkMTEwYjhkNjQ4OGYwNGU=. Last accessed September 15, 2010.

Laux, C., & Leuz, C. (2010). Did fair-value accounting contribute to the financial crisis? Journal of Economic Perspectives, 24(1), 93–118.

Moyer, S. E. (1990). Capital adequacy ratio regulations and accounting choices in commercial banks. Journal of Accounting and Economics, 13(2), 123–154.

Nelson, K. (1991). Fair value accounting for commercial banks: an empirical analysis of SFAS no. 107. The Accounting Review, 71(2), 161–182.

Petroni, K. (1992). Optimistic Reporting within the Property-Casualty Insurance Industry. Journal of Accounting and Economics, 3, 485–508.

Pulliam, S., & McGinty, T. (2009). Congress helped banks defang key rule. Wall Street Journal. (June 3). http://online.wsj.com/article/SB124396078596677535.html#mod=rss_whats_news_us. Last accessed September 15, 2010.

Reilly, D. (2009). Chanos condemns ‘monstrous idea’ that banks love: David Reilly. Bloomberg.com. http://www.bloomberg.com/apps/news?pid=newsarchive&sid=a6nHjl0fo0V4 (Last accessed January 21, 2010.

Securities and Exchange Commission. (2008). Report and Recommendations Pursuant to Section 133 of the Emergency Economic Stabilization Act of 2008: Study on Mark-To-Market Accounting, Washington, D. C. SEC.

Song, C. J., Thomas, W. B., Yi, H. (2009). Value relevance of FAS 157 fair value hierarchy information and the impact of corporate governance mechanisms. Accessed at SSRN: http://ssrn.com/abstract=1198142.

Willens, R. (2009). The fair value litany. Today in Finance: CFO.com April 13. http://community.dynamics.com/blogs/financeheadlines/archive/2009/04/13/the-fair-value-litany.aspx. Last accessed September 15, 2010.

Zeff, S. (2005). “The evolution of U.S. GAAP: the political forces behind professional standards (Part II),” CPA Journal Online, (February). http://www.nysscpa.org/cpajournal/2005/205/index.htm. Last accessed September 15, 2010.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Cathey, J.M., Schauer, D. & Schroeder, R.G. The Impact of FSP FAS 157-4 on Commercial Banks. Int Adv Econ Res 18, 15–27 (2012). https://doi.org/10.1007/s11294-011-9326-z

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11294-011-9326-z