Abstract

The complexity involved in portfolio selection has resulted in the development of a large number of methods to support ambiguous financial decision making. We consider portfolio selection problems where returns from investment securities are random variables with fuzzy information and propose a data envelopment analysis model for portfolio selection with downside risk criteria associated with value-at-risk (V@R) and conditional value-at-risk (CV@R). Both V@R and CV@R criteria are used to define possibility, necessity, and credibility measures, which are formulated as stochastic nonlinear programming programs with random-fuzzy variables. Our constructed stochastic nonlinear programs for analyzing portfolio selection are transformed into deterministic nonlinear programs. Moreover, we show an enumeration algorithm can solve the model without any mathematical programs. Finally, we demonstrate the applicability of the proposed framework and the efficacy of the procedures with a numerical example.

Similar content being viewed by others

Notes

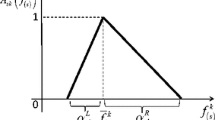

If \( \varphi = Pos \) in Eq. (4), then a V@R-Possibility measure is described as

\( \hbox{min} \,\,f\,\;s.t.\quad Pos\left[ {V@R_{\alpha } \left[ {\sum\limits_{j = 1}^{n} {x_{j} \tilde{r}_{j} } } \right] \le \,f} \right] \ge \beta \,,\,\;E\,\left[ {\sum\limits_{j = 1}^{n} {x_{j} \tilde{r}_{j} } } \right] \ge \eta ,\;\;\sum\limits_{j = 1}^{n} {x_{j} } = 1,\quad \,x_{j} \ge 0,\,\,\,j = 1, \ldots ,n.\, \)

When we refer to a measure, we use V@R instead of \( V@R_{\alpha } \) for simplicity. This applies to the case of CV@R.

References

Artzner P, Delbaen F, Eber J-M, Heath D (1999) Coherent measures of risk. Math Finance 9:203–228

Ayub U, Shah S, Abbas Q (2015) Robust analysis for downside risk in portfolio management for a volatile stock market. Econ Model 44:86–96

Branda M (2016) Mean-value at risk portfolio efficiency: approaches based on data envelopment analysis models with negative data and their empirical behaviour. Q J Oper Res 14(1):77–99

Buckley JJ (2004) Uncertain probabilities III: the continuous case. Soft Comput 8(3):200–206

Buckley JJ, Eslami E (2004) Uncertain probabilities II: the continuous case. Soft Comput 8(3):193–199

Charnes A, Cooper WW, Rhodes E (1978) Measuring the efficiency of decision making units. Eur J Oper Res 2:429–444

Chatterjee R (2014) Practical methods of financial engineering and risk management tools for modern financial professionals. Quantitative finance series. Apress, New York

Chen L, Peng J, Zhang B, Rosyida I (2017) Diversified models for portfolio selection based on uncertain semivariance. Int J Syst Sci 48(3):637–648

Chen W, Gai Y, Gupta P (2018) Efficiency evaluation of fuzzy portfolio in different risk measures via DEA. Ann Oper Res 269(1–2):103–127

Dubois D, Prade H (1978) Operations on fuzzy numbers. Int J Syst Sci 9(6):613–626

Dubois D, Prade H (1980) Operations on fuzzy numbers. Fuzzy sets and system: Theory and applications. Academic Press, New York

Dubois D, Prade H (1988) Possibility Theory. Plenum, New York

Hasuike T, Katagiri H, Ishii H (2009) Portfolio selection problems with random fuzzy variable returns. Fuzzy Sets Syst 160(18):2579–2596

Hirota K (1981) Concepts of probabilistic sets. Fuzzy Sets Syst 5:31–46

Huang X (2008) Mean-semivariance models for fuzzy portfolio selection. J Comput Appl Math 217:1–8

Joro T, Na P (2006) Portfolio performance evaluation in a mean-variance-skewness framework. Eur J Oper Res 175:446–461

Kerstens K, Van de Woestyne I (2018) Enumeration algorithms for FDH directional distance functions under different returns to scale assumptions. Ann Oper Res (forthcoming) 271:1067–1078

Khanjani Shiraz R, Charles V, Jalalzadeh L (2014) Fuzzy rough DEA model: a possibility and expected value approaches. Expert Syst Appl 41(2):434–444

Konno H, Yamazaki H (1991) Mean-absolute deviation portfolio optimization model and its applications to Tokyo stock market. Manag Sci 37:519–531

Kwakernaak H (1978) Fuzzy random variables. Part I: definitions and theorems. Inf Sci 15(1):1–29

Kwakernaak H (1979) Fuzzy random variables Part II: Algorithms and examples for the discrete case. Inf Sci 17(3):253–278

Li X, Qin Z, Kar S (2010) Mean–Variance-skewness model for portfolio selection with fuzzy returns. Eur J Oper Res 202:239–247

Liu B (2002) Theory and practice of uncertain programming. Physica Verlag, New York

Liu B (2007) Uncertainty theory: an introduction to its axiomatic foundations, 2nd edn. Springer, Berlin

Liu B, Liu YK (2002) Expected value of fuzzy variable and fuzzy expected value models. IEEE Trans Fuzzy Syst 10(4):445–450

Liu WB, Zhou ZB, Liu DB, Xiao HL (2015) Estimation of portfolio efficiency. Omega 52:107–118

Ma X, Zhao Q, Liu F (2015) Fuzzy risk measures and application to portfolio optimization. J Appl Math Inform 27(3):843–856

Markowitz H (1952) Portfolio selection. J Finance 7:77–91

Markowitz H (1959) Portfolio selection: efficient diversification of investment. Wiley, New York, p 1959

Markowitz H, Todd P, Xu GL, Yamane Y (1993) Computation of mean-semivariance efficient sets by the Critical Line Algorithm. Ann Oper Res 45:307–317

Morey MR, Morey RC (1999) Mutual fund performance appraisals: a multi-horizon perspective with endogenous bench marking. Omega 127:241–258

Rockafellar RT, Uryasev S (2000) Optimization of conditional value-at-risk. J Risk 2:21–41

Rockafellar RT, Uryasev S (2002) Conditional value-at-risk for general loss distributions. J Bank Finance 26(7):1443–1471

Seiford LM, Zhu J (1998) Stability regions for maintaining efficiency in data envelopment analysis. Eur J Oper Res 108(I 998):I27–I39

Tavana M, Khanjani Shiraz R, Hatami-Marbini A, Agrell P, Paryab K (2012) Fuzzy stochastic data envelopment analysis with application to base realignment and closure (BRAC). Expert Syst Appl 39(15):12247–12259

Tavana M, Khanjani Shiraz R, Hatami-Marbini A, Agrell P, Paryab K (2013) Chance-constrained DEA models with random fuzzy inputs and outputs. Knowl-Based Syst 52(2013):32–52

Tavana M, Khanjani Shiraz R, Di Caprio D (2019) A chance-constrained portfolio selection model with random-rough variables. Neural Comput Appl 31:931–945

Vercher E, Bermúdez JD (2015) Portfolio optimization using a credibility mean-absolute semi-deviation model. Expert Syst Appl 42:7121–7131

Wang B, Wang S, Watada J (2011) Fuzzy-portfolio-selection models with value-at-risk. IEEE Trans Fuzzy Syst 19(4):758–769

Zadeh LA (1978) Fuzzy sets as a basis for a theory of possibility. Fuzzy Sets Syst 1(1):3–28

Liu Y-J, Zhang W-G (2013) Fuzzy portfolio optimization model under real constraints. Insur Math Econ 53(3):704–711

Zhongfeng Q, Kar S, Zheng H (2018) Uncertain portfolio adjusting model using semiabsolute deviation. Soft Comput 20(2):717–725

Zimmermann HJ (1996) Fuzzy set theory and its applications, 2nd edn. Kluwer Academic Publishers, Dordrecht

Acknowledgements

The authors would like to thank the anonymous reviewers and the editor for their insightful comments and suggestions. Dr. Madjid Tavana is grateful for the partial support he received from the Czech Science Foundation (GAČR 19-13946S) for this research. Dr. Khanjani Shiraz received a grant from the Ministry of science, Research and Technology of the Islamic Republic of Iran in partial support of this research.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare no conflict of interest

Additional information

Communicated by V. Loia.

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Khanjani Shiraz, R., Tavana, M. & Fukuyama, H. A random-fuzzy portfolio selection DEA model using value-at-risk and conditional value-at-risk. Soft Comput 24, 17167–17186 (2020). https://doi.org/10.1007/s00500-020-05010-7

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00500-020-05010-7