Abstract

This article proposes a simple statistical approach to combine nighttime light data with official national income growth figures. The suggested procedure arises from a signal-plus-noise model for official growth along with a constant elasticity relation between observed night lights and income. The methodology implemented in this paper differs from the approach based on panel data for several countries at once that uses World Bank ratings of income data quality for the countries under study to produce an estimate of true economic growth. The new approach: (a) leads to a relatively simple and robust statistical method based only on time series data pertaining to the country under study and (b) does not require the use of quality ratings of official income statistics. For illustrative purposes, some empirical applications are made for Mexico, China and Chile. The results show that during the period of study there was underestimation of economic growth for both Mexico and Chile, while official figures of China over-estimated true economic growth.

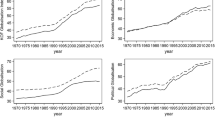

Source: Author’s elaboration with data from NOAA

Source: Authors’ elaboration with data from Banco de Información Económica, INEGI: http://www.inegi.org.mx/sistemas/bie/. Accessed on May 02, 2014

Similar content being viewed by others

References

Aruoba BS, Diebold FX, Nalewaik J, Shorfheide F, Song D (2013) Improving GDP measurements: a measurement-error perspective. National Bureau of Economic Research, Working paper 18954:1–34

Bertinelli L, Strobl E (2013) Quantifying the local economic growth impact of hurricane strikes: an analysis from outer space for the Caribbean. J Appl Meteorol Climatol 52:1688–1697

Chen X, Nordhaus W (2011) Using luminosity data as a proxy for economic statistics. Proc Natl Acad Sci 108(21):8589–8594

Doll C, Muller JP, Elvidge CD (2000) Nightime imagery as a tool for global mapping of socio-economic parameters and greenhouse gas emissions. Ambio 29:157–162

Elliot RJR, Strobl E, Sun P (2015) The local impact of typhoons on economic activity in China: a view from outer space. J Urban Econ 88:50–66

Elvidge CD, Ziskin D, Baugh KE, Tuttle BT, Ghosh T, Pack DW, Erwin EH, Zhizhin M (2009) A fifteen year record of global natural gas flaring derived from satellite data. Energies 2(3):595–622

Ghosh T, Sutton P, Powell R, Anderson S, Elvidge ChD (2009) Estimation of Mexico’s informal economy and remittances using nighttime imagery. Remote Sens 1(3):418–444

Granger CWJ, Newbold P (1974) Spurious regressions in econometrics. J Econom 2:111–120

Guerrero VM (2007) Time series smoothing by penalized least squares. Stat Probab Lett 77(12):1225–1234

Harari M, La Ferrara E (2013) Conflict, climate and cells: a disaggregated analysis. Center for Economic Policy Research (CEPR) Discussion paper no. DP9277. SSRN: https://ssrn.com/abstract=2210247. Accessed 21 Oct 2015

Henderson JV, Storeygard A, Weil DN (2012) Measuring economic growth from outer space. Am Econ Rev 102(2):994–1028

Hodler R, Raschky PA (2014a) Economic shocks and civil conflict at the regional level. Econ Lett 124:530–533

Hodler R, Raschky PA (2014b) Regional favoritism. Q J Econ 129:995–1033

Michalopoulos S, Papaioannou E (2014) National institutions and subnational development in Africa. Q J Econ 129(1):151–213

Nordhaus W, Chen X (2014) A sharper image? Estimates of the precision of nighttime lights as a proxy for economic statistics. J Econ Geogr 15:217–246

Phillips PCB, Perron P (1988) Testing for a unit root in time series regression. Biometrika 75:335–346

Rawski TG (2001) What’s happening to China’s GDP statistics. China Econ Rev 12(4):12–14

Ruppert D, Wand MP, Carroll RJ (2003) Semiparametric regression. Cambridge University Press, Cambridge

Seo N (2011) The impacts of climate change on Australia and New Zealand: a gross cell product analysis by land cover. Aust J Agric Resour 55:220–238

United Nations, European Commission, International Monetary Fund, OCDE and WB (2009) System of national accounts 2008. European Communities, International Monetary Fund, Organisation for Economic Co-Operation and Development, United Nations and World Bank, New York

Wackerly D, Mendenhall W III, Scheaffer RL (2002) Mathematical statistics with applications, 6th edn. Thomson/Brooks-Cole, Grove

World Bank (2002) Building statistical capacity to monitor development progress. World Bank, Washington

Author information

Authors and Affiliations

Corresponding author

Additional information

The authors thank two anonymous referees and the editor of this journal for their valuable comments and suggestions. Víctor M. Guerrero acknowledges financial support from Asociación Mexicana de Cultura, A. C. to carry out this work.

Appendices

Appendix A: Obtaining the BLUE of D y

Let I be the (N − 1)-dimensional identity matrix, \( {\varvec{\upeta}} = \left( {\eta_{2} , \ldots ,\eta_{N} } \right)^{\prime } \) and \( {\varvec{\upvarepsilon}} = \left( {\varepsilon_{2} , \ldots , \varepsilon_{N} } \right)^{\prime } \), so that models (9) and (10) can be written as the system of linear equations

with \( U = \left( {\begin{array}{*{20}c} I \\ {\beta I} \\ \end{array} } \right) \), \( E\left( {\begin{array}{*{20}l} {\varvec{\upeta}} \hfill \\ {\varvec{\upvarepsilon}} \hfill \\ \end{array} } \right) = {\mathbf{0}}_{{2\left( {N - 1} \right)}} \) the zero vector of size 2(N − 1) and

where \( 0_{N - 1} \) is the (N − 1)-dimensional zero matrix and \( \alpha = \sigma_{{}}^{2} /\sigma_{\varepsilon }^{2} \).

Then, by assuming that the parameters \( \beta \), \( \sigma_{\varepsilon }^{2} \) and \( \alpha \) are known, we apply GLS to obtain the best linear unbiased estimator (BLUE) of Dy, which is given by

that leads us to expression (11).

Appendix B: Unbiased estimation of \( \sigma_{\varepsilon }^{2} \)

Within the context of GLS, we can get an unbiased estimator of \( \sigma_{\varepsilon }^{2} \) by defining the residual vectors of models (9) and (10) as

so that the stacked residual vector becomes

Now, since

we get

with

a symmetric and idempotent matrix whose trace, \( {\text{tr}}(H) = N - 1 \), is the number of degrees of freedom for the residual sum of squares, given by

The matrix H is called the “hat matrix” because it transforms the original data Dz and Dx into the estimated data \( \widehat{{D{\mathbf{z}}}} \) and \( \widehat{{D{\mathbf{x}}}} \) by means of the following relationship

Thus, if \( \alpha \) and \( \beta \) were known, we obtain the following unbiased estimator

In practice, we have to use the estimators \( \hat{\alpha }^{ - 1} \) and \( \hat{\beta }^{2} \), in place of the true parameters \( \alpha^{ - 1} \) and \( \beta^{2} \), so that two degrees of freedom are lost and the variance estimator becomes expression (13), where we should notice that \( {\hat{\boldsymbol{\upvarepsilon }}} = \hat{\beta }(\widehat{{D{\mathbf{z}}}} - \widehat{{D{\mathbf{y}}}}). \)

Appendix C: Original data employed in the empirical applications

Year | Mexico | China | Chile | |||

|---|---|---|---|---|---|---|

Ln(DN) | Ln(GDP) | Ln(DN) | Ln(GDP) | Ln(DN) | Ln(GDP) | |

1992 | 0.356540 | 29.3690 | − 0.349342 | 29.1549 | − 1.201073 | 31.0451 |

1993 | 0.548981 | 29.3883 | − 0.266380 | 29.2859 | − 0.896996 | 31.1126 |

1994 | 0.563912 | 29.4319 | − 0.159449 | 29.4090 | − 0.918416 | 31.1681 |

1995 | 0.745930 | 29.3677 | 0.021317 | 29.5125 | − 0.657251 | 31.2691 |

1996 | 0.690892 | 29.4179 | − 0.023675 | 29.6078 | − 0.633634 | 31.3406 |

1997 | 0.593879 | 29.4834 | − 0.017993 | 29.6967 | − 0.671262 | 31.4046 |

1998 | 0.699476 | 29.5313 | 0.078083 | 29.7718 | − 0.494210 | 31.4364 |

1999 | 0.746560 | 29.5693 | 0.048182 | 29.8451 | − 0.513416 | 31.4288 |

2000 | 0.813918 | 29.6333 | 0.141074 | 29.9257 | − 0.417595 | 31.4727 |

2001 | 0.802614 | 29.6317 | 0.180832 | 30.0055 | − 0.380645 | 31.5059 |

2002 | 0.804416 | 29.6399 | 0.283795 | 30.0926 | − 0.336200 | 31.5275 |

2003 | 0.652805 | 29.6533 | 0.191841 | 30.1879 | − 0.491460 | 31.5659 |

2004 | 0.712251 | 29.6927 | 0.362953 | 30.2841 | − 0.406507 | 31.6246 |

2005 | 0.679279 | 29.7242 | 0.319271 | 30.3830 | − 0.477887 | 31.6787 |

2006 | 0.713111 | 29.7712 | 0.425282 | 30.4928 | − 0.409212 | 31.7236 |

2007 | 0.769451 | 29.8027 | 0.521681 | 30.6150 | − 0.376859 | 31.7693 |

2008 | 0.787806 | 29.8203 | 0.557354 | 30.7012 | − 0.356730 | 31.8004 |

Rights and permissions

About this article

Cite this article

Guerrero, V.M., Mendoza, J.A. On measuring economic growth from outer space: a single country approach. Empir Econ 57, 971–990 (2019). https://doi.org/10.1007/s00181-018-1464-1

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-018-1464-1