Abstract

This paper provides empirical evidence of the existence of a long-run causal relationship between GDP and health care expenditures, for a group of Latin American and the Caribbean countries and for OECD countries for the period 1995–2014. We estimated the income elasticity of health expenditure to be equal to unity for both groups of countries, that is, health care in Latin American and OECD countries is a necessity rather than a luxury. We did not find evidence of a causal effect in the opposite direction, i.e. from changes in health expenditure to GDP. We present conclusive evidence of the cross-country dependence of the analyzed series, and consequently we used panel unit root tests, panel cointegration tests, and long-run estimates that are robust to such dependence. Specifically, we use the CIPS panel unit root test and the panel Common Correlated Effects estimator. We also show that the results obtained by mistakenly using methods that assume cross-section independence are unstable.

Similar content being viewed by others

Notes

Unweighted average computed using data from the Global Health Expenditure Database of the World Health Organization.

See Fig. 1 in the Appendix.

Assuming that health care costs and health status of the population are similar across countries.

The growth rate of GDP over the last 20 years was (slightly but still) higher among LA countries than among OECD members.

Sen (2005) finds a positive HE income elasticity with a panel of 15 OECD countries from 1990 to 1998, but using a different methodology. His results are obtained with Generalized Least Squares and Instrumental Variables estimators.

There are at least two other related papers that used panel cointegration techniques with methodological refinements, namely Liu et al. (2011) who showed the existence of structural breaks in the causal relationship between GDP and HE, and Mehrara et al. (2010) who estimated HE income elasticity below one using a panel smooth threshold regression.

The three papers used different methodologies. The main results in Baltagi and Moscone (2010) were based on a Common Correlated Effects estimator, Narayan et al. (2011) used Westerlund (2007) cointegration test and Dynamic OLS estimators, which are not consistent under cross-section dependence, and French (2012) used the Panel Analysis of Non-stationarity in Idiosyncratic and Common components (PANIC) approach of Bai and Ng (2004).

This paper uses unitroot tests that are consistent under the assumption of cross-country dependence, GMM estimators, and test for Granger Causality.

The Latin American and the Caribbean region includes 41 countries. We omitted countries from the sample for which we did not have the complete series of both variables for the time period of interest.

Table 14 in the Appendix presents estimated elasticities by country, obtained with the CCE estimator.

We report the results of the sensitivity analysis in Table 15 in the Appendix.

We conducted Pedroni’s test on the CCE residuals, with similar results.

We briefly describe the test in “Westerlund (2007) cointegration test” section in the Appendix.

Dependency rates and urban population are non-stationary in levels and also in first differences. In order to have a model in which all variables are stationary in first differences, we used the growth rate of these variables, as it is standard in the literature.

We reject the unitary income elasticity hypothesis for the panel of OECD countries when we use the specification without covariates and the recursive correction for small T.

Transformations on the life expectancy series like growth rates are also non-stationary in first differences.

References

Acemoglu, D., Finkelstein, A., & Notowidigdo, M. J. (2013). Income and health spending: Evidence from oil price shocks. The Review of Economics and Statistics, 95, 1079–1095.

Bai, J., & Ng, S. (2004). A PANIC attack on unit roots and cointegration. Econometrica, 72, 1127–1177.

Baltagi, B. (2008). Econometric analysis of panel data. New York: Wiley.

Baltagi, B. H., & Moscone, F. (2010). Health care expenditure and income in the OECD reconsidered: Evidence from panel data. Economic Modelling, 27, 804–811.

Blomqvist, A. G., & Carter, R. (1997). Is health care really a luxury? Journal of Health Economics, 16, 207–229.

Breitung, J. (2001). The local power of some unit root tests for panel data. In B. H. Baltagi, T. B. Fomby, & R. C. Hill (Eds.), Nonstationary panels, panel cointegration, and dynamic panels. Advances in econometrics (Vol. 15, pp. 161–177). Emerald Group Publishing Limited.

Breitung, J., & Das, S. (2005). Panel unit root tests under cross-sectional dependence. Statistica Neerlandica, 59, 414–433.

Chen, B., McCoskey, S. K., & Kao, C. (1999). Estimation and inference of a cointegrated regression in panel data: A Monte Carlo study. American Journal of Mathematical and Management Sciences, 19, 75–114.

Choi, I. (2001). Unit root tests for panel data. Journal of International Money and Finance, 20, 249–272.

Clemente, J., Marcuello, C., Montañés, A., & Pueyo, F. (2004). On the international stability of health care expenditure functions: Are government and private functions similar? Journal of Health Economics, 23, 589–613.

Ditzen, J. (2018). Estimating dynamic common-correlated effects in Stata. Stata Journal, 18, 585–617.

Dreger, C., & Reimers, H.-E. (2005). Health care expenditures in OECD countries: A panel unit root and cointegration analysis. International Journal of Applied Econometrics and Quantitative Studies, 2, 5–20.

Farag, M., NandaKumar, A., Wallack, S., Hodgkin, D., Gaumer, G., & Erbil, C. (2012). The income elasticity of health care spending in developing and developed countries. International Journal of Health Care Finance and Economics, 12, 145–162.

French, D. (2012). Causation between health and income: A need to panic. Empirical Economics, 42, 583–601.

Gerdtham, U.-G., & Löthgren, M. (2000). On stationarity and cointegration of international health expenditure and GDP. Journal of Health Economics, 19, 461–475.

Gerdtham, U.-G., & Löthgren, M. (2002). New panel results on cointegration of international health expenditure and GDP. Applied Economics, 34, 1679–1686. (cited By 17).

Hadri, K. (2000). Testing for stationarity in heterogeneous panel data. The Econometrics Journal, 3, 148–161.

Halıcı-Tülüce, N. S., Doğan, İ., & Dumrul, C. (2016). Is income relevant for health expenditure and economic growth nexus? International Journal of Health Economics and Management, 16, 23–49.

Hansen, P., & King, A. (1996). The determinants of health care expenditure: A cointegration approach. Journal of Health Economics, 15, 127–137.

Harris, R. D., & Tzavalis, E. (1999). Inference for unit roots in dynamic panels where the time dimension is fixed. Journal of Econometrics, 91, 201–226.

Im, K. S., Pesaran, M. H., & Shin, Y. (2003). Testing for unit roots in heterogeneous panels. Journal of Econometrics, 115, 53–74.

Kao, C., Chiang, M.-H., et al. (2000). On the estimation and inference of a cointegrated regression in panel data. Advances in Econometrics, 20, 179–222.

Ke, X., Saksena, P., & Holly, A. (2011). The determinants of health expenditure: A country-level panel data analysis. World Health Organization, working paper, December 2011.

Kouassi, E., Akinkugbe, O., Kutlo, N. O., & Brou, J. M. B. (2018). Health expenditure and growth dynamics in the SADC region: Evidence from non-stationary panel data with cross section dependence and unobserved heterogeneity. International Journal of Health Economics and Management, 18, 47–66.

Lago-Peñas, S., Cantarero-Prieto, D., & Blázquez-Fernández, C. (2013). On the relationship between GDP and health care expenditure: A new look. Economic Modelling, 32, 124–129.

Levin, A., Lin, C.-F., & Chu, C.-S. J. (2002). Unit root tests in panel data: Asymptotic and finite-sample properties. Journal of Econometrics, 108, 1–24.

Liu, D., Li, R., & Wang, Z. (2011). Testing for structural breaks in panel varying coefficient models: With an application to OECD health expenditure. Empirical Economics, 40, 95–118.

Mayer, D. (2001). The long-term impact of health on economic growth in Latin America. World Development, 29, 1025–1033.

McCoskey, S. K., & Selden, T. M. (1998). Health care expenditures and GDP: Panel data unit root test results. Journal of Health Economics, 17, 369–376.

Mehrara, M., Musai, M., & Amiri, H. (2010). The relationship between health expenditure and GDP in OECD countries using PSTR. European Journal of Economics, Finance and Administrative Sciences, 24, 1450–2275.

Narayan, P., Narayan, S., & Smyth, R. (2011). Is health care really a luxury in OECD countries? Evidence from alternative price deflators. Applied Economics, 43, 3631–3643. (cited By 0).

Pedroni, P. (1999). Critical values for cointegration tests in heterogeneous panels with multiple regressors. Oxford Bulletin of Economics and Statistics, 61, 653–670.

Pedroni, P. (2001). Purchasing power parity tests in cointegrated panels. Review of Economics and Statistics, 83, 727–731.

Pedroni, P. (2004). Panel cointegration: Asymptotic and finite sample properties of pooled time series tests with an application to the PPP hypothesis. Econometric Theory, 20, 597–625.

Persyn, D., & Westerlund, J. (2008). Error-correction-based cointegration tests for panel data. Stata Journal, 8, 232–241.

Pesaran, M. H. (2004). General diagnostic tests for cross section dependence in panels. Technical report, Institute for the Study of Labor (IZA).

Pesaran, M. H. (2006). Estimation and inference in large heterogeneous panels with a multifactor error structure. Econometrica, 74, 967–1012.

Pesaran, M. H. (2007). A simple panel unit root test in the presence of cross-section dependence. Journal of Applied Econometrics, 22, 265–312.

Roberts, J. (2000). Spurious regression problems in the determinants of health care expenditure: A comment on Hitiris (1997). Applied Economics Letters, 7, 279–283.

Sen, A. (2005). Is health care a luxury? New evidence from OECD data. International Journal of Health Care Finance and Economics, 5, 147–164.

Stock, J. H., & Watson, M. W. (1993). A simple estimator of cointegrating vectors in higher order integrated systems. Econometrica: Journal of the Econometric Society, 61, 783–820.

Westerlund, J. (2007). Testing for error correction in panel data. Oxford Bulletin of Economics and Statistics, 69, 709–748.

Acknowledgements

We wish to thank Felipe Martin for expert research assistance.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Funding

This work was supported by the Fondo Nacional de Desarrollo Científico y Tecnológico (Fondecyt, Chile) [Project No. 11130058 to M.Nieves Valdés]

Conflict of interest

The authors declare that they have no conflict of interest.

Appendix

Appendix

Health care expenditures as percentage of GDP in the world, and in selected groups of countries

Health care expenditures as percentage of GDP between 1995 and 2014. Notes “LA” is the group of 33 Latin American countries. “OECD” is the group of 35 Organisation for Economic Co-operation and Development member countries. “ALL” includes 192 countries for which HE data is available in the Global Health Observatory of the WHO

Source: Global Health Observatory Map Gallery, WHO

Health care expenditures as percentage of GDP in 2014

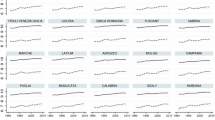

Trends in health care expenditures and GDP

Health care expenditures trends, LA countries. Notes Natural logarithm of health care expenditures per-capita, in constant dollars of 2010

Health care expenditures trends, OECD countries. Notes Natural logarithm of health care expenditures per-capita, in constant dollars of 2010

GDP trends, LA countries. Notes Natural logarithm of GDP per-capita, in constant dollars of 2010

GDP trends, OECD countries. Notes Natural logarithm of GDP per-capita, in constant dollars of 2010

Sensitivity to country exclusion: CIPS panel unit root test

Individual country CCE estimates

See Table 14.

Sensitivity to country exclusion: CCE estimates

See Table 15.

Westerlund (2007) cointegration test

The following description of the test was taken from the help file that accompanies the Stata command xtwest coded by Persyn and Westerlund (2008).

The panel cointegration tests developed by Westerlund (2007) contrast the absence of cointegration by determining whether there is error correction for individual panel members or for the panel as a whole. Consider the following error correction model, where all variables in levels are assumed to be I(1):

where \(a_i\) provides an estimate of the speed of error-correction towards long-run equilibrium \(y_{it} = - (b_i/a_i) * x_{it}\) for the series i.

The Ga and Gt test statistics contrast \(H_0: a_i = 0\) for all i against \(H1: a_i < 0\) for at least one i. These statistics start from a weighted average of the individually estimated \(a_i\)’s and their t-ratio’s respectively. Rejection of \(H_0\) should therefore be taken as evidence of cointegration of at least one of the cross-sectional units.

The Pa and Pt test statistics pool information over all the cross-sectional units to test \(H_0: a_i = 0\) for all i vs \(H_1: a_i < 0\) for all i. Rejection of \(H_0\) should therefore be taken as evidence of cointegration for the panel as a whole.

If the cross-sectional units are suspected to be correlated, robust critical values can be obtained through bootstrapping.

Controls

Rights and permissions

About this article

Cite this article

Rodríguez, A.F., Nieves Valdés, M. Health care expenditures and GDP in Latin American and OECD countries: a comparison using a panel cointegration approach. Int J Health Econ Manag. 19, 115–153 (2019). https://doi.org/10.1007/s10754-018-9250-3

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10754-018-9250-3

Keywords

- Income elasticity of health care expenditures

- Panel cointegration

- Cross-section dependence

- Latin American and the Caribbean and OECD countries