Abstract

Typical public institutions such as government offices, hospitals, and schools play important leading and exemplary roles in the green and low-carbon development of the whole society. This paper analyzes the business and energy consumption characteristics of public institutions, as well as the characteristics of personnel travel, and constructs a carbon accounting model for public institutions. It innovatively proposes a methodology for carbon accounting of personnel travel related to public institutions and validates and analyzes it using a comprehensive hospital as an example. The paper analyzes the carbon emission characteristics of various energy types, systems, and types of travelers in hospitals, provides schemes for the transformation of main energy systems, and corresponding emission reduction effects, thereby providing technical support for the full-chain carbon accounting of public institutions. Additionally, this paper explores the carbon reduction pathways for hospitals to support the peak carbon and carbon neutrality goals of public institutions, and promote the high-quality development of public institutions in China.

Similar content being viewed by others

Introduction

There are approximately 1.6 million public institutions nationwide, with a total energy consumption of 170 million tons of standard coal, accounting for about 3.5% of the total energy consumption in the whole society. They are the main link in China’s energy conservation and emission reduction efforts. Meanwhile, as the formulators, implementers, and supervisors of national energy conservation and emission reduction policies, public institutions have a strong demonstrative and leading role. In 2021, the State Administration of Government Offices issued the “Action Plan for Deepening the Green and Low-Carbon Leadership Action of Public Institutions to Promote the Implementation of Peak Carbon Emissions”, which clearly stated that the annual energy consumption of public institutions nationwide should be controlled within 189 million tons of standard coal, and the total carbon dioxide emissions (hereinafter referred to as carbon emissions) should be controlled within 400 million tons. Therefore, it is urgent to carry out research on carbon accounting of public institutions, unify accounting methods nationwide, and promote the construction of peak carbon and carbon neutrality in public institutions.

At present, research on direct carbon emissions from fossil fuel combustion, and indirect carbon emissions from purchased electricity and heat in public institutions is relatively mature. However, the accounting of direct and indirect emissions mostly involves the overall energy consumption situation, lacking analysis of the carbon emission characteristics of various energy systems in public institutions. There is limited research on other indirect emissions such as travel, domestic waste, and special consumables. Public institutions generally have relatively fixed commuting routes for permanent staff, and their service nature attracts a large number of external personnel such as patients, visitors, and audiences. The carbon emissions generated by the travel of these personnel are an important part of the carbon emissions from travel in the whole society. Currently, there is relatively little research on the carbon emissions from travel of relevant personnel in public institutions, and there is no unified and widely accepted carbon accounting method, which poses certain difficulties for public institutions in carbon reduction efforts. Therefore, studying the analysis of travel carbon emissions, especially in the field of public institutions, has strong practical significance and application value.

This paper aims to address the current state of carbon emissions in public institutions by developing a refined carbon accounting model to quantify the carbon emissions from energy consumption and personnel travel within these institutions. The research will focus on identifying the primary sources of emissions and explore effective strategies for reducing carbon emissions to assist public institutions in achieving peak carbon emissions and carbon neutrality. Additionally, the study is expected to provide references for other institutions such as government agencies, schools, and venues. To achieve the research objectives, the following methods will be employed: first, systematically collect data on energy consumption and travel data of personnel in public institutions. Second, determine the carbon emission factors for different types of energy and modes of travel. Then, using the collected data and carbon emission factors, calculate the carbon emissions from energy consumption and personnel travel in public institutions. Next, identify the primary sources of emissions through comparative analysis of the carbon emissions from different systems and activities. Finally, based on the analysis results, develop targeted measures for reducing carbon emissions and evaluate the effectiveness of these measures to verify their feasibility and effectiveness. Through these methods, this study will provide a scientific basis for the work of carbon emission reduction in public institutions and promote the progress of carbon emission reduction efforts across the entire society.

Research status at home and abroad

Approximately 40% of global carbon emissions come from the construction industry (Zarco-Periñán et al. 2022; International Energy Agency 2018). Relevant studies have shown that the main energy consumption types in buildings are natural gas and electricity (Shahrokni et al. 2014). Among major building types, hospitals have the highest carbon emissions compared to schools and government office buildings (Ma and Du 2017). Currently, common methods for carbon emissions accounting include measurement methods, material balance methods, emission factor methods, and LCA methods, with emission factor methods being more commonly used (Li et al. 2024). In terms of the accounting boundary for building carbon emissions, within the theoretical framework of the Intergovernmental Panel on Climate Change (IPCC) of the United Nations, carbon emissions from the building side are divided into direct emissions and indirect emissions based on the full statistical caliber. It is believed that the construction sector needs to focus on addressing direct emissions, including heating, domestic hot water, and cooking (IPCC 2019). The British BREEAM building assessment system sets requirements for building carbon emissions in the energy section, with the calculation boundary encompassing heating, ventilation, air conditioning, and lighting (Breeam 2019). The U.S. Green Building Council introduced the LEED Zero Carbon certification system in 2018, where carbon emissions in LEED Zero Carbon certification include the emissions generated by the electricity and fuel consumption of the building (USGBC 2018). The Zero Code 2.0 issued by “Architecture 2030” in the United States requires the calculation of carbon emissions from heating, ventilation, air conditioning, lighting, domestic hot water, and electrical outlets (Architecture 2030 2020). In 2015, the National Development and Reform Commission issued the “Guidelines for Greenhouse Gas Emission Accounting Methods and Reports for Public Building Operating Units (Enterprises)” which stipulated that public buildings should use the emission factor method to account for greenhouse gas emissions. This method involves calculating the total carbon emissions based on (Scope 1) and indirect emissions (Scope 2) by obtaining the corresponding consumption and carbon emission factors. Moreover, research on carbon emissions accounting for energy products such as refrigerators and air conditioners in direct emissions (Scope 1) and indirect emissions (Scope 2), including purchased electricity and refrigerants, has also been conducted based on international standards such as PAS 2050:2011, GHG Protocol (2011), and ISO 14067:2018, which utilize the LCA method (British Standards Institution 2008).

Studies indicate that the transportation sector accounts for one-third of greenhouse gas emissions (European Parliament News 2020), and the carbon emissions accounting of other indirect emissions (Scope 3) related to public building involves the travel of relevant personnel, which cannot be ignored. There is a certain research foundation both domestically and internationally for carbon emissions accounting in the transportation sector, mainly through “top-down” and “bottom-up” approaches (Chen et al. 2023; Yan 2018). Authoritative institutions such as the IPCC and China’s Ministry of Ecology and Environment mainly use a “top-down” approach based on energy consumption to calculate transportation carbon emissions. This method involves obtaining the total fuel consumption and corresponding fuel carbon emission factors for various modes of transportation and multiplying them to calculate travel carbon emissions, which is suitable for macro-level carbon emissions calculations at the national and regional levels. Meanwhile, in regional transportation carbon emissions accounting for areas such as cities, districts, and communities, a “bottom-up” approach based on travel data is used. This approach involves obtaining travel distances for various modes of transportation and their corresponding carbon emission factors per unit distance, multiplying them to calculate travel carbon emissions, and is suitable for small-scale transportation carbon emissions calculations directly related to travel indicators such as travel distance and turnover volume, providing clear and intuitive data. Scholars at home and abroad have conducted carbon accounting analysis and research on transportation modes and populations, and some have established methods for estimating and analyzing carbon emissions from urban passenger transportation systems (cars, rail transit, taxis, and buses) (Fan and Lei 2016; Wang et al. 2015). Li, based on the LEAP model (Li 2023), constructed a carbon emissions model for road mobile sources in Shandong Province, predicting and analyzing the peak energy consumption and direct CO2 emissions from road transportation in Shandong Province. Malik and others (Malik et al. 2021) used enterprise employees as research subjects, constructing a carbon emissions accounting model for their commuting travel to and from work.

Existing carbon reduction measures for buildings mainly (Bianco et al. 2017; Taylor et al. 2010; Nejat et al. 2015; Ali et al. 2020; Gangolells et al. 2021; Tian et al. 2019) include envelope structure reconstruction, lighting efficiency improvement, energy efficiency improvement of electrical equipment facilities, efficient cooling and heating equipment, efficient motors, and solar thermal water heating and power generation, achieving certain energy-saving and emission reduction effects.

In summary, foreign countries have achieved a certain level of maturity in accounting for direct and indirect building emissions, with consistent methods and boundaries for accounting. However, in the field of public institutions, there has been no research on accounting for indirect emissions from travel carbon emissions, and there is a lack of analysis of the travel characteristics and carbon emissions of the relevant populations visiting public institutions. Additionally, there is a relative lack of research on the analysis of carbon emission characteristics of various energy-consuming systems in buildings, and the effectiveness of corresponding carbon reduction measures for each energy-consuming system needs to be analyzed. These studies will support the efforts of public institutions to reduce carbon emissions.

Carbon accounting method in public institution

Types of energy consumption in public institutions

According to the data on energy consumption in national public institutions in 2020 (Saisai et al. 2023), it can be observed that energy consumption in public institutions mainly includes electricity, natural gas, district heating, and small amounts of coal, gasoline, diesel, etc., as shown in Fig. 1. From the perspective of energy consumption pathways, electricity is mainly used to support refrigeration systems, lighting systems, data centers, heating systems, power distribution and elevator systems, as well as special energy-consuming units such as canteens. Natural gas is mainly used for heating, domestic hot water, canteen cooking, etc. Coal is mainly used for winter boiler heating, while gasoline and diesel are mainly used for official vehicle consumption, as depicted in Fig. 2.

Distribution of energy consumption in public institutions in 2020

Schematic diagram of energy consumption types in public institutions

Scope and measurement methods of carbon emission accounting in public institutions

Carbon emission accounting in public institutions mainly includes direct carbon emissions from fossil fuel combustion, indirect carbon emissions from purchased electricity and heat, and other indirect carbon emissions. Direct carbon emissions from fossil fuel combustion include carbon emissions generated by the oxidation combustion of fossil fuels such as raw coal, natural gas, gasoline, diesel, and liquefied petroleum gas. Indirect carbon emissions from purchased electricity and heat include carbon emissions corresponding to the consumption of purchased electricity and heat by public institutions. Other indirect carbon emissions mainly encompass carbon emissions associated with round-trip commuting travel of public institution staff and external personnel to public institutions. The specific scope and measurement methods of carbon emissions are outlined in Table 1.

According to Table 1, the carbon emission accounting boundaries for public institutions are determined based on direct emissions, indirect emissions, and other indirect emissions. Specifically:

Direct emissions refer to the carbon dioxide emissions generated during the combustion of fossil fuels used in the operation of public institutions. This mainly includes emissions from the combustion of fossil fuels such as coal, diesel, gas, natural gas, liquefied petroleum gas, etc.

Indirect emissions refer to the carbon dioxide emissions associated with the production processes of purchased electricity and heat (steam, hot water) used in the operation of public institutions.

Other indirect emissions mainly include:

Transportation: Carbon dioxide emissions generated by the commuting (including business travel) of public institution staff using private vehicles, taxis, public transportation, etc. during the operation of public institutions, as well as carbon dioxide emissions generated by external personnel using public transportation during the operation of public institutions.

Calculation formula for carbon accounting in public institutions

The carbon emissions of public institutions are calculated according to formula (1).

where \(E\) is the Total CO2 emissions: measured in metric tons of carbon dioxide (tCO2). EB is the CO2 emissions from fossil fuel combustion: measured in metric tons of carbon dioxide (tCO2). EPE is the CO2 emissions from purchased electricity: measured in metric tons of carbon dioxide (tCO2). EPH is the CO2 emissions from purchased heat: measured in metric tons of carbon dioxide (tCO2). EOIE is the Other indirect CO2 emissions: measured in metric tons of carbon dioxide (tCO2). EOE is the CO2 emissions from electricity output: measured in metric tons of carbon dioxide (tCO2). EOH is the CO2 emissions from heat output: measured in metric tons of carbon dioxide (tCO2).

Due to the carbon emission accounting formulas corresponding to Scope 1 and Scope 2 can be referenced from the “Guidelines for Greenhouse Gas Emission Accounting for Public Building Operating Units (Enterprises)” (Trial), this study focuses on researching the formula for calculating carbon emissions from travel in other indirect emissions. The “top-down” approach obtains overall travel carbon emission data at the national or provincial (city) level, which is not suitable for the travel carbon emissions of public institution personnel. The “bottom-up” approach requires the collection of transportation mileage data for each mode of transportation and the corresponding carbon emission factor per unit of mileage. This article treats public institutions as a specific area where the commuting tools and distances for staff are relatively stable, and other individuals entering public institutions generally need to register their information. Therefore, it is relatively easy for public institutions to collect data on the travel mileage and modes of transportation used by related personnel. The carbon emission factors for various modes of transportation per unit of mileage are usually provided by relevant departments. Hence, this article adopts the “bottom-up” approach to account for travel data in other indirect emissions of public institutions, as shown in formula (2).

where \({E}_{{\text{OIE}}}\) is the Carbon emissions from travel mode, measured in kilograms of carbon dioxide (kgCO2); k is the Mode of travel, options include private car, rail, bus, taxi, cycling, etc.; \({EF}_{PKM,k}\) is the Emission factor per person-kilometer for mode k, measured in kilograms of carbon dioxide per person-kilometer (kgCO2/PKM), default values can be referenced for different modes of travel; \({PD}_{k}\) is the Distance traveled by relevant individuals to and from public institutions using mode k, measured in kilometers (km).

Corresponding data obtained is shown in Table 2.

Case study

A comprehensive hospital in China integrates multiple functions including medical treatment, teaching, scientific research, rehabilitation, and preventive healthcare. It serves over 1 million outpatients annually and has more than 20,000 discharged patients from its inpatient department each year. The hospital employs over 1500 medical and nursing staff members. The hospital comprises office buildings, operational areas, and logistical support facilities. The operational areas mainly include surgery departments, inpatient wards, emergency halls, radiology departments, etc. During its operation, the hospital consumes electricity, natural gas, gasoline, and diesel as its primary sources of energy. Its energy systems mainly consist of heating systems, air conditioning systems, lighting systems, production systems (medical equipment, information rooms, laboratory equipment, sterilization, clean operating rooms), and comprehensive service energy systems (drainage systems, domestic hot water systems, elevator systems, office equipment, kitchen systems). The flow of energy consumption is illustrated in Fig. 3.

The flow of energy consumption

Data collection: Detailed energy resource consumption data were obtained through the hospital's energy audit report. This data includes the types of energy consumed by the hospital over a certain period, such as electricity, natural gas, gasoline, diesel, etc.

Data analysis: According to the energy conversion coefficients for standard coal in GB/T 2589-2020 “General Rules for Calculating Comprehensive Energy Consumption,” the energy consumption of each type of energy was calculated and analyzed for its proportion; combined with Formula 1, the direct and indirect carbon emissions corresponding to each energy type in the hospital were calculated and analyzed for their proportion, as shown in Fig. 4, it can be observed that both electricity and natural gas account for 99% of energy consumption and carbon emissions. Studying the usage of electricity and natural gas in the hospital and implementing emission reduction measures is conducive to achieving carbon reduction goals.

Proportion of energy consumption and carbon emissions by energy type

Combining with the schematic diagram of electricity and natural gas consumption in Fig. 3, the consumption proportions of electricity and natural gas in various aspects of the hospital are analyzed separately. Refer to Figs. 5 and 6 for details. It can be observed that electricity consumption in the hospital is mainly used for air conditioning, lighting, large medical equipment, office equipment, elevators, clean operating rooms, heating systems, and water supply and drainage equipment. Hospital natural gas consumption is primarily for gas steam boiler heating, domestic hot water supply, lithium bromide absorption chiller heat source, cafeteria food preparation, and medical disinfection.

Proportion of electricity consumption by various systems in the hospital

Proportion of natural gas consumption by various systems in the hospital

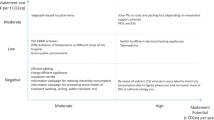

Taking into account the hospital’s primary electricity and natural gas usage, energy-saving renovations were implemented, resulting in a comprehensive energy consumption reduction rate of 11.13% and a carbon emission reduction rate of 12.19%. The main system retrofit plans and emission reduction effects are shown in Table 3.

In conjunction with formula (2), a carbon emission accounting analysis is conducted on the travel data of the hospital. The travel population includes medical staff and patients. The main modes of transportation involve cars, buses, and subways. Due to the current inability to statistically capture the travel data of medical staff on business trips and the round-trip travel data of patients for medical treatment purposes, as well as the relatively low carbon emissions from walking and cycling, this study only accounts for carbon emissions from the travel of hospital staff, outpatient and emergency patients, and inpatients within the hospital’s city, using private cars, buses, and subways as transportation methods for work and medical treatment purposes. The travel carbon emission data is compared with direct and indirect carbon emission data, and an analysis is conducted on the proportion of carbon emissions from different groups and different modes of transportation. Refer to Figs. 7, 8, 9 for details.

Hospital carbon emission distribution (scope one, two, and three)

Proportion of carbon emissions by various modes of transportation

Proportion of carbon emissions by different groups of people

Conclusions and recommendations

Discussion

In the case study of hospital carbon emission accounting, various challenges may indeed be encountered, which require innovative solutions to overcome. Here is a comprehensive discussion of the challenges and their corresponding countermeasures:

-

1.

Verification of Energy Consumption Data and Emission Reduction Effects of Major Energy-Using System Renovation Plans:

Challenge: Historical data obtained from energy audit reports may not be directly verifiable, leading to uncertainties in the accurate assessment of energy consumption and emission reduction effects.

Countermeasures: To verify energy consumption data and the emission reduction effects of major energy-using system renovation plans, a method of side verification can be adopted. For example, indirect verification can be carried out by comparing the energy resource consumption data of hospitals of similar scale. Additionally, collecting industry standard data or utilizing trend analysis of historical data can be considered to enhance the credibility of the data.

-

2.

Carbon Emission Data from Hospital Staff Travel:

Challenge: It is difficult to obtain data on the business travel of hospital medical staff and inter-city travel for patient consultations, which can affect the completeness of carbon emission accounting.

Countermeasures: In this accounting, it can be decided not to include business travel data and inter-city travel data in the carbon emission accounting. The absence of these data should be explicitly indicated in the accounting results, and their possible impact on the final accounting outcomes should be explained. Future research could consider establishing a more comprehensive travel data collection mechanism to improve the accuracy of carbon emission accounting.

-

3.

Universality of the Carbon Accounting Framework:

Challenge: The carbon accounting framework may require adjustments and optimizations when applied to different types of public institutions.

Countermeasures: For government agencies, focus on commuting traffic data of public officials and traffic data of external visitors; for schools, focus on commuting data of faculty and staff, student traffic data on campus, and traffic data during winter and summer breaks, as well as traffic data of external visitors; for venues, focus on commuting data of staff and traffic data of visitors. When dealing with inter-city commuting, special attention should be given to the collection and processing of these data, as they may account for a significant proportion. Through these specific countermeasures, the carbon accounting framework can be ensured to have higher universality and accuracy across different types of public institutions or regions.

Conclusion

In this study, based on the characteristics and relevant requirements of carbon emissions in public institutions, carbon emission accounting models for Scopes 1, 2, and 3 were investigated. Specifically focusing on Scope 3 carbon emissions related to travel in public institutions, a case study was conducted using a comprehensive hospital as an example. Through the analysis of the hospital’s energy flow, carbon emission proportions, and the proportions of carbon emissions from various energy systems, the following observations were made:

-

1.

The main energy consumption in the hospital is electricity and natural gas, accounting for 99% of the total energy consumption and carbon emissions (Scopes 1 and 2). Carbon emissions from electricity consumption (56.47%) are slightly higher than those from natural gas (42.79%), but relatively comparable.

-

2.

Regarding electricity consumption, carbon emissions are primarily contributed by air conditioning (30.04%), lighting (19.02%), medical equipment (18.29%), and office equipment (13.04%), with the air conditioning system being the main contributor to electricity consumption in the hospital.

-

3.

Regarding natural gas consumption, carbon emissions mainly come from heating (39.99%), domestic hot water (24.01%), air conditioning cooling (20.66%), dining systems (10.33%), and sterilization systems (4.92%), with heating boilers being the main contributor to natural gas consumption in the hospital.

-

4.

Current hospital renovation projects mainly focus on air conditioning systems, lighting systems, heating systems, and domestic hot water systems, covering adjustments in energy structure, utilization of new energy sources, use of energy-efficient equipment, and refined management.

-

5.

Carbon emissions from commuting of medical staff and travel of patients to the hospital account for 5% of the hospital’s overall carbon emissions. The carbon emissions from commuting are comprised of three travel modes: private cars (59%), subway (20%), and buses (21%), with patients (carbon emissions proportion: 69%) emitting more than medical staff (carbon emissions proportion: 31%), indicating that patient travel is the main source of hospital travel-related carbon emissions and private cars are the primary means of travel contributing to carbon emissions.

This research pioneeringly introduces an innovative method in the field of public institution carbon emission accounting, which, for the first time, incorporates Scope 3 (travel-related) emissions into the accounting framework alongside the traditional Scope 1 and Scope 2 emissions. This methodological breakthrough not only provides a new perspective and tool for the comprehensive assessment of public institution carbon emissions but also, through detailed empirical analysis, reveals that hospitals contribute a significant portion of carbon emissions from travel, with patient travel being the main source. This finding highlights the importance of travel behavior in the carbon footprint of public institutions and also exposes the significant impact of travel mode choices on carbon emissions. The refined carbon accounting method proposed by this study has had a profound impact on the energy management practices of public institutions, including improvements in energy efficiency, the adoption of green energy, optimization of investment decisions, and the promotion of public participation, all of which together facilitate the transformation of public institutions towards low-carbon and sustainable development.

Recommendations

Based on the analysis of hospital carbon emissions characteristics, the following recommendations are proposed for energy conservation and emission reduction:

-

1.

Optimize energy structure by replacing fossil fuels with non-fossil fuels. Promote continuous optimization of hospital energy structure by implementing “coal-to-electricity” and “gas-to-electricity” transformations, promoting the use of electricity in canteens to reduce consumption of natural gas and liquefied petroleum gas. Increase the use of renewable energy sources such as solar energy, shallow geothermal energy, wind energy, and purchase green electricity. Consider installing solar panels on rooftops to meet daily electricity and hot water needs using renewable energy.

-

2.

Improve energy efficiency by upgrading energy-consuming equipment in major energy systems. Examples include improving the efficiency of central air conditioning systems, using energy-efficient equipment and lighting, smartizing water pump systems, and utilizing waste heat recovery from boilers. Strengthen energy management through intelligent system monitoring and optimization of energy use.

-

3.

Optimize transportation vehicles by gradually phasing out gasoline vehicles and purchasing new energy vehicles for official and ambulance use. Install charging stations within the hospital premises and consider installing a certain proportion of fast charging stations to reduce charging time. Encourage medical staff and patients to use new energy vehicles by providing free or discounted charging services and preferential parking policies.

In the future, the carbon accounting model could be further expanded and optimized to apply more broadly to different types of public institutions, such as government agencies, schools, and venues, in order to provide more comprehensive carbon reduction strategies. Additionally, exploring and implementing intervention measures for the travel behaviors of medical staff and patients, such as promoting the use of public transportation, implementing parking pricing policies, etc., could reduce the use of private cars and the corresponding carbon emissions. Based on the research findings, policy makers could be provided with scientific evidence to develop and implement policies targeting carbon emissions from public institutions, such as carbon taxes, carbon emission quota trading, green building standards, and more.

Availability of data and materials

The datasets generated during and/or analysed during the current study are available from the corresponding author on reasonable request.

References

Ali KA, Ahmad MI, Yusup Y (2020) Issues, impacts, and mitigations of carbon dioxide emissions in the building sector. Sustainability 12:7427

Architecture 2030 (2020) The zero code 2.0

Bianco V, Righi D, Scarpa F et al (2017) Model in energy consumption and efficiency measures in the Italian hotel sector. Energy Build 149:329–338

Breeam UK (2019) New construction buildings technical manual. https://www.breeam.com/NC2018/content/resources/output/10_pdf/a4_pdf/print/nc_uk_a4_print_mono/nc_uk_a4_print_mono.Pdf. Accessed 25 July 2022

British Standards Institution (2008) PAS 2050 Specification for the assessment of the life cycle greenhouse gas emissions of goods and services. British Standard Institution, pp 8–9

Chen ZS, Huang YD, Yang Z (2023) Discussion on transportation carbon emission statistics and calculation methods. Western China Commun Sci Technol 07:204–206

European Parliament News. https://www.europarl.europa.eu/news/en/headlines/society/20180301STO98928/greenhouse-gas-emissions-bycountry-and-sector-infographic. Accessed 17 July 2020

Fan FY, Lei YL (2016) Decomposition analysis of energy-related carbon emissions from the transportation sector in Beijing. Transp Res Part D: Transp Environ 42:135–145

Gangolells M, Casals M, Macarulla M et al (2021) Exploring the potential of a gamified approach to reduce energy use and carbon emissions in the household sector. Sustainability 13:3380

International Energy Agency (2018) 2018 Global Status Report: towards a zero-emission, efficient and resilient buildings and construction sector. United Nations Environment Programme, Nairobi

IPCC (2019) 2019 refinement to the 2006 IPCC guidelines for national greenhouse gas inventory. https://www.ipcc.ch/report/2019-refinement-to-the-2006-ipcc-guidelines-for-national-greenhouse-gas-inventories/. Accessed 22 Feb 2022

Li YN (2023) Scenario analysis and countermeasures of carbon emission from road mobile sources based on LEAP Model—a case study of Shandong Province. Qilu University of Technology

Li ZQ, Xu L, Chen LH et al (2024) Carbon emission calculation and application of low carbon technology in industrial buildings. Build Constr 46(01):143–146

Ma H, Du N et al (2017) Analysis of typical public building energy consumption in northern China. Energy Build 136:139–150

Malik F A, Bell M, Dala L, et al. Modelling transport emission of an out of town centre to achieve emission reduction targets. In: 2021 6th international symposium on environment-friendly energies and applications (EFEA); 2021.

Nejat P, Jomehzadeh F, Taheri MM et al (2015) A global review of energy consumption, CO2 emissions and policy in the residential sector (with an overview of the top ten CO2 emitting countries). Renew Sustain Energy Rev 43:843–862

Saisai JL, Lu B, Han L (2023) Research on the key path and method for the realization of carbon neutrality operation in Public Institutions. Ecol Econ 39(12):19–25

Shahrokni H, Levihn F, Brandt N (2014) Big meter data analysis of the energy efficiency potential in Stockholm’s building stock. Energy Build 78:153–164

Taylor S, Peacok A, Banfill P et al (2010) Reduction of greenhouse gas emissions from UK hotels in 2030. Build Environ 45:1389–1400

Tian C, Feng G, Li S et al (2019) Scenario analysis on energy consumption and CO2 emissions reduction potential in building heating sector at community level. Sustainability 11:5392

USGBC (2018) Leed zero carbon. http://leed.usgbe.org/leed.html. Accessed 25 July 2022

Wang ZJ, Chen F, Fujiyama T (2015) Carbon emission from urban passenger transportation in Beijing. Transp Res Part D: Transp Environ 41:217–227

Yan ZW (2018) The measurement of China’s transportation CO emissions and the spatial econometric analysis of its influencing factors. Beijing Jiaotong University

Zarco-Periñán PJ, Zarco-Soto FJ, Zarco-Soto IM et al (2022) CO2 emissions in buildings: a synopsis of current studies. Energies 15(18):6635

Funding

This paper is supported by the President’s Fund project of China Institute of Standardization “Research and Development and Application of Key Technologies and Platforms for Carbon Reduction in Public Institutions” (542023Y-10359) and the Science and Technology program project of the State Administration for Market Regulation “Research and Development and application of Key Technologies and Platforms for Carbon Reduction in Public Institutions” (S2023MK0540).

Author information

Authors and Affiliations

Contributions

L.Z. wrote the main manuscript text; R.Z. contributed to conceptualization and formal analysis; Y.M. contributed to methodology and validation; Y.B. contributed to writing-review and editing and foundation.

Corresponding author

Ethics declarations

Ethics approval and consent to participate

Not applicable.

Consent for publication

Not applicable.

Competing interests

The authors declare no potential conflict of interests.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Zhang, L., Zhang, R., Ma, Y. et al. Exploring carbon emission accounting methods for typical public institutions: a case study of hospitals. Energy Inform 7, 35 (2024). https://doi.org/10.1186/s42162-024-00337-z

Received:

Accepted:

Published:

DOI: https://doi.org/10.1186/s42162-024-00337-z