Abstract

In this paper, a new estimator is proposed by combining basically the ordinary ridge regression estimator and the principal component regression estimator for a regression model which has multicollinearity and which satisfies some a priori stochastic linear restrictions. The performance of the proposed \(r{-}k\) class estimator in this mixed regression model is compared with those of the mixed regression estimator, ridge regression estimator and the stochastic restricted ridge regression estimator in terms of the mean squared error matrix criterion. Tests for verifying the conditions of dominance of the proposed estimator over the others are also proposed. Furthermore, a Monte Carlo study and a numerical illustration are carried out to empirically study the performance of the estimators by the mean squared error values, and then to perform tests to verify if the conditions for superiority of the proposed estimator over the others hold.

Similar content being viewed by others

Notes

Since the mean squared error matrix is the only criterion used in this paper for the purpose of comparison between two estimators, we use the abbreviation MSE to represent the mean squared error matrix all throughout this paper.

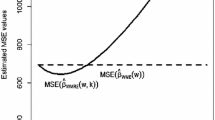

For brevity of space, the EMSE values are presented for one value of \(\phi \) \(viz\), \(\phi =0.5\), only and the process is AR(1) for both \(u_i\) and \(v_i\). The conclusions are same for the two other values of \(\phi \) i.e., \(\phi =0.2\) and \(0.8\), and for MA(1) process as well.

References

Baksalary JK, Trenkler G (1991) Nonnegative and positive definiteness of matrices modified by two matrices of rank one. Linear Algebra Appl 151:169–184

Baye MR, Parker DF (1984) Combining ridge and principal components regression:a money demand illustration. Commun Stat Theory Methods 13(2):197–205

Bayhan GM, Bayhan M (1998) Forecasting using autocorrelated errors and multicollinear predictor variables. Comput Ind Eng 34:413–421

Firinguetti L (1989) A simulation study of ridge regression estimators with autocorrelated errors. Commun Stat Simul Comput 18(2):673–702

Gujarati DN (2002) Basic econometrics, 4th edn. Tata McGraw-Hill, New York

Hoerl AE, Kennard RW (1970) Ridge regression:biased estimation for nonorthogonal problems. Technometrics 12:55–67

Johnson NL, Kotz S (1970) Distributions in statistics: Continuous Univariate Distributions - 2. Wiley, New York

Judge GG, Griffiths WE, Hill RC, Lütkepohl H, Lee TC (1985) The theory and practice of econometrics. John Wiley and Sons, New York

Kaçıranlar S, Sakallioğlu S (2001) Combining the Liu estimator and the principal component regression estimator. Commun Stat Theory Methods 30(12):2699–2705

Liu K (1993) A new class of biased estimate in linear regression. Comm Stat Theory Methods 22:393–402

Massy WF (1965) Principal components regression in exploratory statistical research. J Am Stat Assoc 60:234–266

Newhouse JP, Oman SD (1971) An evaluation of ridge estimators. Rand corporation, Santa Monica, pp 1–29

Özkale MR, Kaçiranlar S (2007) The restricted and unrestricted two parameter estimators. Commun Stat Theory Methods 36(15):2707–2725

Özkale MR, Kaçiranlar S (2008) Comparisons of the r-k class estimator to the ordinary least squares estimator under the Pitman’s closeness criterion. Stat Papers 49:503–512

Özkale MR (2009) A stochastic restricted ridge regression estimator. J Multivar Anal 100:1700–1706

Özkale MR (2012) Combining the unrestricted estimators into a single estimator and a simulation study on the unrestricted estimators. J Stat Comput Simul 62(4):653–688

Rao C, Toutenburg H (1995) Linear models: least squares and alternatives, 2nd edn. Springer, New York

Sarkar N (1992) A new estimator combining the ridge regression and the restricted least squares methods of estimation. Commun Stat Theory Methods 21:1987–2000

Sarkar N (1996) Mean square error matrix comparison of some estimators in linear regressions with multicollinearity. Stat Probab Lett 30:133–138

Sarkar N, Chandra S (2012) Comparison of the \({r-(k, d)}\) class estimator with some estimators under the Mahalanobis loss function, mimeo. www.isical.ac.in/~eru/papers

Theil H, Goldberger AS (1961) On pure and mixed statistical estimation in economics. Int Econ Rev 2:65–78

Trenkler G (1984) On the performance of biased estimators in the linear regression model with correlated or heteroscedastic errors. J Econom 25:179–190

Yang H, Wu J (2011) A stochastic restricted \({k-d}\) class estimator, Statistics, 1–8

Xu J, Yang H (2011) On the restricted \({r-k}\) class estimator and the restricted \({r-d}\) class estimator in linear regression. J Stat Comput Simul 81(6):679–691

Acknowledgments

The authors are thankful to the editor and the reviewers for their valuable comments and suggestions which have led to substantial improvement in the paper.

Author information

Authors and Affiliations

Corresponding author

Additional information

This work was carried out when the first author was a visiting scientist at Indian Statistical Institute, North-East Center, Tezpur, Assam, India, during July 2011–June 2012.

Rights and permissions

About this article

Cite this article

Chandra, S., Sarkar, N. A restricted \(r{-}k\) class estimator in the mixed regression model with autocorrelated disturbances. Stat Papers 57, 429–449 (2016). https://doi.org/10.1007/s00362-015-0664-4

Received:

Revised:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00362-015-0664-4

Keywords

- \(r{-}k\) class estimator

- Mixed regression estimator

- Stochastic linear restrictions

- Autocorrelated errors