Abstract

The goal of this paper is to outline the main factors influencing the diverse consequences of the global economic crisis on housing and mortgage markets in two post-socialist economies—the Czech Republic and Hungary. In the former there was a mild decline of markets while in the latter there has been a depression of markets. The paper also contributes to the convergence and divergence debate on housing policies in Europe. In the last two decades the post-socialist states have moved toward a market-based housing system (a convergence trend), but substantial differences have simultaneously emerged in tenure structure, housing finance institutions and housing policies (divergence trends). The Czech Republic and Hungary have introduced efficient market reforms in their economy but they have followed different paths in reforming their housing systems. This article shows that divergence in housing systems explains some of the differences in the impact of the global economic crisis on the housing and mortgage markets. However, the article concludes that housing policy responses to the impact of the global economic crisis on housing markets may on balance reinforce convergence trends.

Similar content being viewed by others

Notes

With high inflation lenders charge high nominal interest rates. This creates an affordability barrier with annuity mortgages where initial payments are high. However, as time passes loan repayments decline in real value through inflation resulting in repayments constituting a declining share of a borrower’s income. This effect is called a ‘tilt’ problem. Thus, the high real values of payments at the beginning of a loan term prevent many households from qualifying for mortgages.

The first subsidy was a generous interest subsidy for mortgage loans (called a subsidy to increase the demand for mortgage loans). It was equal to the yield from government bonds minus four percentage points (approximately 7.5% in 2000). The interest subsidy was provided for the full term of credit repayment. The second subsidy was an interest subsidy on mortgage bonds that was worth 3% in 2000. It could only be used when the interest on a mortgage loan financed from a subsidized bond did not exceed the interest rate on market bonds by more than 1.5 percentage points. If, for example, the market interest rate on mortgage bonds was 11%, the maximum interest rate that could be set on a mortgage loan was 12.5%. In such cases the bank could request a 3% interest subsidy, which effectively reduced the bank’s costs to 8%. This interest subsidy was increased in 2001 from 3 to 6%; and through a new mechanism it reached a record 10% in 2002. The third subsidy was a tax relief programme. The entire subsidy system was financially untenable in the long term and added substantially to state debt and the budget deficit. As expected, the Hungarian government cut such subsidies in December 2003. The interest subsidy on loans was reduced to 60% of the yield from government bonds, and the interest subsidy on mortgage bonds was reduced even more to 40% of the yield from government bonds. The maximum limit for tax deductions was cut in half, and a tax deduction was in most cases only allowed for the first 4 years of a mortgage. In 2007, all tax deductions on mortgages were abolished.

There are several factors behind these differences such as (1) the privatization policy in Hungary that started in 1986 and resulted in the introduction of right-to-buy legislation in 1993, and (2) strong public support for restitution of housing stock in the Czech Republic during the early phases of the post-communist transition process. Support for public rental housing construction in the Czech Republic after 1990 also has some relevance in this respect.

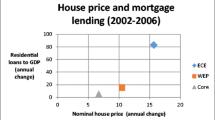

It is generally very difficult to make an international comparison of price-to-income ratios as statistical sources are often incomparable. Although great effort was made to harmonize the calculation methods used, the resulting figures must still be seen as estimates. In other words, there are non-trivial differences between selected countries both in the level and trend of housing affordability (price-to-income) during the period studied, but the real difference cannot be calculated precisely. While owner-occupied housing is generally more affordable in the Czech Republic and less affordable in Hungary, affordability remained steady in Hungary but has worsened in the Czech Republic over the last decade.

The most popular foreign currency was the Swiss franc (90–95% of the foreign currency loans were issued in SF). In 2005 and 2006 one SF was equal to 150–160 HUF (Hungarian forints). By 2009 this exchange rate had increased to 220 HUF. Thereafter, the exchange rate for Swiss francs varied between 180 and 220 HUF; however, it peaked once again at 220 HUF in August 2010.

References

Banai, Á., Király, J., & Nagy, M. (2010). Az aranykor vége Magyarországon (End of the golden age in Hungary). Közgazdasági Szemle, LVII, 2, 105–131.

CNB. (2009). Zpráva o finanční stabilitě (Report on financial stability). Prague: Czech National Bank.

Donner, C. (2006). Housing policies in central eastern Europe. Vienna.

Hegedüs, J. (2002). Housing finance in south-eastern Europe. Report prepared for the Council of Europe (internet publication).

Hegedüs, J. (2010). Towards a new housing system in transitional countries: The case of Hungary. In P. Arestis, P. Mooslechner, & K. Wagner (Eds.), Housing market challenges in Europe and the United States (pp. 178–202). Palgrave: Macmillan.

Hegedüs, J., & Struyk, R. (2005). Divergences and convergences in restructuring housing finance in transition countries. In J. Hegedüs & R. J. Struyk (Eds.), Housing finance: New and old models in central Europe, Russia and Kazakhstan (pp. 3–41). Budapest: LGI.

Hegedüs, J. & Tosics, I. (1996). Disintegration of East-European housing model. In D. Clapham, J. Hegedüs, K. Kintrea, & I. Tosics (eds.) Housing privatization in eastern Europe, (pp. 15–39). Greenwood.

Hodgson, G. (1998). The approach of institutional economics. Journal of Economic Literature, 36, 166–192.

Hodgson, G. (2006). What are institutions? Journal of Economic Issues, 40, 1–25.

Kemeny, J., & Lowe, S. (1998). Schools of comparative housing research: From convergence to divergence. Housing Studies, 13, 161–176.

Lowe, S., & Tsenkova, S. (Eds.). (2003). Housing change in east and central Europe. Integration or fragmentation? New York: Ashgate.

Lux, M. (Ed.). (2003). Housing policy—an end or a new beginning. Budapest: LGI.

Lux, M., & Sunega, P. (2010). The private rental housing in the Czech Republic: Growth and…? Sociologický časopis/Czech Sociological Review, 46, 349–373.

North, D. (1991). Institutions. Journal of Economic Perspectives, 5, 97–112.

Pichler-Milanovich, N. (2001). Urban housing markets in central and Eastern Europe: Convergence, divergence or policy collapse. European Journal of Housing Policy, 1, 145–187.

Struyk, R. (1996). Economic restructuring of the Soviet Bloc: The case of housing. Washington, DC: The Urban Institute.

Sunega, P., & Lux, M. (2007). Market-based housing finance efficiency in the Czech Republic. European Journal of Housing Policy, 7, 241–273.

Tarrow, S. (2010). The strategy of paired comparison: Toward a theory of practice. Comparative Political Studies, 42(2), 230–259.

UN/ECE. (2005). Housing finance systems for countries in transition: Principles and examples. Geneve: UN/ECE.

Acknowledgments

This article was prepared under the Research Project sponsored by the Grant Agency of the Czech Republic with grant number 403/09/1915.

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

Rights and permissions

About this article

Cite this article

Hegedüs, J., Lux, M. & Sunega, P. Decline and depression: the impact of the global economic crisis on housing markets in two post-socialist states. J Hous and the Built Environ 26, 315–333 (2011). https://doi.org/10.1007/s10901-011-9228-7

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10901-011-9228-7