Abstract

Background

The Saudi Healthcare System is universal, financed entirely from government revenue principally derived from oil, and is ‘free at the point of delivery’ (non-contributory). However, this system is unlikely to be sustainable in the medium to long term. This study investigates the feasibility and acceptability of healthcare financing reform by examining households’ willingness to pay (WTP) for a contributory national health insurance scheme.

Methods

Using the contingent valuation method, a pre-tested interviewer-administered questionnaire was used to collect data from 1187 heads of household in Jeddah province over a 5-month period. Multi-stage sampling was employed to select the study sample. Using a double-bounded dichotomous choice with the follow-up elicitation method, respondents were asked to state their WTP for a hypothetical contributory national health insurance scheme. Tobit regression analysis was used to examine the factors associated with WTP and assess the construct validity of elicited WTP.

Results

Over two-thirds (69.6%) indicated that they were willing to participate in and pay for a contributory national health insurance scheme. The mean WTP was 50 Saudi Riyal (US$13.33) per household member per month. Tobit regression analysis showed that household size, satisfaction with the quality of public healthcare services, perceptions about financing healthcare, education and income were the main determinants of WTP.

Conclusions

This study demonstrates a theoretically valid WTP for a contributory national health insurance scheme by Saudi people. The research shows that willingness to participate in and pay for a contributory national health insurance scheme depends on participant characteristics. Identifying and understanding the main influencing factors associated with WTP are important to help facilitate establishing and implementing the national health insurance scheme. The results could assist policy-makers to develop and set insurance premiums, thus providing an additional source of healthcare financing.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

It may be feasible for the government to request that Saudi households bear some of the costs of healthcare. |

If the government cannot finance the increasing costs of healthcare, it may be viable to introduce a national health insurance scheme with affordable premiums. |

There is evidence of the acceptability of healthcare financing reform, especially for the implementation of a national health insurance scheme. |

1 Introduction

The Kingdom of Saudi Arabia (KSA) is a high-income developing country with a landmass of 2,149,690 km2 and a population of 31,742,308 [1]. The vastness of the country impacts the accessibility, quality and equity of healthcare service delivery. Since the discovery of oil in the 1930s, the KSA’s nomadic Bedouin tradition has been replaced by a modern lifestyle similar to that of other highly developed countries. Oil-derived wealth has funded free public-sector services, including healthcare, for all citizens, without collecting taxes or contributions. Oil now accounts for over 90% of the country’s exports and approximately 75% of government revenues [2, 3]; therefore, price fluctuations affect many sectors, including healthcare. To illustrate this, a decline in oil prices caused a fall in GDP per capita in Saudi Arabia from US$14,000 in 1980 to US$7830 in 2002 [4].

Healthcare services are provided through the public sector [including the Ministry of Health (MOH) and other government agencies] and the private sector. The bulk of healthcare service provision in the KSA is undertaken by the public healthcare sector through the MOH, which is funded annually from the total government budget, and runs approximately 60% of hospitals and primary healthcare centres. Recent years have witnessed an effort to improve healthcare services, with a significant increase in the allocated budget, ranging from 5.9% of the government’s total budget in 2006 to 7.0% in 2014 [5]. Baranowski [6] argues that the apparent success of the KSA healthcare system can be attributed to this high level of financing.

Despite the substantial resources that the government is currently able to allocate, the healthcare system is increasingly under strain as a result of the most pertinent challenges faced by all publicly funded healthcare systems—rapid increases in expenditure and demand while resources remain finite. These challenges include: rapid demographic changes, an ageing population, an increase in sedentary lifestyles, rising costs, increasing user expectations, and changing disease patterns [7]. The present situation appears unsustainable in the medium to long term, especially with uncertainties regarding oil prices. The future viability of the current healthcare financing system has therefore been questioned by both academics and international health organizations [8,9,10,11,12,13,14,15].

To reduce the financial burden, the government has implemented Compulsory Employment-Based Health Insurance (CEBHI), which covers all private-sector employees and is paid by their employers. Some researchers have suggested expanding this to cover all citizens [16], whereas others have suggested introducing user fees [17]. The government is also considering shifting towards a national or social-insurance-based system, which could provide a potential solution to some of the country’s current healthcare financing challenges.

Public involvement is believed to be vital to the success of healthcare reforms, and must be considered when designing any healthcare financing system [18]. However, little is known about public preferences and support for healthcare reform in the KSA. According to Mooney [19], “what is needed most fundamentally if healthcare systems are to change and become more socially efficient and equitable is to listen to the informed community voice and to act accordingly”. Hence, using a contingent valuation (CV) method, this study investigated the acceptability of healthcare financing reform in Saudi Arabia, in particular the willingness of Saudis to participate in financing public healthcare services through a contributory national health insurance scheme. It also investigated the willingness to pay (WTP) of those who were willing to participate.

CV is a stated preference method that has been widely used to assess public preferences through eliciting WTP values. It is a hypothetical approach that uses surveys to place economic values on public goods by obtaining information on individual preferences, and to determine what they would be willing to pay for public goods and services when prices are not available [20]. Several studies have been conducted on WTP for health insurance using the CV method in developing and developed countries, including low-, middle-, and high-income countries [21,22,23,24,25,26,27]. However, to the best of the author’s knowledge, no such studies have been conducted in high-income developing countries in the Middle East, in particular countries in the Arabian Gulf region.

This is the first study on the feasibility and acceptability of healthcare financing reform in the KSA, in particular on WTP for a national health insurance scheme. It contributes to knowledge regarding the healthcare financing debate in the KSA and demonstrates evidence of the validity of the CV method to elicit public preferences for financing healthcare. The results could also assist policy-makers to develop and set insurance premiums to provide an additional source of revenue for healthcare services.

2 Methods

2.1 Study Area, Sampling and Setting

A pre-tested interviewer-administered CV questionnaire was used to collect data from heads of households in Jeddah, the country’s second largest city, and its surrounding areas in the Jeddah province of the Mecca region over a 5-month period (October 2014–February 2015). The interviews were conducted in Arabic by a well-trained team of two female and eight male data collectors including the first author (MA). The interviews lasted between 15 and 75 min with an average of 31.4 (± 7.9) min. The sample included participants from urban and suburban areas to obtain a diverse and representative spectrum of citizens’ perspectives.

The individuals involved in the data collection process were postgraduate students and research assistants at King Abdulaziz University in Jeddah City. All individuals involved in the data collection attended a comprehensive training workshop organized by the first author (MA). At the training workshop, the aims and objectives of the research were explained to the data collection team. All questions in the CV questionnaire instrument were discussed. The interviewers were given training in how to conduct the CV questionnaire, and the potential questions that might be raised by respondents during the interviews were discussed. The interviewers read, managed, and completed the questionnaire based on answers provided by the participants in order to accurately record responses, and to make the most efficient use of time.

According to the latest KSA Census, the population of Jeddah and its surrounding areas is estimated at 5,339,660 people, which constitutes 772,151 Saudi households [28]. A larger target sample size will result in greater external validity and better generalizability of the study [29]. Several approaches were triangulated to calculate the minimum sample size and gave broadly comparable results.

The representative target sample size needed to achieve the study objectives and sufficient statistical power was calculated with a sample size calculator [30]. The sample size calculator used a margin of error of ± 4%, a confidence error of 99%, a 50% response distribution, and 772,151 Saudi households, to arrive at a sample size of 1024 participants. Additionally, based on a one-group chi-square test with a 0.05 two-sided significance level and a power of 90%, the minimum required sample size was found to be 1047 participants. Nevertheless, a decision was taken to use a sample of 1250 heads of household to allow for non-usable questionnaires.

To reach the required number of interviews, a total of 2289 heads of household were approached by phone and asked to participate in the study. Of these, 1250 agreed to participate in the study, indicating a response rate of 54.6%. The main reason given for refusing to participate in the study was that they did not have time to be interviewed for 30 min or more. In total, 1187 valid questionnaires were used in the data analysis. The remaining 63 questionnaires were deemed invalid as the information provided was incomplete. This is because some respondents refused to continue the interview, while others refused to provide information on socio-economic characteristics, which were necessary for the analysis.

The sample was selected by a multi-stage sampling procedure. The sampling frame was the primary healthcare centres (PHCs) in Jeddah province–Jeddah city and its surroundings. The PHC network was selected as the sampling frame because all Saudi people are expected to be registered with the PHCs, which act as the gatekeeper for accessing healthcare services [31]. To ensure the sample was representative of the population, Jeddah was divided into five regions: central, west, east, north, and south, from which two PHC centres per region were selected, based on location and the number of registered users. A random selection of users from each PHC was selected, with the sample size being proportional to the size of its catchment population, and potential participants were contacted by phone to arrange interviews at locations convenient to them.

The inclusion criteria for selection were Saudi adults aged 18 and older, and household head. Non-Saudi residents and expatriates were excluded because they are not entitled to access public healthcare services. The survey targeted only heads of household because they are considered the main decision-makers on important matters pertaining to the household. They are responsible for other household members and, in most cases, are the main income-earners in the household, and are the ones who made decisions on household income; all of which would influence the decision on willingness to participate in and contribute to a national health insurance scheme.

2.2 Eliciting Willingness to Pay

The CV questionnaire included sections on information regarding the respondent’s household, use of healthcare services, perceptions of healthcare financing, satisfaction with the quality of public healthcare services, elicitation of willingness to participate and pay, and demographic and socio-economic characteristics. The interviewers explained the aim of the study and the CV method, obtained informed consent, then read, managed, and completed the questionnaire based on answers provided by the participants, to ensure questions were fully understood and responses accurately recorded.

Participants were presented with the following hypothetical scenario:

Following the description of the scenario, respondents were asked about whether they would be willing to participate in a contributory national health insurance scheme and pay a monthly health insurance premium per household member in order to benefit from ensuring the sustainability of the current public healthcare services. This was followed by a double-bounded dichotomous choice with the follow-up elicitation method [32], whereby respondents who were willing to participate and contribute were asked to state the maximum amount they would be willing to pay as a monthly insurance premium per household member. The respondents were reminded about their budget constraints and other expenditure when asked to state the amount they would be willing to pay (Online Appendix A).

2.3 Data Analysis

Tabulations, bivariate and multiple regression analyses were the major data analytic tools used in the study. The number of people who were willing to pay, the mean WTP [with 95% confidence intervals (CIs)] and median WTP (with 25th and 75th percentiles) were computed. Multiple logistic and Tobit regression analyses were conducted to examine the influence of the independent variables on willingness to participate and WTP, and to test the construct (theoretical) validity of the empirical study in order to assess the extent to which the results were consistent with a priori expectations [20]. The specifications and a priori expectations of the independent variables that could influence the willingness to participate and WTP are presented in Table 1.

The Mann–Whitney test was conducted to examine the influence of the continuous independent variables on the willingness to participate, and the chi-square test was conducted to examine the influence of the categorical independent variables on the willingness to participate. Multiple logistic regression was performed for the dichotomous variable to explore factors associated with the willingness to participate and contribute to health insurance. Odds ratios were expressed with 95% CIs. A Tobit regression analysis for limited dependent variables [33] was undertaken to examine the factors associated with the maximum amount that participants were willing to pay.

Data on WTP was skewed to the right, potentially resulting in heteroscedasticity in the regression models. One approach to deal with this is to transform the WTP dependent variable; however, this makes interpreting the regression coefficients difficult because they would no longer be in the same metric as the dependent variable [34]. With continuous data derived from an open-ended WTP question format, the ordinary least squares (OLS) multiple regression is the most commonly used technique to examine factors associated with WTP and assess the construct validity. However, the large number of zero WTP responses called into question the continuity of the dependent variable, and therefore, the use of a standard linear regression model.

OLS estimation fails to account for the qualitative differences between the limit observations (zero WTP) and non-limit observations (positive WTP) [35]. Thus, it is subject to estimation bias and inconsistency in the estimation of the marginal effects [36]. It has been argued that when the nature of the WTP question is continuous with censoring at zero, the most appropriate estimation technique is the limited dependent variable with the Tobit model [35]. This model has also been used in various studies [37,38,39,40].

Tobit regression was conducted to estimate the ‘beta’ coefficients, which explain expected WTP for health insurance and to show how WTP varies with respondents’ socio-economic characteristics. The marginal effects β′ and β″ were estimated where β′ explained the marginal effects for the probability of being uncensored and β″ explained the marginal effects for the expected WTP value conditional on being uncensored: E (WTP | WTP > 0) [41, 42]. All analyses were carried out using STATA SE 14 (StataCorp LP, Texas, USA).

3 Results

3.1 General Descriptive Statistics

3.1.1 Demographic and Socio-Economic Characteristics of the Respondents

Of the total of 1187 respondents, 152 were female (12.8%) and 1035 were male (87.2%). The average age was 39 years, with the oldest being 75 and the youngest being 20. The majority (71.3%) were aged between 25 and 44 years. Of all the participants, 1041 respondents were married (87.7%) and 146 unmarried (12.3%).

The household size ranged from 1 to 15 members, the average being 5. The average education level ‘numbers of schooling years’ was 13.5 years (± 3.5). Respondents were categorized into groups according to their average household income: very low income [< 6000 Saudi Riyal (SR)], low income (6000 SR to < 12,000 SR), moderate income (12,000 SR to < 18,000 SR) and high income (≥ 18,000 SR). For international currency comparison, 1 SR = US$0.27. Two-hundred and sixteen (18.2%) were within the very low-income range, 460 (38.8%) within the low-income range, 348 (29.3%) within the moderate-income range and 163 (13.7%) within the high-income range.

Almost two-thirds of the sample (62.1%) reported that none of the household members suffered from chronic diseases, compared with 37.9% who reported that either they or a family member did. ‘Travel time to the public healthcare facility’ and ‘obstacles to obtain healthcare services’ variables were used as proxies for healthcare access. On average, respondents’ travel time to the public healthcare facility was 21.4 min (± 10.1), with the minimum being 5 min and the maximum 90 min. When asked whether any household members had ever been unable to have the recommended medical care at public healthcare facilities, 214 respondents (18.0%) stated they had, i.e. they had experienced obstacles to access public healthcare services, including a lack of hospital beds, lack of specialist physicians, long waiting times to access services, and referral reasoning.

Regarding satisfaction with healthcare services, 598 respondents (50.4%) were not satisfied with the quality of public healthcare services, whilst 49.6% were. Regarding perception about financing healthcare services, only 16.6% believe that service users should participate in and contribute to healthcare financing, while the remainder believe it is the responsibility of government or employers. Of the total sample, 116 respondents had private health insurance which allowed them to access private healthcare services in addition to their access to public healthcare services.

3.1.2 Willingness to Participate and Pay

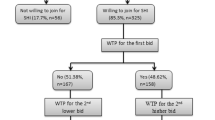

Over two-thirds (69.6%) of the respondents were willing to participate in and financially contribute to a national health insurance scheme to ensure the sustainability of public healthcare services if the government is no longer able to finance them and therefore decided to implement such an insurance scheme.

Table 2 shows the frequency distribution and factors associated with the willingness to participate under the assumption of paying the premium for national health insurance. It was found that location, marital status, household size, chronic disease, satisfaction, financing responsibility, education and income were all statistically significant at 0.01%.

People living in urban areas were more willing to participate and pay an insurance premium for the proposed national health insurance scheme. Of these, 71.1% were willing to participate as compared with 53.4% in suburban or rural areas. Married respondents were more willing to participate than unmarried respondents. Respondents in larger households were less willing to participate than those in smaller households. Respondents who were satisfied with the quality of public healthcare services were more willing to participate than those who were not. Respondents with increasing income were more willing to participate. Of those households with very low incomes (< 6000 SR), only 49.1% were willing to participate, compared with 82.8% of households with the highest incomes.

Following the question about whether the participants were willing to participate in a contributory national health insurance scheme in order to benefit from the sustainability of public healthcare services, the participants who responded “yes” were asked to state the maximum amount they would be willing to pay for each household member. The estimated mean WTP for the full sample was 49.62 SR (95% CI 46.6–52.7), while the median was 50 SR (25th and 75th percentiles; 0–100).

3.2 Econometrics Analysis

3.2.1 Willingness to Participate in a Contributory National Health Insurance Scheme

The multiple logistic regression model was performed (Table 3) to assess the construct validity and explore the determinants of the willingness to participate. The results can be analysed in terms of the construct validity, that is, whether the directionalities of correlations were in line with theory in terms of the significance of the explanatory variables and their odds ratios. Willingness to participate and financially contribute was positively and significantly influenced by location, satisfaction, financing responsibility, education and income. On the other hand, willingness to participate was negatively and significantly influenced by household size and ownership of private health insurance.

The results show that the odds ratios for the positive significant variables were greater than one, suggesting that respondents with these characteristics were more likely to be willing to participate. The odds ratio for households in urban areas was almost 1.64 (suggesting that they were 1.6 times more likely to be willing to participate and contribute). The odds ratio for respondents reporting satisfaction with the quality of healthcare services was almost 1.67, indicating that respondents who are satisfied with public healthcare services are almost 1.7 times more likely to be willing to participate in a contributory national health insurance scheme.

It was expected that there would be a positive relationship between willingness to participate and income. The estimated coefficients for all income ranges were positive and statistically significant. This suggests that as income increases so does willingness to participate. The odds ratios were almost 1.75 for households within the low-income range (suggesting that they were almost 1.8 times more likely to be willing to participate than those within the very low-income range), almost 3.23 for moderate-income households and almost 4.36 for households that were within the high-income range.

Conversely, for household size and ownership of private health insurance, the odds ratios were less than one, suggesting that respondents with these characteristics were less likely to be willing to participate. The estimated coefficient of the household size variable was significant at p < 0.001, indicating that compared with smaller households, larger households were less likely to participate. Households having private insurance were also less likely to participate (p < 0.05), with an odds ratio of 0.59, suggesting that the willingness to participate was almost 0.41 times lower for households with private insurance than those without.

3.2.2 Willingness to Pay for a Contributory National Health Insurance Scheme

The results of the Tobit regression analysis are presented in Table 4, and the marginal effects are calculated in Table 5. Table 5 shows that in accordance with a priori expectations and theoretical predictions, all income ranges and education were significantly associated with WTP, suggesting that the probability that a household within the low-income range would be willing to pay to ensure healthcare sustainability was 0.13 greater than a household within the very low-income range. Moreover, those having a low household income level were willing to pay approximately 13 SR per household member more than those having a very low household income level in order to ensure the sustainability of public healthcare services. The probability that households within the moderate- and high-income ranges would be willing to pay was, respectively, 0.27 and 0.32 greater than households within the very low-income range. Moreover, they were willing to pay approximately 32 SR and 62 SR more, respectively, as a monthly health insurance premium per household member than those having a very low household income level in order to ensure the sustainability of public healthcare services. All the results were significant at p < 0.001.

The education variable also had a positive coefficient in the Tobit regression. Results indicate that household heads with more education, i.e. more years of schooling, had a higher probability to state a positive WTP and were willing to pay more in order to ensure the sustainability of the current healthcare services (p < 0.01). The household size had a negative coefficient in the Tobit model, suggesting that larger households had a lower probability of stating a positive WTP of 0.21 with significance at the 0.001 level.

Perceptions as to who should finance the healthcare system were also found to be significant at p < 0.01. Particularly those who thought that it is not purely the government’s responsibility and that users of public healthcare services should financially contribute, were willing to pay approximately 14 SR more than those who believe it is solely the government’s responsibility. Those respondents reporting satisfaction with the quality of public healthcare services had a higher probability of 0.06 (p < 0.001) of stating a positive WTP. They were also willing to pay approximately 5 SR more than respondents who were dissatisfied.

4 Discussion

In the KSA, people are used to having free public services including healthcare services. Hence, the population’s support and willingness to participate and financially contribute to a particular financing scheme, in this case health insurance, is likely to have a strong influence on the success of the insurance implementation and its sustainability. Thus, understanding the viability of such a scheme requires detailed information gathered from an investigation of people’s willingness to participate in and pay for the scheme.

Overall, a high percentage of the respondents were willing to participate in and pay for a contributory national health insurance scheme, assuming that the government can no longer finance the services currently provided from oil-based revenues. The results show that the willingness to participate in and pay for a contributory national health insurance scheme depends on respondents’ characteristics. Identifying and understanding the main influencing factors associated with the willingness to participate and pay would help to facilitate the establishment and implementation of a national health insurance scheme. Similar determinant factors influenced both the willingness to participate decision (logistic model) and the maximum amount that households would be willing to pay (Tobit model), with the exception of location and private insurance ownership. These variables were exclusively statistically significant at p < 0.05 in the logistic model and influenced the participation decision only.

The results indicated that urban dwellers tended to be more willing to pay than those in suburban and rural areas. This may be because healthcare facilities in urban areas are often more advanced, equipped with the latest medical technology, and typically provide all levels of care including specialist healthcare services, as compared with those in suburban and rural areas. Moreover, although having the same expected negative sign in both the logistic and Tobit models, the ‘ownership of private health insurance’ seems to influence only the decision to participate in a contributory national health insurance scheme. This indicates that households having private health insurance are less willing to participate and incur premium costs if a contributory national health insurance scheme is to be implemented. A possible interpretation is that because they have private health insurance, they can access private healthcare services without needing to access public healthcare services.

Based on a priori expectations, it was difficult to predict the influence of household size on willingness to participate. Household size showed a significant negative effect on the decision to participate and on the maximum amount of money participants are willing to pay, contrasting with arguments that as household size increases, the likelihood of having greater access to cash and the likelihood of using healthcare services is higher and, therefore, willingness to participate and pay would be higher to avoid future health expenses should public provision cease [43,44,45]. The observed negative relationship was consistent with arguments that as household size increases, the head of household would be willing to pay less money per member compared with smaller households within the same income range because disposable income is lower [21, 22, 46]. The rationale for this is that the heads of larger households would have to pay a larger health insurance premium to cover each member in the household.

This result of the household size influence depended on the framing of the valuation scenario, which explained to the participants that they would pay the national health insurance premium for each household member if they decided to participate in a contributory national health insurance scheme. Different results may have been produced if the scenario had been constructed in a different way; for example, one that considered an insurance premium for the family as a ‘family package’ regardless of household size or one describing an insurance policy that states the number of members the health insurance scheme would cover.

The results also showed that the belief that healthcare financing should be a joint responsibility had a significant impact, with those who believed this tending to be more willing to participate and pay compared with those who did not. This finding is perhaps to be expected when considering the KSA’s long history of providing free public services to citizens, including healthcare services, without financial contribution or taxation from the public. This long history is expected to be a barrier that discourages many people from accepting the idea of contributing to the financing of healthcare services (i.e. people have become accustomed to the status quo and might be resistant to change). Similar results were also found in a study conducted in Sudan by Habbani et al. [47] to investigate the WTP for public health services if these services are of good quality.

Highly educated respondents were more willing to participate and pay, perhaps because of a greater awareness of health-related issues, and therefore a greater appreciation for the value of public healthcare services and the potential benefits derived from participating in such a health insurance scheme. They may also have the information and knowledge needed to assess the decision-making process on the proposed contributory national health insurance scheme [43]. This finding is in agreement with several studies that have found a positive relationship between education and willingness to participate in and pay for health insurance [25, 26, 46, 48,49,50].

Overall, the results of the logistic and Tobit regression analyses were consistent with a priori expectations, and the estimated results were in line with theoretical predictions. As expected, all levels of income were statistically significant in both logistic and Tobit models. Theory would suggest that households are more willing to participate in and pay for health insurance as household income increases. Since health is widely considered as a normal good, therefore, as household income increases, there is a greater probability that households are willing to participate in and pay for health insurance. This finding is in agreement with previous studies that have found a positive relationship between income and willingness to participate in and pay for health insurance [23, 26, 44, 51], further supporting the construct validity of the CV method used in this study.

There were, however, some unexpected results. Although not statistically significant, the estimated coefficient of ‘chronic diseases’ was negative in both models. It was expected that households with members who suffered from chronic diseases would be more likely to be willing to participate in, and pay for, a contributory national health insurance scheme in order to ensure the sustainability of public healthcare services because they may require healthcare services more frequently than households without members with chronic disease. This contradicts a finding relating to health insurance in Vietnam by Lofgren et al. [46] who found higher WTP for households with at least one member with a chronic disease. One possible explanation for our finding might be that households with a chronically sick person might be under financial and other strains, which are not captured by income levels.

Overall, the findings suggested that if the government cannot finance the increasing costs of healthcare, it may be viable to introduce a national health insurance scheme with affordable premiums. The findings also provided evidence of the acceptability of healthcare financing reform, especially for the implementation of a national health insurance scheme. These empirical findings support the importance of sustaining public healthcare services to the Saudi people and suggest it may be feasible for the government to request that households bear some of the costs. The results can help the government to set insurance premiums and provide strategic information to help promote maximum participation by the Saudi people.

The CV questionnaire used in this study was developed in accordance with internationally recognised design and methodological standards [32, 52]. The survey administration, the information provided to respondents, the selection of the elicitation method and the payment vehicle, the reminder to participants to consider their disposable income and other obligations and expenditure in the WTP question were given particular attention.

The contingent valuation method is mainly criticized because of the potential biases associated with it. That being said, it is argued that eliminating the associated biases with the contingent valuation method yields valid and reliable results. This study attempted to eliminate the hypothetical bias that can threaten the validity of the contingent valuation technique [20]. A hypothetical bias refers to the extent to which respondents find the valuation scenario realistic, understandable, and believable. In this study, the valuation scenario was realistic and believable in the sense that a simple scenario was provided and that respondents were asked about the recommended insurance-based approach rather than a user-based (i.e. user fees) approach [32, 53]. The insurance-based approach was preferred over the user-based approach, because the respondents were familiar with the insurance system, together with the fact that there was a high level of rejection of the user-based approach during the testing stage of the CV design process.

4.1 Study Limitations

The hypothetical scenario presented to participants can be perceived by different respondents differently, depending on respondents’ past experience of health service utilization from the existing system. This variation in understating about the services of the scheme might influence the WTP estimate. However, the study focuses on the sustainability of the healthcare system and the interviewees explained that aim clearly to the respondents. Moreover, as a result of budget and time constraints, the study sample was selected from Jeddah city and its surrounding areas. This might raise the question of the validity of extrapolating the results to the entire country. The study tried to minimize the effects of this limitation by using a multi-stage sampling procedure which selected participants from different areas in and around Jeddah to reflect population diversity. Nevertheless, further research covering the different regions and provinces of the country to attain more representative results would be warranted to produce a nationally representative result. Moreover, the study sample is relatively skewed towards the male gender, which might raise the question of sample bias. However, this study was conducted at a household level, and for cultural and religious reasons, the heads of household in Saudi Arabia tend to be male, and responsible for household members. Nevertheless, the voices of women were represented in this study.

5 Conclusions

In conclusion, this study contributes to knowledge on the healthcare financing debate in the KSA and demonstrates evidence of the validity of the CV method to elicit public preferences for financing healthcare services, particularly in the KSA context, where the public does not currently pay or contribute. Other Arabian Gulf countries are similar in culture, background, religion, their method of financing healthcare and the challenges they face. Therefore, the results of this study may also be transferable to healthcare reform in these countries.

Data Availability Statement

The datasets generated during and/or analysed during the current study are not publicly available due to privacy, confidentiality and other restrictions, but are available from the corresponding author (MA) on reasonable request.

References

General Authority for Statistics. 2017. https://www.stats.gov.sa/en. Accessed 23 May 2017.

Forest J, Sousa M. Oil and terrorism in the New Gulf: framing US energy and security policies for the Gulf of Guinea. Lanham: Lexington Books; 2006.

Alshehry AS, Belloumi M. Energy consumption, carbon dioxide emissions and economic growth: the case of Saudi Arabia. Renew Sustain Energy Rev. 2015;41:237–47.

Walston S, Al-Harbi Y, Al-Omar B. The changing face of healthcare in Saudi Arabia. Ann Saudi Med. 2008;28:243–50.

MOH (2014) MOH statistics book [online]. http://www.moh.gov.sa/en/Ministry/Statistics/book/Pages/default.aspx. Accessed 4 Dec 2017.

Baranowski J. Health systems of the world: Saudi Arabia. Glob Health. 2009;2:1–8.

Walshe K, Smith J. Introduction: the current and future challenges of healthcare management. In: Walshe K, Smith J, editors. healthcare management. Buckingham: The Open University Press; 2011. p. 1–10.

Mufti MH. Healthcare development strategies in the Kingdom of Saudi Arabia. New York: Springer Science & Business Media; 2000.

World Health Organization. Country cooperation strategy for WHO and Saudi Arabia, 2006–2011. New York: World Health Organization; 2006.

Jannadi B, Alshammari H, Khan A, Hussain R. Current structure and future challenges for the healthcare system in Saudi Arabia. Asia Pac J Health Manag. 2008;3:43–50.

Alsharqi OZ, Abdullah MT. “Diagnosing” Saudi health reforms: is NHIS the right “prescription”? Int J Health Plan Manag. 2012;28:308–19.

Al Salloum NA, Cooper M, Glew S. The development of primary care in Saudi Arabia. InnovaiT Educ Inspir Gen Pract. 2015;8:316–8.

Elachola H, Memish ZA. Oil prices, climate change-health challenges in Saudi Arabia. Lancet. 2016;387:827–9.

Al-Hanawi MK, Alsharqi OZ, Almazrou S, Vaidya K. Healthcare Finance in the Kingdom of Saudi Arabia: a qualitative study of householders’ attitudes. Appl Health Econ Health Policy. 2017. https://doi.org/10.1007/s40258-017-0353-7.

Al-Hanawi MK. The healthcare system in Saudi Arabia: How can we best move forward with funding to protect equitable and accessible care for all? Int J Healthc. 2017;3(2):78–94.

Almalki M, FitzGerald G, Clark M. Health care system in Saudi Arabia: an overview. East Mediterr Health J. 2011;17(10):784–93.

Mufti MH. A case for user charges in public hospitals. Saudi Med J. 2000;21(1):5–7.

Balabanova D, McKee M. Reforming health care financing in Bulgaria: the population perspective. Soc Sci Med. 2004;58(4):753–65.

Mooney GH. Economics, medicine and health care. London: Financial Times Prentice Hall; 2003.

Mitchell RC, Carson RT. Using surveys to value public goods: the contingent valuation method. Washington, DC: Resources for the Future; 1989.

Asenso-Okyere WK, Osei-Akoto I, Anum A, Appiah EN. Willingness to pay for health insurance in a developing economy. a pilot study of the informal sector of Ghana using contingent valuation. Health Policy. 1997;42(3):223–37.

Dror DM, Radermacher R, Koren R. Willingness to pay for health insurance among rural and poor persons: field evidence from seven micro health insurance units in India. Health Policy. 2007;82(1):12–27.

Barnighausen T, Liu Y, Zhang X, Sauerborn R. Willingness to pay for social health insurance among informal sector workers in Wuhan, China: a contingent valuation study. BMC Health Serv Res. 2007;7:114.

Onwujekwe O, Okereke E, Onoka C, Uzochukwu B, Kirigia J, Petu A. Willingness to pay for community-based health insurance in Nigeria: do economic status and place of residence matter? Health Policy Plan. 2010;25(2):155–61.

Bock JO, Heider D, Matschinger H, et al. Willingness to pay for health insurance among the elderly population in Germany. Eur J Health Econ. 2016;17(2):149–58.

Adams R, Chou YJ, Pu C. Willingness to participate and Pay for a proposed national health insurance in St. Vincent and the grenadines: a cross-sectional contingent valuation approach. BMC Health Serv Res. 2015;15:148.

Chanel O, Makhloufi K, Abu-Zaineh M. Can a circular payment card format effectively elicit preferences? Evidence from a survey on a mandatory health insurance scheme in Tunisia. Appl Health Econ Health Policy. 2017;15(3):385–98.

Salam AA, Elsegaey I, Khraif R, Al-Mutairi A. Population distribution and household conditions in Saudi Arabia: reflections from the 2010 Census. SpringerPlus. 2014;3(1):530.

Cavana RY, Delahaye BL, Sekaran U. Applied business research: qualitative and quantitative methods. Milton: John Wiley & Sons Australia; 2001.

Raosoft. Sample size calculator. http://www.raosoft.com/samplesize.html. Accessed 22 Feb 2014.

Al-Hamdan N, Kutbi A, Choudhry A, Nooh R, Shoukri M, Mujib S. WHO stepwise approach to NCD surveillance country-specific standard report Saudi Arabia, WHO Stepwise Approach. Geneva: WHO; 2005.

Arrow K, Solow R, Portney P, Leamer E, Radner R, Schuman H. Report of the NOAA panel on contingent valuation. Washington, DC: National Oceanic and Atmospheric Administration; 1993.

Tobin J. Estimation of relationships for limited dependent variables. Econometrica. 1958;26(1):24–36.

Manning WG. The logged dependent variable, heteroscedasticity, and the retransformation problem. J Health Econ. 1998;17(3):283–95.

Donaldson C, Jones AM, Mapp TJ, Olson JA. Limited dependent variables in willingness to pay studies: applications in health care. Appl Econ. 1998;30(5):667–77.

Greene WH. Econometric analysis. New York: Prentice Hall; 2003.

Whitehead JC, Hoban TJ, Clifford WB. Measurement issues with iterated, continuous/interval contingent valuation data. J Environ Manag. 1995;43(2):129–39.

Awunyo-Vitor D, Ishak S, Seidu Jasaw G. Urban households’ willingness to pay for improved solid waste disposal services in Kumasi metropolis, Ghana. Urban Stud Res. 2013;2013:1–8.

Mataria A, Donaldson C, Luchini S, Moatti J-P. A stated preference approach to assessing health care-quality improvements in Palestine: from theoretical validity to policy implications. J Health Econ. 2004;23(6):1285–311.

Ghorbani M, Hamraz S. A survey on factors affecting on consumer’s potential willingness to pay for organic products in Iran (a case study). Trends Agric Econ. 2009;2(1):10–6.

McDonald JF, Moffitt RA. The uses of Tobit analysis. Rev Econ Stat. 1980;62(2):318–21.

Ekstrand C, Carpenter TE. Using a tobit regression model to analyse risk factors for foot-pad dermatitis in commercially grown broilers. Prev Vet Med. 1998;37(1):219–28.

Mathiyazhagan K. Willingness to pay for rural health insurance through community participation in India. Int J Health Plan Manag. 1998;13(1):47–67.

Kuwawenaruwa A, Macha J, Borghi J. Willingness to pay for voluntary health insurance in Tanzania. East Afr Med J. 2012;88:54–64.

Adebayo EF, Uthman OA, Wiysonge CS, Stern EA, Lamont KT, Ataguba JE. A systematic review of factors that affect uptake of community-based health insurance in low-income and middle-income countries. BMC Health Serv Res. 2015;15:543–55.

Lofgren C, Thanh NX, Chuc NT, Emmelin A, Lindholm L. People’s willingness to pay for health insurance in rural Vietnam. Cost Eff Resour Alloc. 2008;6:16.

Habbani K, Groot W, Jelovac I. Household health-seeking behaviour in Khartoum, Sudan: the willingness to pay for public health services if these services are of good quality. Health Policy. 2006;75:140–58.

Bawa SK, Ruchita M. Awareness and willingness to pay for health insurance: an empirical study with reference to Punjab India. Int J Humanit Soc Sci. 2011;1:100–8.

Babatunde OA, Akande T, Salaudeen A, Aderibigbe S, Elegbede O, Ayodele L. Willingness to pay for community health insurance and its determinants among household heads in rural communities in north-central Nigeria. Int Rev Soc Sci Humanitie. 2012;2:133–42.

Ahmed S, Hoque ME, Sarker AR, Sultana M, Islam Z, Gazi R, Khan JA. Willingness-to-pay for community-based health insurance among informal workers in URBAN Bangladesh. PLoS One. 2016;11:e0148211.

Chen WY, Lee JL, Liang YW, Hung CT, Lin YH. Valuing healthcare under Taiwan’s national health insurance. Expert Rev Pharmacoecon Outcomes Res. 2008;8(5):501–8.

Venkatachalam L. The contingent valuation method: a review. Environ Impact Assess Rev. 2004;24(1):89–124.

O’Brien B, Gafni A. When do the “dollars” make sense? Toward a conceptual framework for contingent valuation studies in health care. Med Decis Mak. 1996;16(3):288–99.

Acknowledgements

We are grateful to all respondents who participated in this study, and we appreciate the unconditional support of Anderson Loundou during the data analysis. Our thanks are also due to the anonymous referees for their comments and suggestions that helped to produce the paper in its current format.

Author information

Authors and Affiliations

Contributions

MA conceived the idea, designed the study, and analysed and interpreted the data under supervision from KV as part of MA’s PhD thesis. MA drafted the first draft of the paper. OA and OO reviewed and suggested the structure of the manuscript. All authors contributed to revisions of the manuscript and approved the final version of the manuscript prior to its submission. MA is the overall guarantor for this work.

Corresponding author

Ethics declarations

Funding

This work is supported by King Abdulaziz University, Jeddah, Saudi Arabia in the form of a PhD scholarship for MA.

Informed consent

Consent was secured from all the respondents who participated in the study.

Conflict of interest

Mohammed Khaled Al-Hanawi, Kirit Vaidya, Omar Alsharqi, Obinna Onwujekwe declare that they have no conflict of interest.

Ethical approval

All procedures performed in studies involving human participants were in accordance with the ethical standards of the institutional and/or national research committee and with the 1964 Helsinki declaration and its later amendments or comparable ethical standards. This research study has been reviewed and given a favourable opinion by Aston University Research Ethics Committee. The study was designed and conducted in accordance with the ethical principles established by Aston University. In addition to Aston University ethical approval, the study has also received ethical approval from the MOH in Saudi Arabia.

Electronic supplementary material

Below is the link to the electronic supplementary material.

Rights and permissions

Open Access This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 International License (http://creativecommons.org/licenses/by-nc/4.0/), which permits any noncommercial use, distribution, and reproduction in any medium, provided you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made.

About this article

Cite this article

Al-Hanawi, M.K., Vaidya, K., Alsharqi, O. et al. Investigating the Willingness to Pay for a Contributory National Health Insurance Scheme in Saudi Arabia: A Cross-sectional Stated Preference Approach. Appl Health Econ Health Policy 16, 259–271 (2018). https://doi.org/10.1007/s40258-017-0366-2

Published:

Issue Date:

DOI: https://doi.org/10.1007/s40258-017-0366-2