Abstract

This paper analyzes the short-term market efficiency of the mutual fund industry around the world. Using a unique database of worldwide domestic equity funds, it employs a parametric (regression model) and non-parametric (data envelopment analysis (DEA) model) approaches to establish a relation between cost (expense ratio, turnover, loads, and risk) and benefit (return) of mutual funds. The empirical results of the parametric approach show a statistically significant negative relationship between expenses and risk-adjusted performance across countries. When we reexamine this relationship using a non-parametric approach, we show, in contrast to our previous result, a positive relationship between expenses and risk-adjusted performance. Thus, using the DEA methodology, we find strong evidence that equity mutual funds around the world are approximately mean–variance efficient.

Similar content being viewed by others

Notes

The US factors are drawn from French’s website: http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/.

An efficient economic outcome is a situation where one party’s position cannot be improved

without making another party’s position worse.

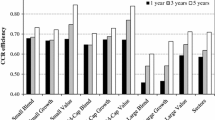

We omit the tables for the sake of brevity. They are, however, available from the authors upon request.

We do not report the coefficient estimates here for brevity but they are available from the authors upon request.

References

Angulo-Meza, L., & Lins, M. P. E. (2002). Review of methods for increasing discrimination in data envelopment analysis. Annals of Operations Research, 1, 225–242.

Basak, S., & Pavlova, A. (2013). Asset prices and institutional investors. American Economic Review, 103, 1728–1758.

Basso, A., & Funari, S. (2001). A data envelopment analysis approach to measure the mutual fund performance. European Journal of Operational Research, 135, 477–492.

Bergstresser, D., & Poterba, J. M. (2002). Do after-tax returns affect mutual fund inflows? Journal of Financial Economics, 63, 381–414.

Berkowitz, M., & Kotowitz, Y. (2002). Managerial quality and the structure of management expenses in the US mutual fund industry. International Review of Economics and Finance, 11, 315–330.

Bollen, N., & Busse, J. (2005). Short-term persistence in mutual fund performance. Review of Financial Studies, 18, 569–597.

Busse, J. A., & Irvine, P. J. (2006). Bayesian alphas and mutual fund persistence. Journal of Finance, 61, 2251–2288.

Castelli, L., Pesenti, R., & Ukovich, W. (2010). A classification of DEA models when the internal structure of the decision making unit is considered. Annals of Operations Research, 1, 207–235.

Carhart, M. (1997). On persistence in mutual fund performance. Journal of Finance, 52, 57–82.

Charnes, A., & Cooper, W. W. (1962). Programming with linear fractional functional. Naval Research Logistics, 9, 181–186.

Charnes, A., Cooper, W. W., Lewin, A. Y., & Seiford, L. M. (1994). Data envelopment analysis: Theory, methodology, and application. Boston: Kluwer Academic Publishers.

Charnes, A., Cooper, W. W., & Rhodes, E. (1978). Measuring the efficiency of decision making units. European Journal of Operational Research, 2, 429–444.

Chen, Y., & Zhu, J. (2003). DEA models for identifying critical performance measures. Annals of Operations Research, 1, 225–244.

Christoffersen, S. E. K., & Musto, D. K. (2002). Demand curves and the pricing of money management. Review of Financial Studies, 15, 1499–1524.

Coval, J., & Stafford, E. (2007). Asset fire sales (and purchases) in equity markets. Journal of Financial Economics, 86, 479–512.

Cremers, M., Ferreira, M. A., Matos, P., & Starks, L. (2016). Indexing and active fund management: International evidence. Journal of Financial Economics, 120, 539–560.

Deaves, R. (2004). Data-conditioning biases, performance, persistence and flows: The case of Canadian equity funds. Journal of Banking and Finance, 8, 673–694.

Díaz-Mendoza, A. C., López-Espinosa, G., & Martínez, M. A. (2014). The efficiency of performance-based fee funds. European Financial Management, 20, 825–855.

Dimson, E. (1979). Risk measurement when shares are subject to infrequent trading. Journal of Financial Economics, 7, 197–226.

Droms, W., & Walker, D. (1996). Mutual fund investment performance. Quarterly Review of Economics and Finance, 36, 347–363.

Elton, E., Gruber, M., Das, M., & Hlavka, M. (1993). Efficiency with costly information: A reinterpretation of evidence from managed portfolios. Review of Financial Studies, 6, 1–22.

Elton, E. J., Gruber, M. J., & Blake, C. R. (1996a). Survivorship bias and mutual fund performance. Review of Financial Studies, 9, 1097–1120.

Elton, E. J., Gruber, M. J., Das, S., & Blake, C. R. (1996b). The persistence of risk-adjusted mutual fund performance. Journal of Business, 69, 133–157.

Fama, E., & French, K. (1993). Common risk factors in the returns on stocks and bonds. Journal of Financial Economics, 33, 3–56.

Fama, E., & MacBeth, J. (1973). Risk, return, and equilibrium: Empirical tests. Journal of Political Economy, 81, 607–636.

Ferreira, M., Keswani, A., Miguel, A., & Ramos, S. (2012). The flow-performance relationship around the world. Journal of Banking and Finance, 36, 1759–1780.

Gil-Bazo, J., & Ruiz-Verdú, P. (2008). When cheaper is better: Fee determination in the market for equity mutual funds. Journal of Economic Behavior and Organization, 67, 871–885.

Gil-Bazo, J., & Ruiz-Verdu, P. (2009). The relation between price and performance in the mutual fund industry. Journal of Finance, 6, 2153–2183.

Greene, J. T., & Hodges, C. W. (2002). The dilution impact of daily fund flows on open end mutual funds. Journal of Financial Economics, 65, 131–158.

Grinblatt, M., & Titman, S. (1989). Adverse risk incentives and the design of performance-based contracts. Management Science, 35, 807–22.

Grinblatt, M., & Titman, S. (1994). A study of monthly mutual fund returns and performance evaluation techniques. Journal of Financial and Quantitative Analysis, 29, 419–444.

Grossman, S., & Stiglitz, J. (1980). On the impossibility of informationally efficient markets. American Economic Review, 70, 393–408.

Gruber, M. J. (1996). Another puzzle: The growth in actively managed mutual funds. Journal of Finance, 51, 783–810.

Hendricks, D., Patel, J., & Zeckhauser, R. J. (1993). Hot hands in mutual funds: Short- run persistence of relative performance, 1974–1988. Journal of Finance, 48, 93–130.

Investment Company Institute. (2015). Mutual fund factbook, 55th ed.

Ippolito, R. (1989). Efficiency with costly information: A study of mutual fund performance, 1965–1984. Quarterly Journal of Economics, 104, 1–23.

Jensen, M. C. (1968). The performance of mutual funds in the period 1945–1964. Journal of Finance, 23, 389–416.

Jensen, M. C. (1969). Risk, the pricing of capital assets, and the evaluation of investment portfolios. Journal of Business, 42, 167–247.

Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3, 305–360.

Khorana, A., Servaes, H., & Tufano, P. (2009). Mutual fund fees around the world. Review of Financial Studies, 22, 1279–1310.

Lehmann, B. N., & Modest, D. M. (1987). Mutual fund performance evaluation: A comparison of benchmarks and benchmark comparisons. Journal of Finance, 42, 233–265.

Malkiel, B. (1995). Returns from investing in equity mutual funds 1971 to 1991. Journal of Finance, 50, 549–72.

Markowitz, H. (1952). Portfolio selection. Journal of Finance, 7, 77–91.

Matallín-Saez, J. C. (2007). Portfolio performance: Factors or benchmarks? Applied Financial Economics, 17, 1167–1178.

Miller, S. M., & Noulas, A. G. (1996). The technical efficiency of large bank production. Journal of Banking and Finance, 20, 495–509.

Morey, M. R., & Morey, R. C. (1999). Mutual fund performance appraisals: A multi-horizon perspective with endogenous benchmarking. Omega, 27, 241–258.

Murthi, B. P. S., & Choi, Y. K. (2001). Relative performance evaluation of mutual funds: A non-parametric approach. Journal of Business Finance and Accounting, 28, 853–876.

Murthi, B. P. S., Choi, Y. K., & Desai, P. (1997). Efficiency of mutual funds and portfolio performance measurement: A non-parametric approach. European Journal of Operational Research, 98, 408–418.

Newey, W. K., & West, K. D. (1987). A simple, positive-definite, heteroskedasticity and autocorrelation consistent covariance matrix. Econometrica, 55, 703–708.

Otten, R., & Bams, D. (2002). European mutual fund performance. European Financial Management, 8, 75–101.

Ramos, S. (2009). The size and structure of the world mutual fund industry. European Financial Management, 15, 145–180.

Reilly, F., & Akhtar, R. (1995). The benchmark error problem with global capital markets. Journal of Portfolio Management, 22, 33–50.

Roll, R. R. (1978). Ambiguity when performance is measured by the securities market line. Journal of Finance, 33, 1051–1069.

Scott, R. C., & Horvath, P. A. (1980). On the direction of preference for moments of higher order than the variance. Journal of Finance, 35, 915–919.

Sharpe, W. F. (1966). Mutual fund performance. Journal of Business, 39, 119–138.

Sirri, E., & Tufano, P. (1998). Costly search and mutual fund flows. Journal of Finance, 53, 1589–1622.

Taylor, B., & Harris, G. (2004). Relative efficiency among South African universities: A data envelopment analysis. Higher Education, 47, 73–89.

Tobin, J. (1958). Liquidity preference as behavior towards risk. Review of Economic Studies, 25, 65–86.

Treynor, J. L. (1965). How to rate management of investment funds. Harvard Business Review, 43, 63–75.

Vidal-Garcia, J. (2013). The persistence of European mutual fund performance. Research in International Business and Finance, 28, 45–67.

Vidal-García, J., & Vidal, M. (2015). Is your fund watching out for you? SSRN working paper.

Vidal-García, J., Vidal, M., Boubaker, S., & Uddin, G. S. (2016). The short-term persistence of international mutual fund performance. Economic Modelling, 52(Part B), 926–938.

Vidal, M., Vidal-García, J., Lean, H. H., & Uddin, G. S. (2015). The relation between fees and return predictability in the mutual fund industry. Economic Modelling, 47, 260–270.

Author information

Authors and Affiliations

Corresponding author

Additional information

This paper was written while Sabri Boubaker was visiting professor in Finance at the International School, Vietnam National University, Hanoi, Vietnam.

Rights and permissions

About this article

Cite this article

Vidal-García, J., Vidal, M., Boubaker, S. et al. The efficiency of mutual funds. Ann Oper Res 267, 555–584 (2018). https://doi.org/10.1007/s10479-017-2429-z

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10479-017-2429-z