Abstract

The bottom-up approach of the Nationally Determined Contributions (NDCs) in the Paris Agreement has led countries to self-determine their greenhouse gas (GHG) emission reduction targets. The planned ‘ratcheting-up’ process, which aims to ensure that the NDCs comply with the overall goal of limiting global average temperature increase to well below 2 °C or even 1.5 °C, will most likely include some evaluation of ‘fairness’ of these reduction targets. In the literature, fairness has been discussed around equity principles, for which many different effort-sharing approaches have been proposed. In this research, we analysed how country-level emission targets and carbon budgets can be derived based on such criteria. We apply novel methods directly based on the global carbon budget, and, for comparison, more commonly used methods using GHG mitigation pathways. For both, we studied the following approaches: equal cumulative per capita emissions, contraction and convergence, grandfathering, greenhouse development rights and ability to pay. As the results critically depend on parameter settings, we used the wide authorship from a range of countries included in this paper to determine default settings and sensitivity analyses. Results show that effort-sharing approaches that (i) calculate required reduction targets in carbon budgets (relative to baseline budgets) and/or (ii) take into account historical emissions when determining carbon budgets can lead to (large) negative remaining carbon budgets for developed countries. This is the case for the equal cumulative per capita approach and especially the greenhouse development rights approach. Furthermore, for developed countries, all effort-sharing approaches except grandfathering lead to more stringent budgets than cost-optimal budgets, indicating that cost-optimal approaches do not lead to outcomes that can be regarded as fair according to most effort-sharing approaches.

Similar content being viewed by others

1 Introduction

As part of the Paris Agreement, almost all countries agreed to focus international climate policy on reducing greenhouse gas (GHG) emissions in order to limit the increase of global mean temperature to well below 2 °C and to pursue efforts to limit it further to 1.5 °C above pre-industrial levels. At the same time, the agreement allows countries to formulate their own national targets in the form of Nationally Determined Contributions (NDCs). This means that the evaluation of the NDC targets is needed in order to ensure that their combined effort leads to the overall objective of the agreement. This evaluation is referred to as the stocktaking process. Several studies have already started to evaluate the combined NDCs with respect to their environmental effectiveness (van Soest et al. 2017; den Elzen et al. 2016; Rogelj et al. 2016a) or costs (Vandyck et al. 2016). The question whether the contribution of individual countries (or regions) is in line with the overall goal is, however, rather complex. In fact, discussions regarding the ‘fair’ contribution of countries have been ongoing since the United Nations Framework Convention on Climate Change (UNFCCC) Article 3 in 1992, specifying that the climate system should be protected ‘in accordance with their common but differentiated responsibilities and respective capability’ (UNFCCC 1992). An extensive literature has emerged using equity principles such as ‘responsibility’, ‘capability’, ‘equality’ and ‘sovereignty’ (Clarke et al. 2014; Höhne et al. 2014) as the basis for several effort-sharing approaches.

Usually, effort-sharing approaches are used to calculate emissions allowancesFootnote 1 or required emission reduction targets over time (BASICS experts 2011; Clarke et al. 2014; Höhne et al. 2014; Pan et al. 2014, 2017; Robiou du Pont et al. 2016; Tavoni et al. 2015; Wang et al. 2017; Holz et al. 2018). More recently, a different strand of effort-sharing literature has started to focus on carbon budgets (Raupach et al. 2014). At the global scale, the carbon budget approach is based on the strong linear relationship between long-term temperature change and cumulative CO2 emissions, because of the long lifetime of CO2 and the main contribution of CO2 to anthropogenic warming (Stocker et al. 2013). As a result, it is possible to derive global targets for cumulative CO2 emissions tolerable over a certain period. Given these global targets, “fair” country-level budgets can be derived based on effort-sharing approaches. Compared to annual GHG emission targets calculations, carbon budgets have the advantage that countries have more flexibility in deciding their own pathway given the allocated budget - should countries attempt to incorporate equity principles, but the disadvantage that they focus on CO2 emissions only.

This paper discusses a wide set of effort-sharing approaches. These are partly based on novel methods for allocating nationalFootnote 2 carbon budgets using effort-sharing approaches. At the same time, results of pathway-based effort-sharing calculations are discussed, i.e. GHG emission targets and implied carbon budgets (cumulative CO2 emissions of mitigation pathways). Both methods are based on the same global data to observe differences and similarities between the novel (carbon budgets) and more conventional (GHG emission pathways) methodologies (see Fig. 1). As a comparison with carbon budgets and GHG emission targets based on effort sharing, a set of recently developed scenarios that implement the different regional emission reduction pathways and carbon budgets based on a cost-efficient allocation was used (McCollum et al. 2018).

Methodology including effort-sharing approaches categorised using equity principles. The effort-sharing approaches are adapted from Höhne et al. (2014). The colours in box 3 represent different regions

This addresses the research question how national carbon budgets, in parallel to the more commonly used emission pathways, differ between a wide set of effort-sharing approaches and how these budgets compare to budgets based on the cost-optimal allocation. Due to the practical limitations of calculating time-dependent abatement costs within time-independent carbon budgets, including these costs is beyond the scope of this research.

The literature has shown that outcomes of effort-sharing approaches depend significantly on the parameter settings within each approach. We used the wide range of authors of this paper from different countries to discuss the parameter settings (using a systematic questionnaire). We explored the sensitivity to specific choices—selecting a default value and sensitivity ranges. In the calculations, we show the effects of different effort-sharing approaches on the allocation of emissions allowances consistent with keeping global mean temperature below 1.5 °C by 2100 with > 66% likelihood (in line with about 400 GtCO2 global carbon budget for the period 2011–2100) and 2 °C with > 66% likelihood (in line with about 1000 GtCO2 for 2011–2100) (Rogelj et al. 2016b; IPCC 2014)Footnote 3.

First, the methodology for calculating national carbon budgets and emission pathways based on effort-sharing approaches is explained, including the key parameters. Subsequently, the resulting parameter sets are presented, as well as the outcomes for national carbon budgets and GHG emission pathways. Carbon budgets refer specifically to CO2 emissions. For the pathways, however, we mainly present GHG results. Our results provide input for the discussions on ratcheting-up of mitigation efforts, part of the upcoming UNFCCC Global Stocktake. More specifically, our results can inform policymakers by comparing NDC targets and implied cumulative emissions until 2030 to emission reduction targets and carbon budgets corresponding to effort-sharing approaches based on equity principles (for which a section is dedicated under the NDCs, Winkler et al. 2017). As such, these results can inform discussions on how to distribute the additional mitigation effort to close the emissions gap.

2 Methods

2.1 Different effort-sharing approaches in this paper

There are different categorisations of effort-sharing approaches. In this research, we followed the categorisation using equity principles of Höhne et al. (2014) and adjusted it to include the grandfathering approach based on the sovereignty principle. In the paper, we selected six different approaches: ‘per capita convergence’ (PCC), ‘equal cumulative per capita emissions’ (ECPC), ‘ability to pay’ (AP), ‘greenhouse development rights’ (GDR) and ‘grandfathering’ (GF), as well as the cost-optimal (CO) allocation. These six approaches span the range of different approaches, as most of them relate directly to one of the equity principles introduced earlier (see Fig. 1 and Table 1).

2.2 Carbon budget and emission pathway calculations

Table 1 presents an overview of the calculations of carbon budgets and emission pathways for the different effort-sharing approaches explored here (see also Online Resource Table S.1 for equations). This analysis uses an effort-sharing framework incorporating a wide spectrum of effort-sharing or burden-sharing approaches available in the literature, as presented in Table 1, which all analyse the allocation of emissions allowances, reduction targets or carbon budgets for different countries. Traditionally, studies first define a global level of GHG emissions in a certain year or period, which is consistent with meeting a long-term climate objective (e.g. 400–450 ppm CO2e, as used in many recent studies), and then apply rules or criteria to allocate efforts to countries with the aim of meeting the global emissions level (Höhne et al. 2014). However, recent literature on mitigation scenarios has also focused on carbon budgets (Raupach et al. 2014). In this paper, we have adapted different approaches to directly derive national carbon budgets from the global carbon budget, and we index these approaches by an asterisk (e.g. AP*) to distinguish them from the traditional emission allowances-based approaches (indicated without an asterisk, e.g. AP).

We applied the effort-sharing approaches by first defining either (i) a global GHG emissions pathway or (ii) a global carbon budget, both consistent with limiting global warming to the 2 °C and 1.5 °C targets with a likely chance. The methods for (i) are the same as in the literature, but for (ii), we made some adjustments, in such a way that they have the same characteristics and underlying equity principles, but may differ in method of allocating the countries’ carbon budgets under the global carbon budget. For the methods directly determining the carbon budgets we did not make any assumptions regarding the emission pathways.

2.3 Data collection

The global carbon budgets and emission pathways were based on the CD-LINKS dataset (McCollum et al. 2018). Historical national GHG emissions until 2014 were collected from the PRIMAP emissions database (Gutschow et al. 2016), to which historical GHG emissions (excluding land use, land-use change and forestry (LULUCF) CO2) from the IMAGE model were harmonised. For LULUCF CO2 emissions, the IMAGE data was used. The Responsibility-Capacity Index (RCI) values necessary for the GDR* approach were based on Kemp-Benedict et al. (2017), which represents historical emissions responsibility, income (GDP per capita) and income distribution (Gini coefficient). The remaining data were used from the reference SSP2 scenario, as implemented in the IMAGE model (van Vuuren et al. 2017) that included no-policy baseline emissions projections (including LULUCF CO2), population and GDP (per capita). The IMAGE model was chosen for this purpose based on the relatively detailed regional disaggregation and representation of different emission sources.

2.4 Parameter settings

The outcomes of effort-sharing approaches critically depend on parameter choices and methods assumed to implement the approach. Several choices need to be made about parameter settings. Therefore, ranges based on literature and several assumptions were presented to the authors of this paper who come from different countries across the world and which are presented in the figures (see Table 2). A questionnaire was used (see Online Resource Table S.2) to determine the parameter sets used for further calculations, with the default settings representing the most chosen option (i.e. mode). A summary of the outcome of the questionnaire is presented in the Online Resource Table S.3.

Some general settings apply to all approaches. One important parameter is the starting year for the calculation of emissions allowances (i.e. whether the allocation has already started or a delay should be implemented). Consistent with the literature (Robiou du Pont et al. 2016; Pan et al. 2017; Höhne et al. 2014), we used 2010 as a starting point for the allocation of emissions allowances or reduction targets. The choice of coverage of GHG emissions also matters, as including all Kyoto GHG emissions including land use, land-use change and forestry (LULUCF) emissions or only energy (and industrial processes)-related CO2 emissions, could lead to significantly different outcomes. We used all GHG emissions for pathways and all CO2 emissions for carbon budgets as default and show energy and industry-related CO2 budgets as a sensitivity analysis in Online Resource chapter 4.

The grandfathering (GF)* approach is, in its pure form, a relatively straightforward approach, with limited variables and parameters. Previous studies have combined this approach with a participation threshold, to exclude lower-income countries from participating in bearing the burden (Pan et al. 2017). Reasons not to include a participation threshold could be transparency and the fact that many countries have committed themselves to the Paris Agreement. No participation threshold was implemented, as the majority of respondents opted for no participation threshold. Furthermore, not including a participation threshold increases comparability with the other approaches that also do not include a threshold.

The immediate equal per capita emissions (IEPC)* approach in its pure form is a relatively straightforward approach, with no additional parameter choice besides the general settings.

In the per capita convergence (PCC)* approach, a weighting factor is used for the carbon budgets to determine how far the approach should weigh towards GF* (current emissions) or IEPC* (population). We put the value right in the middle for the carbon budget approach, with 0.3 and 0.7 as sensitivity range. For the pathway approach, we used convergence years 2050 (default), 2075 and 2100.

The equal cumulative per capita emissions (ECPC)* approach takes into account historical emissions, discount factors and population shares. Firstly, concerning historical emissions, different start years can be chosen. 1850 as a start year could be argued for, as it represents the start of the industrial revolution. 1970 represents the beginning of the decade in which scientists increasingly published about global warming, and from 1990, it was clearly acknowledged that human activity was the cause of global warming, as described in the first IPCC Scientific Assessment Report (1990). 1850 was taken as a default based on the questionnaire results. Secondly, there are several reasons for discounting historical emissions. One of the most important ones is technological progress. As a result of innovation and technological R&D, energy efficiency increases over time, with the consequence that, for example, much more steel and cement per unit carbon can be produced now than in the past. This gives a latecomers’ advantage, which can be accounted for by discounting historical emissions by the rate of emission efficiency improvement (0.8–2.0% per year according to BASICS experts 2011; den Elzen et al. 2013). Another reason for discounting historical emissions could be that emissions from the past would have a relatively smaller impact as some of these have already decayed. Approximately 30% of CO2 is removed from the atmosphere after 150 years, implying 0.8% removal per year (van Vuuren et al. 2011). Therefore, the discount rate range of 1.6–2.8% per year was used, with a median estimate of 2% from literature (den Elzen et al. 2013; Robiou du Pont et al. 2016). Furthermore, the historical population shares are used to calculate the debt (or excess) emission allowances, and the future population shares are used to calculate the future emission allowances, which are summed to determine the net emission allowances.

For the ability to pay (AP)* approach, the average GDP per capita between 2011 and 2100 was used to determine relative reduction targets in the budget approach, and because this approach is not dynamic, no participation threshold was assumed. For the pathway approach, we included a participation threshold in the default case, which was set at such a per capita income level that from 2050 onwards; all countries participate (which, for our scenario, is USD 2,800 when using MER and USD 5,500 when using PPP). Furthermore, we used GDP based on purchasing power parity (PPP) as default. In our sensitivity runs, we included combinations of market exchange rates (MER)-based GDP levels and the case without the participation threshold to determine the total range.

The greenhouse development rights (GDR)* approach uses the Responsibility-Capacity Index (RCI), which has a potentially variable weighting between responsibility and capacity. Part of this index considers the historical emissions, so different start years can be chosen. Similar to the ECPC* approach, we used 1850, 1970 and 1990 as starting years, with 1850 as default. We also included the outcomes of sensitivity runs using RCI based fully on responsibility and fully on capability.

The cost-optimal (CO*) approach is based on results from the CD-LINKS database (McCollum et al. 2018). These scenarios assumed cost-optimal mitigation to start in 2020 (emission reductions are implemented where they are cheapest), meeting global carbon budgets of 1000 (2 °C) or 400 GtCO2 (1.5 °C) over the twenty-first century. For comparison, figures also show the No Policy (BAU*) scenario from the CD-LINKS database, which is based on SSP2, a middle-of-the-road scenario that assumes no new climate policies are implemented after 2010. Median, minimum and maximum values over all models reporting these scenarios are presented for CO* and BAU*.

3 Results

3.1 Allocated carbon budgets and required reduction efforts

This section presents the carbon budgets and GHG emission allowances over time, based on the different effort-sharing approaches, using the results of the questionnaire on the parameters (see also Online Resource Chapters 2 and 3). When comparing the results of the emission pathways and budgets, it should be noted that carbon budgets are independent of time and represent CO2 only, while GHG emission pathways are time-dependent and include all GHG emissions (including LULUCF). Therefore, this comparison is useful for determining similarities or differences in trends, but budgets and pathways should not be compared on their absolute numbers. As there was rare consensus on the parameter settings, the sensitivity ranges of these parameter choices are presented in addition to the default values.

3.2 Results for default settings

Figure 2 summarises the results of the carbon budget approach in terms of national carbon budgets (2011–2100) relative to each country’s 2010 CO2 emissions for all effort-sharing approaches, compared to the cost-optimal national ‘budgets’ (cumulative emissions resulting from cost-optimal scenarios). Online Resource Fig. S.1 and Fig. 3 illustrate the results for the emission pathways’ approach, both in terms of GHG emission allowances over time (Fig. S.1) and in terms of GHG emission reduction targets in 2030 relative to 2010 GHG emissions (Fig. 3).

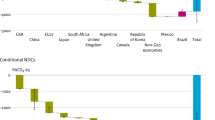

Carbon budgets of different effort-sharing approaches by country. Carbon budgets are given in emission years (2011–2100 CO2 budget/2010 emissions) and are based on a 1075 GtCO2 global carbon budget for the period 2011–2100. Default values shown by the filled bars and error bars illustrate the sensitivity ranges. Three combinations of parameter choices for GDR* are shown separately: sensitivity analysis on start year only (1970/1850/1990) with RCI at 0.5 (default), the start year 1850 with RCI at 0 and the start year 1850 with RCI at 1. USA United States of America, EU European Union, JPN Japan, RUS Russian Federation, CHN China, IND India, BRA Brazil. BAU ‘no policy’ scenario from CD-LINKS, based on SSP2, with no new climate policies assumed to be implemented after 2010; range based on different models, included for illustrative purposes only. Note that India’s BAU is out of the range, and therefore indicated by its values

GHG emission targets in 2030 relative to 2010 emissions. Including LULUCF, based on 2 °C global target. Default values shown by filled bars; error bars illustrate the sensitivity ranges. One combination of parameter choices for GDR is shown: sensitivity analysis on start year only (1970/1850/1990) with RCI at 0.5 (default), where the default is always shown as part of the sensitivity range, even though default has the most extreme parameter choice, i.e. 1850 vs. 1970–1990 in the sensitivity range. USA United States of America, EU European Union, JPN Japan, RUS Russian Federation, CHN China, IND India, BRA Brazil. NDC projections (green bars and dotted lines) are based on den Elzen et al. (2016) (www.pbl.nl/indc) (default) and http://climateactiontracker.org/. Note that the NDC projection for the USA refers to 2025, and for EU is excluding LULUCF. BAU (‘no policy’ scenario from the CD-LINKS dataset) included for illustrative purposes only

The most salient results are the extreme outcomes of the GDR* approach relative to all other approaches. The default values (i.e. 1850 as starting year and capability and responsibility given equal weight) lead to the largest budgets of all approaches for China and India and the smallest budgets for the USA, EU and Japan—both for the budgets and for the pathways. This is a result of a combination of relatively high historical emissions and high GDP per capita for the latter group of countries—resulting in high RCIs. The approach even leads to negative budgets for these countries. This is a consequence of the required reduction in the global budget being allocated to countries and deducted from their BAU budget—and the BAU emissions of the USA, EU, and Japan are projected to remain either constant or even decrease. In other words, it is a combination of relatively low BAU budgets (compared to history) and high RCI levels. For the pathways, emissions allowance allocations are negative by or soon after 2030. For China, the carbon budgets are smaller than for India, given the (much) higher GDP per capita levels and higher historical emissions. Combined, China and India are allocated more than 80% of the global budget in this approach. Note that for the pathways’ approach, GDR gradually moves to AP outcomes as RCI data was not available from 2031 onwards, which explains the change in trend for the GDR pathways in Fig. S.1.

The AP* approach—while sharing some characteristics with the GDR* approach—shows much smaller differences between countries. One reason is that responsibility is not taken into account. Another reason is that unlike the RCI approach, reductions are not a linear function of (responsibility and) capability, as we corrected for the shape of the marginal abatement cost curve in the AP* approach (for more details see Online Resource Table S.1). In practice, this means that a country with a GDP per capita income that is twice as high as the global average GDP per capita, the country’s relative reduction target is 26% larger (so if the average global reduction is 10%, the country needs to reduce 12.6%). This method leads to similar costs as the share of GDP, and so to smaller differences between countries. For China, the AP* approach leads to the smallest budget, as their GDP per capita is already above the world average and projected to still increase strongly while having a low RCI. In the emission pathways, this is visible through the AP approach resulting in a steady decrease in emission allowances to reach negative emission allowances in 2070, while GDR allows for an increase in emission allowances towards a peaking of about 40% above 2010 levels. Under a GF* approach, a relatively large budget is also allocated, due to China’s high current emissions. Even though China also has a large population share (IEPC*), they receive a larger budget based on current emissions. PCC* lies in between these values. The ECPC* has a comparable budget, and thus a larger budget compared to PCC* and GF*, due to China’s high population share and low historical emissions. As can be observed in the emission pathways, China’s emission allowances are projected to rise significantly more under the GF approach compared to the IEPC approach, for the same reasons.

The IEPC* approach gives outcomes similar to, but much less extreme than, the GDR* approach, with negative budgets for the USA and Russia and about zero budgets for the EU, Japan and Brazil (only with the default setting of including land use CO2 emissions). Together, India and China are allocated about half of the total global carbon budget in this approach, which is much less than the GDR* approach. As the IEPC approach implies immediate equal per capita emission allowances for the emission pathways, India is allocated more allowances than baseline emissions until about 2030. Nevertheless, the allocated budget is much smaller than their baseline cumulative emissions. For the USA, the EU, Japan and Russia, the opposite is the case: IEPC immediately leads to much lower allowances than current emission levels given their current high per capita emission levels.

As expected, the GF* approach leads to relatively large budgets for countries with relatively high current emissions per capita, such as the USA and Russia, and it leads to the smallest budget for India. Presented relative to 2010 emission levels, the carbon budgets and emission targets relative to 2010 emissions are the same across countries, as current emission levels determine the budgets (Figs. 2 and 3).

The PCC* approach is a combination of the IEPC* and GF* approaches, with results in the middle of these two approaches.

The ECPC* approach leads to the most extreme outcomes after GDR*: countries with relatively high historical per capita emissions (notably the USA and Russia) are allocated negative budgets, and Japan and the EU roughly zero budgets. Countries with low historical emissions per capita, notably India, are allocated relatively large budgets but still smaller than the GDR* approach.

To summarise, the GDR* approach—as implemented in our study—leads to the most extreme outcomes, with large budgets or emission allowances allocated to developing countries compared to all other approaches. The ECPC* approach leads to the same trend in outcomes, but less extreme. For most countries, the cost-optimal reductions are between the GF* and PCC* allocations. For the USA, EU and Japan, all approaches except GF* lead to more stringent budgets compared to cost-optimal allocation—suggesting that a uniform global carbon price only leads to an equitable outcome based on the principle of acquired rights. The differences between the approaches are very large for countries with very different GDP per capita or per capita emission levels compared to the world average (USA, EU, Japan, India), but are smaller for Brazil, China and Russia. For the USA, for instance, the allocated budget ranges from less than −300 GtCO2 to 160 GtCO2 (about 30 times their current CO2 emissions). For the EU, Japan and India, the differences between the approaches are even larger. It should be noted, however, that for the GDR* approach, we kept RCI values constant after 2030, as no projection was available beyond this year. As RCI values are likely to converge further after 2030, this leads to an overestimation of the budget allocations for developing countries and underestimation for developed countries. In the pathways’ calculations, we corrected for this by assuming a linear convergence towards the AP results. This still leads to GDR resulting in the most extreme results, but less extreme than under the budget approach (the implied carbon budget for the USA would be –150 GtCO2 under the pathways approach instead of −300 GtCO2 under the budget approach (Fig. 4). When only looking at 2030 targets, the results are slightly different. For developed countries, GDR still leads to the most extreme outcomes, but for India, IEPC leads by far to the largest emission allocation by 2030. Given India’s current low per capita emissions, in the short term, IEPC leads to larger allocations than projected baseline emissions, which is by definition not possible under the GDR approach.

Carbon budgets of different effort-sharing approaches per country. The carbon budgets (2011–2100) are given in 2010 emission years. First and third row: based on 1075 GtCO2 global carbon budget, second and fourth row based on 400 GtCO2 global carbon budget. Default values are shown as filled bars for direct carbon budgets, circles for indirect carbon budgets. Three combinations of parameter choices for GDR* are shown separately: sensitivity analysis on start year only (1970/1850/1990) with RCI at 0.5 (default), the start year 1850 with RCI at 0 and the start year 1850 with RCI at 1. For GDR*, the, default is always shown as part of the sensitivity range, even though default has the most extreme parameter choice, i.e. 1850 vs. 1970–1990 in the sensitivity range. USA United States of America, EU European Union, JPN Japan, RUS Russian Federation, CHN China, IND India, BRA Brazil

In this research, we also calculated the indirect carbon budgets by subtracting remaining cumulative non-CO2 GHGs (based on the cost-optimal reduction of the different GHGs) from the total cumulative GHG emissions resulting from the pathways’ approach (see Fig. 4). Differences between these indirect and direct carbon budgets can be explained by the variation in calculation methodologies between carbon budgets and emission pathways. Firstly, in the GF*, IEPC* and PCC* methodology for carbon budgets, instead of a convergence year as used in the emission pathway calculations, a weighting factor was chosen, as carbon budget allocations are independent of time. In addition, instead of reducing from current emissions, the global carbon budget was allocated based on a share irrespective of the country’s current emissions. Secondly, for the GDR* and AP* approach, instead of a BAU pathway as used in the pathways’ calculations, an average baseline over the whole period (2010–2100) was used to calculate the entitled national carbon budget. Thirdly, for all approaches in the carbon budget calculations, instead of a global pathway to 2 °C or 1.5 °C, the global carbon budget was used. Finally, for the GDR approach, we assumed a linear convergence towards the AP approach in the pathways’ calculations from 2030 onwards, leading to less extreme outcomes compared to the budget calculations.

3.3 Sensitivity analysis

The general sensitivities analysed include the global ambition level (apart from the default 1000 GtCO2 budget, we included runs with 400 GtCO2 budget) and including (default) or excluding land use CO2. The sensitivity values used and results are summarised in the Online Resource Table. S.3. and the Online Resource Fig. S.2. Obviously, a more stringent global target leads to more stringent budgets or pathways for all countries. However, the amount to which national budgets decrease depends on the approach. For instance, under the GDR* approach, the difference in carbon budgets between India and the USA is 820 GtCO2 (with India allocated the largest budget) under a global budget of 1000 GtCO2 and 925 GtCO2 under a global carbon budget of 400 GtCO2. As such, the GDR* approach leads to even more extreme outcomes under more stringent global budgets. However, for most of the other approaches, a more stringent budget leads to smaller absolute differences in budget allocations between countries.

The effect of including or excluding LULUCF CO2 emissions mainly has a significant effect on countries with relatively large LULUCF CO2 emissions, notably Brazil and India. Under the ECPC* approach, the budget of Brazil is much more stringent with, than without, land use CO2, as including their historical land use CO2 emissions significantly increase their historical per capita emission levels. For approaches that rely on projected BAU emissions, the results can be ambiguous, as excluding LULUCF CO2 emissions not only affects historical emissions (important for GDR*) but BAU emissions as well. For the GF* approach, this distinction has no effect by definition, because the only determinant to allocate budgets or emission allowances is population.

For all countries except India, the GDR* approach is the most sensitive to the different parametrisations applied here. We analysed two different sensitivities for GDR*, i.e. start year of the responsibility factor and the weighting towards either capability or responsibility. Of those two parameters, the weighting factor has the largest effect on the results, especially for those countries with relatively high or low emissions per capita compared to their GDP per capita. A weighting towards capability, for instance, leads to much smaller budgets for especially the EU and Japan, both of which have relatively low emissions per capita given their GDP per capita level. For Russia, the opposite is the case: a weighting towards responsibility leads to a much smaller budget given their relatively high emissions per capita and low GDP per capita. This is also the case for Brazil, where high LULUCF CO2 emissions also play an important role. The effect of the start year is especially important for the EU, the USA, Russia and China. For the first three countries, starting in 1850 leads to much smaller budgets than starting in 1990, while the opposite is the case for China. In numbers, the EU and the USA are allocated about 90–100 GtCO2 more and Russia 33 GtCO2 more if the starting year is 1990 instead of 1850, while China would be allocated 95 GtCO2 and India 35 GtCO2 less.

The parameterisation of the AP* and ECPC* approach is especially relevant for India. For AP*, the reason is that in terms of PPP, their income is much higher than in terms of MER. This results in a larger budget (by 40 GtCO2) if the ability to pay would be based on MER. For China, the budget would be 35 GtCO2 higher. Likewise, the USA (by 35 GtCO2), the EU (by 48 GtCO2) and Japan (by 15 GtCO2) would be allocated smaller budgets if GDP were to be based on MER. For ECPC*, the starting year is more important than the applied discount rate. Similar reasoning as for GDR* holds here, with an especially larger budget for India and China for a starting year in 1850 compared to 1990 (the difference being 60 GtCO2 for both countries).

4 Conclusions

This research compared different methods and parameterisations of allocating carbon budgets and reduction targets in emission pathways based on effort-sharing approaches for different equity principles. The resulting allocations were compared to cost-optimal approaches based on global optimisation model results (McCollum et al. 2018). We introduced novel methods to directly calculate national carbon budgets from effort-sharing approaches, and showed how for some methods, value judgments on parameter settings play an important role in the results.

Some approaches lead to extreme outcomes, which is a consequence of our staying as closely as possible to the equity principle underlying the effort-sharing approach. Although this represents a full range of outcomes, it means that some of the outcomes are clearly impossible to achieve by domestic emission reductions alone. Although mitigation in countries to achieve the reduction targets could be supported by a mixture of financing, emissions trading and other mechanisms (which could be explored in future research), the outcomes of the approaches should in any way not be regarded as top-down calculated targets and budgets for countries. Instead, they are meant to inform the discussions on ratcheting-up of mitigation efforts, also in view of the upcoming UNFCCC Global Stocktake, in particular with regard to the different notions of fairness, equity and efficiency of the distribution of effort across countries. This implies that in terms of practical implementation, deliberative discussions are needed between policymakers to share the effort of closing the emissions gap fairly.

Carbon budget and emission pathway calculations differ mostly as a function of the different effort-sharing approaches. Still, results were also very sensitive to the parameters chosen within a single approach. Most notably, AP and AP*, in which we considered the choice of GDP (MER or PPP) and the inclusion or exclusion of a participation threshold, showed a large range of outcomes, which was largely due to MER or PPP. Furthermore, the variation in historical start year (i.e. 1850, 1970 or 1990) created significant differences in equal cumulative per capita* (ECPC*) carbon budgets, in addition to the discount rate. Yet, the historical start year did not influence the outcomes of GDR* as significantly, most likely due to the relatively lower weighting towards historical emissions within the RCI compared to ECPC* that focuses on responsibility entirely. The results presented in this research illustrate the importance of parameter choices and calculation methodologies in order to represent effort-sharing approaches, which accurately depict the underlying equity principles.

Apart from grandfathering, all effort-sharing approaches considered here lead to smaller, and sometimes much smaller, carbon budgets for developed countries than the cost-optimal budget. This indicates that cost-optimal approaches do not lead to outcomes that can be regarded as fair according to most effort-sharing approaches.

In general, effort-sharing approaches that (i) calculate required reduction targets in carbon budgets (relative to baseline budgets) and/or (ii) take into account historical emissions when determining carbon budgets can lead to (large) negative remaining carbon budgets for developed countries. This is the case for the equal cumulative per capita approach and especially the greenhouse development rights approach, the latter showing much larger budgets for India, and smaller budgets for EU, Japan and the USA compared to optimal budgets. Both approaches allocate reduction targets below a (budget or pathway) BAU, and because the global reductions are much larger than the global allowances, these approaches can lead to larger differences. Furthermore, they can lead to the allocation of negative emissions allowances or budgets, something which approaches that allocate budgets or emission allowances by definition cannot.

Notes

Used here to refer to outcomes of effort sharing calculations, although these outcomes should not be seen as top-down calculated targets for countries.

Although the European Union is included in this analysis, we refer to countries and national carbon budgets for brevity.

Note that Millar et al. (2017) arrive at larger budgets, which can be explained by methodological differences including the 2015 temperature reference and using a threshold exceedance budget. A larger global carbon budget, however, would not affect our results in terms of differences between countries and approaches, only the absolute values would change.

References

Baer P, Athanasiou T et al (2008) The greenhouse development rights framework: the right to development in a climate constrained world, vol 1. Heinrich-Böll-Stiftung, Berlin.

BASICS experts (2011) Equitable access to sustainable development: Contribution to the body of scientific knowledge BASIC expert group: Beijing, Brasilia, Cape Town and Mumbai

Clarke L et al (2014) Assessing transformation pathways. In: Edenhofer O et al (eds) Climate Change 2014: Mitigation of Climate Change. Contribution of Working Group III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change. Cambridge University Press, Cambridge, UK

den Elzen M, Fuglestvedt J, Höhne N et al (2005) Analysing countries’ contribution to climate change: scientific and policy-related choices. Environ Sci 8:614–636

den Elzen MGJ, Olivier JGJ et al (2013) Countries’ contributions to climate change: effect of accounting for all greenhouse gases, recent trends, basic needs and technological progress. Clim Chang 121(2):397–412. https://doi.org/10.1007/s10584-013-0865-6

den Elzen M, Admiraal A et al (2016) Contribution of the G20 economies to the global impact of the Paris agreement climate proposals. Clim Chang 137(3-4):655–665. https://doi.org/10.1007/s10584-016-1700-7

Gutschow J, Jeffery L et al (2016) The PRIMAP-hist national historical emissions time series (1850-2014). Earth Syst. Sci. Data 8:571–603. https://doi.org/10.5194/essd-8-571-2016

Höhne N, den Elzen M, Escalante D (2014) Regional GHG reduction targets based on effort sharing: a comparison of studies. Clim Pol 14:122–147. https://doi.org/10.1080/14693062.2014.849452

Holz C, Kartha S, Athanasiou T (2018) Fairly sharing 1.5: national fair shares of a 1.5°C-compliant global mitigation effort. International environmental agreements: politics. Law Econ 18:117–134

IPCC (2014) In: Core Writing Team, Pachauri RK, Meyer LA (eds) Climate Change 2014: Synthesis Report. Contribution of Working Groups I, II and III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change. IPCC, Geneva, Switzerland

Kemp-Benedict E, Holz C, et al (2017) The Climate Equity Reference Calculator. Berkeley, CA: Climate Equity Reference Project (EcoEquity and Stockholm Environment Institute). Retrieved from Climate Equity Reference: https://calculator.climateequityreference.org.

McCollum DL, Zhou W, Bertram C, de Boer H-S, Bosetti V, Busch S, Després J, Drouet L, Emmerling J, Fay M, Fricko O, Fujimori S, Gidden M, Harmsen M, Huppmann D, Iyer G, Krey V, Kriegler E, Nicolas C, Pachauri S, Parkinson S, Poblete-Cazenave M, Rafaj P, Rao N, Rozenberg J, Schmitz A, Schoepp W, van Vuuren D, Riahi K (2018) Energy investment needs for fulfilling the Paris Agreement and achieving the Sustainable Development Goals. Nat Energy 3(7):589–599. https://db1.ene.iiasa.ac.at/CDLINKSDB/dsd?Action=htmlpage&page=welcome

Millar RJ et al (2017) Emission budgets and pathways consistent with limiting warming to 1.5°C. Nat Geosci 10(10)741–747. https://doi.org/10.1038/ngeo3031

Pan X, Teng F, Wang G (2014) Sharing emission space at an equitable basis: allocation scheme based on the equal cumulative emission per capita principle. Appl Energy 113:1810–1818. https://doi.org/10.1016/j.apenergy.2013.07.021

Pan X, den Elzen MGJ et al (2017) Exploring fair and ambitious mitigation contributions under the Paris Agreement goals. Environ Sci Pol 74:49–56. https://doi.org/10.1016/j.envsci.2017.04.020

Raupach MR et al (2014) Sharing a quota on cumulative carbon emissions. Nat Clim Chang 4(10):873–879. https://doi.org/10.1038/nclimate2384

Robiou du Pont Y, Jeffery ML et al (2016) Equitable mitigation to achieve the Paris Agreement goals. Nat Clim Chang 7(1):38–43. https://doi.org/10.1038/nclimate3186

Rogelj J et al (2016a) Paris Agreement climate proposals need a boost to keep warming well below 2°C. Nature 534(7609):631–639. https://doi.org/10.1038/nature18307

Rogelj J et al (2016b) Differences between carbon budget estimates unravelled. Nat Clim Chang 6(3):245–252. https://doi.org/10.1038/nclimate2868

Stocker TF et al. (2013) Climate Change 2013: The Physical Science Basis. Working Group I Contribution to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change 2013. Cambridge University Press, Cambridge, United Kingdom and New York, NY, USA, 1535 pp.

Tavoni M et al (2015) Post-2020 climate agreements in the major economies assessed in the light of global models. Nature Clim Change 5(2):119–126

UNFCCC (1992) United Nations Framework Convention on Climate Change. United Nations, UNFCCC Report FCCC/INFORMAL/84, GE.05-62220 (E) 200705. Available at: http://unfccc.int/resource/docs/convkp/conveng.pdf, Bonn, Germany.

UNFCCC (1997) Paper no. 1: Brazil; Proposed Elements of a Protocol to the United Nations Framework Convention on Climate Change. UNFCCC/AGBM/1997/MISC.1/Add.3 GE.97, Bonn

van Soest HL et al (2017) Low-emission pathways in 11 major economies: comparison of cost-optimal pathways and Paris climate proposals. Clim Chang 142(3-4):491–504. https://doi.org/10.1007/s10584-017-1964-6

van Vuuren DP et al (2011) How well do integrated assessment models simulate climate change? Clim Chang 104(2):255–285. https://doi.org/10.1007/s10584-009-9764-2

van Vuuren DP et al (2017) Energy, land-use and greenhouse gas emissions trajectories under a green growth paradigm. Glob Environ Chang 42:237–250. https://doi.org/10.1016/j.gloenvcha.2016.05.008

Vandyck T, Keramidas K et al (2016) A global stocktake of the Paris pledges: implications for energy systems and economy. Glob Environ Chang 41:46–63. https://doi.org/10.1016/j.gloenvcha.2016.08.006

Wang L, Chen W et al (2017) Dynamic equity carbon permit allocation scheme to limit global warming to two degrees. Mitig Adapt Strateg Glob Chang 22(4):609–628. https://doi.org/10.1007/s11027-015-9690-8

Winkler H, Höhne N, Cunliffe G et al (2017) Countries start to explain how their climate contributions are fair: more rigour needed. Int. Environ. Agreements Polit. Law Econ 18(1):99–115. https://doi.org/10.1007/s10784-017-9381-x

Acknowledgements

We thank all CD-LINKS project partners for contributing scenarios to the CD-LINKS database, some of which are used here. The results presented here are not automatically endorsed by CD-LINKS project partners.

Funding

This study benefited from the financial support of the European Commission via the Linking Climate and Development Policies-Leveraging International Networks and Knowledge Sharing (CD-LINKS) project, financed by the European Union’s Horizon 2020 research and innovation programme under grant agreement no. 642147 (CD-LINKS).

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

This article is part of a Special Issue on 'National Low-Carbon Development Pathways' edited by Roberto Schaeffer, Valentina Bosetti, Elmar Kriegler, Keywan Riahi, Detlef van Vuuren, and John Weyant.

Electronic supplementary material

ESM 1

(PDF 428 kb)

Rights and permissions

Open Access This article is distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution, and reproduction in any medium, provided you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made.

About this article

Cite this article

van den Berg, N.J., van Soest, H.L., Hof, A.F. et al. Implications of various effort-sharing approaches for national carbon budgets and emission pathways. Climatic Change 162, 1805–1822 (2020). https://doi.org/10.1007/s10584-019-02368-y

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10584-019-02368-y