Abstract

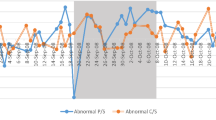

The efficiency of the U.S. market for stock purchase rights is empirically analyzed in an options framework, in which prices of rights, given the prices of underlying stock, are examined with regard to the possibilities of actually earning above-normal profits, considering the risk taken. Two neutral hedging tests for market efficiency, along with a simple buy-and-exercise trading strategy, are applied to daily traded rights data. Results from ex-post hedging tests suggest that the trading strategy based on the rights valuation model is able to differentiate between overpriced and underpriced rights so as to generate substantial book profits. The positive ex-ante hedge return, found to exist empirically, is completely eliminated once transaction costs are introduced, lending support for the efficient U.S. rights offering market on an after-transaction cost basis.

Similar content being viewed by others

References

Bacon, P.W., “The Subscription Price in Rights Offering.” Financial Management 1, 59–64, (1972).

Bae, S.C. and H.Levy, “The Valuation of Stock Purchase Rights as Call Options.” Financial Review 29, 419–440, (1994).

Black, F. and M.Scholes, “The Valuation of Option Contracts and a Test of Market Efficiency.” Journal of Finance 27, 399–418, (1972).

Black, F. and M.Scholes, “The Pricing of Options and Corporate Liabilities.” Journal of Political Economy 81, 637–659, (1973).

Booth, J.R. and R.L.SmithIII, “Capital Raising, Underwriting and the Certification Hypotheses.” Journal of Financial Economics 14, 261–281, (1986).

Constantinides, G.M., “Warrant Exercise and Bond Conversion iin Competitive Markets.” Journal of Financial Economics 13, 371–397, (1984).

Cox, John C. and MarkRubinstein, Options Markets. Englewood Cliffs, NJ: Prentice-Hall, Inc., (1985).

Eckbo, B.E. and R.W.Masulis, “Adverse Selection and the Rights Offer Paradox.” Journal of Financial Economics 32, 293–332, (1992).

Emanuel, D.C., “Warrant Valuation and Exercise Strategy.” Journal of Financial Economics 12, 211–235, (1984).

Galai, D., “The Components of the Return from Hedging Options Against Stocks.” Journal of Business 56, 45–54, (1983).

Goyal, V., C.Y.Hwang, N.Jayaraman, and K.Shastri, “The Ex-Date Impact of Rights Offerings: The Evidence from Firms Listed on the Tokyo Stock Exchanger.” Pacific-Basin Finance Journal 2, 277–291, (1994).

Hansen, R.S., “The Demise of the Rights Issue.” Review of Financial Studies 1, 289–309, (1988).

Hansen, R.S. and J.M.Pinkerton, “Direct Equity Financing: A Resolution of a Paradox.” Journal of Finance 37, 651–665, (1982).

Hansen, R.S., J.M.Pinkerton, and T.Ma, “On the Rightholders' Subscription to the Underwritten Rights Offering.” Journal of Banking and Finance 10, 595–604, (1986).

Heinkel, R. and E.S.Schwartz, “Rights vs. Underwritten Offerings: An Asymmetric Information Approach.” Journal of Finance 41, 1–18, (1986).

Marsh, P., “Equity Rights Issues and the Efficiency of the UK Stock Market.” Journal of Finance 34, 839–862, (1979).

Nelson, J.R., “Price Effects in Rights Offerings.” Journal of Finance 20, 647–650, (1965).

Scholes, M.S., “The Market for Securities: Substitution versus Price Pressure and the Effects of Information on Share Price.” Journal of Business 45, 179–211, (1972).

Smith, C.W., “Alternative Methods for Raising Capital: Rights versus Underwritten Offerings.” Journal of Financial Economics 5, 273–307, (1977).

Author information

Authors and Affiliations

Rights and permissions

About this article

Cite this article

Bae, S.C., Levy, H. Tests of the efficiency of the U.S. rights offering market: An option pricing approach. Rev Quant Finan Acc 6, 259–276 (1996). https://doi.org/10.1007/BF00245184

Issue Date:

DOI: https://doi.org/10.1007/BF00245184