Abstract

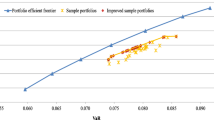

In this paper, we discuss the fuzzy portfolio efficiency evaluation problem in different risk measures. Real frontier approach (RFA) is often used in portfolio performance assessment. However, the computation complexity and the real trading solution make it hard to achieve in practice. In this work, we first present three kinds of DEA (Data envelopment analysis) based fuzzy portfolio estimation models in different risk measures, i.e., possibilistic variance, possibilistic semi-variance, and possibilistic semi-absolute deviation, to evaluate the portfolio efficiency (PE). Furthermore, we carry out large amount of simulations with different sample sizes to compare our proposed models with RFA. All results demonstrate that with adequate sample size, the envelop frontier generated by our models can approximate the real effective portfolio frontier, and PE obtained by these two methods are highly related.

Similar content being viewed by others

References

Banker, R. D., Charnes, A., & Cooper, W. W. (1984). Some models for estimating technical and scale inefficiencies in data envelopment analysis. Management Science, 30, 1078–1092.

Branda, M., & Kopa, M. (2016). DEA models equivalent to general Nth order stochastic dominance efficiency tests. Operations Research Letters, 44, 285–289.

Calvo, C., Ivorra, C., & Liern, W. (2016). Fuzzy portfolio selection with non-financial goals: Exploring the efficient frontier. Annals of Opearation Reaseach, 245, 31–46.

Carlsson, C., & Fullér, R. (2001). On possibilistic mean value and variance of fuzzy numbers. Fuzzy Sets and Systems, 122, 325–326.

Carlsson, C., Fullér, R., & Majlender, P. (2002). A possibilistic approach to selecting portfolios with highest utility score. Fuzzy Sets and Systems, 131, 13–21.

Charnes, A., Cooper, W. W., & Rhodes, E. (1978). Measuring the efficiency of decision making units. European Journal of Operational Research, 2, 429–444.

Chen, W. (2009). Two possibilistic mean–variance models for portfolio selection. Fuzzy Information and Engerneering, 2, 1035–1044.

Chen, W. (2015). Artificial bee colony algorithm for constrained possibilistic portfolio optimization problem. Physica A, 429, 125–139.

Chen, G., Liao, X., & Wang, S. (2009). A cutting plane algorithm for MV portfolio selection model. Applied Mathematics and Computation, 215, 1456–1462.

Chen, W., Wang, Y., & Mehlawat, M. K. (2016). A hybrid FA-SA algorithm for fuzzy portfolio selection with transaction costs. Annals of Operations Research. doi:10.1007/s10479-016-2365-3.

Ding, H., Zhou, Z. B., Xiao, H., Ma, C., & Liu, W. (2014). Performance evaluation of portfolios with margin requirements. Mathematical Problems in Engineering. doi:10.1155/2014/618706.

Edirisinghe, N. C. P., & Zhang, X. (2007). Generalized DEA model of fundamental analysis and its application to portfolio optimization. Journal of Banking Finance, 31, 331–333.

Grootveld, H., & Hallerbach, W. (1999). Variance vs downside risk: Is there really that much difference? European Journal of Operational Research, 114, 304–319.

Huang, X. (2008). Mean-semivariance models for fuzzy portfolio selection. Journal of Computational and Applied Mathematics, 217, 1–8.

Jensen, M. C. (1968). The performance of mutual funds in the period 1945–1964. The Journal of Finance, 23, 389–416.

Joro, T., & Na, P. (2006). Portfolio performance evaluation in a mean-variance-skewness framework. European Journal of Operational Research, 175, 446–461.

Konno, H., Shirakawa, H., & Yamazaki, H. (1993). A mean-absolute deviation-skewness portfolio optimization model. Annals of Operations Research, 45, 205–220.

Konno, H., & Yamazaki, H. (1991). Mean-absolute deviation portfolio optimization model and its applications to Tokyo stock market. Management Science, 37, 519–531.

Krzemienowski, A., & Szymczyk, S. (2016). Portfolio optimization with a copula-based extension of conditional value-at-risk. Annals of Operations Research, 237, 219–236.

Lim, S., Oh, K. W., & Zhu, J. (2013). Use of DEA cross-efficiency evaluation in portfolio selection: An application to Korean stock market. European Journal of Operational Research, 236, 361–368.

Li, X., & Qin, Z. (2014). Interval portfolio selection models within the framework of uncertainty theory. Economic Modelling, 41, 338–344.

Liu, Y. J., & Zhang, W. G. (2013). Fuzzy portfolio optimization model under real constraints. Insurance: Mathematics and Economics, 53, 704–711.

Liu, Y. J., Zhang, W. G., & Wang, J. B. (2016). Multi-period cardinality constrained portfolio selection models with interval coefficients. Annals of Operations Research, 244, 545–569.

Liu, W. B., Zhou, Z. B., Liu, D. B., & Xiao, H. L. (2014). Estimation of portfolio efficiency. Omega, 52, 107–118.

Markowitz, H. (1952). Portfolio selection. The Journal of Finance, 7, 77–91.

Markowitz, H., Todd, P., Xu, G. L., & Yamane, Y. (1993). Computation of mean-semivariance efficient sets by the Critical Line Algorithm. Annals of Operations Research, 45, 307–317.

Mashayekhi, Z., & Omrani, H. (2016). An integrated multi-objective Markowitz-DEA cross-efficiency modelwith fuzzy returns for portfolio selection problem. Applied Soft Computing, 38, 1–9.

Moazeni, S., Coleman, T. F., & Li, Y. (2016). Smoothing and parametric rules for stochastic mean-CVaR optimal execution strategy. Annals of Operations Research, 237, 99–120.

Morey, M. R., & Morey, R. C. (1999). Mutual fund performance appraisals: A multi-horizon perspective with end ogenous bench marking. Omega, 127, 241–258.

Qin, Z. (2015). Mean-variance model for portfolio optimization problem in the simultaneous presence of random and uncertain returns. European Journal of Operational Research, 245, 480–488.

Qin, Z., Kar, S., & Zheng, H. (2016). Uncertain portfolio adjusting model using semi-absolution deviation. Soft Computing, 20, 717–725.

Roll, R. (1978). Ambiguity when performance is measured by the security market line. The Journal of Finance, 33, 1051–1069.

Roy, D. (1952). Safety-first and the holding of assets. Econometrica, 20, 431–449.

Sharpe, W. (1966). Mutual fund performance. The Journal of Business, 39, 119–138.

Speranza, M. G. (1993). Linear programming models for portfolio optimization. The Journal of Finance, 12, 107–123.

Tavana, M., Keramatpour, M., Santos-Arteaga, F. G., & Ghorbaniane, E. (2015). A fuzzy hybrid project portfolio selection method using data envelopment analysis, TOPSIS and integer programming. Expert Systems with Applications, 42, 8432–8444.

Treynor, J. (1965). How to rate management investment funds. Harvard Business Review, 44, 131–136.

Vercher, E., & Bermúdez, J. D. (2015). Portfolio optimization using a credibility mean-absolute semi-deviation model. Expert Systems with Applications, 42, 7121–7131.

Wang, B., Wang, S., & Watada, J. (2011). Fuzzy portfolio selection models with value-at-risk. IEEE Transactions on Fuzzy Systems, 19, 758–769.

Zadeh, L. A. (1965). Fuzzy set. Information and Control, 8, 338–353.

Zhang, W. G., & Nie, Z. K. (2003). On possibilistic variance of fuzzy numbers. Lecture Notes in Computer Science, 2639, 398–402.

Zhao, S., Lu, Q., Han, L., Yong, L., & Hu, F. (2015). A mean-CVaR-skewness portfolio optimization model based on asymmetric Laplace distribution. Annals of Operations Research, 226, 727–739.

Acknowledgements

Authors would like to thank the Editor and the anonymous reviewers for their valuable comments and detailed suggestions that have improved the presentation of this paper. The research of first and second authors is supported by the Humanity and Social Science Youth foundation of Ministry of Education of China (No. 13YJC630012). The second author also acknowledges the support by Graduate Science and Technology Innovation Foundation from the Capital University of Economics and Business, Beijing, China. Furthermore, the third author acknowledges the research support through Research and Development and DST PURSE-II grants from University of Delhi, Delhi, India.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Chen, W., Gai, Y. & Gupta, P. Efficiency evaluation of fuzzy portfolio in different risk measures via DEA. Ann Oper Res 269, 103–127 (2018). https://doi.org/10.1007/s10479-017-2411-9

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10479-017-2411-9