Abstract

The current study analyzes the time–frequency dependencies between financial development (FD) and electrical power consumption (EPC) in the Gulf Cooperation Council (GCC) Countries (Qatar, Saudi Arabia, Kuwait, the United Arab Emirates, Oman, and Bahrain) during the period 1980–2017. The practical examination is based on the wavelet squared coherence that allows assessing the co-movement between the selected variables of FD and EPC. The main objective of this study is to investigate the short- and long-term dependencies between FD for the GCC countries and EPC to provide helpful insights to policy makers, investors, and government to show them if FD is influenced by EPC in GCC countries. Most of previous related studies have employed co-integration, causality, and panel data techniques. However, this study will be the first study that uses the wavelet coherence analysis to examine the relationship between EPC and FD. The results show periodic changes in the model of the co-movements especially after 2008 for all countries at comparatively high frequencies. Besides, the results indicate strength of co-movement varies by country. Such as a high degree of co-movement between the electrical power consumption and financial development in United Arab Emirates, Kingdom of Saudi Arabia, and Qatar, while low co-movement with Kuwait and Bahrain. The result as well document a comprehensive change in electrical power consumption and financial development co-movement after 2008 at comparatively low frequencies especially in Kuwait, Oman, and Bahrain. The results of the current study provide prospective importance implications for policy makers in improving energy plans for GCC countries that redound to EPC depression policies whereas conserving financial development.

Similar content being viewed by others

Introduction

Various researches have investigated the relationship between electrical power consumption (EPC) and financial development (FD), precisely in the recent three decades in various countries for instance [6, 11, 26, 29, 37, 42, 44, 50]. In addition, numerous previous studies presented a robust relationship between the EPC, economic growth, and FD. This suggests that a rise in EPC immediately influences FD and economic growth (see [4, 16, 22, 24, 25, 42, 45, 46]).

Most of the previous studies utilized their methodologies both of time series (see, [9, 11, 26, 48]) and panel data analysis (see, [6, 18, 40, 41]). A large body of empirical studies debates the relationships between the EPC, economic growth, and FD by using the directions of granger causality interconnection that possibly classified as four sections: First, unidirectional assumption runs from FD, economic growth to electricity consumption. In this case, electricity preservation policies prepared to reduce electricity consumption and waste will have a few or no impact on economic growth. Second, the bidirectional hypothesis declares that there are two-ways causality relationships existed between FD and EPC. Third, growth assumption implies that causality runs from EPC to FD. Ozturk and Acaravci [32] indicate that EPC contributes essential function in the process of FD. For that case, the reduction in EPC due to electricity conservation policies may have a catastrophic impact on FD.

Fourth, neutrality hypothesis states that if there is no causal correlation running from EPC to FD, the electricity consumption will have no impact on financial development [16]. Also, Salahuddin et al. [42] found significant and negative association between EPC and FD, and this indicates that EPC and GDP prompt CO2 emissions for GCC, while FD decrease it. However, neutral causality relationship between financial development and CO2 emissions is found by this study. It is very important for different parties such as for government to test the causality direction to construct and apply implications for electricity policies. Thus, it is essential to attain whether there is an existence of causality relationship between FD and EPC with its direction.

What distinguishes this paper from the reviewed literature is that this paper is from the pioneer’s studies that applied one of the synchronous time series mechanisms of wavelet analysis. Wavelet analysis techniques are very appropriate to study the sequential destination for financial variables. Most of the previously related studies have employed co-integration, causality, and panel data techniques. However, this study will be the first study that uses the wavelet coherence analysis to examine the relationship between EPC and FD. Wavelets permit one to run with a non-stationary time series, and it keeps the time-centralized information and, thus, qualifies the measurement of co-movement in the time–frequency area. Wavelet technique is stem from the wavelet transform, whither the index is transformed with the assistance of mission called wavelets. A wavelet mission is a short wave that has a beginning and an ending. Operating those waves by moving them in time and compressing them allows one to perform a series, non-stationary signal as time–frequency elements that are centralized in time [19].

This study contributes to the existing literature by incorporating the impact of two important production factors of EPC and FD and by expanding the production function applying EPC as one of the input variables.

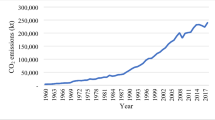

Electricity consumption is increasing worldwide as populations’ electrical power consumption is rising constantly, as people are increasingly having the willingness and the ability to add more electrically powered devices that are highly used in their daily activities than before [35]. Based on recent annual report of International Renewable Energy Agency (IRENA), 2019, the report links the plenty financial development represented by commercial projects and new housing across the GCC over the past decade. The regional EPC grew at an average rate of 7% per annum between 2006 and 2016, faster than anywhere else in the world. Oman and Qatar saw the steepest overall rise in electricity consumption, the consumption growth in Oman reach to 20% (see Fig. 1).

Energy consumption by sector in GCC with comparative of USA, Europe, and the world

Essentially, the destruction into time frequency and the position of the mutuality between sub-time series are the main two closely estimated ranges of the wavelet tools in finance [3]. Growing EPC in integration with high-rate energy bill and ecological warnings show a functional defy for GCC nations. There is pressing necessity to design sustainable and renewable energy mechanisms that can resist the further defies. The main objective of this study is to investigate the short- and long-term dependencies between FD for the GCC countries and EPC to provide helpful insights to policy makers, investors, and government to show them if FD is influenced by EPC in GCC countries. Moreover, the study attempts to answer two research questions in particular: First, does movement in EPC over time affect the FD of GCC markets? Second, which country among GCC is most affected by EPC co-movement?

The results proved very low co-movement and dependence between the EPC and FD variables in Kuwait and Bahrain. However, the EPC is strongly related to FD over many periods especially at high frequencies with high degree of co-movement and dependence for the three countries of KSA, UAE, and Qatar. Furthermore, the results suggested high degree of co-movement in Oman for the high frequency only until the year 2010, after that it reveals less dependent between EPC and FD.

The rest of the study is structured as follows: the next section explores the previous literature. Literature review” section illustrates the study methodology and data. “Methods” section presents the empirical results, while conclusion and policy implications are presented in the last section.

Literature review

The relationship between economic growth, EPC, energy consumption, and FD have attracted many researchers such as Bekhet and Matar [8], April), Bekhet et al. [9], Cowan et al. [14], Matar and Bekhet [26], Ntanos et al. [28], Omri et al. [30], Onuonga [31], Ozturk and Acaravci [33], Sbia et al. [43], Shahbaz et al. [47], Sunde [49], Tang et al. [50], Yildirim et al. [54].

Using panel data for 22 emerging countries, Sadorsky [40] found a positive relationship between financial development and energy consumption. The same previous author [41] found the same result when he applied the same method on 9 Central and Eastern European frontier economies. However, no significant relationship is found by Coban and Topcu [12] in the EU27 using GMM model.

Rashid and Yousaf [37] applied GMM approach along with principal component analysis and suggested a significant positive linkage between electricity consumption and financial development in India and Pakistan.

Ziaei [56] examined the effects of financial development on energy consumption and CO2 emissions by using panel vector auto-regression (PVAR) in 13 European and 12 East Asia and Oceania countries. He found that energy consumption and CO2 emission shocks on financial indicators such as private sector credit are not very pronounced in both groups of countries.

Gaies et al. [18] investigated the relationship between energy consumption and financial development in the MENA countries by applying linear and nonlinear dynamic panel model. They suggested a positive significant relationship between FD and energy consumption.

By applying cross-country panel data from 21 transitional countries, Yue et al. [55] found that there are no significant linear relationships between financial development and energy consumption. However, FD does have significant nonlinear impacts on energy consumption in transitional countries.

Tang et al. [50] examined the relationship between EPC and FD, and FDI. He found that GDP, FD, exchange rate, and macroeconomic uncertainty are positively related to FDI. Cowan et al. [14] suggested various results for the granger causality (neutral, bidirectional, and unidirectional) between EPC, CO2, and GDP in the BRICS nations. Wolde-Rufael [52] examined the causal relationship between electricity consumption and economic growth for 15 countries. He found neutral causality in Moldova, Slovenia, Albania, and Serbia; in Belarus and Bulgaria a unidirectional running from EPC to economic growth and bidirectional causality in Ukraine.

By applying panel data for the period of 1980–2012, Salahuddin et al. [42] examined the relationship between EPC, FD, economic growth, and CO2 emissions in the GCC countries. They found a positive long-run relationship between EPC, economic growth, and CO2 emissions and negative relationship between FD and CO2 emissions. Salahuddin et al. [42] analyzed the short-run and long-run effects of FD, GDP, imports, export, and capital on EPC in Japan by using ARDL co-integration model. Their results indicated that 1% rise in FD, import, export, and GDP will increase the load on EPC by 0.24%, 0.21%, 0.09%, and 0.50%, respectively.

Matar and Bekhet [26] investigated the dynamic relationship among the FD, GDP, EPC, and export in Jordan over the 1976–2011 period by employing ARDL approach and granger causality test. They found a long-term equilibrium relationship between EPC and GDP with unidirectional causality association run from real GDP to EPC. Komal and Abbas [21] examined the impact of FD on energy consumption in Pakistan by using the system GMM estimation technique. They found that FD has positive impact on energy consumption. Moreover, they found positive impact of economic growth and urbanization on energy consumption, while the impact of energy prices over energy consumption is negative.

Shahbaz et al. [48] explored the asymmetric relationship between FD, economic growth, and energy consumption by using NARDL bounds testing approach. The results suggested co-integration among the variables and indicated that the negative shocks to FD have impacts on economic growth. Bekhet et al. [9] analyzed the causal relationships among FD, GDP, and CO2 for GCC countries by using ARDL bound testing approach. The results indicated a long-run and causal relationships among FD, GDP, CO2, and energy consumption for all GCC nations with the exception of UAE.

Nur-Syazwani [29] investigated the relationship between EPC and GDP in Malaysia over the 1971–2014 period by employing ARDL bounds testing approach. The results showed that there was a co-integration between EPC and GDP, and also the study suggested that EPC, and FDI positively affected GDP in the short-run. The study recommended improving current energy production and motivating the exploration of alternative energy sources to promote economic growth in Malaysia. Bouznit et al. [11] analyzed the relationship between EPC and income GDP for Algeria over the 1970–2013 period by using ARDL bound testing approach. The results showed that the relationships between electricity use and GDP present an inverted N-shape, with the second turning point having been reached. Moreover, the results suggested to increase the electricity production by renewable energy sources to meet the increasing demand.

Baloch and Meng [6] found that electricity consumption granger causes financial development in OECD countries. Pata [34] suggested that financial development increases the environmental degradation and causes great increase in CO2. Destek and Sarkodie [15] found that there is inverted U-shaped relationship between financial development and ecological footprint.

By employing the wavelet analysis, the current paper is distinguished from the previous literature since most of the previous literature using the relationship between these variables by employing co-integration and panel data tests.

Methods

Different models have been applied to investigate the relationship between energy consumptions, EPC, and GDP by using various co-integration and causality models such as Al-Iriani [1], Al-Mulali [2], Arouri et al. [5], Boutabba [10], Farhani and Ben Rejeb [17], Mehrara [27], Wolde-Rufael [52], and Tang and Ozturk (2014).

Numerous studies have applied the wavelet coherence model to analyze economic and financial time series but with different variables. For instance, Grinsted et al. [20] Ramsey and Lampart [36], Rua and Nunes [39], and Torrence and Compo [51] provided detailed and formal description of wavelet approach. Through wavelet approach, time series can be consisted into frequency elements. Whereas the determined tool for frequency elements, the totally eligible of symbolizing a stationary time series is Fourier analysis.

Rua [38] developed a new wavelet-based measure of co-movement, which enables to examine the co-movement both at frequency level and over time domain. This new scale permits one to observe change of the degree of co-movement over time periods and frequencies. This spectral analysis provides a more unified framework by incorporating the time dependence of the co-movement.

Wavelet is short wave that starts at a specific period in time and finishes at a later final specific period in time. Fourier analysis can be noticed as an expansion of the wavelet analysis with some beneficial features for close out the data into various frequencies. This close out feature gives the ability to study the different return layers that comprise the total returns as an alternative of studying the returns from different durations. Wavelets have been widely looked out in economic and finance with only a small exclusion [7]. It is originally time series analysis, and there are three types of wavelet analysis, the first one is continues with the function w(t) that has two properties with zero mean and unit energy:

Following Ramsey and Lampart [36], Rua and Nunes [39], and Aloui and Hkiri [3], the continuous wavelet transform of a discreet time series is given by:

where u represents the scale, s is the time position and * denotes a complex conjugate. The major utility of wavelet transform is the capacity to reconstruct and thus decompose the model x(t) as follows:

The major advantage of the wavelet modify is the power conservation of the chosen time series. This feature is utilized for the power spectrum technique that assigns the variance as:

To examine the cross-correlation behavior during the time period and frequency, we apply the wavelet square coherence by introducing first cross-wavelet transform, second the wavelet squared coherence as following (6) and (7) models, respectively [51].

The express wavelet switch is defined of two variables x(t) and y(t) with the continuous switches of \(wx\left( {u,s} \right)\) and \(wy\left( {u,s} \right)\) where, u is the position index, s is the scale, * refers to the complex conjugate. Eventually, to test the consistency of the cross-wavelet switches in the time frequency area, we employ the squared coherence wavelet called wavelet coherence that can be defined as:

It can be concept as a correlation coefficient with a range between 0 and 1, s denotes the smoothing parameter. In the no smoothing case, the wavelet coherence will be equal 1. In addition, the coefficients of squared wavelet coherence are in the range \(0 \le R^{2} \left( {u,s} \right) \le 1\) and their values are slight to 0 articulate low correlation, while those slight to one prove the existence of high correlation [3].

Data and preliminary findings

Quarterly data for per capita EPC and FD variables covering the period of 1980Q1–2017Q4 collected from the World Bank [53] because World Bank databases provide the sufficient and suitable data for this study. Where, an EPC represents the per capita electrical power consumption measures in kw/h and FD is a representative of domestic credit provided by financial sector (% of GDP) in GCC countries. For the wavelet analysis, the current study applied the LA (8) filter not HAAR since the HAAR filter according to Lee and Tarng [23] is not continuous and not differentiable. However, LA (8) filter achieves coefficients that are approximately uncorrelated between scales while having a filter width short enough such that the impact of boundary conditions is acceptable [13].

Table 1 shows the descriptive statistics for FD and EPC. All of the analyzed data have positive mean, Oman FD and Kuwait EPC have the highest standard deviation, while KSA for FD and Bahrain EPC have the lowest standard deviation. UAE has the largest FD skewness, at 1.0532, and Bahrain has the largest EPC skewness with 0.6335. All GCC exhibit positive kurtosis; and Oman has the highest FD kurtosis at 13.258, whereas Kuwait has the highest EPC kurtosis, at 2.4425.

In addition, results indicate that we can accept the H0 of normality whereby the distributions for all variables are normal due to the Jarque–Bera P values.

Table 2 presents the unconditional correlation between FD and EPC in the GCC. The result shows that the Qatari FD has the highest correlation with the EPC. The lowest correlation between the tested variables is found in Bahrain. The correlation of the United Arab Emirates, Saudi Arabia, Kuwait, and Oman falls in the range, from 0.0852 to 0.5427.

Results and discussion

This section discusses the results for selective countries that are shown in Figs. 2, 3, 4, 5, 6, and 7. The contour plot wavelet-based measure of co-movement is presented through three dimensions. The vertical axis represents the frequency, and the horizontal axis represents the time. To interpret the results easily, the figures are colored with various colors from the light area to (toward blue) the hot colors. Merely, the light areas (toward blue) denote the weak co-movement, while the hot areas denote the strong co-movement between the variables. Consequently, the contour plot can identify into the vertical axis for frequency strips and the horizontal axis for the time periods; the higher the frequency, the lower the scale. The time series move together and estimate if the strength of the co-movement varies toward frequencies over the time; the warmer the color is, the more dependent the series are. The figures below reveal the country pairs one by one in terms of the co-movement between EPC and FD for each country in GCC. Figures 2, 3, and 4 present the wavelet results of the KSA, UAE, and Qatar, and the figures show that EPC is highly correlated with FD over different phases especially at high frequencies with high degree of co-movement and dependence for the three countries of KSA, UAE, and Qatar. These results are in consistent with, Baloch and Meng [6], Bekhet et al. [9], Komal and Abbas [21], Wolde-Rufael [52] and Salahuddin et al. [42] and inconsistent with Bouznit et al. [11], and Destek and Sarkodie [15].

Comovement between the electrical power consumption and financial development in KSA

Comovement between the electrical power consumption and financial development in UAE

Comovement between the electrical power consumption and financial development in Qatar

Figure 5 reveals high degree of co-movement in Oman for the high frequency only until the year 2010, after that it reveals less dependent between EPC and FD. Figures 6 and 7 present the wavelet results of Kuwait and Bahrain countries, and it shows that very low co-movement and dependence between the EPC and FD variables indicate low correlation between tested variables at these countries. Thus, we can conclude that there is a small significant area of dependence on these countries. These results are in consistent with Shahbaz et al. [48], Bouznit et al. [11], and Destek and Sarkodie [15] and inconsistent with Baloch and Meng [6] and Pata [34].

Comovement between the electrical power consumption and financial development in Oman

Comovement between the electrical power consumption and financial development in Kuwait

Comovement between the electrical power consumption and financial development in Bahrain

These results are remarkable for many parties like policy makers, corporations, governments, and investors whether they are domestic or foreign. Nevertheless, the importance of this study refers to the reason that electricity bill reflects a distinguished portion in GDP for GCC countries. Besides, the costs of electricity bills are impacted by oil prices which have risen up with high rate, especially during the period of 2008-2017 refer to various economic and politic crises and events in the Middle East. Therefore, the rise in the oil prices has positively influenced the electricity costs. Most of the previous studies of the relationship between GDP and EPC have been globally performed in developed regions. So far, there seems to be no sufficient regarding the relationship in GCC countries. The main result of this study reveals robust dynamics in co-movement especially in KSA, UAE, and Qatar during different financial horizons. Our results suggest to the countries with high association between EPC and FD to pay attention regarding that and trying to find sustainable and renewable energy sources.

Conclusion, limitations, and recommendations

This study explores the co-movement relationships between EPC and FD for GCC nations. To test the co-movement relationship between the mentioned variables, the study used the wavelet analysis for the period of 1980–2017. The empirical results proved that the EPC is strongly related to FD over many periods especially at high frequencies with high degree of co-movement and dependence for the three countries of KSA, UAE, and Qatar. Furthermore, the results suggested high degree of co-movement in Oman for the high frequency only until the year 2010, after that it reveals less dependent between EPC and FD and shows very low co-movement and dependence between the EPC and FD variables in Kuwait and Bahrain. This means that in these countries the electricity consumption strategies will not influence the financial development. However, the results of strong co-movement in KSA, UAE, Qatar, and Oman indicate that EPC plays a fundamental role in FD and economic growth. The results answer the study questions that the FD is affected by EPC, and the most country is affected by EPC co-movement is Qatar. However, some limitations should be noted. First, this study is one of a very few studies that uses wavelet time series to analyze the relationship between the study variables; hence, we do not find any paper so far used this methodology which make our result incomparable with previous studies using the same method. Second, since we applied time series long period, the data are not available for six GCC from their own official websites; hence, we collect it from World bank data stream limited with annual data only. The results of the current study provide prospective importance implications for policy makers especially for the high-degree co-movement countries which indicate that they have to look out to the positive correlation between FD and EPC. Thus, the high financial development will result in high electricity consumption.

The GCC countries with high affected EPC on FD like KSA, UAE, and Qatar governments should apply the potential of renewable or alternative energy for electricity generation, such as the solar energy as this will apart from decreasing electricity bills and activate these countries economic growth, the electrical power generation from nuclear power, and controlling account deficits of some countries like KSA recently. On the electrical demand side, citizens should be made aware of the importance of effective use of electricity, particularly given our results that electricity consumption positively contributes to economic growth. Eventually, for further studies, we suggest more factors that may cause the obvious structural breaks on EPC, such as trade openness, CO2 emissions, consumer price index, investment, political events, and populations size.

Availability of data and materials

The data were available.

Abbreviations

- FD:

-

Financial development

- EPC:

-

Electrical power consumption

- GCC:

-

Gulf Cooperation Council

- KSA:

-

Kingdom of Saudi Arabia

- UAE:

-

United Arab Emirates

- GDP:

-

Gross domestic product

- ARDL:

-

Autoregressive distributed lags

References

Al-Iriani MA (2006) Energy–GDP relationship revisited: an example from GCC countries using panel causality. Energy Policy 34(17):3342–3350

Al-Mulali U (2011) Oil consumption, CO2 emission and economic growth in MENA countries. Energy 36(10):6165–6171

Aloui C, Hkiri B (2014) Co-movements of GCC emerging stock markets: new evidence from wavelet coherence analysis. Econ Model 36:421–431

Apergis N, Payne JE (2011) A dynamic panel study of economic development and the electricity consumption-growth nexus. Energy Econ 33(5):770–781

Arouri MEH, Youssef AB, M’henni H, Rault C (2012) Energy consumption, economic growth and CO2 emissions in Middle East and North African countries. Energy policy 45:342–349

Baloch MA, Meng F (2019) Modeling the non-linear relationship between financial development and energy consumption: statistical experience from OECD countries. Environ Sci Pollut Res 26(9):8838–8846

Basdas, U. (2012). Interaction between MENA stock markets: a comovement wavelet analysis. Available on: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2333774

Bekhet HA, Matar A (2013) The Impact of global financial crisis on the economic growth and capital market returns: evidence from Jordan. In: the twelfth scientific annual international conference for business (human capital in a knowledge economy), pp 22–25, Apr 2013

Bekhet HA, Matar A, Yasmin T (2017) CO2 emissions, energy consumption, economic growth, and financial development in GCC countries: dynamic simultaneous equation models. Renew Sustain Energy Rev 70:117–132

Boutabba MA (2014) The impact of financial development, income, energy and trade on carbon emissions: evidence from the Indian economy. Econ Model 40:33–41

Bouznit M, Pablo-Romero M, Sánchez-Braza A (2018) Residential electricity consumption and economic growth in Algeria. Energies 11(7):1656

Çoban S, Topcu M (2013) The nexus between financial development and energy consumption in the EU: a dynamic panel data analysis. Energy Economics 39:81–88

Cornish CR, Bretherton CS, Percival DB (2006) Maximal overlap wavelet statistical analysis with application to atmospheric turbulence. Bound-Layer Meteorol 119(2):339–374

Cowan WN, Chang T, Inglesi-Lotz R, Gupta R (2014) The nexus of electricity consumption, economic growth and CO2 emissions in the BRICS countries. Energy Policy 66:359–368

Destek MA, Sarkodie SA (2019) Investigation of environmental Kuznets curve for ecological footprint: the role of energy and financial development. Sci Total Environ 650:2483–2489

Faisal F, Tursoy T, Gunsel Resatoglu N, Berk N (2018) Electricity consumption, economic growth, urbanisation and trade nexus: empirical evidence from Iceland. Econ Res 31(1):664–680

Farhani S, Ben Rejeb J (2012) Energy consumption, economic growth and CO2 emissions: Evidence from panel data for MENA region. University of Sousse, Tunisia

Gaies B, Kaabia O, Ayadi R, Guesmi K, Abid I (2019) Financial development and energy consumption: is the MENA region different? Energy Policy 135:111000

Graham M, Nikkinen J (2011) Co-movement of the Finnish and international stock markets: a wavelet analysis. European Journal of Finance 17:409–425

Grinsted A, Moore JC, Jevrejeva S (2004) Application of the crosswavelet transformand wavelet coherence to geophysical time series. Nonlinear Process Geophys 11:561–566

Komal R, Abbas F (2015) Linking financial development, economic growth and energy consumption in Pakistan. Renew Sustain Energy Rev 44:211–220

Lai TM, To WM, Lo WC, Choy YS, Lam KH (2011) The causal relationship between electricity consumption and economic growth in a Gaming and Tourism Center: the case of Macao SAR, the People’s Republic of China. Energy 36(2):1134–1142

Lee B, Tarng YS (1999) Application of the discrete wavelet transform to the monitoring of tool failure in end milling using the spindle motor current. Int J Adv Manuf Technol 15(4):238–243. https://doi.org/10.1007/s001700050062

Lorde T, Waithe K, Francis B (2010) The importance of electrical energy for economic growth in Barbados. Energy Econ 32(6):1411–1420

Malik MNA, Masih M (2018) The relationship between energy consumption, financial development and economic growth: an evidence from Malaysia based on ARDL

Matar A, Bekhet HA (2015) Causal interaction among electricity consumption, financial development, exports and economic growth in Jordan: dynamic simultaneous equation models. Int J Energy Econ Policy 5(4):955–967

Mehrara M (2007) Energy consumption and economic growth: the case of oil exporting countries. Energy Policy 35(5):2939–2945

Ntanos S, Skordoulis M, Kyriakopoulos G, Arabatzis G, Chalikias M, Galatsidas S et al (2018) Renewable energy and economic growth: evidence from european countries. Sustainability 10(8):2626

Nur-Syazwani M (2018) The impact of electricity consumption on economic growth in Malaysia: evidence from ARDL bounds testing (Kesan Penggunaan Elektrik kepada Pertumbuhan Ekonomi di Malaysia: Bukti dari Pemeriksaan ‘ARDL Bounds’). Jurnal Ekonomi Malaysia 52(1):223–233

Omri A, Mabrouk NB, Sassi-Tmar A (2015) Modeling the causal linkages between nuclear energy, renewable energy and economic growth in developed and developing countries. Renew Sustain Energy Rev 42:1012–1022

Onuonga, S. M. (2012). The relationship between commercial energy consumption and gross domestic income in Kenya. The Journal of Developing Areas, 305-314

Ozturk I, Acaravci A (2011) Electricity consumption and real GDP causality nexus: evidence from ARDL bounds testing approach for 11 MENA countries. Appl Energy 88(8):2885–2892

Ozturk I, Acaravci A (2013) The long-run and causal analysis of energy, growth, openness and financial development on carbon emissions in Turkey. Energy Econ 36:262–267

Pata UK (2018) Renewable energy consumption, urbanization, financial development, income and CO2 emissions in Turkey: testing EKC hypothesis with structural breaks. J Clean Prod 187:770–779

Qader MR (2009) Electricity consumption and GHG emissions in GCC countries. Energies 2(4):1201–1213

Ramsey JB, Lampart C (1998) The decomposition of economic relationship by time scale using wavelets: expenditure and income. Stud Nonlinear Dyn Econ 3:23–42

Rashid A, Yousaf N (2015) Linkage of financial development with electricity-growth, nexus of India and Pakistan. EuroEconomica 34(2):151–160

Rua A (2010) Measuring comovement in the time–frequency space. J Macroecon 32(2):685–691

Rua A, Nunes LC (2009) International comovement of stock market returns: a wavelet analysis. J Empir Finance 16(4):632–639

Sadorsky P (2010) The impact of financial development on energy consumption in emerging economies. Energy Policy 38(5):2528–2535

Sadorsky P (2011) Financial development and energy consumption in Central and Eastern European frontier economies. Energy Policy 39(2):999–1006

Salahuddin M, Gow J, Ozturk I (2015) Is the long-run relationship between economic growth, electricity consumption, carbon dioxide emissions and financial development in Gulf Cooperation Council Countries robust? Renew Sustain Energy Rev 51:317–326

Sbia R, Shahbaz M, Hamdi H (2014) A contribution of foreign direct investment, clean energy, trade openness, carbon emissions and economic growth to energy demand in UAE. Econ Model 36:191–197

Shahbaz M (2011) Electricity consumption, financial development and economic growth nexus: a revisit study of their causality in Pakistan. University Library of Munich, Germany

Shahbaz M, Lean HH (2012) The dynamics of electricity consumption and economic growth: a revisit study of their causality in Pakistan. Energy 39(1):146–153

Shahbaz M, Hye QMA, Tiwari AK, Leitão NC (2013) Economic growth, energy consumption, financial development, international trade and CO2 emissions in Indonesia. Renew Sustain Energy Rev 25:109–121

Shahbaz M, Sbia R, Hamdi H, Ozturk I (2014) Economic growth, electricity consumption, urbanization and environmental degradation relationship in United Arab Emirates. Ecol Ind 45:622–631

Shahbaz M, Van Hoang TH, Mahalik MK, Roubaud D (2017) Energy consumption, financial development and economic growth in India: new evidence from a nonlinear and asymmetric analysis. Energy Econ 63:199–212

Sunde T (2020) Energy consumption and economic growth modelling in SADC countries: an application of the VAR Granger causality analysis. Int J Energy Technol Policy 16(1):41–56

Tang CF, Yip CY, Ozturk I (2014) The determinants of foreign direct investment in Malaysia: a case for electrical and electronic industry. Econ Model 43:287–292

Torrence C, Compo GP (1998) A practical guide to wavelet analysis. Bull Am Meteorol Soc 79:61–78

Wolde-Rufael Y (2014) Electricity consumption and economic growth in transition countries: a revisit using bootstrap panel Granger causality analysis. Energy Econ 44:325–330

World Bank (2018) GCC. Available from: http://www.data.worldbank.org/country. Accessed 10 Feb 2018

Yildirim E, Aslan A, Ozturk I (2014) Energy consumption and GDP in ASEAN countries: bootstrap-corrected panel and time series causality tests. Singap Econ Rev 59(2):1–15

Yue S, Lu R, Shen Y, Chen H (2019) How does financial development affect energy consumption? Evidence from 21 transitional countries. Energy Policy 130:253–262

Ziaei SM (2015) Effects of financial development indicators on energy consumption and CO2 emission of European, East Asian and Oceania countries. Renew Sustain Energy Rev 42:752–759

Acknowledgements

The author is grateful for Dr. Mahmoud Al-Radaydeh for his ongoing assistance in the technical analysis by providing the software packages such as R programming and its manual and to Jadara University policies on its encouragement the scientific researches.

Funding

I confirm that there are no known conflicts of interest associated with this publication and there has been no significant financial support for this work that could have influenced its outcome.

Author information

Authors and Affiliations

Contributions

All contributions of this manuscript with all its sections belong to the individual author who is the main and corresponding author. The author read and approved the final manuscript.

Corresponding author

Ethics declarations

Competing interests

The author declares that they have no competing interests.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Matar, A. Does electricity consumption impacting financial development? Wavelet analysis. Futur Bus J 6, 18 (2020). https://doi.org/10.1186/s43093-020-00017-w

Received:

Accepted:

Published:

DOI: https://doi.org/10.1186/s43093-020-00017-w