Abstract

In this paper, we use the Domar aggregation approach to study the evolution of Brazil’s productivity growth from 2000 to 2014, thus allowing us a disaggregated assessment of the issue. We found that the Brazilian economy’s overall performance is the outcome of a decrease in the economy’s density, as defined by the existing backward and forward connections amongst industries in intermediate inputs chains. It also can be explained by the poor performance of its sectors. Despite the relatively high density of the manufacturing sector, it performed a negative role concerning aggregate productivity growth both directly and indirectly. Directly insofar as that sector had negatives productivity growths during the period under consideration, and indirectly due to its high interconnection, which spread negative rather than positive productivity gains across the economy. Therefore, to improve the Brazilian economy’s poor performance, it is mandatory to restore the manufacturing sector’s capability to yield and spread productivity gains.

Similar content being viewed by others

1 Introduction

At least since Adam Smith, economists acknowledge productivity growth as the primary source of the wealth of nations. Solow’s (1956) growth model highlights that the growth rate of per capita output, capital and consumption is given by the exogenous technological change. However, within that framework, the total factor productivity (TFP) is calculated as a residual, somewhat unsettling. Since then, several authors have worked on what became known as growth accounting [see, e.g., Hulten (2010) and Jorgeson et al. (1987)]. Notwithstanding the considerable literature that followed Solow’s (1957) first attempt to measure TFP, they underestimate the contribution of intermediate inputs insofar as they are not explicitly considered. In the present work, we fill this gap, paying particular attention to intermediate inputs’ role in analysing the Brazilian economy’s productivity growth from 2000 to 2014.

Intermediate inputs have a unique role in spreading productivity growth [see, e.g., Aulin-Ahmavaara (1999)]. According to Jones (2011), they provide linksFootnote 1 that create a multiplier insofar as an industry may benefit from increased productivity in other industries from which it acquires inputs, which also generates impacts for aggregate productivity. The author proposes that linkages are a crucial part of the explanation by delivering a noteworthy example:

“Low productivity in electric power generation - for example, because of theft, inferior technology, or misallocation - makes electricity more costly, which reduces output in banking and construction. But this in turn makes it harder to finance and build new dams and therefore further hinders electric power generation.” Jones (2011, p. 1-2)

To provide a more in-depth analysis of the behaviour of both sectoral and aggregate Brazilian productivity and economic growth between 2000 and 2014, we use here the MFP (Multifactor Productivity) with Domar aggregation. With this approach, we overcome the MFP shortcoming of treating each industry in isolation, not capturing the productivity transfer between them [see, e.g., De Juan and Eladio (2000)]. To the best of our knowledge, although some authorsFootnote 2 focus on sectoral and aggregate productivity growth concerning Brazil, this is the first paper that adopts the above-mentioned strategy for the Brazilian economy. One of our aims is precisely to overcome the MFP limitation using the Domar method insofar as it explicitly considers that technical advancement occurs at the industry level.

This method’s advantage is that it can capture the productivity growth contributions of individual industries and those gains that accrue from the linkages among them.Footnote 3 Considering the effect of transferring productivity between industries in the MFP approach allows us to treat industries within an interdependent and interconnected system via intermediate capital goods. Besides, a noteworthy characteristic of Domar aggregation is that it is not a weighted average but a weighted sum of industrial productivity growth, with the sum of its weights higher than unity in input–output economies. The added Domar weights then measure the interconnection and linkages potential between sectors, which we call density, capable of propagating productivity growth throughout the economy.

After Domar (1961), several authors improved the method theoreticallyFootnote 4 and used it empiricallyFootnote 5 to perform growth accounting. Some essential theoretical works are Hulten (1978) which related the Domar aggregation with a macroproduction possibility frontier. Jorgeson et al. (1987) is a seminal work about using it with several theoretical improvements, while Aulin-Ahmavaara (1999) formulated explicitly the output price reductions caused by the productivity in downstream sectors. More recently, Ten Raa and Shestalova (2011) and Balk (2020) also have delivered essential contributions.Footnote 6

Given the usefulness of Domar aggregation, particular research fields have used it as a tool to calculate and decompose productivity growth. It has been useful, for instance, to study the implications of the Baumol Cost Disease within input–output frameworks [e.g., Oulton (2001), Sasaki (2007), Baumol (1967), Hartwig and Krämer (2019) and Sasaki (2020)]. It has also been adopted to study production networks and shock propagation channels as a mechanism for transforming microeconomic shocks into macroeconomic fluctuations [e.g., Acemoglu et al. (2012), Carvalho (2014), Carvalho and Salehi (2019) and Baqaee and Farhi (2019)].

Another useful methodology of calculating productivity growth that captures the role of interconnectedness among industries and ultimately the economic system as a whole is the vertical integration approach [e.g., De Juan and Eladio (2000), Gaberllini and Wirkierman (2009,2014) and Lind (2020)]. An essential difference between the two methods is that they follow different ways of organising the economic system. While the Domar aggregation deals with the economy in a traditional input–output industrial setup, the second method measures productivity from a vertically integrated perspective, in which each sector is characterised by a composition of industries needed to produce every final commodity in the economy [Cas and Rymes (1991)].

An additional relevant difference between Domar aggregation and the vertical integration approach is that while the former aggregates industrial MFP, the latter calculates the total usage of labour per final output, both directly and indirectly. Authors, such as Cas and Rymes (1991) and Aulin-Ahmavaara (1999), though using distinct assumptions, have formally demonstrated that, in the aggregate, the measurements arising from the productivity of vertically integrated sectors and Domar aggregation tend to coincide and are closer the higher the level of aggregation.

Our main aim in the present paper is to structurally analyse the Brazilian economy’s productivity behaviour using this method to highlight interdependence and interconnection between industries. We aim to focus on the productivity gains (or losses) that spread amongst industries via circulating capital due to increased productivity and lower (or higher) costs. Using the Domar aggregation to decompose Brazil’s overall productivity growth for three macrosectors, we confirmed some results [e.g., Souza and da Cunha (2018)] and found new ones. We verified that services and primary industries macrosectors positively impacted average productivity growth, although the macromanufacturing sector contributed to negative productivity growth.

But we also went a step further in focusing on the multiplicative effect of propagating productivity growth due to Domar weights. We conclude that manufacturing had a higher sectoral density than its value-added share, albeit it seems to have spread negative productivity growth in most of the given period. These findings reassert the importance of the industrial sector as one of the main drivers of growth. Had this sector presented a better performance during the time under consideration, the Brazilian economy’s overall productivity growth would be better both by the direct and indirect channels.

We organise this paper as follows: besides this brief introduction, in the next section, we present an outlook of the Brazilian economy. Section 3 is the methodological section, with both an explanation of the database and a theoretical review of Domar aggregation and its usage. In the fourth section, we use this method empirically for delivering the main results of our analysis, which considers 48, 10 and 3 sector levels of aggregation. Finally, Sect. 5 concludes the paper.

2 An outlook of the Brazilian economy

The Brazilian economy was one of the fastest growing economies between the 1930s and 1980s, converting the landscape from a vast rural and backward country to an urban and somehow industrialised one. However, after that period of consistent economic growth, the productivity of the Brazilian economy remained stagnant during the eightiesFootnote 7 and the nineties [see e. g., Nassif et al. (2020)], gaining momentum in the early 2000s, especially after 2003, with income distribution, higher growth rates, a steady decrease in unemployment and increases in investments [see, e.g., Borghi (2017)]. Barbosa-Filho and Pessôa (2014) and de Souza and da Cunha (2018) also registered a resurge of productivity growth at the beginning of the first decade of the century. Still, it lasted until the 2008 crisis, with both mostly sectoral and aggregate productivity growth declining after that.

Some factors help us to disentangle this path. A crucial one is related to the intense deindustrialisationFootnote 8 process registered in the last decades. Borghi (2017) argues that since the 1980s, the Brazilian manufacturing sector has been losing its GDP share, which declined from more than 40% to about one-third in the early 1990s and less than one-sixth during the 2010s. That movement has been accompanied by an increasing service sector and rising competitiveness of the primary sectors internationally. Although a spasm of manufacturing industries resurge in the early 2000s, the global economic growth and the production and exports of primary products have become the locomotive of Brazilian expansion.

In that period, the global demand set out to grow more intensely due to the development of Asian economies, mainly from China. Such a process was accompanied by an intense appreciation of the real, owing to the easy inflow of foreign currencyFootnote 9 [see, e.g., Marconi et al. (2016)]. As a result, there was an increase in imports of manufactured goods, raising 155% at constant prices between 2002 and 2008, as shown by Borghi (2017). That damaged the competitiveness of Brazilian manufactured products and led to a significative ‘reprimarization’ of the productive structure. One of the shortcomings of such a process was a decrease in the density, insofar as manufacturing industries have stronger linkages or densityFootnote 10 as defined here. A higher density means more forwarding and backward links amongst the industries, which is essential to spread productivity gains through vertically integrated sectors. One could argue that such a decrease is the outcome of integration to global value chains (GVCs).

As the global economy is structured around GVCs, [see, e.g., Gereffi and Fernandez‐Stark (2011)] the extent of participation in those chains seems to be an important explanatory variable to the decreaseFootnote 11 in domestic density. However, such as other Latin America’s economies, Brazil remains poorly integrated in terms of GVCs [see, e.g., and Andreoni and Tregena (2020)], which does not explain the density reduction. It shows a deterioration of the quality of the productive structure. This means that the manufacturing industries are less interconnected with the remaining sectors. Therefore, since the Brazilian manufacturing macrosector has been losing ground in the productive structure, the national economy has faced a decrease both in density and the capacity to spread productivity growth among industries, as will be formally shown in the next section.

Appendix B shows that among the 21 industries composing the macromanufacturing sector, only 6 of them did not present a decline in the value-added shareFootnote 12 of the GDP. Moreover, considering the same industries, only two of them did not decline their Domar weights, indicating an interconnection and density fall. Besides, when considering the average productivity growth for the whole period for each particular industry, the manufacturing industries are by far the ones with lower productivity advance. Indeed, from the 21 industries composing the mentioned macrosector, only seven did not face negative average productivity growth, as depicted in Appendix B. Despite their better productivity growth performance, the services and primary industries, macrosectors have less density, especially the primary industries macrosector. For instance, Arias et al. (2017) show that agriculture has been an island of success in productivity growth in the last decades compared to other Brazilian economy sectors.

The lack of productivity advance through the manufacturing industries may be related, among other causes, to the low competitiveness and lack of both domestic and foreign demand. De Jesus et al. (2018), performing an empirical evaluation of the post-Kaleckian model for the Brazilian economy since the 70s, reported the prevalence of a profit-led regime. If it is true, the presence of a trend of appreciation of the exchange rate can explain lower growth and capacity utilisation rates during the time under consideration. On the external front, although some authors, such as Franco (1998), argue that the appreciated exchange rate and high inflow of imported intermediate inputs would increase the manufacturing competitiveness, the demand effect has more than offset the cheap imported inputs effect. Indeed, Oulton and O’Mahony (1994) found empirically for the UK a positive relationship between demand growth rate (or output growth rate) and (MFP) productivity growth among manufacturing industries.

3 Methodology

3.1 Database

We analyse the Brazilian economy between 2000 and 2014 using the Domar aggregation approach. To do that, we use the Socio-Economic Accounts (SEA) data from the World Input–Output Database (WIOD). The SEA tables provide us with all the necessary dataFootnote 13 and are organised in a directly compatibleFootnote 14 way, as shown by Dietzenbacher et al. (2013) and Timmer et al. (2015). The data comprises the period 2000 to 2014 and 48 industries. Aiming to improve the visualisation results, we have split the industries, besides the original 48 levels of aggregation from the data,Footnote 15 to 10 and 3 levels of aggregation, as shown in detail in Appendix A.

3.2 Method

Following the methodology proposed by Jorgeson et al. (1987) and Jorgenson and Stiroh (2000), consider an economy with \(n\) discinct industries. Each of them can sell its products both to final demand and intermediate demand from other industries. The expression below shows that the nominal gross output production of the \(i\) th sector (\({P}_{i}{Q}_{i}\)) is sold both to final demand (\({P}_{i}{Y}_{i}\)) and to intermediate demand (\(\sum_{j=1}^{n}{P}_{i}{Q}_{ij}\)) from all \(j\) sectors that require the good or service produced by \(i\) as an intermediate input to its production:

where \({P}_{i}\) represents the selling price of the industry’s \(i\) goods, both to final and intermediate demand. Moreover, \({Q}_{i}\), \({Y}_{i}\) and \({Q}_{ij}\) are, respectively, real gross output, real final demand and real intermediate demand produced by the \(i\) th industry. Symmetrically, consider that the gross nominal production of all \(i\) sectors can also be described from its inputs side. It means that each sector \(i\) yields a homogeneous good or service that requires, for its production, an intermediate input set bought from other industries \(\sum_{j=1}^{n}{P}_{j}{Q}_{ji}\), as well as a set of rental price of capital and labour inputs, respectively, defined as \({P}_{Ki}{K}_{i}\) and \({P}_{Li}{L}_{i}\), as shown by the equation below:

The sectoral nominal value-added (\({P}_{i}^{V}{V}_{i}\)), or net output, is, therefore, the difference between their respective gross production and intermediate demand.Footnote 16 In our model, it is precisely equal to the sum of sectoral primary inputs expenditures, as shown by the next expression:

Equalising (1) to (1’), and summing up for all the \(i\) industries, we find the definition of the economy’s gross domestic product (GDP). It can be measured both from the sum of all final demands and value-added. It is worth noting that the intermediate inputs demand and supply cancel out each other avoiding double counting.

Assume that each industry’s production technology is described, in a more general form, as a sectoral production function that relates time and its inputs—both primary and intermediate—with the gross industrial product. The Hicks-neutral type of this function is:

Differentiating totally (3) with respect to time, using (1’) and considering that a hat (^) denotes growth rate, we find the next equation that describes the \(i\) th sector multifactor productivity growth. For the sake of notation simplicity, the sectoral inputs to gross output shares are denotedFootnote 17 by \({\upsilon }_{Li}=\frac{{{P}_{Li}L}_{i}}{{{P}_{i}Q}_{i}}\), \({\upsilon }_{ki}=\frac{{{P}_{Ki}K}_{i}}{{{P}_{i}Q}_{i}}\) and \({\upsilon }_{{Q}_{ji}}=\sum_{j=1}^{n}\frac{{{P}_{j}Q}_{ji}}{{{P}_{i}Q}_{i}}\).

The term \({\widehat{q}}_{i}\) denotes sectoral multifactor productivityFootnote 18 growth. The multifactor productivity growth—MFP growth hereafter—is defined as the difference between the growth rate of the gross product and the growth rate of the inputs, weighted by the share of the input’s value in the value of the gross product [see, e.g., Cas and Rymes (1991)]. One of the first authors to formalise the concept of MFPFootnote 19 growth was Hulten (1978). Note that the equation above can be written in discrete time using a TörnquistFootnote 20 or translog discrete-time approximation, where the \(\Delta\) term is the difference between the variable in the current and previous time:

We can describe the sectoral gross output growth rate as the average mean of the growth rates of both real net output and intermediate inputs, weighted by its respective shares of the gross production. In the equation below, the term \({\upsilon }_{Vi}\) equals to \({\upsilon }_{{L}_{i}}+ {\upsilon }_{{K}_{i}}\).

Using (4) and (5) and after some algebraic manipulations, it is possible to find the following expression that relates the growth rate of the sectoral value-added with the growth rate of capital stock, labour force and productivity:

From an aggregate point of view, the economy’s GDP is described as the sum of all sectoral values added (or amount of all sector final demand). That is, being the nominal GDP of the whole economy \(PY\), we have that \(PY={P}_{v}V=\sum_{i=1}^{n}{P}_{i}^{V}{V}_{i}\). We use a general function that relates the aggregated value added with the relevant inputs and timeFootnote 21:

When differentiating totally (7) with respect to time, and after some algebraic manipulations, we find an expression that connects the growth rate of aggregate productivity, defined as \(\widehat{q}\), with the growth rate of the total value added of the economy and the weighted sum of the sectorial primary inputs capital and labour:

Aiming to unearth an equation that relates the productivity growth rate of the whole economy with the growth rates of sectoral productivity—the Domar aggregation—we combine (6) and (8) to obtain:

Expression (9) is known as the Domar aggregation of sectoral MFP growth. Although Domar (1961) was the first to find this relationship formally, other authors, such as Hulten (1978) and Jorgeson et al. (1987) later improved it. In discrete time, we can write the expression (9) as:

Note that the weighted sum of sectoral MFP has the striking feature that it sums to more than unityFootnote 22 in economies with intermediate goods. The higher the participation of intermediate inputs in the economy, the higher the sum of the weightings. Regarding the ‘sum to more than the unity’ of Domar aggregation and its intuition, Jorgenson (2018, p. 881) considers that:

“A distinctive feature of Domar weights is that they sum to more than one, reflecting the fact that an increase in the growth of the industry’s productivity has two effects: the first is a direct effect on the industry’s output and the second an indirect effect via the output delivered to other industries as intermediate inputs.”

Similarly, Oulton and O’Mahony (1994, p. 14) explains the intuition behind the role of intermediate inputs in the aggregated productivity growth and the Domar weights behaviour:

“The intuitive justification for the sum of the weights exceeding one is that an industry contributes not only directly to aggregate productivity growth but also indirectly, through helping lower costs elsewhere in the economy when other industries buy its product”.

The Domar aggregation method establishes a link between the industrial’s level of productivity growth and aggregate productivity growth. An aggregated economy’s overall productivity may exceed the average productivity gains across sectors, given that flows of intermediate inputs among sectors contribute to total productivity growth by allowing productivity gains—or losses—in successive industries to augment one another. Moreover, an industry’s contribution to the overall productivity growth depends (besides the direct productivity growth in this sector) on the efficiency changes in the production of its intermediate inputs. To clarify the mechanism in which the direct and indirect effects above mentioned behave within the model, we substitute Eqs. (1’) and (2) into the numerator of (9) to obtain:

Disaggregating the second term of the expression above for all sectors, we get:

Note that the sum of the value-added weights, in the first term of the equation above the right-hand side, is precisely one. The terms on the right, however, depict the sectoral productivity impacts from intermediate inputs deliveries. Therefore, the weights on the right are the ones that exceed the unity considering the overall aggregation. From the equation above, it must be clear that the higher the degree of interconnection, or density of the economy in terms of intermediate inputs deliveries, the higher the potential of productivity growth augmenting given the growth of sectoral productivities.

To visualise the mechanism involved, assume that \({\theta }_{ij}=\frac{\sum_{j=1}^{n}{P}_{j}{Q}_{ji}}{\sum_{i=1}^{n}{P}_{i}^{V}{V}_{i}}\) is the share of aggregate demand for intermediate inputs in the economy, which measures the degree of sectoral density or sectorial interconnection. Substituting \({\theta }_{ij}\) into Eq. (10), we find the equation below:

The term \(\sum_{i=1}^{n}{\theta }_{ij}\) measures the degree of interconnection, or density, of the economy, since it defines the relative importance of vertical interaction of the sectors or industries. The greater the term \({\theta }_{ij}\) is in each \(i\) th sector, the more significant is the sectoral capability to spread productivity and to augment the sum of the whole economy due to Domar weights. Let us suppose that, for some reason, the density \({\theta }_{ij}\) of some sector \(i\) increases due to a more significant share of intermediate demand by the given sector in the economy’s GDP. Then, by differentiating the aggregate productivity growth with respect to \({\theta }_{ij}\) in (12) we have that:

Hence, if the sectoral productivity growth in the given sector is positive, then an increaseFootnote 23 in \({\theta }_{ij}\) leads, by itself, to a higher aggregate productivity growth, given all sectoral productivity growth. In this vein, if the share of intermediate goods in the economy increases, the sum of Domar weights increases as well. In that case, the economy is subject to a higher densityFootnote 24 that generates an augmented potential of aggregate productivity growth. Finally, using Eqs. (4) and (5) and summing up for all sectors, it is possible to find an expression concerning the interactions between aggregate productivity growth and economic (GDP) growth:

Thus, as shown by the above equation, the aggregate value-added growth rate can be equivalent to the weighted sum of labour, capital, and Domar aggregated productivity growth contributions.

4 Results and discussion

Figure 1 shows, on the top side, that the manufacturing sectors were the ones that used intermediate inputs the most as a proportion of its gross output. Moreover, albeit the service sectors were very heterogeneous compared with primary industries, they still had, on average, a more substantial share of intermediate inputs than primary sectors.

Characteristics and dispersion of the sectors of the Brazilian economy

Concerning the ratio between value-added and GDP, when summing up all service sectors, they represented the majority share in GDP compared with the other two macrosectors, as expected. However, the manufacturing sectors were the ones with higher average intermediates inputs to GDP share—or density as defined in the last section—compared to services and primary industries macrosectors. Whereas the services sectors had extensive heterogeneity regarding intermediate inputs to gross output shares, it did not happen concerning sectoral density. Furthermore, both the manufacturing and services sectors presented relevant shares of Domar Weights, and, therefore, more potential to spread productivity growth than primary industries.

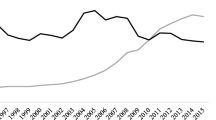

Figures 2 and 3 show a time series analysis using the ten sectors level of aggregation regarding both sectorial values added to GDP share and intermediate inputs to gross output share. Notice that, in Fig. 2, while agriculture, forestry and fishing sectors have shown some stability in the GDP share, manufacturing industries have had a slight decline during the given period. Most services sectors have shown an increase in their share, except for the information and communication sector and other traditional services sectors.

10 sector value added share in GDP. Authors calculations using WIOD Brazilian data

10 sector intermediate input relative to gross output share. Authors calculations using WIOD Brazilian data

Concerning sectoral behaviour about intermediate input to gross output share, displayed in Fig. 3, note that manufacturing industries have been the sector with the highest demand for intermediate inputs compared to its gross output with something around sixty to eighty per cent during the given period. Agriculture, forestry and fishing experienced a slight increase to something above forty per cent of intermediate inputs share. Mining, quarrying, electricity, gas and water supply has had a significant share as well, above most services sectors. In addition, notice from Fig. 3 that the services sectors, as expected from the previous analysis, have exhibited a heterogeneous pattern, with a relatively high share in financial and insurance activities and a relatively small share in real estate activities.

In Table 1, it is provided calculations for sectoral density (intermediate input to GDP share), value-added share in GDP, sectoral Domar weights (gross output to GDP share) and sectoral multifactor productivity growth for both 10 and 3 sector levels of aggregation. By analysing the time series, we found an inflexion point on the patterns of change in most variables studied before and after 2008, confirming the findings of de Souza and da Cunha (2018), who identified the same pattern using an alternative methodology. Hence, we decided to split the analysis for two distinct periods: from 2000 to 2008 and 2009 to 2014. Considering the average of the entire period analysed—2000–2014—the sum of Domar weights for the whole economy is 2,042. This means that in addition to the sum of the shares of the values added to GDP, which add up to the unit, there is an extra weight of 1.042 relative to the sectorial densities. This additional portion of the sums of the sectorial weights refers to the degree of sectorial interconnection. It is clear from Table 1 that the macrosector with the highest Domar weight is the services one, with 52%, followed by the manufacturing and primary sector macrosectors, with 43.5% and 4.5%, respectively.

Although the manufacturing sector is the one with the most significant capacity to propagate productivity growth in the economy, its high sectoral density seems to have bred a decrease in productivity due to its average − 0.5% annual MFP growth. That has a double impact—direct and indirect—decreasing the economy’s aggregate productivity, especially after 2008. The primary sector was the one that generated the highest average annual productivity growth, with an average of 1.8% per year. However, the sector showed low interconnection potential and, therefore, insufficient capacity to propagate productivity growth. The services sector, on the other hand, although it had a vital ability to spread productivity growth, presented a modest average of MFP growth, with an annual average of 0.5%. However, it showed heterogeneous behaviour when observing in more disaggregated terms.

Regarding sectoral Domar weights, considering the yearly average period, the service sector had a 1.05 Domar weight, followed by 0.89 in manufacturing and only 0.093 in the primary industries. It is worth noting that although the services sector was the macrosector with a higher Domar weight, with about 52%, it had almost 68% of the total value-added. The manufacturing sector presented 43.5% of the average Brazilian Domar weight but around 27% of total value-added. This fact shows that the impact of intermediate inputs in the manufacturing sector generates a boost in its Domar weight compared to its value-added share.Footnote 25 The primary industries sector, in its turn, had only 4.5% of the total average Domar weight, with almost 5% of the value-added share, on average.

Although both macrosectors—manufacturing and services—have had a high capacity for potentialising productivity growth throughout the economy, many manufacturing industries showed negative productivity growth due to their Domar weights. Thus, the macromanufacturing sector’s high density acted negatively concerning aggregate productivity growth, spreading and increasing negative industrial productivity growth. It is, therefore, crucial to improving the productivity growth behaviour of the macromanufacturing sector, since it has a high impact on the whole economy.

Regarding possible reasons for low productivity growth at the industrial level, which is the case concerning industries composing the Brazilian manufacturing macrosector, Cas and Rymes (1991, p. 12) argue that a possible reason is a lack of demand:

“When Keynesian problems of insufficient aggregate demand are experienced, the waiting or saving of owners of capital is largely spilled onto the sands, and this shows up as a decline in multifactor productivity measures”.

The services macrosector, in its turn, showed a positive average multifactor productivity growth and then its relatively high Domar weight has performed a positive effect on potentialising productivity growth. The primary industries macrosector, albeit the sector with a higher productivity growth average, had the lowest sectoral Domar weight, with a relatively limited capacity to boost aggregate productivity growth.

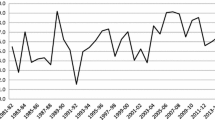

Figure 4 shows the aggregate Brazilian Domar weight behaviour between 2000 and 2014. It presented a slightly upward trend until 2008, of almost 5%. After 2008, the pattern has reverted and has more than compensated for previous growth. This fact indeed spawned a decrease of average Brazilian sectoral density and, therefore, a decline in both sum of Domar weights and structural capacity in potentialising sectoral productivity growth at the aggregate level. That fact is easier to see in Figs. 5 and 6, which show the aggregate productivity growth measured by the Domar aggregation method for the whole economy and decomposed by macrosectors, respectively. Both figures show the yearly and cumulative Domar aggregate productivity growth.

Sum of Brazilian Domar Wheights 2000–2014

Domar aggregation: yearly and cumulative productivity growth

Domar aggregation: yearly and cumulative productivity growth decomposed by macrosectors

Using Eq. (9’), it is possible to calculate the yearly and aggregate cumulative productivity growth using the Domar aggregation method. Indeed, given sectoral productivities growths and sectoral densities, the Brazilian aggregate productivity growth increased, from a cumulative point of view, from 2000 to 2010. However, despite that behaviour, the aggregate productivity growth was negative in 2001, 2003 and 2009. However, after that and despite 2010, the yearly aggregate productivity growth was negative in all years, which led to an almost complete reversal of cumulative productivity growth previously undergone, from nearly 17% cumulative growth in 2010 to roughly 3% in 2014.

The behaviour of aggregate productivity growth decomposed by macrosectors and shown in Fig. 6. Although the cumulative productivity growth in services and primary industries macrosectors was positive, the manufacturing sector was consistently negative due to its negative (MFP) growth potentialised by its high Domar weight and sectoral density. It is interesting to note that although the Primary industries macrosector was the one with more consistent yearly MPF growth, its positive contribution to overall productivity was limited due to low density and Domar weight, portrayed in the figure above. The services macrosector presented a relatively high variance in its annual productivity growth, but it still delivered most of the productivity growth in the economy thinking as an aggregate. After 2009, such as aggregate productivity, the services macrosector decreased both cumulative and average yearly productivity growth.

As pointed out by Wolff (2013), there are two ways of increasing economic growth. The first one is by augmenting the factors available for production (‘factor augmentation’), while the second one is by raising the rate of productivity growth. Table 2 reveals each input’s contribution and decomposed Domar aggregate productivity growth for each unity of value-added for all the three macrosectors and the whole economy, considering the average of 2000–2014.

Considering the three macrosectors and the economy as a whole, the average growth rate of value-added generated by the primary macroindustry had a negative contribution from the labour input of − 18.5%, a positive contribution of capital input of 44.9% and a vital productivity contribution of 73.6%. The manufacturing sector obtained a positive contribution from primary inputs labour, and capital with 61.4% and 103%, respectively, but a considerable negative productivity contribution of − 64.4%, for each added value generated. In turn, the services sector had a positive contribution from either labour and capital inputs and productivity growth, with 46.9%, 29.3% and 23.8%, respectively. The average of each unit of the added value generated by the economy in the period, considering the economy as a whole, attained the contribution of 45.2% of labour input, 45.9% of capital and 8.9% of generated productivity measured by Domar aggregation. The result that the productivity growth in the service sector was higher than that of the industrial sector is somewhat surprising insofar as we would expect that the latter would have a higher productivity gain than the former.Footnote 26

5 Concluding remarks

In this paper, we use the Domar aggregation to study the evolution of productivity growth in Brazil from 2000 to 2014. This method was adopted in other countries, but this is the first time for the Brazilian economy to the best of our knowledge. That is particularly important, because it allowed us to disaggregated the Brazilian productivity and growth pattern during that period. We can explain the Brazilian economy’s overall productivity performance in terms of the poor performance of its sectors and diminishing industrial density, with fewer backward and forward connections amongst industries in terms of chains of intermediate inputs.

Besides, despite the relatively high density of the macromanufacturing sector compared to other sectors in the Brazilian economy, it performed a negative role in aggregate productivity growth both directly and indirectly. Directly insofar as that sector had negatives productivity growths during the period under consideration, and indirectly due to its high interconnection, which helped spread negative rather than positive productivity growth across the economy.

Therefore, to improve the Brazilian economy’s poor performance in recent years, it is mandatory to enhance the Brazilian manufacturing macrosector’s capability to generate productivity growth. It is also essential for future investigations to understand the Brazilian economy’s low productivity advance and the macromanufacturing sector. In sum, Brazil has failed in its task to deepen its industrial density. Consequently, it has witnessed a prematurely shrink in the manufacturing sector’s share in GDP, being stuck in a middle-income trap.

Availability of data and materials

We use the Socio-Economic Accounts (SEA) data from the World Input–Output Database (WIOD). The data comprises the period between 2000 and 2014, and 48 sectors for the Brazilian economy. Aiming to improve the visualisation results, we have split the sectors, besides the original 48 levels of aggregation from the data, to 10 and 3 levels of aggregation as can be seen in detail in the appendix. The original subdivision of sectors is given by the ISIC (International Standard Industrial Classification of All Economic Activities) revision n. 4, from the United Nations Statistics Division, which can be found at https://unstats.un.org/unsd/classifications/Econ/ISIC#isic1.

Notes

As pointed out by Amit and Konings (2007), and Goldberg et al. (2010), such goods allow for quality improvement in final products and broader participation of a country in international trade. Besides, its increased availability may facilitate product diversification and trigger pro-competition effects, inducing cost reductions and improved diversification, with the creation of productive linkages and spillover effects. The notion that linkages across industries can be crucial to economic performance dates back at least to Leontief (1936), which introduced the field of input–output economics. Hirschman (1958) emphasised the role of forwarding and backward linkages to economic development.

See de Souza and da Cunha (2018) for a work using similar period of time as here and for a review of articles about Brazil using TFP methodology.

While Strobel (2016) investigates the contribution of ICT inputs to industrial productivity growth using a TFP method (with intermediate inputs), we use the industrial MFP (or TFP with intermediate inputs) and aggregate it, using the Domar approach, into macro sectors to measure its interconnections and productivity change transmissions through industries.

See also Hulten (2010) for a complete survey on growth accounting and its relationship with Domar aggregation and other methods.

Some interesting empirical works are e.g. Oulton and O’Mahony (1994) about productivity growth in United Kingdon manufacturing industries, Jorgenson and Stiroh (2000) and Oliner and Sichel (2000) concerning United States, Timmer and van Ark (2005) about Europe Union and focusing on Information and Communication Technology sectors, Gu and Yan (2016) about China and Cao et al. (2019) regarding several developed countries.

After a challenging decade in the 1980s, which became known as the “lost decade”, due to a hyperinflation process and low economic growth, in the 1990s the Brazilian economy experienced an inflation’s stabilisation but at the cost of the strong appreciation of the domestic currency, due to a fixed exchange rate regime, and high trade liberalisation. The beginning of the 2000s was marked by the consequences of the end of a fixed exchange rate regime and a considerable devaluation of the national currency.

The wane of manufacturing share in the national income share is not just the outcome of a faster decline in the price of manufacturing goods when compared to the cost of services. Even if one calculates the shares of different sectors in terms of constant prices, as opposed to current prices, it will conclude that manufacturing value-added is decreasing. Besides, Brazil’s deindustrialisation is premature, happening at lower per capita income levels than the average of industrialised countries. And the migration of the labour force is occurring towards final services, which tend to have lower productivity than the business services. The outcome is a reduction in overall productivity gains.

The quantitive easing in the US economy combined with the Brazilian macroeconomic policy whereby the increase in interest rate was used to decrease consumption and control inflation explains the massive inflows of capital in Brazil during this period. Marconi et al. (2016, p. 472) also highlight the adverse effects of currency appreciation due to the well-known “Dutch disease”.

The literature based on the Domar aggregation highlights an increase of density as a possible source of better growth performance. In the presence of an intermediate (or business) service sector, the shift of resources to the service sector may enhance rather than decrease aggregate productivity growth even if the productivity growth of the service sector is lower than that of the industrial sector.

Andreoni and Tregena (2020, p. 327) highlightes this trade-off by reporting that “(…) in a number of cases, middle-income countries that have attempted to integrate globally have also ended up ‘de-linking domestically’ and hollowing out the domestic manufacturing sector”.

Considering the average for the period between 2000 and 2008 versus the average from 2009 until 2014.

We use, from SEA tables, sectorial capital stocks, labor expenditures, hours worked, gross output and value added at current and constant prices. The only necessary data that is not explicitly in SEA tables is sectoral capital stock growth rate in constant prices. We have used an appropriated deflator to calculate it from nominal capital stock.

The (SEA) WIOD data is built in a way that the value added per sector is equal to the sum of expenses of labor and capital inputs in one hand and equal to the difference between sectorial gross output value and intermediate inputs value in other hand, just like in the model provided.

The original subdivision of industries is given by the ISIC (International Standard Industrial Classification of All Economic Activities) revision n. 4, from the United Nations Statistics Division, which can be found at https://unstats.un.org/unsd/classifications/Econ/ISIC#isic1.

Notice that conceptually the definition of nominal value-added is just a residual, precisely the difference between gross output and intermediate demand of each industry. Due to our assumptions concerning (1’), the mentioned residual turns out to be precisely the sum of values of labour and capital. However, concerning real magnitudes, the data has been built using the double deflation method to obtain real value-added, which is found in the WIOD database.

Using (1’) it’s easy to see that \({\upsilon }_{{L}_{i}}+{\upsilon }_{{K}_{i}}+{\upsilon }_{{Q}_{ji}}=1\).

There is an upshot of the way MFP growth is calculated. Income distribution between labour and capital affects the weights of the MFP, irrespective of their physical growth rates. We recognize that this can affect the growth accounting but not consider this possibility here.

According to Oulton and O’Mahony (1994), the MFP growth is, theoretically speaking, the rate at which output would have increased in some period if all inputs had remained constant. Furthermore, it is noteworthy that if we calculate MFP growth over some period and it turns out to be about zero, then we can at least say that any eventual growth in labor productivity must have been due to increased use of other inputs.

See, for example, Diewert (1976), Ten Raa and Shestalov (2011) and Hulten (2010) about the use of Törnquist index for discrete time aproximations and uses in productivty growth theory. The nickname Translog index is due to Diewert (1976), who has shown that the approximation is exact for the translog production function.

Accordingly to Ten Raa and Shestalova (2011), more common productivity aggregation in the literature, like aggregating sectoral TFP-growth (without explicitly dealing with intermediate inputs in sectoral production functions), can be represented as a simple weighted average of sectoral productivity growth. However, the aggregation of sectoral multifactor productivities growth comprises a tricky aggregation issue, when dealing with input–output economies, which has been analyzed by Domar (1961). The point is that the national product of an economy does not comprise the sum of all gross output, but only the sum of net outputs. Avoiding for double counting, the Domar aggregation spawns an aggregation where the weights sum to more than one.

Indeed, there are more than one possibly way that can lead to an augmented sum of Domar weights, or density of the economy. It can happen both if one or more sectors start to be more integrated, demanding higher shares of intermediate inputs for its production, or if one or more sectors with a structurally high share of intermediate inputs in its gross output increases its share in the whole economy in a way that led to a higher sum of Domar weights.

An increase of density as a source of better growth performance is highlighted by the complex literature advanced by Hausmann and Klinger (2006). According to this view, industries with higher ‘implied productivity’ are those whose are well connected with other industries of the economy, being this connection made by the supply of intermediate inputs. Hidalgo and Hausmann (2009) went a step further and concluded that the ease in which a country moves from the production of one good to another depends on its position in the ‘product space’, which is the network connections between various sectors.

These findings corrobarates the view emphasized by authors such as Szirmai (2012) and Tregenna (2009), among others, that the manufacturing plays an important role in the growth process due to its forwarding and backward linkages, which are more pronounced than in the service and agricultural sectors. More recently, Gabriel et al. (2020), using panel data and input–output matrix show that the manufacturing industry’s output multipliers and employment are higher than that from the other sectors for developing countries, thus confirming also confirmed the view that productive linkages and spillover effects are stronger within manufacturing industries [Szirmai et al. (2013)].

This hypothesis is commonly associate to Baumol’s model of unbalanced growth in which he assumes that the service sector is the stagnant one due to its lower productivy gains when compared to the industrial sector. Such view was confirmed empirically by a number of authors such as Appelbaum and Schettkat (1999) and Nordhaus (2008).

References

Acemoglu D, Carvalho VM, Ozdaglar A, Tahbaz-Salehi A (2012) The network origins of aggregate fluctuations. Econometrica 80(5):1977–2016

Amiti M, Konings J (2007) Trade liberalization, intermediate inputs, and productivity: evidence from Indonesia. Am Econ Rev 97(5):1611–1638

Andreoni A, Tregenna F (2020) Escaping the middle-income technology trap: a comparative analysis of industrial policies in China, Brazil and South Africa. Struct Chang Econ Dyn 54:324–340

Appelbaum L, Schettkat R (1999) Are Prices Unimportant? The changing structure of the industrialized economies. J Post Keynesian Econ 21(3):387–398

Arias D, Vieira P, Contini E, Farinelli B, Morris M (2017) Agriculture productivity growth in Brazil: recent trends and future prospects. World Bank, Washington, DC

Aulin-Ahmavaara P (1999) Effective rates of sectoral productivity change. Econ Syst Res 1:349–363

Balk MB (2020) A novel decomposition of aggregate total factor productivity change. J Prod Anal 53:95–105

Baqaee DR, Farhi E (2019) The macroeconomic impact of microeconomic shocks: beyond hulten’s theorem. Econometrica 87(4):1155–1203

Barbosa-Filho F, Pessôa S (2014) Pessoal Ocupado e Jornada de Trabalho: uma releitura da evolução da produtividade. Rev Bras Econ 1:149–169

Baumol WJ (1967) Macroeconomics of unbalanced growth: the anatomy of urban crisis. Am Econ Rev 57(3):415–426

Borghi RA (2017) The Brazilian productive structure and policy responses in the face of the international economic crisis: an assessment based on input-output analysis. Struct Change Econ Dyn 43(C):62–75

Cao J, Ho S, Jorgenson M, Ren D, Sun L, Yue X (2019) Industrial and aggregate measures of productivity growth in China, 1982–2000. Rev Income Wealth 55:485–513

Carvalho VM (2014) From micro to macro via production networks. J Econ Perspect 28:23–48

Carvalho VM, Tahbaz-Salehi A (2019) Production networks: a primer. Ann Rev Econ 11:635–663

Cas A, Rymes TK (1991) On the Concepts and Measures of Multifactor Productivity in Canada 1961–1980. Cambridge University Press, Cambridge

De Juan O, Eladio F (2000) Measuring productivity from vertically integrated. Econ Syst Res 12:65–82

De Souza T, da Cunha M (2018) Performance of Brazilian total factor productivity from 2004 to 2014: a sectoral and regional analysis. Econ Struct 7:24

De Jesus C, Araujo R, Drumond C (2018) An empirical test of the Post-Keynesian growth model applied to functional income distribution and the growth regime in Brazil. Int Rev Appl Econ 32(4):428–449

Dietzenbacher E, Los B, Stehrer R, Timmer M, De Vries G (2013) The construction of world input-output tables in the WIOD project. Econ Syst Res 25:71–98

Domar ED (1961) On the measurement of technological change. Econ J 71:709–729

Franco G (1998) A inserção externa e o desenvolvimento. Revista De Economia Política 18(3):10–41

Gaberllini N, Wierkierman AL (2009) Changes in the Productivity of Labour and Vertically Integrated Sectors - An Empirical Study for Italy. MPRA Paper No. 18871

Gaberllini N, Wierkierman AL (2014) Productivity Accounting in Vertically (Hyper-) integrated terms: bridging the gap between theory and empirics. Metroeconomica 65:1

Gabriel LF, de Santana RLC, Jayme FG Jr, da Costa OJL (2020) Manufacturing, economic growth, and real exchange rate: empirical evidence in panel data and input-output multipliers. PSL Quart Rev 73(292):51–75

Gereffi G, Fernandez‐Stark K (2011) Global value chain analysis: a primer. Center on Globalization, Governance & Competitiveness, Durham, NC

Goldberg PK, Khandelwal A, Pavcnik N, Topalova P (2010) Imported intermediate inputs and domestic product growth: evidence from India. Q J Econ 125(4):1727–1767

Gu W, Yan B (2016) Productivity growth and international competitiveness. Rev Income Wealth 63:1–21

Hartwig J, Krämer H (2019) The ‘Growth Disease’ at 50 – Baumol after Oulton. Struct Chang Econ Dyn 51:463–471

Hausmann R, Klinger B (2006) Structural Transformation and Patterns of Comparative Advantage in the Product Space. Working Paper Series 2006.128, Harvard University, Cambridge

Hidalgo C, Hausmann R (2009) The building blocks of economic complexity. Proc Natl Acad Sci USA 106(26):10570–10575

Hirschman AO (1958) The Strategy of Economic Development. Yale University Press, New Haven

Hulten CR (1978) Growth accounting with intermediate inputs. Rev Econ Stud 45:511–518

Hulten, C (2010) Growth Accounting, In B Hall and N. Rosenberg eds, Handbook of the Economics of Innovation, North-Holland, Volume 2, pp 987–1031

Jones CI (2011) Intermediate goods and weak links in the theory of economic development. Am Econ J 3:1–28

Jorgenson D (2018) Production and welfare: progress in economic measurement. J Econ Liter 56:867–919

Jorgenson D, Stiroh K (2000) US economic growth at the industry level. Am Econ Rev 90:161–167

Jorgeson DW, Gollop FM, Fraumeni BM (1987) Productivity and US Economic Growth. Harvard University Press, Cambridge

Leontief WW (1936) Quantitative input and output relations in the economic system of the United States. Rev Econ Stat 1:105–125

Lind D (2020) A vertically integrated perspective on nordic manufacturing productivity. Int Prod Monitor 39:53–73

Marconi N, Rocha IL, Magacho GR (2016) Sectoral capabilities and productive structure: An input-output analysis of the key sectors of the Brazilian economy. Braz J Pol Econ 36(3):470–492

Nassif A, Lucilene M, Araújo E, Feijó C (2020) Structural change and productivity growth in Brazil: where do we stand? Brazil. J Polit Econ 40:2

Nordhaus W (2008) Baumol's Diseases: A Macroeconomic Perspective. The B.E. Journal of Macroeconomics 8: 1–37

Oliner SD, Sichel DE (2000) The resurgence of growth in the late 1990s: is information technology the story? J Econ Perspect 14:3–22

Oulton N (2001) Must the growth rate decline? baumol’s unbalanced growth revisited. Oxf Econ Pap 53(4):605–627

Oulton N, O’Mahony M (1994) Productivity and growth: a study of British industry 1954–1986. Cambridge University Press, Cambridge

Sasaki H (2007) The rise of service employment and its impact on aggregate productivity growth. Struct Chang Econ Dyn 18(4):438–459

Sasaki H (2020) Is growth declining in the service economy? Struct Change Econ Dyn 53:26–38

Solow R (1956) A contribution to the theory of economic growth. Quart J Econ 70:65–94

Solow R (1957) Technical change and the aggregate production function. Rev Econ Stat 39(3):312–320

Strobel Thomas (2016) ICT intermediates and productivity spillovers—Evidence from German and US manufacturing sectors. Structural Change and Economic Dynamics 37(C):147–163

Szirmai A (2012) Industrialization as an engine of growth in developing countries, 1950–2005. Struct Chang Econ Dyn 23:406–420

Szirmai, A, Naudé W and Alcorta, L (2013) Pathways to Industrialization in the Twenty-First Century: New Challenges and Emerging Paradigms. Oxford: Oxford University Press

Ten Raa T, Shestalova V (2011) The Solow residual, Domar aggregation, and inefficiency: a synthesis of TFP measures. J Prod Analy. 36(1):71–77

Timmer MP, Van Ark B (2005) Does Information and Communication Technology Drive EU-US Productivity Growth Differentials? Oxford Econ Papers. 57(4):693–716

Timmer MP, Dietzenbacher E, Los B, Stehrer R, De Vries GJ (2015) An illustrated user guide to the world input–output database: the case of global automotive production. Rev Int Econ 23(3):575–605

Tregenna F (2009) Characterising deindustrialisation: an analysis of changes in manufacturing employment and output internationally. Camb J Econ 33:433–466

Wolff E (2013) Productivity convergence: theory and evidence. Cambridge University Press, Cambridge

Acknowledgements

We wish to thank useful comments from two anonymous reviewers, Andrew Trigg and the participants of the Seminar on Production and Structural Change, hosted by The Open University and held at Hamilton House in London. The usual disclaimer applies.

Funding

Ricardo Araujo wishes to thank financial support from CNPq and Capes/Proex/Print-UnB. Theo Santini whishes to thank Capes/Print-UnB.

Author information

Authors and Affiliations

Contributions

All authors contributed equally to all sections. Both authors read and approved the final manuscript.

Corresponding author

Ethics declarations

Competing interests

None of the authors have any competing interests in the manuscript.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Santini, T., Araujo, R.A. Productivity growth and sectoral interactions under Domar aggregation: a study for the Brazilian economy from 2000 to 2014. Economic Structures 10, 14 (2021). https://doi.org/10.1186/s40008-021-00243-7

Received:

Revised:

Accepted:

Published:

DOI: https://doi.org/10.1186/s40008-021-00243-7