Abstract

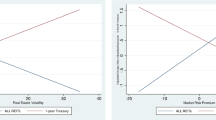

The aim of this paper is to investigate risky-prices sensitivity to interest rate changes in the Spanish market and to see if sensitivity is lower than public debt. To contrast this hypothesis, this paper presents a model that analyzes the risky-prices sensitivity to interest rate changes through effective duration and convexity. The most relevant contribution of the paper is to obtain a better specification to the duration expression that contribute to the marginal increment of the coefficient of determination and the construction of a conditional volatility model that overcomes the linearity models of constant variance.

Similar content being viewed by others

References

Bera, A. K.; Jarque, C. M. “An Efficient Large-Sample Test for Normality of Observations and Regression Residuals,” Working paper in Econometrics, Australian National University, Canberra, 40, 1981.

Bollerslev, T. “Generalized Autoregressive Conditional Heteroskedasticity,”Journal of Econometrics, 31, 1986, pp. 307–27.

Duffee, G. R. “Estimating the Price of Default Risk,”Review of Financial Studies, 12, 1999, pp. 197–226.

Escribano, F. “Interest Risk and Default Risk: A Conditional Volatility Study,”International Advances in Economic Research, 9, 1, 2003, pp. 56–63.

Fons, J. S. “Default Risks and Duration Analysis,” in Altman E. I.The High- Yield Debt Market: Investment Performance and Economic Impact, ed., Dow Jones-Irwin, 1990.

Ilmanen, I.; McGuire, D.; Warga, A. “The Value of Duration as a Risk Measure for Corporate Debt,”Journal of Fixed Income, 4, 1, 1994, pp. 70–6.

Longstaff, F. A.; Schwartz, E. S. “A Simple Approach to Valuing Risky Fixed and Floating Rate Debt,”Journal of Finance, 50, 1995, pp. 789–819.

Macaulay, F. R.Some Theoretical Problems Suggested by the Movements of Interest Rates, Bond Yields and Stock Prices Since 1856, New York: National Bureau of Economic Research, 1938.

Nelson, D. B.: “Conditional Heteroscedasticity in Asset Returns,”Econometrica, 59, 1991, pp. 347–70.

Author information

Authors and Affiliations

Additional information

The author would like to acknowledge the financial support provided by Junta de Comunidades grants, PAC 02-001.

Rights and permissions

About this article

Cite this article

Sotos, F.E. Duration and convexity in spanish corporate bonds. International Advances in Economic Research 10, 273–277 (2004). https://doi.org/10.1007/BF02295140

Issue Date:

DOI: https://doi.org/10.1007/BF02295140