Abstract

Australia is seen as being at the forefront of shifts to an explicit asset-based policy in its approach to maintaining post-retirement living standards, having initiated a move away from an unfunded retirement income system to a universal, funded system in the early 1990s. This move supplemented a considerable implicit asset-based policy based on home ownership. This paper examines the potential that asset-based welfare has to protect households from poverty after retirement by focusing on the role of home ownership in preventing poverty among older Australians and on likely future trends in asset accumulation. It suggests that, although asset-based welfare has the potential to ease the fiscal constraints faced by the state, it may well lead to poorer social insurance outcomes for households with limited saving capacity over their lifetime. Older households who miss out on home ownership are shown to be multiply disadvantaged: they have lower non-housing wealth, lower disposable incomes and higher housing costs in retirement than homeowners and they have significantly higher after-housing poverty rates. Projections suggest that this group will grow in size in the coming decades. These outcomes suggest that Australia’s asset-based welfare system is crumbling.

Similar content being viewed by others

Notes

This imagery owes its origins to Torgersen (1987) who saw housing as a wobbly pillar of the welfare state because of its capital intensive nature and its reliance on private provision. See, also Kemeny (2001) and Malpass (2008). The metaphor has been extended here to suggest that it has already begun to decline.

Like many Western economies, Australia has an ageing population. In 2006, people aged 65 years and over made up 13% of its population. By 2051 this proportion is projected to double. This puts Australia behind the trends in Western Europe and ahead of those in North America. Demographic data for Australia can be found in ABS (2006, 2007). Demographic data for Western Europe and North America can be found in the US Census Bureau's International Data Base, Table 094 (http://www.census.gov/ipc/www/idb/tables.html). Whiteford and Whitehouse (2006) provide an overview of the challenges that an ageing population brings to social protection systems and of the pension reforms that have been undertaken in OECD countries to address these challenges.

Details on the historical development of this retirement income system can be found in this 2001 Treasury paper on the history of the Australian retirement income system since Federation. Parts of this section rely heavily on the material in that paper.

Coverage is 72% for casual employees.

Details of the changes made in 2007 can be found in a Parliamentary Library Research Paper (Nielson 2007). Details of current taxation arrangements regarding superannuation arrangements can be found on the Tax Office website at http://www.ato.gov.au/super/default.asp. Similar concessions apply to superannuation contributions made by the self-employed.

For example, the Senate Select Committee (2002, para 2.3) quoted Treasury as reporting World Bank endorsement of Australia's general approach to the provision of retirement incomes. This report of endorsement was repeated in 2004 in the Treasurer's policy paper on retirement income (Australian Government 2004).

"Replacement rates are defined as ratios of a person’s income or spending power after retirement to that before retirement. The proposition underlying the replacement rate concept is that a person’s standard of living in retirement should be a reasonable proportion of his or her standard of living during working life" (Rothman, p. 3) Treasury prefer use of an expenditure rather than income definition to allow for the drawdown of capital during retirement.

Top-up arrangements ensure that no worker who has made compulsory superannuation contributions receives a retirement income that is less than he or she would have received had they received a full old-age pension.

As in most countries, neither capital gains on owner-occupied property nor imputed income are taxed (although the benefit of this latter subsidy is less than in some countries because mortgage interest costs, except for a short period, have not been deductible). Owner-occupied housing is also exempt from state-based land taxes that apply to all other property and first home buyers are generally exempt from state-based stamp duties associated with home purchase.

Castles acknowledges Jones (1990, p. 181) as the source of this argument.

DiPasquale and Wheaton (1994) provide a formal analysis of housing market dynamics and the future of housing prices that explicitly takes into account the fixity of land. In such a model the long run cost of supplying housing increases as demand increases. Tsatsaronis and Zhu (2004) point to the role of the availability and cost of land, the cost of construction and investments in improving the quality of the housing stock as key long run determinants. Meen (2002) provides estimates of house prices in the US and UK which explain differences in the rate of house price growth in each country by differences in their respective supply elasticities and, in particular, shows that supply restrictions add to pressures on dwelling prices. This is supported by evidence from Green et al. (2005) who show that estimates of supply elasticities vary substantially from place to place but are relatively inelastic in metropolitan areas (which means that house prices will rise with increased demand). Boehm and Schlottman (2004) show the importance of housing in life-time wealth accumulation. Their results, from US panel data, suggest that housing wealth makes up the whole of their total wealth for households with lower permanent incomes.

In their cross-country comparisons of income inequality, for example, the first two studies found distinct differences in inequality within and between countries depending on whether imputed rent was included or excluded from the definition of income. These differences arise primarily because of distinct differences in home ownership rates, particularly among the low-income elderly.

Dewilde and Raeymaeckers (2008) make the important point that access to social housing can ameliorate this effect.

Details on the Henderson poverty line and an overview of its strengths and weaknesses can be found in Saunders (1994, pp. 245–260).

Only households in receipt of social security payments are eligible for rent assistance. See the Appendix for more details.

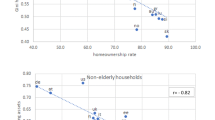

The weakness of relying on cross-section data, as in Figs. 2 and 3, to draw conclusions about changes over time is recognised but the key purpose of the data presented here is to compare outcomes for households in different tenures at every point in the life-cycle at a given point in time. Figure 4 below takes cohort effects into account.

This life-cycle pattern of net worth by age shows the same pattern as illustrated for median net worth holdings by age generated from the LWS data base for a select range of OECD countries (OECD 2008, Figure 10.1). Unfortunately, the comparative data in the OECD publication are not disaggregated by tenure but the fact that the contribution made to the total by the household's principal residence ownership is in excess of 50% in each of the countries covered suggests that the patterns of wealth holdings are likely to be similar to that illustrated here for Australia. Belsky (2008, p. 7) shows that even more extreme disparities in wealth holdings of owners and renters at different life-cycle stages than illustrated in Fig. 3 occur in the US. In 2008, real asset prices in Australia were still well above their 2003–04 levels despite downturns in some asset markets.

ABS Cat No 6554.0 Household Wealth and Wealth Distribution, Australia, 2003–04, Table 20.

Trend increases in real house prices have been in the order of 2–3% per annum although, as in most countries, Australia experienced a rapid increase in growth in real house prices in the early part of the twentyfirst century. More details of past trends and explanations of the drivers of past and more recent trends can be found in Yates et al. (2008).

The tenure projections were based on the assumption that long term (1971–2001) trends in house prices and household incomes would continue (from their pre-bubble 2001 level) and that the incremental increase in home ownership rates as households age would be the same in the future as it had been in the past. This is based on the conservative assumption that access to housing in the future is no worse than it was prior to 2001. More detail about these assumptions can be found in Yates et al. (2008). Since mid-2008, the Commonwealth government in Australia has increased the support to first home buyers as part of an economic stimulus package in response to the global financial crisis. This has been effective in bringing forward home purchase for many but it remains to be seen whether it will be retained for long enough to reverse the structural decline.

In June 2008, A$1 = €0.60. All figures have been rounded to the nearest $1,000.

To ensure people with the same amount of assets are treated fairly and to encourage people to earn more income from their assets, financial assets are assumed to earn a certain amount of income, regardless of what they actually earn. If the actual income received from investment exceeds the deemed income, the extra income is not counted when assessing pension rates. Deeming rates are continually monitored and tend to be below market rates. An even lower rate applies for the first $39,000 for singles and $65,000 for couples.

References

Australian Government. (2004). A more flexible and adaptable retirement income system. The Treasury: Canberra. http://demographics.treasury.gov.au/content/_download/flexible_retirement_income_system/flexible_retirement_income_system.pdf. Downloaded February 26th 2004.

Australian Bureau of Statistics (ABS). (1995). Australian social trends, 1995, ABS Cat. No. 4102.0. Canberra: ABS.

Australian Bureau of Statistics (ABS). (2001). Year Book Australia, 2001, ABS Cat. No. 1301.0. Canberra: ABS.

Australian Bureau of Statistics (ABS). (2006). Population projections, 2004 to 2101 Reissue, ABS Cat. No. 3222.0. http://www.abs.gov.au. Downloaded 30th May 2008.

Australian Bureau of Statistics (ABS). (2007). Basic community profile (Australia), ABS Cat. No. 2001.0. http://www.abs.gov.au. Downloaded 28th August 2007.

Bateman, H. (2006). Recent superannuation reforms: Choice and flexibility in retirement. Australian Accounting Review, 16(3), 2–6.

Belsky, E. (2008). Housing Wealth Effects and the Course of the US Economy: Theory, Evidence, and Policy Implications, Joint Center for Housing Studies Working Paper W08-7. http://www.jchs.harvard.edu/publications/finance/w08-7_belsky.pdf. Downloaded 9th December 2008.

Beverly, S., Sherraden, M., Zhan, M., Williams-Shanks, T., Nam, Y., & Cramer, R. (2008). Determinants of asset building. Urban Institute. http://www.urban.org/url.cfm?ID=411650. Downloaded 10th July 2008.

Boehm, T., & Schlottmann, A. (2004). Wealth accumulation and homeownership: Evidence for low-income households, U.S. Department of Housing and Urban Development. http://www.huduser.org/publications/HOMEOWN/WAccuNHomeOwn.html. Downloaded 10th July 2008.

Botsman, P., & Latham, M. (Eds.). (2001). The enabling state: People before bureaucracy. Annandale: Pluto Press.

Bradbury, B. (2008). ‘Housing wealth as retirement saving: Does the Australian model lead to over-consumption of housing?’ Luxembourg Wealth Study Working Paper No. 7. http://www.lisproject.org/publications/lwswpapers.htm. Downloaded 16th April 2009.

Bradbury, B., Rossiter, C., & Vipond, J. (1986). Poverty Before and After Housing, Reports and Proceedings No 56, Social Policy Research Centre, University of New South Wales.

Buhmann, B., Rainwater, L., Schmaus, G., & Smeeding, T. (1988). Equivalence scales, well-being, inequality and poverty: Sensitivity estimates across ten countries using the Luxembourg Income Study Database. Review of Income and Wealth, 34, 115–142.

Castles, F. (1997). The institutional design of the Australian Welfare State. International Social Security Review, 50(2), 25–41.

Castles, F. (1998). The really big trade-off: Home ownership and the welfare state in the New World and the Old. Acta Politica, 33(1), 5–19.

Churi, M., & Jappelli, T. (2006). Do the elderly reduce housing equity? An international comparison, Luxembourg Income Study Working Paper Series, Working Paper No. 436. http://www.lisproject.org/publications/liswps/436.pdf. Downloaded 7th July 2008.

Commission of Inquiry into Poverty (the Henderson Report). (1975). Poverty in Australia, first main report (Vol. 1). Canberra: Commonwealth of Australia.

DeWilde, C., & Raeymaeckers, P. (2008). The trade-off between home-ownership and pensions: Individual and institutional determinants of old-age poverty. Ageing and Society, 28, 805–830.

DiPasquale, D., & Wheaton, W. (1994). Housing market dynamics and the future of housing prices. Journal of Urban Economics, 35(1), 1–27.

Disney, R., & Whitehouse, E. (2002) The Economic Well-Being of Older People in International Perspective: A Critical Review, MPRA Paper No. 10398. http://mpra.ub.uni-muenchen.de/10398/1/MPRA_paper_10398.pdf. Downloaded 22nd April, 2009.

Frick, J., & Grabka, M. (2003). Imputed rent and income inequality: A decomposition analysis for Great Britain, West Germany and the U.S. Review of Income and Wealth, 49(4), 513–537.

Gilbert, N., & Gilbert, B. (1989). The enabling state: Modern welfare capitalism in America. New York: Oxford University Press.

Green, R., & Malpezzi, S. (2003). U.S. housing markets and housing policy, AREUEA monograph series no. 3. Washington D.C.: The Urban Institute Press.

Green, R., Malpezzi, S., & Mayo, S. (2005). Metropolitan-specific estimates of the price elasticity of supply of housing, and their sources. American Economic Review, 95(2), 334–339.

Harmer, J. (2008). Pension review background paper, Appendix C. Department of Families, Housing and Community Affairs. http://www.facs.gov.au/seniors/pension_review/pension_review_paper.pdf. Downloaded 31st October 2008.

Holzman, R., & Hinz, R. (2005). Old-age income support in the 21st century an international perspective on pension systems and reform. World Bank: Washington, D.C. http://siteresources.worldbank.org/INTPENSIONS/Resources/Old_Age_Income_Support_Complete.pdf.

Jones, M. (1990). The Australian welfare state, Third Edition. Sydney: Allen and Unwin, cited in Castles, F. (1998).

Kemeny, J. (1977). A political sociology of home ownership in Australia. Journal of Sociology, 13(1), 47–52.

Kemeny, J. (2001). Comparative housing and welfare: Theorising the relationship. Journal of Housing and the Built Environment, 16(1), 53–70.

Kemeny, J. (2005). “The Really Big Trade-Off” between home ownership and welfare: Castles’ evaluation of the 1980 thesis, and a reformulation 25 years on. Housing Theory and Society, 22(2), 59–75.

King, A. (1998). Income poverty since the early 1970s. In R. Fincher & J. Nieuwenhuysen (Eds.), Australian poverty: Then and now. Melbourne: Melbourne University Press.

Malpass, P. (2008). Housing and the New Welfare State: Wobbly Pillar or cornerstone? Housing Studies, 23(1), 1–19.

Meen, G. (2002). The time series behaviour of house prices. Journal of Housing Economics, 11(1), 1–23.

National Housing Supply Council. (2009). State of Supply Report, Canberra: Department of Families, Housing, Community Services and Indigenous Affairs. http://www.fahcsia.gov.au/sa/housing/pubs/housing/national_housing_supply/Documents/NHSC_StateofSupplyReport.pdf. Downloaded 22nd April 2009.

Nielson, L. (2006). An adequate superannuation-based retirement income? Parliamentary Library Research Brief, no. 12, 2005–06. http://www.aph.gov.au/library/pubs/rb/2005-06/06rb12.pdf. Downloaded 6th June 2008.

Nielson, L. (2007). An adequate superannuation-based retirement income? Parliamentary Library Research Paper, 1 August 2007, no. 2, 2007–08. http://www.aph.gov.au/library/pubs/rp/2007-08/08rp02.pdf. Downloaded 6th June 2008.

Organisation for Economic Cooperation and Development (OECD). (2008). Growing unequal? Income distribution and poverty in OECD countries. Directorate for Employment, Labour and Social Affairs, Paris: OECD. http://www.oecd.org/document/53/0,3343,en_2649_33933_41460917_1_1_1_1,00.html. Downloaded 23rd October 2008.

Ritakallio, V.-M. (2003). The importance of housing costs in cross-national comparisons of welfare (state) outcomes. International Social Security Review, 56(2), 81–101.

Rothman, G. (2007). The adequacy of Australian retirement incomes—new estimates incorporating the better super reforms. In Paper presented to the Fifteenth Colloquium of Superannuation Researchers, University of New South Wales, 19 & 20 July 2007, Conference Paper 07/1. http://rim.treasury.gov.au/content/pdf/CP07_1.pdf. Downloaded 1st May 2008.

Rothman, G., & Bingham, C. (2004). Retirement income adequacy revisited. In: Conference Paper 2004/1, Paper presented to the Twelfth Colloquium of Superannuation Researchers, University of New South Wales, 12 & 13 July 2004. http://rim.treasury.gov.au/content/pdf/CP04_1.pdf. Downloaded 1st May 2008.

Saunders, P. (1994). Welfare and inequality: National and international perspectives on the Australian welfare state. Cambridge: Cambridge University Press.

Saunders, P., Patulny, R., & Lee, A. (2004). Updating and Extending Indicative Budget Standards for Older Australians, prepared for the Association of Superannuation Funds Australia, SPRC Report 2/04. http://www.sprc.unsw.edu.au/reports/ASFA_Report.pdf. Downloaded 9th June 2008.

Senate Select Committee on Superannuation. (2002). Superannuation and standards of living in retirement, A report on the adequacy of the tax arrangements for superannuation and related policy. http://www.aph.gov.au/senate/committee/superannuation_ctte/completed_inquiries/2002-04/living_standards/report/report.pdf. Downloaded 30th May 2008.

Senate Standing Committee on Community Affairs. (2008). A decent quality of life, inquiry into the cost of living pressures on older Australians. http://www.aph.gov.au/senate/committee/clac_ctte/older_austs_living_costs/report/report.pdf. Downloaded 9th June 2008.

Sherraden, M. (2005). Assets and public policy. In M. Sherraden (Ed.), Inclusion in the American dream: Assets, poverty and public policy (pp. 3–19). Oxford: Oxford University Press.

Torgersen, U. (1987). Housing The Wobbly Pillar under the welfare state. In J. Kemeny, L. Lundqvist, & B. Turner (Eds.), Between state and market. Stockholm: Almqvist and Wicksell International.

Treasury. (2001). Towards higher retirement incomes for Australians: a history of the Australian retirement income system since Federation. Economic Roundup, Centenary Edition 2001. http://www.treasury.gov.au/documents/110/PDF/round4.pdf. Downloaded December 1st 2001.

Treasury. (2002). Submission to the inquiry into superannuation and standards of living in retirement, Senate Select Committee on Superannuation. http://www.aph.gov.au/Senate/committee/superannuation_ctte/completed_inquiries/2002-04/living_standards/submissions/sub078.doc. Downloaded 30th May 2008.

Tsatsaronis, K., & Zhu, H. (2004). What drives housing price dynamics: Cross-country evidence. BIS Quarterly Review, March 2004. www.bis.org/publ/qtrpdf/r_qt0403f.pdf. Downloaded 4th January 2005.

Whiteford, P., & Kennedy, S. (1995). Incomes and Living Standards of Older People: A Comparative Analysis, UK Department of Social Security, Research Report number. 34, London: HMSO.

Whiteford, P., & Whitehouse, E. (2006). Pension challenges and pension reforms in OECD countries. Oxford Review of Economic Policy, 22(1), 78–94.

World Bank. (1994). Averting the old age crisis: Policies to protect the old and promote growth. New York: Oxford University Press.

Yates, J., & Bradbury, B. (2009). “Home ownership as a (crumbling) fourth pillar of social insurance in Australia”, Luxembourg Wealth Study Working Paper No. 8. http://www.lisproject.org/publications/lwswpapers.htm. Downloaded 16th April 2009.

Yates, J., Kendig, H., Phillips, B., Milligan V., & Tanton, R. (2008). Sustaining fair shares: The Australian housing system and intergenerational sustainability, AHURI National Research Venture 3: Housing Affordability for Lower Income Australians, Research Paper 11. http://www.ahuri.edu.au/nrv/nrv3/NRV3_Assoc_docs.html. Downloaded 23rd February 2008.

Acknowledgments

We would like to thank the Australian Research Council for financial support and Peter Saunders, seminar participants at the University of New South Wales and two anonymous referees for comments on earlier versions of this paper.

Author information

Authors and Affiliations

Corresponding author

Appendix: The Australian age pension

Appendix: The Australian age pension

The pension rate for single persons is set at 25% of AWE. For couples, the per person rate is 83% of the single rate. In June 2008, the maximum pension was approximately A$14,000 per year for a single person and A$24,000 per year for a couple.Footnote 23

In addition to their pension, age pensioners in the private rental market are eligible for rent assistance which increases as rent increases above a specified amount to a maximum payment of around A$6,000 per year for a single person and A$8,000 per year for a couple (Harmer 2008). Subject to meeting the assets test, single persons retain eligibility for the full pension if their non-pension income is less than A$3,000 per year and retain eligibility for a part pension if non-pension income is less than A$40,000 per year. For couples, the combined income test is less than A$6,000 per year for full pension eligibility and less than A$66,000 for a part pension.Footnote 24

The assets test applies differentially to homeowners and to renters. Apart from their family home (on which there is no value limit), single persons retain eligibility for a full pension if their (non owner-occupied housing) assets are less than A$167,000 and for a part pension if their assets are less than A$535,000. For owner-occupier couples, these tests are set at A$237,000 for full pension eligibility and A$849,000 for part pension eligibility. The respective assets tests for non-homeowners are A$121,000 higher than those for homeowners, an additional allowance which is less than one-third of the Australia-wide average dwelling value.

Rights and permissions

About this article

Cite this article

Yates, J., Bradbury, B. Home ownership as a (crumbling) fourth pillar of social insurance in Australia. J Hous and the Built Environ 25, 193–211 (2010). https://doi.org/10.1007/s10901-010-9187-4

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10901-010-9187-4