Abstract

The paper shows that currencies of countries with persistent current account surpluses and high foreign-currency denominated assets, such as the Swiss franc and the Japanese yen, are under persistent appreciation pressure, particularly when the centres of the world monetary system follow expansionary monetary policies. This limits the choice of exchange rate regime. Given flexible exchange rates, a negative risk premium on the domestic interest rate can emerge. Empirical estimations provide mixed evidence for a negative impact of net foreign asset positions and exchange rate uncertainty on interest rates of international creditor countries at the periphery of the world monetary system.

Source: Pacific Exchange Rate Service

Source: IMF, Reuters/Thomson, Federal Reserve, Swiss National Bank. Long-term is approximated by 10-year government bonds yields, short-term is approximated by money market rates

Source: IMF, ECB, Reuters/Thomson, Pacifics Exchange Rate Service

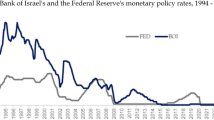

Source: OECD, IMF, Swiss National Bank

Similar content being viewed by others

Notes

Kugler and Weder (2009) reconsider this effect.

Investing in time t one unit of saving in home has a return of 1 + iCH (1 + iJap) after the end of the investment period in t + 1. For one unit invested in the euro area, the return in domestic currency at the end of the investment period is ((1 + iEA(US))/et)*et + 1) with e being the exchange rate between the Swiss franc and the euro (between the Japanese yen and the US dollar) in price notation.

This assumption corresponds to the regional currency habitat in the world economy. Whereas in Europe (and some neighbouring countries) the euro is the dominating international medium of exchange, unit of account, store of value, anchor currency, intervention currency and reserve currency, the dollar is the dominating international currency in the rest of the world (McKinnon 2013).

The equilibrium condition for the Swiss investor is 1 + iCH = ((1 + iEA)/et)*et + 1) which is equivalent to the uncovered interest rate parity as in equation (1). Empirical evidence on the uncovered interest rate parity is mixed (see for instance Wu and Show-Lin 1998, Chinn 2005, Lothian and Wu 2011).

Germany (euro area) is assumed to be a net debtor country versus Switzerland and in absolute terms a larger net creditor country versus the rest of the world. This implies an overall international creditor position for Germany (euro area).

In Japan, this trend halted with the introduction of Abenomics, starting in January 2013.

For a historical overview of exchange rate policies including Switzerland and Japan see Bordo et al. (2012).

Given a starting point in year 1, the net foreign asset position in year n is equivalent to the accumulated current account positions up to the year n: \( {NIIP}_n={\sum}_{s=1}^n{CA}_s \)

In this context, Lane and Milesi-Feretti (2005) stress that also revaluation effects matter. The change in the net international investment position NIIP is equivalent to the current account (CAt) and revaluation effects RVt: NIIP t − NIIP t − 1 = CA t + RV t . Revaluation effects can originate in changes in foreign asset prices and exchange rate changes.

Note that in Japan, following the 2011 tsunami disaster, current account surpluses declined as energy imports have increased.

This analysis focuses on aggregated net international investment positions. Joyce (2015) takes a closer look on the compositions of net international investment positions disentangling the asset and liability side as well as different forms of international assets such as FDI.

Brown et al. (2009) provide a detailed overview of the currency composition of Swiss international assets. Since the turn of the millennium Swiss and Austrian banks (by borrowing from Swiss banks) have issued substantial amounts of Swiss franc credit in many central and eastern European economies as well as in Germany (mainly held by local public entities). By Swiss franc lending the Swiss and Austrian banks could circumvent the exchange rate risk of international lending. The Swiss franc appreciation shock in early 2015 revealed, however, that this type of lending transforms currency risk into default risk (McKinnon and Schnabl 2004a, b). In case of a strong appreciation of the creditor currency the credit taking households, enterprises and local public entities are threatened by default. In some central and eastern European countries policy makers have shifted the costs of the revaluation effects of the franc appreciation back to banks.

This is coined “Conflicted Virtue” by McKinnon and Schnabl (2004b), as a complementary expression to “Original Sin” as put forward by Eichengreen and Hausmann (1999). Countries such Japan, Switzerland and China are virtuous because of their high saving rates. The resulting current account surpluses and rising foreign-currency denominated international creditor positions create, however, the curse of persistent appreciation pressure and foreign exchange risk.

This is regarded as a mercantilist trade strategy. See for instance Dooley et al. (2004).

In the portfolio balance model by Branson (1977) investors have a preference for domestic assets in face of exchange rate uncertainty, and hold foreign assets only for a risk premium. The portfolio balance model can also explain why – as in the case of Japan – the currency of a country with a persistently positive current account balance follows an appreciation trend: An (expansionary) monetary policy shock causes the domestic interest rate to depreciate beyond the long-term equilibrium, which implies a continuous appreciation path which goes along with a positive current account position.

See Calvo and Reinhart (2002) for this asymmetry of the world monetary system.

Austria, Belgium, Bosnia-Herzegovina, Bulgaria, Croatia, Czech Republic, Denmark, Estonia, Finland, France, Hungary, Iceland, Ireland, Italy, Japan, Latvia, Lithuania, Luxemburg, Netherlands, Norway, Poland, Portugal, Romania, Slovak Republic, Slovenia, Spain, Sweden, Switzerland and United Kingdom.

Lane and Milesi-Feretti (2001) use nominal exports for normalization. They argue that normalizing by GDP or alternatively by exports does not significantly change the econometric estimation results.

We do not assume a systematic impact of the interest rate differential on exchange rate uncertainty.

References

Abrahamsen Y, Simmons-Süer B (2011) Die Wechselkursabhängigkeit der Schweizer Wirtschaft. KOF Studien 24:2011

Bénétrix A, Lane P, Shambaugh J (2014) International currency exposures, valuation effects and the global financial crisis. NBER working paper 20820

Bernholz P, Minsch R (2015) Der Franken-Schock: Die Freigabe des Schweizer Franken – wer gewinnt und wer verliert? Ifo Schnelldienst 68(5):9–13

Bordo M, Humpage O, Schwartz A (2012) Epilogue: foreign-exchange-market operations in the twenty-first century. NBER working paper 17984

Branson W (1977) Exchange rates in the short run: the dollar deutsche mark rate. Eur Econ Rev 10:303–324

Brown M, Peter M, Wehrmüller S (2009) Swiss franc lending in Europe. Aussenwirtschaft 64(2):167–181.

Calvo G, Reinhart C (2002) Fear of floating. Q J Econ 117(2):379–408

Chinn M (2005) The (partial) rehabilitation of interest rate parity in the floating rate era: longer horizons, Alternative Expectations, and Emerging Markets. J Int Money Financ 25(1):7–21

Corsetti G, Pesenti P, Roubini N (1999) Paper tigers? A model of the Asian crisis? Eur Econ Rev 43(7):1211–1236

Danne C, Schnabl G (2008) A role model for China? Exchange rate flexibility and monetary policy making in Japan. China Econ Rev 19(2):183–196

Dooley M, Folkerts-Landau D, Garber P (2004) The revived Bretton woods system. Int J Financ Econ 9(4):307–313

Eichengreen B, Hausmann R (1999) Exchange rates and financial fragility. NBER working paper 7418

Goyal R, McKinnon R (2003) Japan's negative risk premium in interest rates: the liquidity trap and the fall in Bank lending. World Econ 26(3):339–363

Joyce J (2015) External balance sheets as countercyclical crisis buffers. Mimeo

Kugler P, Weder B (2005) Why are returns of Swiss franc assets so low? CEPR Discussion Paper 5181.

Kugler P, Weder B (2009) The demise of the swiss interest rate puzzle. University of Basle Faculty of Business and Economics Working Paper 2009/04

Lane P, Milesi-Feretti GM (2001) Long-term capital movements. NBER working paper 8366

Lane P, Milesi-Feretti GM (2005) A global perspective on net external positions. IMF working paper 05/161

Lane P, Milesi-Feretti GM (2007) The external wealth of nations mark II: revised and extended estimates of foreign assets and liabilities. J Int Econ 73(2):223–250

Lothian J, Wu L (2011) Uncovered interest-rate parity over the past two centuries. J Int Money Financ 30(3):448–473

McKinnon R (2013) The unloved dollar standard: from Bretton woods to the rise of China. Oxford University Press, Oxford

McKinnon R, Ohno K (1997) Dollar and yen: resolving economic conflict between the United States and Japan. MIT Press, Cambridge

McKinnon R, Schnabl G (2004a) The east Asian dollar standard, fear of floating, and original sin. Rev Dev Econ 8(3):331–360

McKinnon R, Schnabl G (2004b) The return to soft dollar pegging in East Asia? Mitigating conflicted virtue. Int Financ Rev 7(2):169–201

McKinnon R, Schnabl G (2009) The case for stabilizing China's exchange rate: setting the stage for fiscal expansion. Chin World Econ 17:1–32

Wu J-l, Show-Lin C (1998) A re-examination of real interest rate parity. Can J Econ 31:837–851

Acknowledgements

We thank Hannes Böhm, Talina Sondershaus and David Herok for excellent research assistance. We thank Eiji Ogawa, the participants of the 2015 EEFS conference in Brussels and the participants of the Hitotsubashi research seminar in Tokyo for useful comments.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Latsos, S., Schnabl, G. Net foreign asset positions and appreciation expectations on the Swiss franc and the Japanese Yen. Int Econ Econ Policy 15, 261–280 (2018). https://doi.org/10.1007/s10368-017-0403-5

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10368-017-0403-5

Keywords

- Swiss franc

- Japanese yen

- Exchange rate risk

- Negative risk premium

- Self-fulfilling expectations

- Appreciation pressure