Abstract

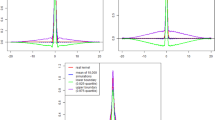

This paper studies nonparametric kernel type (smoothed) estimation of quantiles for long memory stationary sequences. The uniform strong consistency and asymptotic normality of the estimates with rates are established. Finite sample behaviors are investigated in a small Monte Carlo simulation study.

Similar content being viewed by others

References

Avram F and Taqqu MS (1987). Noncentral limit theorems and Appell polynomials. Ann Probab 15: 767–775

Beran J (1994). Statistics for long-memory processes. Chapman and Hall, New York

Cai ZW and Roussas GG (1992). Uniform strong estimation under β-mixing with rates. Stat Probab Lett 15: 47–55

Cai ZW and Roussas GG (1997). Smooth estimate of quantiles under association. Stat Probab Lett 36: 275–287

Csörgő S and Mielniczuk J (1995a). Density estimation under long-range dependence. Ann Stat 23: 990–999

Csörgő S and Mielniczuk J (1995b). Nonparametric regression under long-range dependent normal errors. Ann Stat 23: 1000–1014

Csörgő M, Szyszkowicz B and Wang L (2006). Strong invariance principles for sequential Bahadur–Kiefer and Vervaat error processes of long-range dependent sequences. Ann Stat 34: 1013–1044

Davydov YA (1970). The invariance principle for stationary processes. Theory Probab Appl 15: 487–498

Dehling H and Taqqu MS (1989). The empirical process of some long-range dependent sequences with an application to U-statistics. Ann Stat 17: 1767–1783

Doukhan P, Oppenheim G and Taqqu MS (2003). Theory and applications of long-range dependence. Birkhäuser, Boston

Draghicescu D, Ghosh S (2003) Smooth nonparametric quantiles. In: Proceedings, MENP-2, 22–27 April 2002. Geometry Balkan Press, Bucharest, pp 45–52

Estévez G and Vieu P (2003). Nonparametric estimation under long-memory dependence. J Nonparametric Stat 15: 535–551

Falk M (1984). Relative deficiency of kernel type estimators of quantiles. Ann Stat 12: 261–268

Falk M (1985). Asymptotic normality of the kernel quantile estimator. Ann Stat 13: 428–433

Falk M and Reiss RD (1989). Weak convergence of smoothed and nonsmoothed bootstrap quantile estimates. Ann Probab 17: 362–371

Ghosh S, Beran J and Innes J (1997). Nonparametric conditional quantile estimation in the presence of long memory. Student 2: 109–117

Ghosh S, Draghicescu D (2002) An algorithm for optimal bandwidth selection for smooth nonparametric quantile estimation. Statistical data analysis based on the L 1 norm and related methods, pp 161–168

Granger CW and Joyeux R (1980). An introduction to long-range time series models and fractional differencing. J Time Ser Anal 1: 15–30

Guégan D (2005). How can we define the concept of long memory? An econometric survey. Economet Rev 24: 113–149

Ho HC and Hsing T (1996). On the asymptotic expansion of the empirical process of long-memory moving averages. Ann Stat 24: 992–1024

Hosking JRM (1981). Fractional differencing. Biometrika 68: 165–176

Lejeune M and Sarda P (1991). Smooth estimators of distribution density functions. Comp Stat Data Anal 14: 457–471

Lobato I and Robinson PM (1996). Averaged periodogram estimation of long-memory. J Economet 73: 303–324

Moulines E and Soulier P (2003). Semiparametric spectral estimation for fractional processes. In: Doukhan, P, Oppenheim, G and Taqqu, MS (eds) Theory and applications of long-range dependence, pp 251–301. Birkhäuser, Boston

Nadaraya EA (1964). Some new esimates for distribution function. Theory Probab Appl 9: 497–500

Parzen E (1979). Nonparametric statistical data modeling. J Am Stat Assoc 74: 105–121

Ralescu SS and Sun S (1993). Necessary and sufficient conditions for the asymptotic normality perturbed sample quantiles. J Stat Plan Inference 35: 55–64

Read RR (1972). The asymptotic inadmissibility of the sample distribution function. Ann Math Stat 43: 89–95

Reiss RD (1980). Estimation of quantiles in certain nonparametric models. Ann Stat 8: 87–105

Robinson PM (1994). Semiparametric analysis of long-memory time series. Ann Stat 22: 515–539

Robinson PM (1995). Log-periodogram regression of time series with long range dependence. Ann Stat 23: 1048–1074

Robinson PM (1995). Gaussian semiparametric estimation of long range dependence. Ann Stat 23: 1630–1661

Wang Q, Lin Y and Gulati M (2003). Strong approximation for long-memory processes with applications. J Theor Probab 16: 377–389

Yamato H (1973). Uniform convergence of an estimator of a distribution function. Bull Math Stat 15: 69–78

Youndjé É and Vieu P (2006). A note on quantile estimation for long-range dependent stochastic processes. Stat Probab Lett 76: 109–116

Author information

Authors and Affiliations

Corresponding author

Additional information

Research supported by NSFC under grants No. 10501020, No. 10671089 and by SRF for ROCS, SEM Grant of Lihong Wang at Nanjing University.

Rights and permissions

About this article

Cite this article

Wang, L. Kernel type smoothed quantile estimation under long memory. Stat Papers 51, 57–67 (2010). https://doi.org/10.1007/s00362-007-0115-y

Received:

Revised:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00362-007-0115-y