Abstract

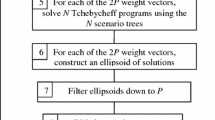

To solve a decision problem under uncertainty via stochastic programming means to choose or to build a suitable stochastic programming model taking into account the nature of the real-life problem, character of input data, availability of software and computer technology. In applications of multistage stochastic programs additional rather complicated modeling issues come to the fore. They concern the choice of the horizon, stages, methods for generating scenario trees, etc. We shall discuss briefly the ways of selecting horizon and stages in financial applications. In our numerical studies, we focus on alternative choices of stages and their impact on optimal first-stage solutions of bond portfolio optimization problems.

Similar content being viewed by others

References

Ainassari, K., M. Kallio, and A. Ranne. (1998). “Selecting an Optimal Investment Portfolio for a Pension Insurance Company.” Papers of the 8th AFIR Colloquium, pp. 7–23.

Bertocchi, M., J. Dupačová and V. Moriggia. (2000). “Sensitivity of Bond Portfolio's Behavior with Respect to Random Movements in Yield Curve: A Simulation Study.” Ann. Oper. Res. 99, 267–286.

Birge, J.R. and F. Louveaux. (1997). Introduction to Stochastic Programming, Springer, New York.

Black, F., E. Derman, and W. Toy. (1990). “A One-Factor Model of Interest Rates and Its Application to Treasury Bond Options.” A Financial Analysts Journal, pp. 33–39.

Bradley, S.P. and D.B. Crane. (1980). “Managing a Bank Portfolio Over Time.” In M.A.H. Dempster (ed.), pp. 449–471.

Brodt, A.I. (1984). “Intertemporal Bank Asset and Liability Management.” J. Bank. Res. 15, 82–94.

Cariño, D.R., D.H. Myers, and W.T. Ziemba. (1998). “Concepts, Technical Issues, and Uses of the Russell-Yasuda Kasai Financial Planning Model.” Oper. Res. 46, 450–462.

Carino, D.R. and A.L. Turner. (1998). “Multiperiod Asset Allocation with Derivative Assets.” In W.T. Ziemba and J. Mulvey (eds.), pp. 182–204.

Consigli, G. and M.A.H. Dempster. (1998). “Dynamic Stochastic Programming for Asset-Liability Management.” Ann. Oper. Res. 81, 131–161.

Cox, J.C., J.E. Jr. Ingersoll, and S.A. Ross. (1985). “A Theory of Term Structure of Interest Rates,” Econometrica 53, 385–407.

Dempster, M.A.H. (ed.), (1980). Stochastic Programming, Academic Press, London.

Dempster, M.A.H. and A.M. Ireland. (1988). “A Financial Expert Decision Support System.” In Mathematical Models for Decision Support, G. Mitra (ed.), NATO ASI Series 48, pp. 415–440.

Dert, C.L. (1998). “A Dynamic Model for Asset Liability Management for Defined Benefit Pension Funds.” In W.T. Ziemba and J. Mulvey (eds.), pp. 501–536.

Dupačová, J. (1995). “Postoptimality for Multistage Stochastic Linear Programs.” Ann. Oper. Res. 56, 65–78.

Dupačová, J. (1999). “Portfolio Optimization Via Stochastic Programming: Methods of Output Analysis.” MMOR 50, 245–270.

Dupačová, J. (2000). “Stability Properties of a Bond Portfolio Management Problem.” Ann. Oper. Res. 99, 251–265.

Dupačová, J. (2000). “Horizon and Stages in Applications of Stochastic Programming in Finance.” WP 30, University of Bergamo.

Dupačová, J. (2001). “Output Analysis for Approximated Stochastic Programs.” In Stochastic Optimization: Algorithms and Applications, S. Uryasev and P. M. Pardalos (eds.), Kluwer Acad. Publ., pp. 1–29.

Dupačová, J. (2002). “Applications of Stochastic Programming: Achievements and Questions.” European J. Oper. Res. 140, 281–290.

Dupačová, J. and M. Bertocchi. (2001). “From Data to Model and Back to Data: A Bond Portfolio Management Problem.” European J. Oper. Res. 134, 261–278.

Dupačová, J., M. Bertocchi, and V. Moriggia. (1998). “Postoptimality for Scenario Based Financial Models with an Application to Bond Portfolio Management.” In W.T. Ziemba and J. Mulvey (eds.), pp. 263–285.

Dupačová, J., G. Consigli, and S.W. Wallace. (2000). “Scenarios for Multistage Stochastic Programs.” Ann. Oper. Res 100, 25–53.

Dupačová, J., J. Hurt, and J. Štěpán. (2002). Stochastic Modeling in Economics and Finance, Kluwer Acad. Publ., Dordrecht.

Fleten, S.E., K. Høyland, and S.W. Wallace. (2002). “The Performance of Stochastic Dynamic and Fixed Mix Portfolio Models.” European J. Oper. Res. 140, 37–49.

Frauendorfer, K. and Ch. Marohn. (1998). “Refinement Issues in Stochastic Multistage Linear Programming.” Stochastic Programming Methods and Technical Applications, In K. Marti and P. Kall (eds.), LNEMS 458, pp. 305–328.

Golub, B. et al. (1995). “Stochastic Programming Models for Portfolio Optimization with Mortgage-Backed Securities.” European J. Oper. Res. 82, 282–296.

Grinold, R.C. (1986). “Infinite Horizon Stochastic Programs.” SIAM J. Control Optim. 24, 1246–1260.

Kall, P. and S.W. Wallace. (1994). Stochastic Programming, Wiley, Chichester.

Kouwenberg, R.R.P. (1998). “Scenario Generation and Stochastic Programming Models for Asset Liability Management.” European J. Oper. Res. 134, 279–292.

Kusy, M.I. and W.T. Ziemba. (1986). “A Bank Asset and Liability Management Model.” Oper. Res. 34, 356–376.

Messina, E. and G. Mitra. (1996). “Modelling and Analysis of Multistage Stochastic Programmnig Problems: A Software Environment.” European J. Oper. Res. 101, 343–359.

Mulvey, J.M., D.P. Rosenbaum, and B. Shetty. (1997). “Strategic Financial Risk Management and Operations Research.” European J. Oper. Res. 97, 1–16.

Mulvey, J.M. and W.T. Ziemba. (1995). “Asset and Liability Allocation in a Global Environment.” Chapter 15 Handbooks in OR& MS 9, In R. Jarrow et al. (eds.), Elsevier.

Nielsen, S.S. and R. Poulsen. (2004). “A Two-Factor, Stochastic Programming Model of Danish Mortgage-Backed Securities, J. Econ. Dynamics and Control 28(7), 1267–1289, Elsevier.

Nielsen, S.S. and S.A. Zenios. (1996). “A Stochastic Programming Model for Funding Single Premium Deferred Securities.” Math. Programming 75, 177–200.

Prékopa, A. (1995). Stochastic Programming, Kluwer, Dordrecht and Académiai Kiadø, Budapest.

Shapiro, A., T. Homem-de-Mello, and J. Kim. (2002). “Conditioning of Convex Piecewise Linear Stochastic Programs.” Math. Programming A94, 1–19.

Wets, R.J.-B. and W.T. Ziemba. (eds.) (1999). Stochastic Programming. State of the Art, 1998. Ann. Oper. Res. 85.

Zenios, S.A. and M.S. Shtilman. (1993). “Constructing Optimal Samples from a Binomial Lattice.” J. Inform. Optim. Sci. 14, 125–147.

Zenios, S.A. et al. (1998). “Dynamic Models for Fixed-Income Portfolio Management under Uncertainty.” J. Econ. Dynamics Control 22, 1517–1541.

Ziemba, W.T. and J. Mulvey. (eds.) (1998). World Wide Asset and Liability Modeling, Cambridge Univ. Press.

Author information

Authors and Affiliations

Corresponding author

Additional information

AMS Subject classification 90C15 . 92B28

Rights and permissions

About this article

Cite this article

Bertocchi, M., Moriggia, V. & Dupačová, J. Horizon and stages in applications of stochastic programming in finance. Ann Oper Res 142, 63–78 (2006). https://doi.org/10.1007/s10479-006-6161-3

Issue Date:

DOI: https://doi.org/10.1007/s10479-006-6161-3