Abstract

In the present contribution, the innovative nonlinear state marginal price vector model introduced in Toll and Kintzel (CEJOR 27(4):1079–1105, 2019) (plus Errata herein) is enriched to include budgeting problems under agency conflicts. Under asymmetric information, a company owner as principal can only rely on information transmitted to her from her managers as agents. In the related modeling, it is assumed that slack and capital rationing are optimal. The governing budgeting relations are integrated into a nonlinear framework furnished by a multi-period newsvendor approach and are solved numerically by means of a two-step valuation procedure based on two successive nonlinear convex optimizations. The capital market is assumed to be imperfect. As case study, the M&A-valuation case of a merger of two IT-service companies is considered subjected to optimal combined dimensioning of capacities and budgets under stochastic demand. On balance, by addressing agency conflicts within the well-established nonlinear framework, the practical application field of the valuation procedure is widened.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

In the framework of M&A’s, acquisitions or sales of whole companies or distinct business units are in the center of considerations. For this purpose, to value companies or business units, a reliable and valid valuation procedure is required (Matschke et al. 2010; Brösel et al. 2012; Matschke and Brösel 2013). Broadly speaking, in valuation theory, it is distinguished between market-oriented and investment-oriented valuation procedures. In market-oriented approaches, the principle of objectivity is of great importance relying on common market prices or derived values based on market prices of other entities traded in a market, which are valid and similar for all market participants. In contrast, the principle of subjectivity lies at the core of investment-oriented approaches. Market-oriented models are based on the assumption of freedom of arbitrage in an ideal market equilibrium and the related rule of value additivity. Consequently, a more or less subjective value can only be reached by adding a number of supplementary premiums, which gives a huge leeway for discretion. In contrast, subjective decision fields and a number of relevant financial and real-economical interrelationships can be taken into account in investment-oriented models, which result in values which may be more relevant from the perspective of a valuation subject. Here, the concept of a marginal price is crucial, which can be determined in a state of indifference between feasible contiguous comparative valuation states.

In the current publication, we make use of the valuation procedures of Hering (2000) and Toll (2010). Here, the marginal price is computed by means of two optimization approaches, the so-called base and valuation approaches, which furnish two viable comparative valuation states. In a base approach as reference state, a situation is considered, before a transaction has actually been realized. In a subsequent valuation approach, the valuation object, which is in the focus of interest, is integrated into the investment and financing program in return for a certain compensation to be paid, which may be given as upfront payment paid at the beginning of the planning period, meaning at the moment of transfer of ownership of the valuation object, or as a certain structured price stream. Unter the constraint that the target values are comparable, the marginal price is the critical price for a valuation object in question which gives the same degree of satisfaction in terms of target values. Thus, by means of two optimization approaches, without and with inclusion of a valuation object, the marginal price can be determined as the critical price at which a certain valuation subject as valuation addressee becomes indifferent.

The original model of Hering (2000) was invented on the basis of the ideas of Weingartner (1963), Hax (1964), Jaensch (1966), Laux and Franke (1969) and Matschke (1975). It was formulated as linear programming problem according to Hax and Weingartner based on two successive linear optimizations, the above-mentioned base and valuation approaches. In the primal formulations of both optimization approaches, the primal variables are determined. In the related dual formulations, the dual variables are determined like endogenous marginal interest rates or other shadow prices associated with the primal programming problem. Since both optimization approaches are solved more or less independently from each other except for some coupling constraints (to reach a common target value, for instance), a basis change can occur and, thus, a restructuring among the investment and financing objects, which may change the marginal interest rates. What can be said definitely is that the marginal price must lie within a certain interval bounded by upper and lower bounds reflecting the present values of earnings of a valuation object discounted by means of marginal discount factors of the base and valuation program, respectively, particularly in the valuation case of a purchase and vice versa in the valuation case of a sale. According to Hering (2000), this valuation procedure was called state marginal price model. In Toll (2010), a price vector was introduced to yield a marginal price stream as compensation providing the advantage of higher flexibility. In Toll and Kintzel (2019), the latter model was reformulated and recast in a nonlinear setting. The main motivation was the consideration of nonlinear synergy effects as suggested by Pfaff et al. (2002). The main result was a supplementary nonlinear arbitrage value term, which cannot be described by a mere basis change among investment and financing objects, but which is the result of arbitrage related to nonlinear convex programming. Finally, the so-called nonlinear state marginal price vector model was applied to the practical case study of a merger of two IT-service companies, whose capacities were optimized by employing a newsvendor model.

The approaches of Hering (2000), Toll (2010) as well as Toll and Kintzel (2019) allow, in contrast to usual market-oriented approaches, the consideration of subjective decision and action fields, meaning the consideration of a number of diverse and relevant certain or uncertain, risky or unrisky investment and financing objects as embedding action space of financial opportunities or liabilities at the disposal of a valuation subject as valuation addressee, who, in addition, may have individual targets based on individual consumption spending preferences. The complete model is eventually solved by means of simultaneous total optimization, which is reliant on well-posed and proper formulations of base and valuation approaches. Stochastic effects can be taken into account by applying a simulative risk analysis in a staggered approach. Concluding, it is possible to take a wide range of diverse model assumptions into account, which are not prone to the same extent of ambiguities in discretion as it is usually the case in market-oriented approaches, in which, moreover, decisions within the investment and financing areas and their related optimal investment and financing programs are normally treated as independent, which is too restrictive since in imperfect capital markets the Fisher separation theorem doesn’t hold (Fisher 1930).

The purpose of the present paper is to extend the model presented in Toll and Kintzel (2019) by agency conflicts based on the publications Mayer et al. (2005), Inwinkl and Schneider (2008) and Inwinkl et al. (2009), which introduces a further relevant source of nonlinearity into the model. Agency conflicts can occur if a company owner as principal cannot verify the truth behind information transmitted to her from her managers as agents. Because of asymmetric information, managers have an information advantage. Clearly, they know the true costs for an investment project, but are inclined to overstate costs toward head office to build up slack for themselves, which leads to increased budgets for cost allocation to be able to receive certain privileges like expensive or fancy equipment, noble company cars, certain benefits, etc. To face the problem of asymmetric information on the side of the owner, those additional costs due to agency conflicts must be considered within the optimization procedure. Thereby, it is assumed that managers strive to maximize slack for themselves and that a company owner likes to maximize company profits on the basis of hurdle rates signaled to her by her managers under consideration of her favourite consumption spending preferences like wealth or income maximization, for instance (Fig. 1).

Historic timeline of the agency relationship between manager and company owner

The modeling of agency conflicts is based on the original works of Antle and Eppen (1985) and Falee et al. (1996). In Antle and Eppen (1985), capital rationing problems and organizational slack in capital budgeting were discussed. It was found out that the cut-off or hurdle rate of a project reported by managers under presence of asymmetric information is of higher relevance for decision-making than the mere market rate of interest. First-best and second-best solutions were analyzed and the truth-telling condition as constraint was established. In Falee et al. (1996), agency conflicts were solved analytically for a single investment project in the framework of a single-period and a two-period model and related optimality conditions were derived. It was found out that the first-best solution overestimates utility for a company owner under presence of asymmetric information. In both works, it was stated that slack as well as capital rationing are optimal. This proposition is supported by empirical studies (Cyert and March 1963; Schiff and Lewin 1968; Poterba and Summers 1995). However, the integration into a multi-period framework or a combined consideration among other investment projects was not realized, probably owing to the complexity of the resulting equation system.

In Inwinkl and Schneider (2008) and Inwinkl et al. (2009), the mentioned conceptions were revisited, reformulated and integrated into the linear state marginal price model of Hering (2000), but only visionary and without concrete application. In Inwinkl and Schneider (2008), a one-sided agency conflict was addressed, meaning a single manager is responsible for an investment project and reports to a company owner, a problem which is considered also in the present contribution. In Inwinkl et al. (2009), a more complex double-sided agency conflict was in the focus of interest based on the preliminary insights in Mayer et al. (2005), in which the theoretical groundwork was laid. In a double-sided agency conflict, an investment project is controlled by two managers who like to maximize slack independently from each other. In both publications, the equations were solved analytically and were integrated en bloc into the linear state marginal price model of Hering (2000). However, a clear numerical strategy for the integration of more general problems under asymmetric information was still lacking. This shortcoming shall be remedied in the present publication, in which agency conflicts are considered in a multi-period general format and within a sound nonlinear framework.

In contrast to the former works, in the present paper, the equations are not integrated in analytical form into the nonlinear framework, but are solved numerically. For this purpose, the case study of a merger of two IT-service companies considered in Toll and Kintzel (2019) is once again taken as prototype example. As budgeting problem, it is assumed that the budgets B(c) resp. \(B(c^*)\) relate to the overstated cost \(c^*\) reported by a manager. Thereby, we assume that the variable cost term \(c \, Q\) within the profit term P(Q) of the newsvendor model is subjected to agency conflicts, i.e. \(P(Q,c^*)\). A multi-period approach is addressed and a numerical solution of the simultaneous optimization problem of the complete equation system is accomplished. Practically, the first-best solution corresponds to the approach already presented in Toll and Kintzel (2019). The second-best solution is addressed in the current publication.

The current work is structured as follows: At first, a simple single-period budgeting problem is explained in the framework of a single-period optimization approach considered in isolation whereby the simplifying assumption of a single investment project with earnings e(c) and cost c is made. Subsequently, this model is integrated consistently into a single-period newsvendor approach according to Toll and Kintzel (2019). Then, we review the fundamentals of the nonlinear state marginal price vector model briefly. Afterward, we propose a multi-period simultaneous planning approach in the framework of formulations of base and valuation approaches whereby we make reference to the exemplary case of a merger of two IT-service companies according to Toll and Kintzel (2019). With the parameters chosen therein, the multi-period valuation model is calibrated and solved numerically. The result of the second-best solution is eventually compared with the first-best solution already addressed in Toll and Kintzel (2019) and is discussed briefly. As in the first-best solution, we make in the current enriched model the simplifying assumption of risk-neutrality as well, i.e. we maximize wealth resp. end value by assuming a risk-neutral valuation subject. The extension to a risk-averse attitude of a valuation subject will be the subject of a forthcoming paper.

2 A simple single-period budgeting problem under agency conflicts

As realistic assumption, the goal of managers in budgeting processes of investment projects is to maximize personal utility and to optimize slack for themselves. If a company owner does not know the true costs of a project, she can only plan on the basis of costs reported by her manager. It is assumed that both the company owner and the manager know the true earnings e(c), which is assumed to be flat, i.e. \(e(c) = e\). But only the manager knows the true cost c. However, the manager is inclined to report an overstated cost \(c^*\). As best guess, the company owner must assume in her planning that the manager strives to maximize slack in the framework of a given decision field. Thus, on the side of head office the following optimization problem is to be solved for a single investment project, compare Inwinkl and Schneider (2008):

subject to

Hence, the true cost lies somewhere within the interval \([{\underline{c}},{\overline{c}}]\) and the costs are distributed according to a probability distribution function f(c). The truth-telling constraint (TT), also known as revelation condition, guarantees that the manager likes to report truthfully, meaning in agreement with true budget conditions and project specifications. The resource feasibility constraint (RF), also known as participating condition, tells us that slack must be positive. Hence, the manager only wants to carry out a project if it guarantees her a certain slack. In a first step, we simplify the model by assuming the budget to be straightly linear, i.e. \(B(c) = c^* \, I(c)\) in dependence on the cost \(c^*\) reported by the manager. Furthermore, to fulfill the constraints in any case, we define the project indicator function I(c) as follows:

In agreement with the latter assumptions, the optimization problem then simplifies to:

subject to

which is self-evident. Hence, practically, we receive a simple unconstrained optimization problem except for the conditions \(c^* \ge {\underline{c}}\) and \(c^* \le {\overline{c}}\), which can be readily integrated into an overall optimization model. Thereby, the thruth-telling constraint is binding. Actually, head office maximizes profits under consideration of the reported cost \(c^*\).

We can recast the optimization problem also as follows:

whereby U measures the total utility of the manager, which is defined as:

Hence, the utility of the manager corresponds exactly to her weighted wealth benefit. Since utility is positive, the related profit for a company owner is smaller in the second-best situation. To conlude, both like to achieve maximum utility. The manager likes to maximize slack and the company owner likes to maximize profits. A simple partial integration then results in:

Because of \(F({\underline{c}}) = 0\), the boundary term vanishes. Even for the assumption of a more general B(c), we yield in general:

if we assume Eq. (3) and utility to be defined by \(U(c) = B(c) - c \, I(c)\), see Appendix A, which is consistent with the former result in Eq. (8) for \(B(c) = c^* \, I(c)\). However, the boundary term may change for arbitrary but convex budgets in terms of \(c^*\) as long as the resource feasibility constraint is fulfilled like \(B(c) = 1.2 \, c^* \, I(c)\), for instance.

In the present case, it remains:

The so-called Mills-quotient \(\frac{F(c)}{f(c)}\) is positively increasing such that the resulting optimization problem is convex. If we bring both results together, we yield eventually as optimization problem to be solved:

We can interpret the problem in agreement with Mayer et al. (2005) by concluding that profits become maximal if the cumulative probability of acception of the marginal budget \(F(c^*)\) is equal to the supplementary marginal surplus of \([e-c^*] \, f(c^*)\). For the case of a simple uniform distribution, the model shall now be analyzed analytically.

For a uniform distribution, we find \(f(c) = \frac{1}{{\overline{c}}-{\underline{c}}}\) und \(F(c) = \int ^c_{{\underline{c}}} f(c) \, dc = \frac{c-{\underline{c}}}{{\overline{c}}-{\underline{c}}}\). If we enforce the optimality condition \(\partial _{c^*} P = 0\), we obtain (Fig. 2):

Probability density, profit \((\max \, P = (e-c^*) \, F(c^*))\) and slack \((\max \, U = (c^*-{\underline{c}}) \, \frac{F(c^*)}{2})\) for a uniform distribution (according to the intercept theorems we have \(\frac{F(c^*)-F({\underline{c}})}{c^*-{\underline{c}}} = \frac{F({\overline{c}})-F({\underline{c}})}{{\overline{c}}-{\underline{c}}}\) or, eventually, \(F(c^*) = \frac{c^*-{\underline{c}}}{{\overline{c}}-{\underline{c}}}\))

We then get for the maximum utility of the manager for the given \(c^*\):

As maximum profit of the company owner, we receive:

For the simple exemplary case of \({\overline{c}} = 1\), \({\underline{c}} = 0\), it follows:

In the extraordinary case that the determined value \(c^*\) surpasses the upper bound \({\overline{c}}\), we enforce \(c^* = {\overline{c}}\) in all equations and perform the integration. Hence, concluding, in the simple case of a uniform distribution with \({\overline{c}} = 1\) and \({\underline{c}} = 0\), we obtain:

3 The classical newsvendor model under agency conflicts

In Toll and Kintzel (2019), IT-service companies were in the focus of interest considering the business model of call centers as prototype case. For the related dimensioning of capacities representing required personnel and technical infrastructure, a newsvendor model was used. By means of a newsvendor model, a nonlinear profit functional is optimized under stochastic demand whereby an optimum trade-off between risks of overstocking and understocking of capacities and their related earnings is pursued. Clearly, a maximum amount of capacities is achieved, which should meet demand in an optimal way. Below this limit, hence, if only fewer clients call than expected, costs from overstocking arise and, if more clients want to be served, costs from understocking arise since the call center can only operate at its capacity limit. In a corresponding profit maximum, a trade-off is reached which minimizes the risks of over- and understocking of capacities. In the following, we consider the variable cost term \(c \, Q\), which represents energy, standby and maintenance costs, to be subjected to agency conflicts. Accordingly, only a certain portion of the total earnings term \(p_{NV}\) per unit of capacity is under control of the manager.

The classical newsvendor model is usually applied to optimize the supply and storage of inventory stock. In Höck (2005, 2008), this approach was suggested for the dimensioning of capacities of IT-service companies, which was adopted in Toll and Kintzel (2019) to optimize the capacities of call centers in a corresponding case study. By means of the classical newsvendor model, an optimum trade-off between underage costs due to shortages and overage costs due to leftover stock is achieved (Porteus 1990). Concerning IT-service companies, shortages in capacities may lead to loss of goodwill while costs due to overcapacities may lead to unnecessary holding costs. The optimum is achieved in a related profit maximum. The earnings term is defined by:

whereby the earnings \(p^*_{NV}\) per unit of capacity are defined by:

Q is the maximum capacity provided and x is the actual amount of clients served. \(p_{NV}\) are the average earnings for each treated client and e are the corresponding earnings as far as agency conflicts are concerned. For a demand below the capacity limit, i.e. for \(x \le Q\), it is met. For a demand above the capacity limit, i.e. for \(x > Q\), only Q clients can be served. The earnings are distributed according to a stochastic probability function \(\varphi (x)\) with the related differential \(d\psi (x) = \varphi (x) \, dx\).

The costs term is divided into variable costs c, storage or liquidation costs \(c_H\), also known as lock-in or holding costs, for \(x \le Q\) and out-of-stock costs \(c_S\) for \(x > Q\). To model the present economic problem of moral hazard caused by asymmetric information, i.e. an unequal distribution of information among a principal (owner of a company) and her agent (manager), whereby the latter has usually an information edge, referring solely to the variable cost term c, we introduce the cost-related agency terms from Sect. 2.

Finally, the corresponding profits are defined by \(P(Q,c^*) = E(Q,c^*) -L(Q,c^*)\) as difference beween earnings and costs. In the sequel, we apply a normal distribution \(\varphi (x) = \frac{1}{\sigma \sqrt{2 \, \pi }} \, e^{-\frac{1}{2}(\frac{x-\mu }{\sigma })^2}\) as probability function with mean value \(\mu \) and standard deviation \(\sigma \). The probability density \(f(c)=\frac{1}{{\overline{c}}-{\underline{c}}}\) is chosen as uniform distribution throughout this contribution.

4 The nonlinear state marginal price vector model

For the formulation of the nonlinear state marginal price vector model, we use compact vector algebra: A vector \(\mathbf{a}\in \mathbb { R}^k\) of dimension k represents a tuple \((a_1,..,a_k)\) of k single components. The dot-product of two vectors \(\mathbf{a}\cdot \mathbf{b}= \sum _{i=1}^k a_i b_i\) of the same dimension is defined as component-wise sum of the products of both vectors. Relational operations like \(\mathbf{a}\ge \mathbf{b}\) should be understood component-wise, in this case meaning \(a_i \ge b_i \; \forall \; i \in [1,k]\). \(\mathbb { H}\) is a linear mapping between vectors, i.e. \(\mathbf{a}= \mathbb { H} \cdot \mathbf{b}\), for instance. \(\mathbf{h}(\cdot )\) is a nonlinear mapping between vectors, e.g. \(\mathbf{a}= \mathbf{h}(\mathbf{b})\).

4.1 Formulation of the nonlinear base and valuation approaches

To determine the marginal price resp. marginal price stream for a valuation object, we formulate two optimization approaches whereby an initial base approach is taken as reference state for a subsequent valuation approach. As target for the base approach, we employ maximization of wealth whereby the withdrawals \(\mathbf{G}^{Ba}\) measure annual monetary surpluses available for consumption spending. Within the target function to be maximized, the stream of withdrawals is weighted by means of a weighting vector \(\mathbf{w}^{Ba} \ge \mathbf{0}\) to a point quantity whereby in particular the case \(w^{Ba}_{n} = 1\) in combination with \(w^{Ba}_t = 0\) for \(t \in [0,n-1]\) is of special importance, which leads to a maximum end value EV as total monetary surplus at the planning horizon. After having solved the base approach, we obtain maximum utility as target value \(\overline{{\textit{GW}}}{}^{Ba}\), before a transaction has actually been realized, which means without consideration of the valuation object in question.

To satisfy the liquidity conditions at the end of each period \(\Delta t_{t-1,t}\), the cash flows of all active investment or financing objects as well as autonomous payments have to be equilibrated with the withdrawals \(G_t^{Ba}\). The so-called autonomous payments represent pre-determined cash flows which include already fixed payments or withdrawals and are defined by the vector \(\mathbf{b}^{Ba}\) bounding the liquidity conditions. The decision field is modeled by concave nonlinear functionals \(\mathbf{h}^{Ba}(\cdot )\) (Pfaff et al. 2002) in dependence on \(\mathbf{x}^{Ba}\) as investment and financing objects. In the latter, financial assets or liabilities as well as cash holdings or investments in reals assets as well as all other independent variables to be optimized like \(\mathbf{c}^*\) as optimal budgets, for instance, are taken into consideration. The upper bounds for all objects \(j \in [1,m]\) are defined by the vector \(x^{max,Ba}_j\), which may include the unconstrained case of infinity as special case as well. For all independent variables, namely the withdrawals \(G^{Ba}_t\) and the objects \(x^{Ba}_j\), we assume non-negative real-valued quantities. Accordingly, the base approach can be formulated as:

subject to

The possible situation after realization of the transaction under consideration is modeled in a corresponding valuation approach. Hence, now, the valuation object is integrated into the valuation approach in return for a price stream as related compensation. The optimal solution (base program) provided the maximum target value \(\overline{{\textit{GW}}}{}^{Ba}\) as point quantity. A transaction is economically advantageous if at least this target value is reached in the valuation program again. Hence, to enforce the same degree of target value achievement, we introduce a further coupling constraint in terms of the corresponding annual withdrawals \(\mathbf{G}\) which are condensed to a point quantity by taking the weighting vector \(\mathbf{w}\) into account. The decision field is modeled by concave nonlinear functionals \(\mathbf{h}(\cdot )\) (Pfaff et al. 2002) whereby \(\mathbf{h}^{Ba}(\cdot )\) and \(\mathbf{h}(\cdot )\) can differ. However, even in the special case of \(\mathbf{h}^{Ba}(\cdot ) = \mathbf{h}(\cdot )\), the active investment and financing objects can be different owing to a possible restructuring among the investment and financing programs if a basis change occurs. By convention, for both approaches, negative-valued entries \(\mathbb { H}_{tj}\) of the unique linear cash flow streams \(\mathbb { H}_j\), \(j \in [1,m]\) represent cash outflows while positive-valued entries represent cash inflows, and similarly for \(\mathbf{h}^{Ba}(\cdot )\) and \(\mathbf{h}(\cdot )\). Furthermore, to include all earnings or costs accompanied with a valuation object, we use the so-called cash flow stream of the valuation object \(\mathbf{g}_K := (g_{K0},\ldots ,g_{Kn})\), which contains all already known financial in- or outflows over the planning period, which result from ordinary business operations or could be extraordinary by nature. As corresponding compensation, the investor has to pay at utmost \(\mathbf{p}= p \, \mathbf{z}\) (Toll 2010) where \(\mathbf{z}\) is a distribution vector and p is the width of the marginal price stream. To obtain the maximally affordable monetary compensation, the maximum value \({\bar{p}}\) of the width of the marginal price stream has to be computed. Therefore, a multi-decision problem must be solved by maximizing the compensation under consideration of a subjective decision field. Thus, the valuation approach eventually reads as:

subject to

It is noted that \(\mathbf{w}= \mathbf{w}^{Ba}\). For the corresponding dual optimization problem and the supplementary nonlinear arbitrage value term, please see a comprehensive in-depth discussion in Toll and Kintzel (2019). Here, we consider the valuation case of a purchase. In the alternative valuation case of a sale, the signs of the earnings of the valuation object and the marginal price stream are reversed, which means a valuation subject wants to sell a valuation object and receives a compensation in return from the buyer. However, both optimization problems are similar except for this important difference. Clearly, the width of the marginal price stream must be minimized in the valuation case of a sale.

For the width of the marginal price stream, we can find an interval, in which the actual width of the marginal price stream must lie:

where \(\bar{\varvec{\rho }}\) and \(\bar{\varvec{\rho }}{}^{Ba}\) are the marginal discount factors of the valuation and base program, respectively. As mentioned above, in the related valuation case of a sale, the signs of the width of the marginal price stream p and the earnings \(\mathbf{g}_K\) are simply reversed. After multiplication of this relation with the factor \(-1\), the inequality signs then alter as well.

The analytical so-called valuation formula can be recast in the nonlinear regime and for the valuation case of a purchase as:

by setting \(\mathbf{h}({\bar{\mathbf{x}}}_{lin}) \cdot \bar{\varvec{\rho }} = \bar{\varvec{\rho }} \cdot \mathbb { H} \cdot \mathbf{x}^{max}_{lin}\) and \({\bar{\mathbf{x}}} = {\bar{\mathbf{x}}}_{lin} \oplus {\bar{\mathbf{x}}}_{nonlin}\). \({\bar{\delta }}\) is a discounted shadow price. For more details, please see Toll and Kintzel (2019).

5 Embedding of the newsvendor model into the nonlinear state marginal price vector model

5.1 Modeling of the multi-period nonlinear optimization approach

The single-period newsvendor model according to Eqs. (17) and (19) is integrated into a multi-period decision problem (analogously to Angelus and Porteus 2002), for more details please see Toll and Kintzel (2019). To enforce maximization of profits within the model, we measure the total monetary surplus at the end of the planning period by means of the end value EV as proposed in Sect. 4.1. The important task is to formulate the base and valuation approaches within a simultaneous optimization approach. Clearly, all what changes is the implementation of the new formulations in Eqs. (17) to (19) instead of Eqs. (18) and (19) in the original model in Toll and Kintzel (2019) as well as the integration of \(c^*\) resp. \(c_t^{Ba \, *}\) and \(c_t^*\) for \(t \in [t_1, t_{n+1}]\) as additional independent variables into the optimization approach.

5.1.1 Equation system for the base approach

Maximize \({\textit{EV}}{}^{Ba}\) subject to

The Lagrange function can be established as

We are able to derive the following dual optimization problem:

subject to

5.1.2 Equation system for the valuation approach

Maximize p subject to

The Lagrange function can be established as

We are able to derive the following dual optimization problem:

subject to

5.2 Errata for the dual objective functions in Toll and Kintzel (2019)

Unfortunately, the dual objective functions were documented wrongly in Toll and Kintzel (2019). A good proof for the correctness of the implemented formulas is to test whether the objective functions coincide numerically with regard to both optimization problems, namely the primal and dual optimization problems, for both approaches. In the present case, all computations cited in the article were correct, but since the pre-determined capacities \(Q_0\) and \(Q{}_0^{Ba}\) are constant and their derivatives vanish, the corresponding expressions concerning the exponents \(\beta \) and \(\beta ^{Ba}\), respectively, were not printed out correctly in this article. Therefore, the correct dual objective functions are reiterated here.

5.2.1 Errata for the objective function of the dual base approach

5.2.2 Errata for the objective function of the dual valuation approach

5.3 Validation of the single-period newsvendor model under agency conflicts

To test the correctness of the implementation of the single-period model, we formulate the following simple optimization problem as shown below.

Maximize \({\textit{EV}}\) subject to

under the constraints \(EV \ge 0, Q \ge 0\), \(Q \le \infty \), \({\underline{c}} \le c^*\) and \(c^* \le {\overline{c}}\).

Actually, we arrive at the profit maximum for the optimal values \(Q^*\) and \(c^*\), meaning at the vertex of the profit function. Differently to the case without agency conflicts, the optimal quantity \(Q^*\) is not a variable anymore which is fixed throughout the computation, but which depends on \(c^*\).

By computing the first derivative of the profit function and equating to zero, we yield the necessary condition for the profit maximum, see appendix B. To test if the implementation is correct, we can compare the following definition for e:

The plot of the cumulative distribution function \(\Psi (Q^*)\) with respect to \(c^*\), see Eq. (37), is shown in Fig. 3 on the left-hand side. The actual upper bound of capacities \(Q^*\) with respect to \(c^*\) is shown on the right-hand side. For a numerical prove, using the parameters from Table 1 and the data of Table 2 from the not bracketed column \(\Delta t_{0,1}\) for the sake of exemplification, we get \(\mu = 10.0\) and \(\sigma = 2.12132035\). The optimal results are computed as \(Q^* = 12.2578998\) and \(c^* = 12.0306491\). With \(\frac{\Gamma (Q^*)}{Q^*} = 0.196935\), Eq. (26) is fulfilled. As can be observed, \(c^*\) is only slightly different to the mean value \(c_{mean} = \frac{{\underline{c}}+{\overline{c}}}{2} = 12.0\).

Plot of (a) \(\Psi (Q^*)\) and (b) \(Q^*\) with respect to \(c^*\) for \([{\underline{c}},{\overline{c}}]=[8,16]\), see Eq. (37)

Technically speaking, for integration into the optimization approach, we interpolate the function for the upper bound of capacities \(Q^*(c^*)\) by employing the model of a polynomial of fifth order as best fit:

For the current example, we compute \(Q^*( 12.0306491) = 12.2578444\), which is left from the vertex, see the optimum value \(Q^* = 12.2578998\). Normally, the related constraint for the upper bound of capacities is never binding.

5.4 Validation of the multi-period optimization approach

By implementing the primal and dual optimization problems of the base and valuation approaches, we have a proper benchmark to test if the equation system has been correctly formulated and implemented. That what is implicit in the primal optimization problem is explicit in the dual optimization problem (like optimality conditions as constraints) and vice versa. The end values should be equal in both programs. Secondly, we can compute the analytical valuation formula in Eq. (25) to test if both optimization problems are consistent since the valuation formula is uniquely based on the primal and dual optimization problems. To test the implementation results for the multi-period newsvendor model regarding the new expressions concerning \(c_t^*\), we can draw also on the optimality conditions for \(c_t^*\). Thus, we obtain in a first step, see appendix B:

The optimality condition \(-{\bar{d}} \, {\bar{\partial }}_{c^*} P(Q,c^*) - {\bar{v}} \, {\bar{\partial }}_{c^*} Q^*(c^*) - {\bar{m}} + {\bar{n}} = 0\) reads as:

for a corresponding \({\bar{Q}}\). By means of this analytical solution, we can test in hindsight if the implementation of the novel budgeting condition was correct.

5.5 Calibration of the multi-period nonlinear optimization approach

5.5.1 Practical business model of call centers

As mentioned above, we are concerned with the dimensioning of call centers on the basis of a newsvendor model presented in Sect. 3, which was applied for the first time in Toll and Kintzel (2019). Under dimensioning of capacities we understand the quantitative determination of personnel (administrative, technical and service-related) and technical infrastructure (computers, mainframes, terminals) whereby demand is not certain, but stochastic. Clearly, an optimum trade-off is achieved by which means a call center can optimally react to its clients, i.e. callers by telephone. As far as call centers are concerned, the capacity Q and the number of clients x in Eqs. (17) and (19) represent flow-oriented quantities measured per minute, which applies to all parameters.

5.5.2 Valuation case of a merger of two IT-service companies

In the present example, a merger of two IT-service companies is in the focus of attention in the framework of a second-best solution, which is based on the example in the framework of the first-best solution discussed in-depth in Toll and Kintzel (2019). The problem can be described as follows: The owner of a call center A wants to acquire another call center B to enlarge its client base and to yield a more advantageous organizational structure modeled by the parameters \(\beta ^{Ba}\) and \(\beta \) in the resulting merger to a call center A+B. As starting point of our analysis, the economic situation for call center A is to be evaluated in a corresponding base approach as referential state. Finally, the end point of our analysis in form of a merger to the call center A+B is taken into account in a corresponding valuation approach. By measuring all monetary gains realizable in the final state with respect to the reference state, an investor can determine her individual ultimate willingness to concede to the transaction agreement, i.e. her subjective decision value. Thereby, all capacities and budgets in both states are determined in an optimal manner and the marginal price vector mirrors finally the critical monetary compensation at which the investor is indifferent between both scenarios.

5.5.3 Chosen parameters and notations of the model

The parameters \(p_{NV}\), e, \({\underline{c}}\), \({\overline{c}}\), \(c_S\), \(c_H\), \(h_c\), K and k of the multi-period newsvendor model are fixed throughout the planning period according to Table 1.

The projected planning phase stretches over 6 periods from \(t_0\) to \(t_6\) whereby at \(t_6\) all capacities are liquidated, i.e. the autonomous payments beyond the planning horizon are \(b_\infty ^{Ba} = b_\infty =0\) with \({\bar{b}}_{n+1} = b_{n+1}\) and \({\bar{\alpha }}= \alpha =1\), accordingly. We introduce two types of demand functions with mean values \(\mu _t^{Ba}\) and \(\mu _t\) as well as standard deviations \(\sigma _t^{Ba}\) and \(\sigma _t\) in each period referring to the states before and after the merger, respectively, based on forecasted values as educated guesses in Table 2.

With the given values from Table 2, we compute the means \(\mu _t = {\textstyle \sum _{i=1}^3} pb_i \, D_{i \, \Delta _t }\) and standard deviations \(\sigma _t = ({\textstyle \sum _{i=1}^3} pb_i \, (D_{i \, \Delta _t} - \mu _{t})^2)^{\frac{1}{2}}\) for each period \(\Delta t_{t-1,t}\) for six equidistant annual time periods \(\forall \; t \in [t_1,t_6]\). The cash flow stream of the valuation object \(\mathbf{g}_K\) and the autonomous payments \(\mathbf{b}\) within the planning period are given in Table 3 whereby we assume \(\mathbf{b}^{Ba} = \mathbf{b}\).

A fixed down payment of 50.0 has to be made upfront at \(t_0\). Thereafter, annual cash inflows are at one‘s disposal at the end of each period. The exponents referring to the variable cost term \(h_c(\cdot )\) are set to \(\beta ^{Ba} = 1.04\) and \(\beta = 1.02\). The initial capacities are specified in advance as \(Q_0^{Ba} = 10.0\) and \(Q_0 = 13.0\).

As embedding action space of financing objects we consider the cash flow streams according to Table 4. Thereby, we have introduced single-period financing objects with a lending interest factor \(q_L\) and a borrowing interest factor \(q_B\). Furthermore, we have introduced an annuity and a coupon rate series. The corresponding upper bounds (limits) of the financing objects are shown in Table 4 in the last row.

5.6 Simulation with the multi-period nonlinear optimization approach

The results for the width of the marginal price stream \({\bar{p}}\) for various \(\mathbf{z}\)-vectors are shown in Table 5. Compared to the first-best solution in Toll and Kintzel (2019), we can state that the end value \({\overline{EV}}_{{ second}} = 3703.0895\) is smaller than \({\overline{EV}}_{{ first}} = 4068.2383\) leading almost to a reduction of 9% in end value. Clearly, also the resulting present values of the marginal price vectors are smaller compared to the first-best solution. In the sequel, solely the results for \(\mathbf{z}= \{3,2,1,0,\ldots \}\) are discussed. Concluding, the dual factors of the liquidity conditions in Table 8 are the same as in the first-best solution. The structure of computed credits \(C_t\) and investments \(I_t\) in Table 7 is similar, too, however with different realizations.

Concerning the optimal budgets under agency conflicts in Table 6, we can state that the computed budgets \(c^*_t\) differ strongly from the mean value \(c_{\mathrm{mean}}=12.0\) and are considerably larger than in the simple single-period newsvendor model presented in Sect. 5.3. The optimality conditions in Eq. (29) are completely fulfilled. For instance, for the first period with \(\mu = 10.0\) and \(\sigma = 2.12132035\), we obtain \(\Gamma (10.0) = 0.84628387\) where \(Q_0^{Ba} = 10.0\), which fulfills the optimality condition for the computed \({\bar{c}}{}_1^{Ba \, *} = 13.15371613\) (Tables 2 and 6).

To add further relevant information, the tranches of the coupon rate series are \({\bar{x}}_2^{Ba} = 248.065\) and \({\bar{x}}_2 = 670.795\) as well as \({\bar{x}}_1 = 539.990\) for the annuity. As the coupon rate series and the annuity are only partially realized and, hence, marginal, their corresponding dual factors \({\bar{u}}_1\), \({\bar{u}}_2^{Ba}\) and \({\bar{u}}_2\) are zero. For \(\mu \) we find \({\bar{\mu }} = 0.12271826\), the same as in the first-best solution. All other dual variables vanish since the related upper or lower bounds are not reached.

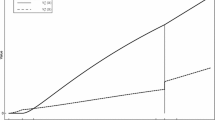

As final application, a short sensitivity analysis is done. In Fig. 4a, the end value \({\overline{EV}}\) is plotted for distinct e. For rising e, the end value falls until a plateau is reached when the optimum value \(c^*\) approaches the upper bound \({\overline{c}} = 16\) for large e. \({\overline{EV}}\) must fall with rising e since a higher portion of income is subjected to agency conflicts. Finally, in Fig. 4b, the left bound \({\underline{c}}\) in the cost interval \([{\underline{c}},{\overline{c}}]\) is varied while the right bound \({\overline{c}}\) complies with \(c_{mean} = 12.0\). As can be oberved, we obtain a convex curve for \({\overline{EV}}\) with a minimum roughly around \({\underline{c}}=5.0\), hence, for \([{\underline{c}},{\overline{c}}]=[5.0,19.0]\). For \({\underline{c}}=10.0\), the related upper bound \({\overline{c}} = 14.0\) is reached also in this case. Normally, e is known, but if we had no clear knowledge about the actual bounds of the cost interval for uniformely distributed costs c, it would be wise to use the parameters \({\underline{c}}\) and \({\overline{c}}\) holding in the minimum of \({\overline{EV}}\) to be on the safe side since, generally, the lower the end value \({\overline{EV}}\) the larger the residual width of the marginal price stream \({\overline{p}}\) in the present valuation case of a purchase. Hence, a brief sensitivity analysis could be done in advance of any comprehensive company valuation to find out the most appropriate parameter set for the considered cost interval. To fulfill this task, just the primal base approach needs to be solved.

Plot of EV for (a) discrete e with \([{\underline{c}},{\overline{c}}]=[8,16]\) and for (b) discrete \({\underline{c}}\) with \(c_{mean}=12.0\)

6 Conclusion and outlook

In Toll and Kintzel (2019), the linear state marginal price model of Hering (2000) and the linear state marginal price vector model of Toll (2010), suitable for company valuations, were extended to the nonlinear case. The so-called nonlinear state marginal price vector model was subsequently applied to the practical case study of a merger of two call centers as certain prototypes of IT-service companies. In the current contribution, we have enriched the latter model to take asymmetric information into account based on the publication of Inwinkl and Schneider (2008) where a one-sided agency conflict between a company owner and her manager was in the focus. Clearly, the manager of a certain department has an information edge over company management since she knows all costs actually incurred in her department, but is inclined to overstate costs to build up slack for herself. In the present case, we have been concerned with this well-known problem of moral hazard whereby one of the participants has more information than the other ones and can shield this information advantage. If an investor had no reasonable clues about such private information, it would be wise to consider this deficiency of moral hazard within the modeling framework. Clearly, the present case of moral hazard represents only a first step. Further improvements are conceivable, which would end up in more sophisticated modeling frameworks, which, however, was beyond the scope of the current introductory treatise. For instance, to take adverse selection into account, the owner or investor could bind her managers by contract to establish a closer agency relationship to signal a well-behaved demeanor and to motivate them to disclose some of their private information. All this could be treated within the framework of the nonlinear state marginal price vector model by means of suitable equation systems. For this purpose, a scalar composition factor were conceivable, which would moderate between the extremal states of symmetric and asymmetric information. The double-sided agency conflict, presented in Inwinkl et al. (2009), was beyond the scope of the present work as well. In a double-sided agency conflict, the case is considered that two managers report to head office and optimize slack independently from each other. The uniform probability density then turns into a step-wise linear probability density based on a Irwin-Hall distribution. Clearly, a crucial advantage of our numerical approach is that we can readily apply also those more complicated probability densities in our model. As outlook, we would like to remedy a further shortcoming of our model, namely the assumption of a risk-neutral attitude of a valuation subject. For this purpose, we like to integrate nonlinear concave time-continuous utility functions into the target function, whose related consumption preferences can only be formulated by using distinct step-wise weighting parameters \(\mathbf{w}\) and \(\mathbf{w}^{Ba }\) by now, which will be the topic of a forthcoming paper.

References

Angelus A, Porteus EL (2002) Simultaneous capacity and production management of short-life-cycle, produce-to-stock goods under stochastic demand. Manage Sci 48(3):399–413

Antle R, Eppen GD (1985) Capital rationing and organizational slack in capital budgeting. Manage Sci 31:163–174

Brösel G, Matschke MJ, Olbrich M (2012) Valuation of entrepreneurial businesses. Int J Entrepreneurial Ventur 4(3):239–256

Cyert R, March J (1963) The behavioral theory of the firm. Prentice Hall, Englewood Cliffs

Falee M, Fellingham J, Young A (1996) Properties of economic income in a private information setting. Contemp Account Res 13:401–422

Fisher I (1930) The theory of interest. The Macmillan Company, New York

Hax H (1964) Investitions- und Finanzplanung mit Hilfe der linearen Programmierung. Schmalenbachs Zeitschrift für betriebswirtschaftliche Forschung 16(6):430–446

Hering T (2000) Das allgemeine Zustands-Grenzpreismodell zur Bewertung von Unternehmen und anderen unsicheren Zahlungsströmen. Die Betriebswirtschaft 60(3):362–378

Höck M (2005) Dienstleistungsmanagement aus produktionswirtschaftlicher Sicht. Gabler, Wiesbaden

Höck M (2008) Ein Planungsansatz zur Kapazitätsdimensionierung von IuK-Techniken. Zeitschrift für Planung und Unternehmenssteuerung 19(2):143–158

Inwinkl P, Schneider G (2008) Unternehmensbewertung und Zustands-Grenzpreismodelle bei Agency-Problemen. Betriebswirtschaftliche Forschung und Praxis 60(3):276–292

Inwinkl P, Kortebusch D, Schneider G (2009) Das allgemeine Zustands-Grenzpreismodell zur Bewertung von Unternehmen bei beidseitigen Agency-Konflikten. Betriebswirtschaftliche Forschung und Praxis 61(4):403–421

Jaensch G (1966) Ein einfaches Modell der Unternehmensbewertung ohne Kalkulationszinsfuß. Zeitschrift für Betriebswirtschaftliche Forschung 18:205–233

Laux H, Franke G (1969) Zum Problem der Bewertung von Unternehmungen und anderen Investitionsgütern. Unternehmensforschung 13(3):205–223

Matschke MJ (1975) Der Entscheidungswert der Unternehmung. Gabler, Wiesbaden

Matschke MJ, Brösel G (2013) Unternehmensbewertung, Funktionen-Methoden-Grundsätze, 4th edn. Springer, Wiesbaden

Matschke MJ, Brösel G, Matschke X (2010) Fundamentals of functional business valuation. J Bus Valuat Econ Loss Anal 5(1):1–39

Mayer B, Pfeiffer T, Schneider G (2005) Wertorientierte Unternehmenssteuerung mit differenzierten Kapitalkosten: Einzel- versus Gesamtbewertung. Die Betriebswirtschaft 65:7–20

Pfaff D, Pfeiffer T, Gathge D (2002) Unternehmensbewertung und Zustands-Grenzpreismodelle. Betriebswirtschaftliche Forschung und Praxis 54(2):198–210

Poterba J, Summers L (1995) A CEO survey of US companies time horizons and hurdle rates. Sloan Manage Rev 37:43–53

Porteus EL (1990) Stochastic inventory theory. In: Heyman DP, Sobel MJ (eds) Handbooks in operations research and management science, vol 2. North-Holland, Amsterdam, pp 605–652

Schiff M, Lewin A (1968) Where traditional budgeting fails. Financ Exec May:259–269

Toll C (2010) Unternehmensbewertung bei Vorliegen verhandelbarer Zahlungsmodalitäten. Betriebswirtschaftliche Forschung und Praxis 62(4):384–411

Toll C, Kintzel O (2019) A nonlinear state marginal price vector model for the task of business valuation. A case study: the dimensioning of IT-service companies under nonlinear synergy effects. CEJOR 27(4):1079–1105

Weingartner HM (1963) Mathematical Programming and the Analysis of Capital Budgeting Problems. Prentice Hall, Englewood Cliffs

Funding

Open Access funding enabled and organized by Projekt DEAL.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

A Utility for the manager and the truth-telling constraint

The utility of the manager is defined by:

If we consider the truth-telling constraint:

where c and \(c'\) can swap places due to our assumption, see Eqs. (2):

we yield:

If we assume the project indicator function to be defined by:

we finally obtain:

for \(c^* \ge c\) and \(c^* \ge c'\), compare Inwinkl and Schneider (2008). Thereby, the truth-telling constraint is binding since \(B(c) \ge B(c')\) and \(B(c') \ge B(c)\) are only fulfilled for \(B(c) = B(c')\). Hence, in reverse, in view of Eq. (30), we can state that the satisfaction of the truth-telling constraint for arbitrary B(c) rests upon Eqs. (34).

B Profit maximum for the single-period newsvendor model

The profit function \(P(Q,c^*)\) reads as

where \(\mu \) is the mean value of the probability function.

By computing the first derivative with respect to Q and equating to zero, we obtain:

where \(\Psi (Q^*) = \psi (x \le Q^*) = \int \limits ^{Q^*}_0 d \psi (x)\), see “Appendix B” in Toll and Kintzel (2019).

By computing the first derivative with respect to \(c^*\) and equating to zero, we obtain:

From this, we receive:

The right-hand side of the latter term can be transformed to:

with the so-called Gamma-function \(\Gamma (Q)\) of the probability function since the boundary term at the left-hand side vanishes under the assumption that \(\psi (0)= \int ^0_{-\infty } d\psi (x) \approx 0\).

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Kintzel, O., Toll, C. Company valuation and the nonlinear state marginal price vector model under agency conflicts. Cent Eur J Oper Res 30, 1279–1305 (2022). https://doi.org/10.1007/s10100-021-00765-2

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10100-021-00765-2