Abstract

We construct a new database of extensive margin changes to multiple aspects of corporate tax bases for OECD countries between 1980 and 2004. We use our data to systematically document the tendency of countries to implement policies that both lower the corporate tax rate and broaden the corporate tax base. This correlation informs our interpretation of previous estimates of the relationship between corporate tax rates and corporate tax revenues, which typically do not include comprehensive measures of the corporate tax base definition. We then re-examine the relationship between corporate tax rates and corporate tax revenues. We find that accounting for unobserved heterogeneity attenuates the relationship between corporate tax rates and corporate tax revenues, and increases the implied revenue-maximizing tax rate. Controlling for our new tax base measures does not substantively impact the magnitude of this relationship.

Similar content being viewed by others

Notes

The countries are Australia, Austria, Belgium, Canada, the Czech Republic, Denmark, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Italy, Japan, South Korea, Luxembourg, Mexico, the Netherlands, New Zealand, Norway, Poland, Portugal, the Slovak Republic, Spain, Sweden, Switzerland, Turkey, the UK and the USA.

These publications were produced annually from 1965 through 2002 and then in 2004. We utilize publications beginning in 1980 to focus on the time period that have been used in previous cross-country analyses of the relationship between corporate tax rates and corporate tax revenues. The 750 figure is a strictly upper bound on the number of country-years available. These measures are all set to zero in years prior to the existence of countries, when applicable. Because there are no corporate tax rate or revenues data for these country-years, these observations are not included in our analysis of the relationship between corporate tax rate and tax base changes or in any of the regression analysis.

The contemporaneous GDP is used for these calculations.

A description of the PDV of allowances data can be found in Devereux et al. (2002). Updated versions of the data used in Devereux and Griffith (2003) are available at http://www.ifs.org.uk/publications/3210.

These data are available at http://unctadstat.unctad.org.

These data are available at http://data.worldbank.org/indicators.

Table 3 shows that in 419 country-years there was no base change, so \(750-419=331\). The number of country-years with base changes in only one direction is the sum of base changes counts in the first row and first column, less the number of instances with no base change. Only base narrowers occur in \(80+19+7+2=108\) instances, and only base broadeners occur in \(118+36+7=161\) instances.

This finding is consistent with the conclusion of Becker and Fuest (2011), where the present discounted value of depreciation allowances is the only measure of the tax base considered.

A test on the equality of means shows that within 3 years of a tax rate change, base-broadening measures are almost 13 % more likely than base-narrowing measures when the corporate tax rate falls, and 3 % more likely when the corporate tax rate rises. Both differences are statistically significant at the 10 % level. Thus, the tendency for policies with offsetting revenue effects is persistent over a longer period, as well.

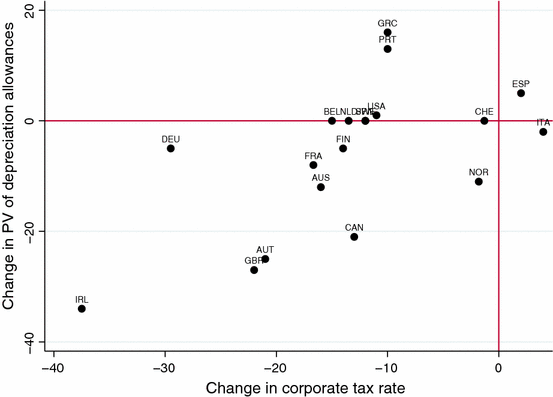

This figure provides complementary evidence to Fig. 1 in Becker and Fuest (2011), which plots year-to-year changes in corporate tax rates and the PDV of allowances for 19 OECD countries between 1982 and 2003 using the same source data. Becker and Fuest (2011) show that the majority of tax reforms in these country-years resulted in a decrease in the corporate tax rate, a decrease in depreciation allowances (i.e., a broadening of the corporate tax base), or both.

Fig. 2

Change in corporate tax rates and change in depreciation allowances, 1980–2008. The figure shows the net change in the corporate tax rate and the net change in the PDV of depreciation allowances between 1980 and 2008. This figure complements evidence presented in Fig. 1 of Becker and Fuest (2011), which provides similar evidence on a country-year level

In a similar spirit, Gruber and Rauh (2007) estimate the impact of the corporate tax rate on the level of corporate taxable income for publicly traded US firms. Using Compustat data, they implement an empirical design that is motivated by the elasticity of taxable income literature for individual income taxation, and find an elasticity of \(-\)0.2. In a similar vein, Devereux et al. (2014) estimate this elasticity for UK firms using administrative tax data; Patel et al. (2015) estimate this elasticity for US firms using administrative tax data.

An alternative is to investigate the determinants of the tax base, rather than tax revenue. The decisive problem with this approach is that the base is not known and can be approximated as R/\(\tau \), which imparts potentially serious division bias to the extent of measurement error in \(\tau \).

These analyses, as ours that follows, ignore the possibility that tax rate and tax base changes may affect GDP (indeed that is often their motivation), so that the estimated effects may not reflect solely the impact of the explanatory variables on tax revenues. Nor does this methodology allow us to parse out the effects that operate via the incidence of the tax changes, e.g., that corporate taxes may reduce wage income if they reduce the domestic capital stock.

For example, the estimates in Clausing (2007) imply a revenue-maximizing tax rate of 57 % for relatively large, closed countries, such as the USA

For example, Slemrod and Gillitzer (2014) provide a detailed exposition regarding the importance of the administration of the tax system and the extent of tax evasion in the discussion of optimal taxation.

Robinson and Slemrod (2012) investigate this issue in the context of individual income taxation.

Clausing (2007) proxies for the size of corporate profits with the GDP growth rate and the unemployment rate, and proxies for the share of the corporate sector with GDP per capita. In another specification, she includes corporate share of GDP, corporate profitability and the system for taxing worldwide income to account for the tax base. Devereux (2007) uses a more direct measure of the corporate tax base—the present discounted value of tax depreciable allowances per dollar of investment in plant and machinery.

Following the previous literature, we do not pursue the potential endogeneity of tax policy, nor attempt to distinguish business-cycle-exogenous policy changes, as in Romer and Romer (2014), for example.

For ease of reading, the corporate tax rate squared is divided by 100 in the regressions. In the baseline model that includes no other controls, we estimate that \(\hat{\beta }_{1}=0.23\) (\(\mathrm{se} = 0.04\)) and \(\hat{\beta }_{2}=-0.35\) (\(\mathrm{se}= 0.08\)), which gives an implied revenue-maximizing rate of 33.0 % (\(\mathrm{se}=2.22\)). There are 640 observations, and standard errors are clustered at the country level.

See Riedl and Rocha-Akis (2012) for recent empirical support for including other countries’ tax rates in such an equation. Our ability to identify income shifting across countries is limited because we include only the tax rates for the other countries included in this study, as is done in the previous literature. Thus, this measure does not capture incentives to shift to tax havens outside of our sample of countries. Desai et al. (2003) provide evidence on the behavioral responses of US firms’ foreign direct investment to international tax rates and Altshuler and Grubert (2004) provide evidence on responses in a larger set of countries. Both report a large tax elasticity of measured foreign investment. Desai et al. (2006a) develop a model where tax havens may increase business activity in non-haven countries, with empirical support in Desai et al. (2006b).

As in the previous specification, we provide the marginal effect of tax rates on tax revenues evaluated at the sample mean of the estimation sample and for the baseline case. The marginal effect is now much closer to zero, reflecting that the sample mean is quite close to the implied revenue-maximizing rate for small and less open countries.

The FE and FD estimators are both estimation strategies for removing country-specific fixed effects, either through first-differencing (FD) or through mean-differencing (FE). In the simple case when there are only two time periods, these estimators are equivalent. With more than two time periods, as in our case, these estimators differ in their assumptions over the idiosyncratic error term.

With respect to our clustered standard errors, serial correlation will matter for computing standard errors in the FD specification if differences in corporate tax revenues are serially correlated. For these specifications, clustered and non-clustered standard errors produce very similar results, and statistical inference is effectively unchanged.

We do not believe there is no insight at all to be gained from cross-country comparisons. There is no doubt, for example, that Ireland’s relatively low corporate tax rate is partly responsible for its large corporate tax revenues relative to its GDP. We leave for future research the appropriate way to learn from this with minimal bias in estimated causal relationships.

In regressions not shown, we find that when we restrict our attention to the specification in Gravelle and Hungerford (2007) (i.e., years prior to 2003 and using the variables included in their analysis), the relationship between corporate tax rates and tax revenues is no longer statistically significant. The point estimate of the revenue-maximizing corporate tax rate from these specifications is between 37 and 53 %.

Another potential reason for the difference in point estimates between the FE and FD specifications is that first-differencing amplifies the variation in highly variable data.

This test estimates the following regression, \(\Delta y_t = \Delta x_t\beta + w_t\gamma + \Delta u_t\), where \(w_t\) is a subset of the included covariates (excluding time dummies) and tests the hypothesis \(\gamma = 0\).

If we were able to construct a continuous measure of the breadth of the corporate tax base, summarized by a single variable, b, we could alternatively include it directly in our FE regression, along with its interactions with the corporate tax rate variables.

As in the previous specification, our new data provide a more thorough analysis of the impact of the corporate tax system on corporate tax revenues; however, these specifications beg the question of comparability within a category across countries and years.

The exception is that the unemployment rate is not statistically significant at the 10 % level.

The p value on the level of corporate tax rates in column (1) is 0.12.

References

Altshuler, R., & Grubert, H. (2004). Taxpayer responses to competitive tax policies and tax policy responses to competitive taxpayers: Recent evidence. Tax Notes International, 34, 1349–1362.

Becker, J., & Fuest, C. (2011). Optimal tax policy when firms are internationally mobile. International Tax and Public Finance, 18, 580–604.

Blouin, J., Huizinga, H., Laeven, L., & Nicodeme, G. (2014). Thin capitalization rules and multinational firm capital structure. CEPR discussion papers 9830.

Brill, A., & Hassett, K. (2007). Revenue-maximizing corporate income taxes: The Laffer curve in OECD countries. AEI working paper no. 137.

Clausing, K. (2007). Corporate tax revenues in OECD countries. International Tax and Public Finance, 14, 115–133.

Desai, M., Foley, C. F., & Hines, J., Jr. (2003). Chains of ownership, tax competition, and the location decision of multinational firms. In H. Herrmann & R. Lipsey (Eds.), Foreign direct investment in the real and financial sector of industrial countries (pp. 61–98). Berlin: Springer.

Desai, M., Foley, C. F., & Hines, J., Jr. (2006a). Do tax havens direct economic activity? Economic Letters, 90, 219–224.

Desai, M., Foley, C. F., & Hines, J., Jr. (2006b). The demand for tax haven operations. Journal of Public Economics, 90(3), 513–531.

Devereux, M. (2007) Developments in the taxation of corporate profit in the OECD since 1965: Rates, bases, and revenues. Working paper no. 07/04, Oxford University Centre of Business Taxation.

Devereux, M., & Griffith, R. (2003). Evaluating tax policy for location decisions. International Tax and Public Finance, 10, 107–126.

Devereux, M., Griffith, R., & Klemm, A. (2002). Corporate income tax reforms and international tax competition. Economic Policy, 35, 451–495.

Devereux, M., Liu, L., & Loretz, S. (2014). The elasticity of corporate taxable income: New evidence from UK tax records. American Economic Journal: Economic Policy, 6(2), 19–53.

Gordon, R., & Slemrod, J. (2002). Are ‘real’ responses to taxes simply income shifting between corporate and personal tax bases? In J. Slemrod (Ed.), Does Atlas shrug? The economic consequences of taxing the rich (pp. 240–280). New York City: Russell Sage Foundation.

Gravelle, J., & Hungerford, T. (2007). Corporate tax reform: Issues for congress. Congressional research service report RL34229.

Gruber, J., & Rauh, J. (2007). How elastic is the corporate income tax base? In A. Auerbach, J. Hines Jr., & J. Slemrod (Eds.), Taxing corporate income in the 21st century (pp. 140–163). Cambridge: Cambridge University Press.

International Bureau of Fiscal Documentation. (1980–2004). Annual report—International Bureau of Fiscal Documentation. International Bureau of Fiscal Documentation.

Lohse, T., Riedel, N., & Spengel, C. (2012). The increasing importance of transfer pricing regulations? A worldwide overview. Working paper 12/27, Oxford University Centre for Business Taxation.

Patel, E., Seegert, N., & Smith, M. (2015). At a loss: The real and reporting elasticity of corporate taxable income. Working paper.

Riedl, A., & Rocha-Akis, S. (2012). How elastic are national corporate income tax bases in OECD countries? The role of domestic and foreign tax rates. Canadian Journal of Economics, 45(2), 632–671.

Robinson, L., & Slemrod, J. (2012). Understanding multidimensional tax systems. International Tax and Public Finance, 19(2), 237–267.

Romer, C., & Romer, D. (2014). The incentive effects of marginal tax rates: Evidence from the interwar era. American Economic Journal: Economic Policy, 6(3), 242–281.

Slemrod, J., & Gillitzer, C. (2014). Tax systems. Cambridge: MIT Press.

Acknowledgments

We are grateful for comments from Kimberly Clausing, Michael Devereux, Martin Feldstein, James Hines Jr., participants at the NBER 2012 Trans-Atlantic Public Economics Seminar (TAPES) held at Oxford University and the 2012 Michigan Tax Invitational, as well as for comments from several anonymous referees. We thank Allison Paciorka, Jacqueline Schwartz and Jonathan Slemrod for their able research assistance and Richard Resen for providing us with the 2001–2002 and 2003–2004 International Bureau of Fiscal Documentation Annual Reports publications.

Author information

Authors and Affiliations

Corresponding author

Additional information

The views expressed in this paper are those of the authors and do not necessarily reflect the policy of the US Department of Treasury.

Appendices

Appendix 1: Data appendix

In this Data Appendix, we provide details of the methodology employed to translate summaries of tax policy changes into indicator variables for types of changes to the corporate income tax base. These indicator variables are derived from summaries of important tax policies published in the International Bureau of Fiscal Documentation’s Annual Report publications. For each of the variables, changes that broaden the corporate tax base are coded as \(+\)1, while changes that shrink the tax base are coded as \(-\)1.

1.1 Description of corporate tax base indicator variables

-

Research and development tax credit

- \(-\)1:

-

Research and/or development credit (or deduction) was made available or extended; additional deduction of research costs was permitted.

- \(+\)1:

-

Research and/or development credit (or deduction) was reduced.

-

Credits for foreign taxes paid

- \(-\)1:

-

Foreign tax credit was introduced or increased; the foreign tax credit became easier to obtain; ability to carry forward or back the foreign tax credit was made available or extended; losses could be used to offset foreign source income.

- \(+\)1:

-

The scope for the foreign tax credit was reduced or denied; limitation to the offset of foreign source losses (Germany 1982).

-

Tax treatment of foreign companies

- \(-\)1:

-

Tax exemptions, deductibility of costs, or other investment incentives aimed at attracting foreign investment or multinational headquarter placement; limited taxation or tax-exempt status of (some) nonresident companies; liberalization of inward foreign investment; reduced corporate taxes on companies with a foreign holding; holdings in foreign corporations granted new exemptions (Germany 1993); lower tax rates extended to EU companies where previously only applied to resident companies (Greece 2000); foreign company entry made easier (Korea 1994).

- \(+\)1:

-

Tax incentives to foreign investors or foreign companies were reduced or withdrawn; benefits to dual resident companies denied; certain tax rules extended to nonresident companies; definition of a resident corporation was expanded; taxes on income derived from subsidiaries in tax privileged countries were imposed; limited deduction of expenses of branch offices of nonresident companies; final withholding on nonresident corporations increased; deduction for expenses between resident and non-EC companies was disallowed (Italy 1991/2).

-

Policies that target evasion or avoidance by companies

- \(-\)1:

-

Increased efforts to combat evasion or avoidance, unless specifically directed at the individual level only, including provisions addressing international profit shifting, provisions to curtail the underground economy and a temporary tax amnesty to encourage the repatriation of capital illegally held abroad.

-

Investment credits or other tax incentives to promote investment

- \(-\)1:

-

Investment allowance/premium/deduction was introduced, increased or extended; exclusion of certain investments from taxation; tax holiday for investment projects or capital investments; incentives to promote investment; safe harbor leasing rules for investment credits.

- \(+\)1:

-

Investment premium or deduction was abolished, reduced or restricted; companies were no longer allowed to allocate profits to a tax-free investment reserve.

-

Accelerated depreciation or other depreciation allowances

- \(-\)1:

-

Increased depreciation rates; depreciation period shortened; accelerated write-off of capital expenditures; threshold for depreciation was increased; special depreciation allowances granted; free depreciation scheme introduced.

- \(+\)1:

-

Use of accelerated depreciation was reduced or abolished; depreciation rates were reduced; depreciation period was extended.

-

Other tax rates that may affect the corporate tax base

- \(-\)1:

-

Additional tax on business: Exceptional company profits or extraordinary business income (Hungary 1998; Portugal 1987); excess accumulated income (Korea 1994); municipal business tax on capital (Luxembourg 1998); assets tax (Mexico 1995); special temporary corporation tax (Japan 1994); branch profits tax (Australia, 1987); enterprise tax (Japan 1997); company formation tax (Hungary 1998). Capital taxes: Property transfer tax (Austria 1987); transfer of capital (Spain 1980); income from the increase in invested capital (Italy 1998). Development land tax (UK 1985). Specific business types: Shipping (Portugal 1991); foreign technology licensors (Korea 1988).

- \(+\)1:

-

Additional tax on corporations: Surtax on corporations or surcharge on corporate income tax (France 1995, 1997; Germany 1991; Turkey 1995); large corporation tax on capital (Canada 1989, 1990); flat tax on tax-reserves of companies (Greece 1998); special temporary corporation tax (Japan 1991); special corporate rate on exempt entities (Spain 1987); branch profits tax (US 1986). Specific business types: Large banks, investment funds or financial institutions (Austria 1981; Denmark 1989; France 1981; Korea 1982); life insurance companies (Australia 1988; Germany 1993; Sweden 1986); oil companies or oil windfall profits tax (France 1980, 1981, 2000; Norway 1980; US 1986); manufacturing profits tax on computer software and data processing firms (Ireland 1984); telecommunications (Turkey 1999). Capital taxes: Immovable property (Belgium 1994, Germany 1982; Spain 1991); movable capital (Portugal 1980, 1983). Surcharge on the employment fund (Luxembourg 1991, 1994).

-

Loss carry forward

- \(-\)1:

-

Loss carry forward was extended or expanded; limits for carry-forward loss amounts were removed.

- \(+\)1:

-

Ability to carry forward losses was suspended or restricted.

-

Loss carry back

- \(-\)1:

-

Loss carry back was introduced.

- \(+\)1:

-

Ability to carry-back losses was restricted.

-

Thin capitalization rules

- \(+\)1:

-

Thin capitalization rules were introduced or strengthened (widened); adjustments were made to thin capitalization rules (assumed to be positive); debt-to-equity ratio was reduced.

-

Controlled foreign company legislation

- \(-\)1:

-

CFC legislation was introduced or redefined.

-

Other changes to the corporate tax base

- \(-\)1:

-

Eased tax burden of companies generally (Netherlands, 1983); new deduction or exemption permitted: Losses from disposal of fixed assets (Czech Republic 1995); investment abroad (France 1988); payroll (France 1998); cost of issuing new shares (Germany 1984); new employees (Ireland 1982); bonuses to directors (Portugal 1999); undistributed profits that are wholly reinvested (Greece 1988); repatriated earnings (Ireland 1988); income from overseas services if not taxed in the source country (Australia 1980); corporate income tax incentives in the form of a credit (Hungary 2002); participation exemption under the corporate income tax was extended (Luxembourg 1988); level of income below which a proportion tax reduction is allowed was raised (Finland 1984).

- \(+\)1:

-

Measures to or emphasis on broadening the tax base, without mention of specific provisions (Hungary 1994; Japan 1998; Mexico 1987; US 1982; Turkey 1981); taxable base for lower rate was increased (Korea 1989); previous tax incentives restricted or abolished (Poland 1992); credits reformulated resulting in a sharp decrease in benefits (Spain 1988); certain provisions replaced, expected to keep total tax burden unchanged (Sweden 1989); loss of some deduction (Australia 1985; Netherlands 1989); allowances restricted (Hungary 1991); expenses were no longer recognized as business-related costs (Hungary 1993); inventory deduction abolished (Netherlands, 1986); extension of employment deduction for small and medium-sized businesses; reduction of certain tax expenditures (Belgium 1984); certain tax exemptions to promote growth of SME (Belgium 1998); deductions for corporate entertainment restricted (Japan 1994); investment deduction for employee profit sharing schemes eliminated (France 1985); maximum amount allowed to be credited to bad debt reserve was reduced (Japan 1982); full carry-over of tax benefits from international or contractual agreements (Portugal 1989); capital allowances phased out (UK 1984); corporate AMT extended (US 1986).

Appendix 2: Additional replication of previous work

In this Appendix, we conduct a replication exercise of Devereux (2007), as we did for Clausing (2007) in Sect. 4.3, using a similar baseline specification. We begin with the simple linear regression given by:

where \(R_{it}\) is the ratio of corporate tax revenues to GDP, \(\tau _{it}\) is the top statutory corporate tax rate, \(X{}_{it}\) are control variables, \(\mu _{t}\) are year fixed effects, and i denotes country and t denotes year. We use specifications that appear in columns (7) and (9) in Table 1 of Devereux (2007), which correspond to the most generous set of controls. The potential for income shifting is accounted for in two ways: specifications either include the GDP-weighted average of corporate tax rates in other OECD countries or include the top personal tax rate of the home country. Both sets of regressions include a measure of the corporate tax base, the present discounted value of tax depreciable allowances per dollar of investment in plant and machinery (PDV of allowances), interacted with all included tax variables.

Table 12 presents results from our replication exercise. Panel A presents results including the GDP-weighted average of other countries’ corporate tax rates in the regression as the “alternative” tax rate, and Panel B presents results including the top personal tax rate as the “alternative” tax rate. Standard errors are clustered at the country level. An important difference between these replications and the replications of Clausing (2007) is that these regressions now only include 20 OECD countries, as opposed to 30, due to the availability of data on the PDV of allowances.

Results from estimating these specifications via OLS appear in column (1) of Table 12. The results are qualitatively consistent with Devereux (2007). There is evidence of a nonlinear relationship between corporate tax rates and corporate tax revenues, which is highly statistically significant when controlling for the personal tax rate.Footnote 31 The estimated revenue-maximizing corporate tax rate evaluated at the mean of the PDV of allowances for the estimation sample (0.773) is 32 %. As found in the original study, the “alternative” tax rate variable plays a significant role in neither specification.

Next, we account for unobserved time-invariant heterogeneity by including country-specific fixed effects (FE) and by estimating equation in first-differences (FD). Results from the FE and FD specifications are presented in columns (2) and (3) of Table 12, respectively. In all of these specifications, the relationship between corporate tax rates and corporate tax revenues becomes attenuated, and none of the corporate tax rate variables are statistically significant at the 5 % level. Some of these specifications oddly imply a convex relationship between corporate tax rates and corporate tax revenues. The implied revenue-maximizing rates from these specifications cover a surprisingly large range, from \(-\)18 % to over 100 %. These results are consistent with the explanation put forth in both Clausing (2007) and Devereux (2007) for not controlling for time-invariant unobserved heterogeneity: that insufficient within-country variation remains to identify corporate tax rate effects.

Rights and permissions

About this article

Cite this article

Kawano, L., Slemrod, J. How do corporate tax bases change when corporate tax rates change? With implications for the tax rate elasticity of corporate tax revenues. Int Tax Public Finance 23, 401–433 (2016). https://doi.org/10.1007/s10797-015-9375-y

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10797-015-9375-y