Abstract

This paper investigates the dynamic relationship between market efficiency, liquidity, and multifractality of Bitcoin. We find that before 2013 liquidity is low and the Hurst exponent is less than 0.5, indicating that the Bitcoin time series is anti-persistent. After 2013, as liquidity increased, the Hurst exponent rose to approximately 0.5, improving market efficiency. For several periods, however, the Hurst exponent was found to be significantly less than 0.5, making the time series anti-persistent during those periods. We also investigate the multifractal degree of the Bitcoin time series using the generalized Hurst exponent and find that the multifractal degree is related to market efficiency in a non-linear manner.

Similar content being viewed by others

Notes

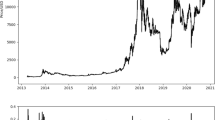

Since we find no trading data from January 4, 2015 to January 9, 2015 due to the hacking incident to Bitstamp, we patch the missing data with the data from Bitfinex at Bitcoincharts.

References

Al-Yahyaee, K. H., Mensi, W., & Yoon, S. M. (2018). Efficiency, multifractality, and the long-memory property of the bitcoin market: A comparative analysis with stock, currency, and gold markets. Finance Research Letters. (forthcoming).

Alvarez-Ramirez, J., Rodriguez, E., & Ibarra-Valdez, C. (2018). Long-range correlations and asymmetry in the Bitcoin market. Physica A, 492, 948–955.

Bariviera, A. F. (2017). The inefficiency of Bitcoin revisited: A dynamic approach. Economics Letters, 161, 1–4.

Baur, D. G., Dimpfl, T., & Kuck, K. (2018). Bitcoin, gold and the us dollar-a replication and extension. Finance Research Letters, 25, 103–110.

Bouoiyour, J., & Selmi, R. (2016). Bitcoin: A beginning of a new phase. Economics Bulletin, 36(3), 1430–1440.

Caporale, G. M., Gil-Alana, L., & Plastun, A. (2018). Persistence in the cryptocurrency market. Research in International Business and Finance, 46, 141–148.

Cheah, E. T., & Fry, J. (2015). Speculative bubbles in Bitcoin markets? An empirical investigation into the fundamental value of Bitcoin. Economics Letters, 130, 32–36.

Coinmarketcap. (2019). https://coinmarketcap.com/. Accessed Jan 2019.

Dyhrberg, A. H. (2016a). Bitcoin, gold and the dollar-A GARCH volatility analysis. Finance Research Letters, 16, 85–92.

Dyhrberg, A. H. (2016b). Hedging capabilities of Bitcoin. Is it the virtual gold? Finance Research Letters, 16, 139–144.

El Alaoui M, Bouri E, & Roubaud D (2018) Bitcoin price–volume: A multifractal cross-correlation approach. Finance Research Letters (forthcoming)

Jiang, Y., Nie, H., & Ruan, W. (2018). Time-varying long-term memory in Bitcoin market. Finance Research Letters, 25, 280–284.

Kantelhardt, J. W., Zschiegner, S. A., Koscielny-Bunde, E., Havlin, S., Bunde, A., & Stanley, H. E. (2002). Multifractal detrended fluctuation analysis of nonstationary time series. Physica A, 316(1), 87–114.

Katsiampa, P. (2017). Volatility estimation for Bitcoin: A comparison of GARCH models. Economics Letters, 158, 3–6.

Khuntia, S., & Pattanayak, J. (2018). Adaptive market hypothesis and evolving predictability of Bitcoin. Economics Letters, 167, 26–28.

Koutmos, D. (2018). Bitcoin returns and transaction activity. Economics Letters, 167, 81–85.

Kristoufek, L. (2018). On Bitcoin markets (in) efficiency and its evolution. Physica A, 503, 257–262.

Nakamoto S (2008) Bitcoin: A peer-to-peer electronic cash system. https://bitcoin.org/bitcoin.pdf

Phillip A, Chan J, & Peiris S (2018) On long memory effects in the volatility measure of cryptocurrencies. Finance Research Letters (forthcomimg)

Sensoy A (2018) The inefficiency of Bitcoin revisited: A high-frequency analysis with alternative currencies. Finance Research Letters (forthcomming)

Takaishi, T. (2018). Statistical properties and multifractality of Bitcoin. Physica A, 506, 507–519.

Takaishi, T., & Adachi, T. (2018). Taylor effect in Bitcoin time series. Economics Letters, 172, 5–7.

Tiwari, A. K., Jana, R., Das, D., & Roubaud, D. (2018). Informational efficiency of Bitcoin? An extension. Economics Letters, 163, 106–109.

Urquhart, A. (2016). The inefficiency of Bitcoin. Economics Letters, 148, 80–82.

Urquhart, A. (2017). Price clustering in Bitcoin. Economics Letters, 159, 145–148.

Wei, W. C. (2018). Liquidity and market efficiency in cryptocurrencies. Economics Letters, 168, 21–24.

Zargar, F. N., & Kumar, D. (2019). Informational inefficiency of Bitcoin: A study based on high-frequency data. Research in International Business and Finance, 47, 344–353.

Zunino, L., Tabak, B. M., Figliola, A., Pérez, D., Garavaglia, M., & Rosso, O. (2008). A multifractal approach for stock market inefficiency. Physica A, 387(26), 6558–6566.

Acknowledgements

The fund was provided by Japan Society for the Promotion of Science (Grand No: JP18K01556). Numerical calculations for this work were carried out at the Yukawa Institute Computer Facility and at the facilities of the Institute of Statistical Mathematics.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Takaishi, T., Adachi, T. Market Efficiency, Liquidity, and Multifractality of Bitcoin: A Dynamic Study. Asia-Pac Financ Markets 27, 145–154 (2020). https://doi.org/10.1007/s10690-019-09286-0

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10690-019-09286-0