Abstract

Online retailers in emerging markets like South Africa are adopting Bitcoin payments. This study explores factors driving consumer adoption and word-of-mouth (WOM) recommendations for Bitcoin in online transactions. Using an integrated model combining valency theory, social contagion theory, and the technology acceptance model (TAM), we analyse data from 521 South African online shoppers. Findings reveal that perceived usefulness, ease of use, social pressures, trust, and perceived risk significantly influence both adoption and WOM. Importantly, self-efficacy moderates the relationship between these factors and behaviour. This research contributes to the literature by offering a comprehensive understanding of Bitcoin adoption. For business and policy actors, enhancing consumer self-efficacy can foster trust, ease concerns, and encourage positive WOM, ultimately aiding successful Bitcoin implementation and promotion.

Similar content being viewed by others

Introduction

Cryptocurrencies have witnessed remarkable growth in recent years. Over 2 000 cryptocurrencies circulated in the market in February 2019, valued at a total market capitalisation of USD 131.8 billion and daily transactions of USD 24 billion [95]. By February 2021, the total market capitalisation of cryptocurrencies increased to USD 1.4 trillion [21], reaching more than USD 1.5 trillion by June 2022 [52]. The most widely used cryptocurrency is Bitcoin, which has increasingly gained acceptance for wide-ranging transactions, including online commercial marketplaces. In April 2023, one Bitcoin Cash token was worth USD 123.1, compared to USD 2 500 in 2017 [132].

Despite a growing interest in Bitcoin cryptocurrency for e-commerce payments in Western countries, such as the USA, and Asian countries like China, its actual use has not gained enough traction. It is estimated that 46 million USA citizens intend to make online payments using Bitcoin, yet its cryptocurrency electronic commerce (e-commerce) payments total is only 2% of all e-commerce transactions [32]. Wu et al. [153] identified the leading countries in cryptocurrency usage or investment as Vietnam (21%), the Philippines (19%), Turkey (16%), Peru (16%), Colombia (15.3%), Argentina (14.3%), and Indonesia (13%). In Africa, South Africa (17.8%) and Nigeria (31%) are the major role players in cryptocurrency investments [153]. As the usage of Bitcoin continues to grow at a rapid rate, some online retailers have started accepting payments for goods and services facilitated with bitcoins [149]. Bitcoin has been adopted by various online retailers in South Africa as a mode of payment [50]. Moreover, Pick n Pay retail stores (e.g. PnP Express and PnP Clothing shops) enable consumers to purchase electricity and airtime, buy bus and plane tickets, and other products, and pay municipal bills using Bitcoin CryptoQR at the counter [19].

In South Africa, the use of bitcoin as a medium of exchange is fairly new and not yet widespread [50, 149]. Therefore, this study was conducted in South Africa. As a significant emerging market role player where online retailers accept payments for goods and services facilitated with bitcoins [50, 149], South Africa represents an attractive market for promoting Bitcoin cryptocurrency innovation for online payments among consumers. To date, relatively little research has been conducted in an emerging country like South Africa [149], which is witnessing a growing interest in Bitcoin for online transactions. Nevertheless, prior research has not devoted attention to examining consumers’ intentions to use Bitcoin for online payments and their WOM in South Africa, which is the objective of this study.

A review of the literature in Table 1 shows that many research issues in the areas of consumer acceptance and cryptocurrency use have been addressed. However, several key questions remain unaddressed in the literature, making them relevant for this study. First, while emerging research [23, 25, 80, 114, 127] has recognised the important role of social contagion in technological innovation acceptance and use, there is an observable gap in the literature regarding the role of social contagion in explaining consumers’ adoption intentions and WOM, specifically related to the Bitcoin cryptocurrency for online payments. Consequently, this study aims to address the following research question: How does social contagion influence consumers’ acceptance of Bitcoin for online payments and their WOM? Examining the impact of social contagion on consumers’ use intentions of Bitcoin for online payments and WOM holds significant research importance, as the findings would not only fill a critical gap in the literature, but also offer valuable managerial insights into leveraging social contagion to promote the acceptance of Bitcoin for online payments and to stimulate positive WOM recommendations from customers.

Second, the importance of the technology acceptance model (TAM) constructs—namely perceived usefulness and perceived ease of use—in shaping consumers’ acceptance of technological innovations has been widely emphasised in previous research [10, 83]. Similarly, the literature on Bitcoin cryptocurrency has recognised the significance of these constructs in influencing consumers’ intentions to use the technology (see Table 1). Furthermore, customers’ WOM plays a central role in shaping other customers’ perceptions of the innovation [110]. However, the relationship between customers’ beliefs about the usefulness and ease of use of technological innovations and their WOM remains unexplored in technological innovation and Bitcoin cryptocurrency literature. The current study addresses this research gap by examining how consumers’ beliefs about cryptocurrency for online payments influence their WOM, specifically Bitcoin usage. Moreover, there is limited understanding in the literature on how essential variables, such as trust and risk perceptions, affect consumers’ WOM. Therefore, this study addresses the following research question: How do consumers’ beliefs about the usefulness, ease of use, trust, and social contagion influence their WOM regarding Bitcoin for online payments? By examining the impact of beliefs about usefulness, ease of use, risk, trust, and social contagion on WOM, we uncovered how these beliefs influence the spread and adoption of Bitcoin for online payments. This knowledge could guide marketing strategies and communication efforts required in leveraging positive WOM to drive the adoption and use of Bitcoin for online payments and increase its market penetration.

Third, studies have acknowledged the significance of self-efficacy as a crucial individual difference variable that affects the acceptance and adoption of innovations [56, 77, 105]. Consumers’ perceptions of self-efficacy are pivotal in enhancing their confidence and reinforcing their beliefs about innovation, particularly in emerging technological innovations, such as Bitcoin. Despite this recognition, the existing body of research on Bitcoin’s application in e-commerce transactions has failed to investigate the influence of self-efficacy on consumers’ conviction about and adoption of this innovative payment method. Consequently, this study aims to bridge this gap by addressing the following research question: How do consumers’ perceptions of their self-efficacy in using Bitcoin for online payments moderate their beliefs about the innovation? Examining the moderating role of self-efficacy could provide a deeper understanding of how and why consumers’ beliefs about their capabilities strengthen or weaken the interaction of their perceived attributes of innovation, use intentions, and WOM. This understanding could provide valuable insights into the factors that drive or hinder the adoption and usage of Bitcoin and WOM for similar technological innovations.

Last, extant research has not adequately addressed the factors that explain consumers’ acceptance of Bitcoin in this context. As a result, there is limited knowledge of the specific determinants that could trigger and influence consumers’ interest in using Bitcoin for online payments. Consequently, a critical research gap must be addressed to understand the factors underlying consumers’ intentions to use Bitcoin for online payments and spread WOM communication about it. Understanding these factors is essential for businesses, policymakers, and researchers seeking to promote the adoption and effective use of Bitcoin as a payment method in South Africa’s unique market context.

This study offers several significant contributions to theory and practice. First, it makes a unique contribution to the literature by examining the role of social contagion in predisposing consumers to develop an intention to use Bitcoin for online payments and by explaining their WOM communication behaviour. By investigating the influence of social contagion on consumers’ adoption intentions and communication behaviour related to Bitcoin, this study expands understanding of the social dynamics that drive the acceptance and dissemination of innovative payment methods this blockchain technology offers. Second, the study’s findings contribute to and extend the literature by highlighting the essential role of beliefs about Bitcoin for online payments in shaping consumers’ intentions to use it and their WOM. By examining these beliefs and their impact on consumer behaviour, this study provides valuable insights into the cognitive processes and decision-making mechanisms that underpin consumers’ acceptance and promotion of Bitcoin as a payment method. Furthermore, this study reveals an essential moderating effect of consumers’ perceptions of self-efficacy on the relationship between their beliefs about using Bitcoin for online payments and WOM. By demonstrating that self-efficacy perceptions can strengthen or weaken the influence of these beliefs, this research uncovers a nuanced understanding of the interplay between individual factors and cognitive processes in shaping consumers’ intentions to adopt Bitcoin for online payments and spread positive WOM. The results have practical implications for designing targeted interventions that enhance consumers’ self-efficacy and address specific beliefs to foster greater acceptance and usage of Bitcoin for online payments and its WOM.

The next section discusses the literature and theories underlying the scope of the current study. Thereafter, the conceptual model and the research hypotheses development are presented. The study’s research methodology and findings are then outlined. Later, the implications of the theory and practice from the study’s results are noted. In conclusion, this study’s limitations are outlined and directions for future research are identified.

Review of the literature

Bitcoin cryptocurrency was primarily invented by Satoshi Nakamoto [103] as the first electronic payment system between exchange parties (peer to peer) without involving financial corporation services, such as banks or external agencies [48]. Bitcoin cryptocurrency has since formed part of the new technological inclusion in international economics and financial transactions [66]. While over 18 000 cryptocurrencies circulated in the global digital market by March 2022, as the first successful and leading digital currency, Bitcoin had a market capitalisation of USD 377.53 billion by June 2022, with a 0.23% maximum median on day-to-day return [52]. In recent years, payment processors and stores have approved significant developments to warrant more accessible cryptocurrency payment experiences [21]. According to Arias-Oliva et al. [13] and Ter Ji-Xi et al. [139], today’s global technology leaders, such as Microsoft and Amazon, accept Bitcoin electronic payments from consumers. In 2019, such payments amounted to nearly USD 10 million daily [24]. By 2021, there were already 14 915 Bitcoin automated teller machines worldwide, with 11 386 being in the USA (overall 89.4% in North America), Europe (8.9%), Asia (1%), South America (0.5%), Oceania (0.1), and Africa (0.1%) [131].

Unlike conventional payment systems, such as bank credit or debit cards, Bitcoin is more advantageous because it is less complicated to set up, payments are immediate, and there are no transactional charges (for local or international payments) or limited payment amounts [7]. The encryption techniques Bitcoin uses verify funds paid and regulate the digital currency [120]. A Bitcoin user sends and receives native tokens, while simultaneously validating the payment in a decentralised mode and a transparent system [37]. Users only need: (1) a public key, such as an address; (2) a private key; and (3) a technology application that enables them to access the blockchain ledger and interact with the reserved funds [21]. This private key is critical; if it is lost, the ownership of the Bitcoin gets lost in the blockchain system [135].

Consequently, the adoption of the Bitcoin blockchain technology is influenced by several socio-economic factors [109]. Despite the gradual increase and potential growth predictions, a literature review (see Table 1) shows that most Bitcoin cryptocurrency studies have been conducted in Western countries, including but not limited to Australia, the USA, the UK, Germany, and Ireland [7, 37, 73, 123, 143]. However, relatively little research has been conducted in an emerging market, such as South Africa [149], and prior studies tend to focus on the tax implications of Bitcoin transactions [50, 119]. The limited knowledge and scarcity of research on customers’ acceptance of Bitcoin payments for online transactions creates valuable opportunities for this study to contribute to the existing literature. By addressing these gaps, our research aims to investigate an underexplored area, providing valuable insights into factors driving consumers’ use intentions and WOM communication for using Bitcoin for online payments and their implications for e-commerce trade.

Technology acceptance model

Developed by Davis [34], the TAM presents a theory founded on the traditional theory of reasoned action (TRA) [43] to explain individuals’ intentions to use an innovative technology. Unlike TRA, researchers have sculpted TAM by removing the attitude component [145] and have proposed that a person’s intention to use new technology is influenced by perceptions of ease of use and usefulness, both having a direct and positive effect on the intention to use [118].

TAM is a decision-making process theory that explains whether or not an individual is likely to accept a new technology [34]. It has been used as the foundational theory to study individuals’ adoption intentions of a new technology, such as Bitcoin [2, 44, 91, 92, 154]. This study measures TAM’s factors that evaluate the impact of perceived ease of use and usefulness on South African consumers’ intentions to adopt the Bitcoin mode of payment in an online shopping environment. Furthermore, based on the literature review, TAM might not have been applied mainly to examine these consumers’ intentions to use the Bitcoin payment system in an online retail marketplace in the context of South Africa, an emerging economy. Therefore, the present study is a pioneer undertaking.

Valence theory

Valence theory [112] originated in the disciplines of psychology and economics and uses a “cognitive-rational” consumer decision-making model [108]. The theory posits that consumers have positive (i.e. evaluation of benefits) and negative (i.e. evaluation of risks) expectations before they engage with a product or a service holistically to achieve a net valence [36]. According to valence theory, buyers seek to exploit the benefits of a product or service and to reduce its perceived risks [112]. That is, according to Tang et al. [138], in decision-making, value is the most essential factor for consumers to attain all the perceived product or service benefits.

Valence theory continues to be used widely in marketing research in various contexts. It was unified to examine consumer behaviour [108], the benefits and uncertainties impacting consumers’ intentions to repeat purchases in e-commerce in a cross-border situation [100], and consumers’ perceptions of online recommendation agents [49], as well as to evaluate consumers’ trust in online food service [134]. Earlier studies tended to expose valence theory as a valid theory to apply in research in an e-commerce environment, but no previous research has applied it to understand consumers’ use of online payment systems, such as Bitcoin cryptocurrency, which is a unique contribution of this study.

Social contagion theory

Social contagion theory was developed by Burt [20] and is rooted in the medical philosophy of contagion. It explains the spread and acceptance of beliefs, knowledge, attitudes, emotions, and behaviour from organisations, individuals, groups, and others who might witness and be prompted by the beliefs, knowledge, attitudes, emotions, and behaviour displayed by the influencers [114]. Burt [20] explained that in social contagion theory, people’s behaviour, attitudes, and perceptions are mainly influenced by interpersonal processes or social networks, which affect how they manage the uncertainty of innovation [146]. This theory argues that prior to planning or deciding, individuals search for similar experiences from members of their closest networks who have encountered similar situations [20]. In other words, social contagion theory views individuals’ thinking processes, behaviour, and emotions as mainly driven by the behaviour and emotions displayed by significant others in their social networks. Individuals’ communications have egos that mostly impact mutual friendships, ego-perceived friendships, and alter-perceived friendships. However, with alter-perceived friendships, the effect might not exist at all, as egos might not be self-aware of alters, let alone of altering behaviour [29]. Angst et al. [9] and Huang [62] agreed that, intentionally or accidentally, people are influenced and influencers might consciously or unconsciously intend to influence other people and spread self-beliefs, emotions, attitudes, or behaviour, while those who are influenced might do so voluntarily or unintentionally.

Traditionally, social contagion occurs physically (face to face) between the involved parties [20], although scholars have found its presence in online environments, too [40, 72]. Research on social contagion theory [25, 80, 114] has emphasised that individuals can change their behaviour after interacting with others because of normative pressure, mimetic pressure, and coercive pressure. These factors can be applied strictly in an offline or an online setting and are thus a suitable fit to explain consumer acceptance and adoption of Bitcoin for online payments in an e-commerce context. Social contagion theory has been used in different fields, such as in the medicine and hospital sector [9, 29, 146], experiential information shared through bulletin board technology [62], online gaming [23], mobile banking [25], and the tourism sector [114]. Moreover, research shows how organisations can influence peer WOM communication and social contagion by making viral attributes an integral part of products and their marketing campaigns [12]. Nevertheless, there is scarcely any application of social contagion theory in research on the Bitcoin system of online payments. Consequently, this study applies social contagion theory to measure individuals’ beliefs about the use of Bitcoin for online payments in South Africa, an emerging country.

Overview of self-efficacy theory

According to Bandura [15, 16], people’s behavioural choice of activities and ability to stick to those choices are highly influenced by their perceptions of self-efficacy and the expected outcomes. Self-efficacy theory, as an integral measure of cognitive psychology theory, refers to “confidence in one’s ability to perform a given behavior in different situations” [79]. In a technological context, self-efficacy denotes “an individual judgment of one’s capability to use a computer” [31, 84]. Correspondingly, self-efficacy is a pivotal concept in predicting individuals’ ability to accept or reject new innovations amidst several obstacles [63, 74, 137]. However, few existing studies have assessed the moderating effect when individuals perceive self-efficacy in using Bitcoin cryptocurrency for online payments. A major contribution of this study lies in determining self-efficacy’s influence on individuals’ ability to use Bitcoin to perform online payments in an online retail environment.

Development of the hypotheses in the research model

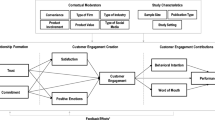

By merging the theories presented in the previous section, this study’s research model (see Fig. 1) has been developed to theorise TAM’s dimensions of perceived ease of use and usefulness; the valence constructs of evaluations of risk and trust; and the social contagion factors of normative pressure, mimetic pressure, and coercive pressure as imperative explanatory variables of consumers’ intentions to use Bitcoin cryptocurrency for online payments and of their WOM. The model further posits that consumers’ beliefs about their self-efficacy regarding online payments significantly moderate the impact of their beliefs about Bitcoin for online payments (perceived ease of use and usefulness from TAM, and evaluations of risk and trust from valence theory) on their use intentions and WOM. In addition, the model controls the effects of age, gender, online payment experience, online merchant’s reputation, and the device regularly used for online shopping on consumers’ intentions to use Bitcoin for online payments and WOM.

Proposed research model

Perceived usefulness and behavioural outcomes

According to Davis [34], perceived usefulness denotes the extent to which people believe that the use of a specific technological system or innovation could improve their task performance. In the Bitcoin context, perceived usefulness involves consumers’ optimistic attitudes that utilising Bitcoin for online payments helps to increase their effectiveness and productivity [2, 91, 92]. Research shows that perceived usefulness is an important contributor to South African consumers’ attitudes towards the use of Bitcoin for online payments [149]. Studies have confirmed that the usefulness of Bitcoin cryptocurrency positively impacts consumers’ intentions to use it as a system of online payments [4, 117, 126]. Moreover, usefulness can encourage consumers’ WOM about new innovations, such as artificial intelligence-enabled voice assistants and digital currencies like Bitcoin [6, 22]. If consumers believe that using Bitcoin cryptocurrency for online payments is highly beneficial and improves their performance with online shopping, they could spread positive WOM. Therefore, this research hypothesises that:

H1a

Perceived usefulness has a positive impact on consumers’ intentions to use Bitcoin for online payments.

H1b

Perceived usefulness has a positive impact on consumers’ WOM recommendations of Bitcoin online payments.

Perceived ease of use

Davis [34] referred to perceived ease of use as “the degree to which a person believes that using a particular system would be free of effort”. In this study, the evaluation of ease of use denotes the level to which consumers believe that the use of the Bitcoin method of payment when shopping online is relatively effortless. Research shows the positive and significant effect that the perception of ease of use imposes on customers’ trust in shopping online [96]. Nadeem et al. [102] argued that if an innovation, such as Bitcoin, is not perceived as easy to use or user-friendly, there is a high probability that it will negatively affect consumers’ intentions to utilise it. Researchers found that consumers’ intentions to use a cryptocurrency system are positively affected by perceived ease of use [2,3,4, 92, 126]. Similarly, ease of use influences consumers’ WOM [28]. When it is easy for consumers to learn a new technology and it is easier for them to use it, they might recommend it to others [76]. In the cryptocurrency context, it could be stated that the simpler it is for consumers to use Bitcoin for online payments, the greater the probability that they may spread positive WOM about it. Consequently, this research hypothesises that:

H2a

Perceived ease of use has a positive impact on consumers’ intentions to use Bitcoin for online payments.

H2b

Perceived ease of use has a positive impact on consumers’ WOM recommendations of Bitcoin online payments.

Perceived risk

Perceived risk is referred to as “consumer awareness to uncertainty and bad consequences of his/her participation in a certain action” [54]. In an electronic payment context, perceived risk refers to consumers’ beliefs of uncertainty on whether being involved in an online transaction may result in a loss of money [69]. The literature has also identified consumers’ perceived risk as an essential factor of the acceptance and use of technology [33, 85, 147]. Higher perceived risk and a lack of consumer trust are increased by the impersonal nature of an e-commerce environment and by other factors causing online payments to be abandoned [57]. If consumers perceive a high risk in using Bitcoin, the probability of their intention to use it in e-commerce for payment will be very low [156]. Anser et al. [11] examined consumers’ behaviour in social media usage and their intentions to accept the use of Bitcoin, grounded in the theory of planned behaviour and perceived risk. The results showed that consumers are unlikely to adopt Bitcoin online payment systems owing to higher perceived risk, even though they hold positive intentions towards using it. Surprisingly, Mendoza-Tello et al. [91] found an insignificant effect of perceived risk on consumers’ intentions to use Bitcoin cryptocurrency when making online payments. Research shows that perceived risk reduces consumers’ WOM [121]. Prior studies have revealed that perceived risk exerts a negative and significant impact on consumers’ WOM in other contexts, such as e-retail, hospitality, and healthcare activities [64, 78, 101]. As the results reported in those studies were unanimous, it is likely that the perceived risk of using Bitcoin for online payment in e-retailing could negatively impact consumers’ WOM recommendations. Thus, this research hypothesises that:

H3a

Perceived risk has a negative impact on consumers’ intentions to use Bitcoin for online payments.

H3a

Perceived risk has a negative impact on consumers’ WOM recommendations of Bitcoin online payments.

Consumer trust

Morgan and Hunt [97] referred to trust as consumers’ confidence in sellers’ integrity, dependability, and ability to offer a product or a service that meets their expectations. Since uncertainty about an innovation can significantly deter consumers’ intentions to use it [30], establishing trust could reduce uncertainty and increase expectations for a positive transactional experience [111]. Prior studies point to trust as an essential element in encouraging consumers’ intentions to use various innovations, such as Bitcoin cryptocurrency for online payments [4, 71, 92, 126, 149]. Prior studies show a positive and significant impact of trust on consumers’ behavioural intentions towards using electronic systems, such as digital payment applications [136], cryptocurrency transactions [2, 5], and electronic cryptocurrency payments in social media [91]. Like behavioural intention, trust could predict consumers’ positive WOM [130]. An absence of trust in a firm’s product or service inhibits customers from spreading positive WOM about it. Consumers who are not confident in a product are less likely to recommend it to others [157]. Hence, this research hypothesises that:

H4a

Trust has a positive impact on consumers’ intentions to use Bitcoin for online payments.

H4b.

Trust has a positive impact on consumers’ WOM recommendations of Bitcoin online payments.

Coercive pressure and behavioural outcomes

According to Chaouali and El Hedhli [25], “coercive pressure refers to individuals’ behavioural change dictated by more powerful social actors”. Coercive pressure occurs when relevant stakeholders impose a strong pressure through rules and regulations, punishments or sanctions, and even rewards for individual behavioural change [25, 80]. For instance, government agencies and retailers might require consumers to use specific and exclusive channels to pay for online purchases. From a cryptocurrency perspective, coercive pressures can come in the form of online retailers giving product discounts exclusively to consumers who use Bitcoin as a mode of online payment in online shopping in an attempt to change consumers’ behaviour. Studies show that coercive pressure significantly and positively influences consumers’ intentions to use several technological innovations, such as geographical information technologies [8], collaborative robots [129], and electronic business [81]. Organisations or influencers also perform an essential role in encouraging the speed of new technology acceptance—for instance, when they become early adopters of innovation and spread positive WOM, thus increasing widespread adoption [146]. As social interactions improve the sense of belonging in a society and consumer self-disclosure, they encourage consumers to develop WOM communication [128]. Given this knowledge, the study proposes that:

H5a

Coercive pressure has a positive influence on consumers’ intentions to use Bitcoin for online payments.

H5b

Coercive pressure has a positive influence on consumers’ WOM recommendations of Bitcoin online payments.

Mimetic pressure

Chaouali and El Hedhli [25] stated that mimetic pressure refers to encouraging “social actors to behave by seeking examples of established practices and behaviour to follow through voluntarily and consciously copying the same practices and behaviour of other successful and high-status actors”. In relation to technology acceptance, mimetic pressure plays a crucial role for non-adopters to avoid risks involving finances and privacy that early adopters or pioneers have encountered in an online environment [68]. Often, consumers are more likely to emulate the behaviour of others, owing to the belief that it will yield them more value or higher results [18]. In this sense, consumers’ willingness to adopt Bitcoin as a mode of payment in online shopping will occur if it is perceived to have more benefits for first-mover consumers. Considering that the important relationship between mimetic pressure and consumers’ intentions to use Bitcoin as a mode of payment in online shopping remains a research gap in the literature, the external force of mimetic influences from other consumers and external stakeholders is thought to promote intention to use this blockchain technology [39, 106, 133, 150]. Research shows that mimetic pressure promotes WOM communication about new technology adoption [53]. To avoid high uncertainty, consumers can imitate other successful organisations or consumers through WOM reference. As a way of self-expression or improving self-image, consumers tend to mimic high-status individuals who have used the innovation before [25] via online or offline WOM. Relative to competitor pressure, research shows that mimetic pressure from consumers is more valuable [81], often passed through WOM. Accordingly, this research hypothesises that:

H6a.

Mimetic pressure has a positive impact on consumers’ intentions to use Bitcoin for online payments.

H6b.

Mimetic pressure has a positive impact on consumers’ WOM recommendations of Bitcoin online payments.

Normative pressure

Chaouali and El Hedhli [25] stated that normative pressure refers to “one’s behavioural change as a result of his/her unconscious desire to comply with social norms”. According to Sherer et al. [127], when behaviour becomes law or popular among familiar people, such as family, close friends, or colleagues, non-users are likely to follow suit. The more these consumers perceive that important people think it is vital to engage or partake in a certain behaviour, the higher their likelihood to adopt that behaviour [42]. Otherwise, consumers do not want to be subjected to frustration and discomfort when their peers who are engaging in the unusual behaviour refer to them as “old fashioned” or “laid back” [25]. In the cryptocurrency context, non-adopter consumers may feel obligated to start using Bitcoin for online payments if people they look up to use it as well. From an organisational perspective, prior studies in blockchain technology adoption support this notion that normative pressure positively affects the intention to use new technology [46, 59, 104, 107]. Since normative pressure relies on the perception that “everyone is doing it” [107], it is likely to lead to greater WOM referrals. In fact, WOM is a significant source of information for consumers to adopt new technologies [35]. In this sense, the more consumers use Bitcoin for online payments, the greater the likelihood that they will engage in positive WOM. Consequently, this study proposes that:

H7a.

Normative pressure has a positive impact on consumers’ intentions to use Bitcoin for online payments.

H7b.

Normative pressure has a positive impact on consumers’ WOM recommendations of Bitcoin online payments.

Consumers’ intentions to use Bitcoin

According to Ajzen [1], “consumer intention to use” is a measure of the strength of their intention to task-perform a specified behaviour. In a cryptocurrency context, it can be described as the probability of Bitcoin cryptocurrency acceptance behaviour in an e-commerce environment for online payments [32]. Research indicates that consumers form the intention to use a new technological system when they believe it will offer a positive effect for factors, such as higher security and greater performance [99]. Therefore, consumers could develop the intention to use Bitcoin for online payments in an e-commerce environment if it is perceived to enhance their overall online shopping experience. Guo et al. [51] reported that consumers’ intentions to use new technology, such as an automated bus service, have influenced WOM communication. Put simply, the greater the individuals’ intentions to use, the more likely they are to recommend the new technology to others [141]. In a similar vein, consumers’ intentions to use a Bitcoin system of online payment in an e-commerce environment could determine their intention to spread WOM about it. Thus, this research hypothesises that:

H8.

Consumers’ intentions to use Bitcoin for online payments have a positive impact on their WOM recommendations of Bitcoin online payments.

Moderation effect of perceived self-efficacy

One of the most crucial factors for consumers’ adoption and use of new technologies is their perception of self-efficacy [26, 142]. Previous studies have shown that self-efficacy moderates the positive influence that perceived ease of use has on consumers’ intentions to use a biometric facial recognition payment system [98] and e-government services [94]. Moreover, self-efficacy significantly moderates the influence that perceived usefulness has on Italian teachers’ intentions to use technologies [90]. Ukpabi et al. [142] found that the positive relationship between trust and consumers’ use intentions towards the coronavirus disease 2019 (COVID-19) contact tracing app was moderated by their self-efficacy. According to Cheah et al. [26], consumers with lower self-efficacy are highly risk-averse about using an innovation. In contrast, if individuals’ self-efficacy is higher, they will perceive lower risk levels and will be more likely to become early adopters with increased WOM communication about new technologies.

Considering the objective of this study, the moderating role of self-efficacy for a Bitcoin system of online payment in electronic shopping is assessed on the relationship between the TAM and valence theory factors, and the behavioural outcomes of intentions to use and WOM recommendation. Yi and Gong [155] reported that the impact of consumer satisfaction on WOM is significantly moderated by self-efficacy. However, research shows that before a consumer is satisfied with a technological innovation, it has to be evaluated as easy to use [41]. In this regard, it is relevant to propose that the significant impact of the perception of ease of use on WOM recommendation is reinforced when consumers positively perceive self-efficacy. As perceived risk leads to the abandonment of online payments in an e-commerce environment [57], consumers with low self-efficacy have a good probability of being WOM ambassadors, warning potential consumers of the risk of adopting new technology. In contrast, people with greater self-efficacy have a higher likelihood of performing better as a result of the trust they have in their capabilities and certain skills to perform a task [148]. The current literature (refer to hypothesis H4b) proves trust is one of the drivers of WOM recommendation. For this reason, this research hypothesises that:

H9a.

Perceived self-efficacy has a positive moderating effect on the relationship between usefulness and the intention to use Bitcoin for online payments.

H9b.

Perceived self-efficacy has a positive moderating effect on the relationship between usefulness and WOM recommendation of Bitcoin online payments.

H9c.

Perceived self-efficacy has a positive moderating effect on the relationship between ease of use and the intention to use Bitcoin for online payments.

H9d.

Perceived self-efficacy has a positive moderating effect on the relationship between ease of use and WOM recommendation of Bitcoin online payments.

H9e.

Perceived self-efficacy has a negative moderating effect on the relationship between risk perception and the intention to use Bitcoin for online payments.

H9f.

Perceived self-efficacy has a negative moderating effect on the relationship between risk perception and WOM recommendation of Bitcoin online payments.

H9g.

Perceived self-efficacy has a positive moderating effect on the relationship between trust and the intention to use Bitcoin for online payments.

H9h.

Perceived self-efficacy has a positive moderating effect on the relationship between trust and WOM recommendation of Bitcoin online payments.

Covariates

To better understand consumers’ adoption of Bitcoin payments in online retailing, this study examines covariates, such as gender, age, online payment experience, online merchants, and devices used for online payments. The study proposed these covariates to determine their effect on consumers’ intentions to use Bitcoin for online payments and WOM referrals. Scholars realise the importance of examining gender differences in online retailing, which generally favours males [61, 113]. Despite this viewpoint having been long accepted and much studied [17, 93] and concentrating on examining the gender gap in Bitcoin literacy, little research in online retailing has examined gender roles from a South African perspective. Furthermore, Lee and Charles [75] believe that different age groups might exhibit different online shopping behaviour, and recommend studies investigate this further. The literature asserts that consumers who lack online payment experience have less trust in, and perceive high risk in using online retailers’ websites [54, 147]. Schleiden and Neiberger [124] explained that online merchants play an important role in influencing consumers’ online purchases or transaction decisions. Moreover, Marriott and Williams [85] noted that the device used for online payments affects perceived risk and online consumers’ purchase intentions. This evidence confirms the need to examine covariates, such as gender, age, online payment experience, online merchants, and the devices used for online payments, which impact use intentions of Bitcoin for online payments and WOM recommendation.

Research methodology

This section will outline a detailed research methodology used in this study. It covered the description of research instrument used, the population, sample elements, and data collection methods. This will be followed by data analysis procedure and results in order to understand the significant implications for research and practice in this article.

Instrument development

This study designed an instrument to measure respondents’ demographic data. The constructs measured in the research model were evaluated with multi-scale items that were validated and adapted in previous research. The TAM’s measures of ease of use (four items) and usefulness (four items) were adapted from Davis [34]. Valence theory’s perceptions of risk (four items) were adapted from Dabbous et al. [33], and those evaluating trust (four items) were adapted from Almarashdeh [5]. The social contagion theory factors of coercive pressure (three items), mimetic pressure (three items), and normative pressure (three items) were adapted from Chaouali and El Hedhli [25]. The measures of self-efficacy (three items) and intentions to use Bitcoin for online payments (four items) were adapted from Almarashdeh [5]. Finally, the measures of WOM recommendation (three items) were adapted from Van Tonder et al. [144]. Table 3 details each construct that was measured in the research model and its respective scale items. All scale items in the instrument were weighed using a five-point Likert scale, with (1) “strongly disagree” and (5) “strongly agree” as anchors. The paragraph preceding the scale items in the instrument explained what using Bitcoin for online payments means and provided graphical examples of how online payment with Bitcoin works. Thereafter, a question asked potential participants if they understood how online payment with Bitcoin works. They were requested to assume that they had a Bitcoin account that could be linked to online payments and to use this assumption when responding to each item.

The draft instrument was piloted on 30 respondents who fitted the definition of the study’s target population. The survey asked respondents to indicate the level on which their evaluations of each statement or item were agreeable, disagreeable, or felt neutral. The aim was to evaluate the content and face validity of the measurement instrument, increase its overall readability, and encourage more enthusiastic participation. The feedback from the pilot study identified a few typographical issues, including unclear wording in the statements. Cronbach’s alpha, when computed on the pilot data, varied from 0.804 for perceived risk to 0.920 for perceived trust. These estimates surpassed the 0.7 threshold, confirming the reliability statistic for each construct measured in the instrument [55]. After resolving the issues identified in the pilot exercise, the questionnaire was finalised for the data-gathering stage.

Population, sample elements, and data collection methods

This study targeted online shoppers who had made online payment transactions in the month preceding the survey and who understood how the Bitcoin payment option for online transactions works. Two screening questions were used to select respondents who met these criteria. An online survey was created and managed with Research.net, which sent an invitation letter and a brief requesting participation in this study to potential respondents who fitted the population of interest. Non-probability convenience and snowball sampling procedures were used to recruit respondents. Potential respondents who were readily available to the researchers were forwarded e-mail invitations with the Research.net link. Those who fitted the target population criteria and provided complete responses were thanked for partaking in the survey.

Data analysis procedure and results

After the online survey had run for nine weeks (April–May 2022), 548 responses were realised. The data gathered were explored for missing responses and 27 questionnaires were deleted due to missing responses, resulting in 521 complete questionnaires being utilised for data analysis (a 95% response rate). Table 2 shows the respondents’ demographic data (n = 521), which were estimated with the SPSS version 28. The statistical analysis revealed that the respondents were 57.8% female and 42.2% male. Majority of individuals were aged 18–24 years old (38.8%), followed by 25–29 years old (28.4%), and 30–34 years old (14.8%). Most respondents spent less than R1 000 (26.9%) on online transactions, followed by R1 000–R1 999 (20.2%). Most respondents (67.2%) used their mobile devices for online transactions, followed by their laptops (18.6%). Moreover, majority of respondents purchased from Takealot.com (63.1%), followed by Superbalist (11.9%). In total, 39.5% of respondents indicated they were well informed about the uses of Bitcoin cryptocurrency, followed by 34.5% who were somewhat informed.

Common method variance

Both a priori and post hoc statistical measures were implemented to avert and address the potentially adverse impact of common method bias in the data set. With the a priori measures, we followed the recommendation of previous researchers [60, 82] and only used multi-item scales that had been pre-validated in earlier studies, adapted to evaluate the constructs in the research model this study investigated. Complying with the recommendations by Podsakoff et al. [116], the pilot testing of the questionnaire identified and rectified a lack of clarity in the instructions and wording of the questionnaire. During the survey, the anonymity of the respondents’ participation in the study and the confidentiality of their responses were guaranteed. The Harman [58] single-factor technique was implemented as a post hoc statistical measure. The single factor explained 28.08% of total variance, which was below the traditional 40% threshold recommended by Babin et al. [14], showing the least of common method bias at a particularly high level. In addition, we used confirmatory factor analysis (CFA) in Amos 28 to assess the model fit of all the items forming a single-factor model of the constructs in our research model. The total fit of the scale items in a single-factor model (χ2 = 8116.996, df = 988, χ2/df = 8.216, comparative fit index [CFI] = 0.670, standardised root-mean-square residual [SRMR] = 0.078, root-mean-square error of approximation [RMSEA] = 0.118) was significantly worse (Δχ2 = 6298.409, Δdf = 209, p < 0.001) than that of the hypothesised CFA model (χ2 = 1818.587, df = 779, χ2/df = 2.335, CFI = 0.947, SRMR = 0.0467, RMSEA = 0.051). This proved that this study obtained and analysed data that were not affected severely by common method bias.

Measurement model validation

The validation of the measurement was carried out using covariance-based structural equation modelling (CB-SEM). This was appropriate because the research focused on examining the proposed comprehensive theoretical model (shown in Fig. 1) to determine its fit with the data and estimate complex relationships among latent variables. CB-SEM offers capabilities for model fit analysis and robust parameter estimates, which are crucial for assessing the theoretical model [70]. While other techniques such as PLS exist, they tend to have limitations in model fit analysis and are often used when the emphasis is on prediction, which was not the aim of this study.

The validation of the measurement model entailed using CFA to evaluate the psychometric properties of the scales employed in the study. The maximum likelihood estimation technique was implemented using Amos 28 software. The CFA procedure that was followed included estimating the convergent validity, discriminant validity, and goodness of fit. The initial estimations of the CFA model showed that a construct measuring habit had one item with a weak loading. This item was dropped and the model was re-specified and tested. All indices for the final measurement model showed a good model fit (χ2 = 1257.121, df = 443, p < 0.001, χ2/df = 2.838, SRMR = 0.0516, CFI = 0.941, RMSEA = 0.059). The factor reliability of each construct was established by means of Cronbach’s alpha. From the results illustrated in Table 3, the lowest Cronbach’s alpha of 0.808 (for perceived risk) exceeds the 0.7 threshold, which confirms the reliability of the measures of this construct. Following the confirmation of the reliability of each construct in this study’s model, the standardised factor estimates, composite reliability (CR), and average variance extracted (AVE) of the CFA model were evaluated for convergent validity. To obtain convergent validity, each construct’s factor loadings and its CR value were significant and larger than 0.7, while the estimated AVEs were greater than 0.5 for latent constructs [55]. The results in Table 3 show that for the convergent validity of the CFA model, the standardised factor estimated for each construct is significant at p < 0.001 and above the threshold of 0.7, with the lowest estimate being 0.716. Moreover, all the constructs had a CR value exceeding 0.7, with the lowest estimate being 0.841. Finally, the AVEs exceeded the 0.5 requirement, with the lowest value being 0.570. These estimates collectively provided the required convergent validity for the model.

After confirming the convergent validity of the measurement model, the next step in the CFA procedure entailed calculating its discriminant validity, which was attained by applying the Fornell and Larcker [45] technique. This technique suggests that for a CFA model to achieve discriminant validity, the square root of the AVE (see the bold estimates in Table 4) of each construct must exceed the inter-factor correlations. Table 4 presents the evidence that this criterion was met, thus strengthening the evidence that the CFA model attained discriminant validity. Having achieved both the convergent and the discriminant validity of the measurement properties in assessing the CFA model, we could affirm its accuracy in measuring the structural model and so test the proposed hypotheses.

Structural model

The study’s structural model was evaluated using a two-step sequential analysis. In the first step, the structural model with path effects—along with the control variables and the moderating variable (but free from the path effects)—was specified and analysed. In analysing the structural model, we ascertained (i) the goodness of model fit, (ii) the explanatory control of endogenous variance measured by R2, and (iii) the path coefficients and their levels of significance using the indicators of t-value (> 1.96) and p-value (p < 0.000). All indices for the structural model showed a good model fit, resulting in goodness of fit (χ2 = 1537.516, df = 657, p < 0.000, χ2/df = 2.340, SRMR = 0.044, CFI = 0.940, RMSEA = 0.051). The estimated R2 for the endogenous variables was 0.745 and 0.800 for use intentions and WOM, respectively.

In the second step, we mean-centred the moderator (perceived self-efficacy concerning the use of the Bitcoin system of online payments) and the four independent variables of interest to the moderation analyses and generated interaction terms as products of the mean-centred moderating variable with each of the four separate mean-centred independent variables. The generated interaction terms were added to the model. Next, we restricted the paths of the interaction terms, such that the model without the interaction terms was nested within the one with the relationships. Thereafter, we constrained the paths of the interaction terms, such that the former model without the interaction terms was nested within the latter one with the interaction. Subsequently, we performed a nested model analysis to compare the model with interaction terms against the one without. The results of the Chi-square comparisons of this analysis showed that the addition of the interaction terms to the model significantly improved the fit of the model (Δχ2 = 17.151, Δdf = 7, p < 0.05), thus emphasising the importance of the moderator in the model (Fig. 2). Moreover, the results of the nested model analysis showed that the R2 of the model with the interaction increased marginally from 0.745 (for the model without the interaction terms) to 0.756 (for the model with the interaction terms) for use intention, and from 0.800 (for the model without the interaction terms) to 0.807 (for the model with interaction terms) for WOM. The results of the parameter estimates are presented in Table 5.

Source: Based on authors’ computation. Note: Bold values represent the coefficients for intention to use, and non-bold values are coefficients for WOM

Results of structural equation modelling.

The analysis of the maximum likelihood estimates suggested that perceived usefulness had a significant and positive influence on customers’ intentions to use Bitcoin for online payments (β = 0.375, t = 20.165, p < 0.001) and on positive WOM (β = 0.076, t = 4.033, p < 0.001). This analysis supported H1a and H1b. The analysis also revealed that perceived ease of use of Bitcoin for online payments did not only significantly influence customers’ use intentions positively, as expected (β = 0.102, t = 5.092, p < 0.001), but also positively influenced their WOM of Bitcoin online payments (β = 0.048, t = 2.630, p < 0.01), providing support for H2a and H2b. Moreover, the results indicate that the perceived risk associated with using Bitcoin for online payments had a significantly negative effect on customers’ use intentions (β = − 0.085, t = − 2.395, p < 0.05) and subsequently had a negative impact on their WOM (β = − 0.094, t = -10.057, p < 0.001). These results supported H3a and H3b. In addition, the analysis indicated that trust in the use of Bitcoin for online payments significantly and positively influenced customers’ use intentions (β = 0.216, t = 11.651, p < 0.001) and WOM (β = 0.214, t = 12.147, p < 0.001). These results supported H4a and H4b.

Regarding the social contagion factors, we found that coercive pressure had a significantly positive effect on consumers’ use intentions of Bitcoin for online payments (β = 0.082, t = 4.444, p < 0.001) and on their WOM (β = 0.189, t = 11.009, p < 0.001), providing support for H5a and H5b. In contrast, the analysis indicated that while mimetic pressure had a significantly positive influence on consumers’ use intentions (β = 0.170, t = 9.502, p < 0.001), its effect on their WOM of Bitcoin online payments remained significant but negative (β = − 0.222, t = − 12.974, p < 0.001). Although H6a was supported, H6b was not. Similar conflicting results were obtained for normative pressure: normative pressure’s influence on consumers’ use intentions was statistically insignificant (β = 0.003, t = 0.168, p > 0.05). Conversely, normative pressure showed a significant influence on customers’ WOM of Bitcoin online payments (β = 0.205, t = 12.025, p < 0.001). Consequently, the evidence supported H7b, but not H7a. Finally, the analysis showed that consumers’ use intentions of Bitcoin for online payments significantly and positively influenced their WOM, providing support for H8.

Concerning the moderation effects, six of the eight moderation effects were measured. The results indicated that self-efficacy positively moderated the impact of usefulness on consumers’ WOM of Bitcoin online payments (β = 0.065, t = 4.545, p < 0.001). Similarly, self-efficacy was found to positively moderate the impact of ease of use on WOM of Bitcoin online payments (β = 0.056, t = 4.370, p < 0.001). The moderation analysis also showed self-efficacy as positively moderating the negative effect of the perceived risk in using Bitcoin for online payments on consumers’ use intentions (β = 0.057, t = 4.671, p < 0.001). Moreover, the analysis indicated the relationship between perceived risk in using Bitcoin for online payments and consumers’ WOM as being positively moderated by self-efficacy (β = 0.061, t = 6.742, p < 0.001). In addition, the analysis showed that the positive impact of perceived trust on use intentions was positively moderated by self-efficacy (β = 0.055, t = 3.869, p < 0.001), and the impact of perceived trust on consumers’ WOM of Bitcoin online payments (β = 0.065, t = 3.493, p < 0.001). These analyses underscored H9b, H9d, H9e, H9f, H9g, and H9h. To further clarify these significant effects of the moderating variable, illustrations of a simple slope analysis were compiled using unstandardised parameter estimates. Figures 3, 4, 5, 6, 7, and 8 show the summary illustrations of the simple slope analysis.

Moderating terms of self-efficacy in the usefulness–WOM relationship

Moderating terms of self-efficacy in the ease of use–WOM relationship

Moderating terms of self-efficacy in the perceived risk–use intentions relationship

Moderating terms of self-efficacy in the perceived risk–WOM relationship

Moderating terms of self-efficacy in the trust–use intentions relationship

Moderating terms of self-efficacy in the trust–WOM relationship

The simple slope analysis showed that customers’ perceptions of their self-efficacy strengthened the significant and positive relationships between the perceived usefulness of Bitcoin for online payments and WOM, and between ease of use of Bitcoin for online transactions and WOM. Furthermore, the results indicated that customers’ perceptions of their self-efficacy weakened the negative impact of the perceived risk of using Bitcoin for online payments on both use intentions and WOM. The findings also indicated, by the simple slope analysis, that customers’ perceptions of their self-efficacy strengthened the perceived effect of trust on both the use intentions and WOM of Bitcoin for online payments.

In respect of the impact of the control variables, five of the controlled relationships were significant—specifically, gender had a positive influence on consumers’ WOM concerning Bitcoin use for online payments (β = 0.016, t = 1.968, p < 0.001). Likewise, despite age’s positive relationship with use intentions towards using Bitcoin for online payments (β = 0.072, t = 7.678, p < 0.001); unexpectedly, its effect on consumers’ WOM was significantly negative (β = − 0.035, t = − 4.100, p < 0.001). Moreover, the device frequently used for online shopping was found to have a negative effect on consumers’ WOM about using Bitcoin for online payments (β = − 0.035, t = − 3.769, p < 0.001) and their use intentions (β = − 0.020, t = − 2.435, p < 0.05). Additionally, the online merchants that customers patronised had a significantly negative effect on their intentions to use Bitcoin for online payments (β = − 0.034, t = − 3.606, p < 0.001), although there was no evidence of statistically significant relationships between online merchants and WOM (β = 0.011, t = 1.265, p > 0.05). Finally, gender (β = − 0.008, t = -0.883, p > 0.05) and online payment experience (β = 0.009, t = 0.955, p > 0.05) had statistically insignificant relationships with consumers’ intentions to use Bitcoin for online payments, and a statistically insignificant relationship between online payment experience and WOM of using Bitcoin for online payments (β = 0.009, t = 1.018, p > 0.05).

Discussion

This study’s objectives were twofold. First, the study aimed to examine the important factors (e.g. perceptions of usefulness and ease of use, trust and risk, and the normative pressure, mimetic pressure, and coercive pressure) that determine consumers’ use intentions of Bitcoin for online payments and WOM recommendations. Second, the study aspired to ascertain the role of perceived self-efficacy in moderating the impact of perceptions of usefulness and ease of use, and trust and risk evaluations on consumers’ intentions to use Bitcoin for online payments and on their WOM.

The study’s analysis shows the constructs of the TAM (i.e. perceived usefulness and perceived ease of use) to be instrumental explanatory variables of consumers’ use intentions towards Bitcoin for online payments and their WOM. This means that when consumers find using Bitcoin for online payments to be significantly useful and relatively easy to use, they may not only form positive intentions towards its use, but could also spread positive WOM about this innovation to others. The results presenting the perceived usefulness intentions relationship concur with those of previous studies on Bitcoin [4, 91, 117, 126], while the findings presenting the perceived ease of use intentions relationship are similar to those from the research of Shahzad et al. [126]. Interestingly, the level of influence that perceptions of usefulness and ease of use have on consumers’ WOM of Bitcoin online payments has not been examined so far in the literature.

This scholarly work shows that perceptions of trusting the use of the Bitcoin electronic payment system and the risk associated with processing of its online payments can influence customers’ intentions to use it for online retail payments. These findings corroborate those of earlier research by Mendoza-Tello et al. [91], which showed trust to be an enabler of Bitcoin adoption intention and perceived risk to hinder consumer innovation adoption [11]. Trust in the Bitcoin system for online payments provides structural assurance and dependability, which are widely considered to be critical determinants of e-commerce success [67, 88]. Similarly, the role of customers’ risk perceptions as barriers to the growth of e-commerce have been widely acknowledged [147, 152, 153], thus their role in this study serves as a dampener of consumers’ intentions to use Bitcoin for online payments, as shown in the literature.

Furthermore, this study reports that customers’ trust in Bitcoin for online payments influences their WOM. Interestingly, the effect of the trust–use intentions relationship (β = 0.216) is similar to that of the trust–WOM relationship (β = 0.214), suggesting that customers’ trust in the use of Bitcoin for online payments plays an equal role in their intentions to use Bitcoin for online payments and their WOM. Moreover, the effect of the risk perceived by customers on their use intentions towards Bitcoin for online payments is similar to that of the risk–WOM relationship. These results not only reveal the consistency of the impact of customers’ trust on their Bitcoin use intentions and their WOM, but also show that the strength of the impact that customers’ risk perceptions have on their Bitcoin use intentions could almost equal its impact on the WOM recommendations.

Concerning the role of social contagion factors in consumers’ use intentions towards Bitcoin for online payments and their WOM, we observed that while mimetic pressure could engender consumers’ positive intentions to use Bitcoin for online payments, it induces negative WOM from consumers. This means that consumers could “voluntarily” use Bitcoin for online payments, but such actions could result in negative WOM. Self-determination theory [122] might support this interesting finding. The use of “voluntary workshops” could induce an engagement that may encourage consumers’ autonomy in expressing their strong opposition to such practices through negative WOM. The results further suggest that, while normative pressure might not influence consumers’ intentions to use Bitcoin for online payments, it could influence their WOM recommendations. This means that consumers are not influenced to use Bitcoin for online payments if other people whom they admire use it. The fact that the same consumers who do not want to use Bitcoin for online payments—despite its popularity among people who are familiar to them—would unconsciously spread positive WOM about the innovation is quite interesting. This finding could explain that consumers’ WOM behaviour is a function of normalcy. Last, the results show that consumers’ intentions to use Bitcoin for online payments and their WOM could be explained by coercive pressure. This emphasises that the pressure consumers experience to conform to other consumers’ behaviour through threats or punishment could drive their intentions to use Bitcoin for online payments and to spread positive WOM. These findings corroborate those of Mena and Schoenherr [89] and Scott [125], who underscored the criticality of the coercive dimension of social contagion in influencing consumer behaviour.

Our findings also suggest that consumers with intentions to spread positive WOM messages about using Bitcoin for online payments are likely to develop positive intentions to use the innovation. This observation is supported by prior studies [38, 65, 115] that have found consumers’ WOM to positively influence their intentions to buy. Furthermore, the results show that consumers’ self-efficacy in making online payments utilising Bitcoin is fundamental to strengthening their perceptions of the usefulness and ease of use of Bitcoin for online payments and their WOM, respectively. Moreover, the results demonstrate that higher perceptions of self-efficacy reduce the impact of risk evaluation in negatively affecting consumers’ intentions to use Bitcoin for online payments and their WOM. Finally, the research indicates that self-efficacy reinforces customers’ trust in the use of Bitcoin for online payments. These findings not only validate an innovative approach that understanding the mechanism through self-efficacy affects consumers’ beliefs about the use of Bitcoin blockchain innovation, but also underline the criticality of self-efficacy as an individual difference variable that explains consumers’ innovation acceptance behaviour [140, 151].

Theoretical contributions

The study makes several crucial theoretical contributions to the literature. First, it integrates the TAM, valency theory, social contagion theory, and self-efficacy theory into a comprehensive theoretical model, reconciling what was previously treated as independent strands in the literature. By examining these theories together, the study demonstrates how the variables from these theories collectively influence consumers’ intentions to use Bitcoin for online payments and their positive WOM recommendation. The substantial variance that is explained—75% and 80% in Bitcoin use intentions and WOM, respectively—underscores the significance of the integrated theoretical framework in providing a robust explanation for customers’ intentions and their positive WOM recommendations about Bitcoin cryptocurrency payments in online retailing, thus representing a crucial contribution to the literature. This is because previous studies have not incorporated these theories comprehensively, leading to less variance being explained.

Second, while social contagion theory (e.g. the dimensions of coercive pressure, mimetic pressure, and normative pressure) has been acknowledged as a crucial driver in consumer innovation behaviour, previous studies on cryptocurrencies have largely overlooked its role in consumers’ adoption behaviour. The present study fills this gap by revealing that while coercive and normative pressure significantly impact use intentions, the impact of mimetic pressure on Bitcoin use for online payments is not significant. Moreover, the study demonstrates that the dimensions of social contagion explain consumers’ WOM more effectively than their intentions to use Bitcoin for online payments. These findings offer an original contribution to the literature by elucidating how the social contagion factors of coercive pressure and normative pressure—not mimetic pressure—concurrently explain WOM behaviour about Bitcoin use for online payments, although its use intentions are explained only by coercive pressure and mimetic pressure, and not normative pressure.

Third, while the constructs of perceived ease of use and perceived usefulness from the TAM have been extensively examined in the literature, their impact on consumers’ WOM has received less attention. This study extends the literature on cryptocurrency and Bitcoin by confirming the influence of perceived usefulness and perceived ease of use in explaining customers’ intentions to use Bitcoin for online payments and by highlighting their central role in explaining customers’ WOM. These findings are significant, as they expand previous research that mainly focused on the explanatory role of perceived usefulness and perceived ease of use in Bitcoin use intentions, thus advancing our understanding of the drivers of consumers’ WOM recommendations.

Fourth, considering that using Bitcoin for online payments is a relatively new approach in e-commerce, consumers’ self-efficacy becomes instrumental in reinforcing their perceptions of the innovation’s instrumental attributes of trust and risk. The study’s findings on the moderating role of self-efficacy explain how self-efficacy serves as a boundary condition that influences the relationships between perceived usefulness, perceived ease of use, trust, perceived risk, and the behavioural outcomes of Bitcoin use intentions and WOM. This unique contribution to the literature highlights the significance of self-efficacy in shaping consumers’ beliefs, strengthening the effects of other factors on Bitcoin use intentions and WOM.

Managerially, this research offers valuable contributions by providing insights that could assist online merchants in understanding the factors influencing consumers’ intentions to use Bitcoin for online payments and their WOM. The study also highlights the role of consumers’ self-efficacy beliefs in using Bitcoin for online payments and their impact on consumers’ instrumental beliefs about the innovation. It reveals that consumers’ confidence in their ability to use Bitcoin could reinforce or weaken their beliefs about this blockchain payment method. This knowledge is essential for online merchants and other stakeholders who seek to promote the use of Bitcoin for online payments, mainly in emerging countries like South Africa and in similar contexts.

Practical implications

This study raises several managerial implications for those interested in promoting the adoption of cryptocurrencies, specifically Bitcoin, for online payments. First, the study shows that the constructs of the TAM—perceived usefulness and ease of use—remain significant factors to consider in positively driving consumers’ use intentions towards Bitcoin for online payments and WOM. Thus, if managers want to increase consumers’ intentions to use Bitcoin and promote positive WOM, they need to stimulate consumers’ perceptions of the usefulness of the functional benefits they could derive from using Bitcoin innovation for online payments, such as quicker and more secure transactions at relatively lower fees. Messages that emphasise and reinforce these benefits could be developed by managers in simple and clear language that their target market understands, and presented to them using the appropriate marketing channels. Similarly, consumers’ perceptions of Bitcoin’s ease of use for online payments could be promoted by designing e-commerce sites that make it easy to use this innovation. Managers need to display all the steps involved in the online shopping process—from ordering and payments to the delivery of the purchased items. When customers complete an order, online retailers must transfer the buyers to a payment page with clear and easy-to-read payment instructions. Redirecting buyers to the recipient wallet address of online retailers and displaying the cost to be transferred are some tactics that may increase the perceived ease of use in initiating the transaction. As a short time frame (e.g. less than 15 min) is usually allocated to initiate the payment, the payment process should be brief with a minimum number of clicks mainly to mitigate the risk of exchange loss for online retailers caused by the volatility of cryptocurrency rates.

Educational marketing programmes could be initiated on social media networks and above-the-line media to institute learning through influencers, opinion leaders, testimonial comments, and vigorous marketing to familiarise customers with cryptocurrencies, specifically Bitcoin for online payments. When consumers believe that using a Bitcoin payment method is easy (i.e. effortless), the adoption of Bitcoin and its perceived usability may increase. This could result in a positive intention to use, which might also make customers more eager to spread positive WOM about Bitcoin for online payments.

Second, our research indicates that the social contagion factors of coercive and mimetic pressures are predictors that explain Bitcoin use intentions, while normative and coercive pressures as predictors explain WOM. This suggests that managers could develop a market expansion strategy exploiting the advantage of the contagious effects of normative pressure that consumers experience to conform with others whose approval motivates their use intentions of Bitcoin for online payments and spread positive WOM about such innovative modes of payments. Managers could successfully target and position Bitcoin for online payments among early adopters and potential buyers by providing discounts, coupons, vouchers, gift cards, payment terms (e.g. interest-free credit), group buying, refunds, and guarantees, which could increase consumers’ use intentions towards Bitcoin for online payments and their WOM.

Third, the results show that managers who want to increase trust and then reduce perceived risk as considerable factors of valence theory that influence consumers’ intentions to use Bitcoin and spread positive WOM could pre-empt moves by instilling consumers’ confidence in the use of Bitcoin for online payments. Providing security mechanisms (e.g. cryptography, encryption), showing users the product to be purchased with a price in the selected cryptocurrency, and offering quick response (QR) codes/matrix barcodes with scanning functionality on the app in easy steps might help to achieve this goal. It might not be sufficient to trust only the code supplied by online retailers; users should also be trusted and engaged while using the Bitcoin cryptocurrency. As the leading cryptocurrency, Bitcoin should be recognised as a “risk-free” cryptocurrency and/or as one that reduces perceived risk to a minimum level against other current cryptocurrencies available.

Fourth, our study emphasises the importance of managers increasing consumers’ perceived self-efficacy—that is, improving users’ comfort beliefs when they access and utilise the services to the point of believing in their capabilities to perform this function. Users need the correct online retailer’s address and the capability to open their crypto wallet, insert the required amount, and then authorise the transfer of the Bitcoin. Through strategic planning initiatives, policymakers and governments could promulgate laws and regulations that suit the online shopping environment for Bitcoin to gain market trust and certainly reduce consumers’ perceptions of risk about its use for online payments. Our study shows that managers who cultivated this capability among users to use Bitcoin to purchase from online stores generate trust and reduce risk perceptions, which could stimulate use intentions and WOM. Immediately after detecting the completion of a payment by a user, the online retailer must send a notification message informing the buyer that the payment has been processed. Upon sufficient confirmations made on the blockchain ledger, the online retailer should confirm the completion of the transaction and authorise delivery of the product or service to the user. Given the risks related to uses of cryptocurrencies (e.g. volatility, network attacks, and lack of regulation) [91], online retailers could succeed by providing easy-to-read instructions, guidelines, and detailed information to consumers prior to them making electronic payments with Bitcoin.

Finally, our study offers direction for a market segmentation strategy for online retailers targeting different consumer groups. It suggests that to prosper, online retail practitioners could tailor their sales promotion campaigns about the use of Bitcoin for online payments to different age cohorts, and use creative advertising that targets specific genders to stimulate topics of Bitcoin use for online payments, predominantly for mobile device apps, as the preferred device consumers for online shopping. The prominence of these initiatives on online shoppers with use intentions towards Bitcoin for online payments could significantly increase positive WOM. Building stable comfort for users when they access and use such services may instil the belief that they have the capability to use Bitcoin for online shopping and strengthen the perception of its usefulness, ease of use, and trust, while reducing risk perception, which together could increase use intentions and the spread of positive WOM.

Conclusion and recommendations for future research

When conducting this research, we developed, proposed, tested, and validated the research model that examined the extent to which valence, social contagion, and TAM factors simultaneously influence consumers’ use intentions towards Bitcoin for online payments and their WOM. The findings suggest that when consumers perceive usefulness and ease of use as positively increasing their use intentions towards Bitcoin for online payments, they also increase their positive WOM recommendations in South Africa’s online retail sector. Perceived risk negatively affects use intentions towards Bitcoin for online payments and WOM; yet trust could positively instil these intentions and WOM. Mimetic and coercive pressures affect consumers’ use intentions towards Bitcoin for online payments, but normative pressure does not. Surprisingly, coercive pressure and normative pressure predict WOM, but mimetic pressure does not. These factors have explained 75% and 80% of intention towards Bitcoin use for online payments and WOM, respectively.