Abstract

Background

Increasing financial risk protection is a key feature of Universal Health Coverage and the path towards health for all. Publicly Funded Health Insurance Schemes (PFHIS) have been considered as one of the pathways to safeguard against financial shocks and potentially reduce Out-of-Pocket Expenditure (OOPE). The south Indian state of Kerala has roughly a decade-long experience in implementing PFHIS. To date, there have been very few assessments of the coverage of these schemes and their impact on expenditure. Aiming to fill this gap, we explored the extent of and inequalities in insurance coverage, as well as choice of providers, and median cost of hospitalization in Kerala among insured and uninsured individuals.

Methods

A cross-sectional household survey was conducted in four districts of Kerala as part of a larger health systems research study from July–October 2019. We employed multistage random sampling to collect data from 13,064 individuals covering 3234 households in the catchment area of eight primary health care facilities. We used descriptive statistics, bivariate and multivariate analysis. We evaluated socioeconomic disparities using an absolute measure of inequality—the Slope Index of Inequality (SII) and a relative measure—the Relative Concentration Index (RCI).

Results

A substantial proportion of our study respondents reported that they were covered by PFHIS (45.8%). Respondents belonging to lowest and middle wealth quintiles of household had significantly greater odds of being covered by insurance than respondents belonging to the richest wealth quintile. The negative magnitude of RCI [-16.8% (95%CI: -25.3, -8.4)] and SII [-21.5% (95%CI: -36.1, -7.0)] suggest a higher concentration of PFHIS coverage among the poor. Median OOPE for hospitalisation at private health facilities was INR 9000 (approx. USD 108.70) among those covered by PFHIS, whereas it was INR 10500 (approx. USD 126.82) at private health facilities among those not covered by insurance.

Conclusion

While PFHIS seems to be appropriately targeting poorer populations, among the insured, OOPE for hospitalization persists. Among the uninsured, population subgroups with advantage are spending the greatest amount, raising questions about whether those facing relative disadvantage are forgoing care altogether or seeking care using cheaper, public avenues. Further policy action to more effectively reduce financial burden among left behind eligible populations under PFHIS will be essential to UHC progress in the state.

Similar content being viewed by others

Background

Sustainable Development Goal (SDGs) 3.8 of the United Nations calls for countries to progressively achieve Universal Health Coverage (UHC) through coverage of a wide range of services across population subgroups, assuring financial risk protection [1, 2]. For this, latter commitment of increasing financial risk protection and averting catastrophic expenditure, Publicly Funded Health Insurance Schemes (PFHIS) are considered a key strategy in many developing countries [3, 4]. PFHIS in developing countries may improve service access and avert financial catastrophe among those seeking in-patient care [4,5,6]. There remain many gaps, however.

A wide range of PFHIS programs were introduced by various state governments as well as the national government over the past two decades. The Universal Health Insurance scheme was introduced by the Central government in 2003 and later revamped in 2008 to become the Rashtriya Swasthya Bhima Yojana (RSBY) [7]. This scheme offered health insurance coverage of Rs.30000/- (approx. USD 364.88) to five members of Below Poverty Line (BPL)Footnote 1 families for hospitalization on a floater basisFootnote 2 [7, 8].

Many studies have evaluated the effects of PFHIS in India with regards to enrolment, utilization, Out-of-Pocket Expenditure (OOPE), and access to healthcare [9,10,11,12,13,14,15,16]. A majority of the studies report that while PFHIS have had little to no impact in reducing OOPE [9, 10, 13, 15, 17], they have improved access and utilization of healthcare services [14,15,16]. The majority of the data on the impact of PFHIS in India shows that it has not succeeded in providing financial security [4, 5, 17,18,19,20,21,22,23]. A few studies have documented reduced out-of-pocket expenditure (OOPE) as a result of PFHIS [24,25,26]. According to some studies, there has been an increase in inpatient care usage as a result of PFHIS [17, 18, 21, 24]. On the contrary some studies have not found evidence of increased hospital utilization due to PFHIS [4, 22].

Kerala, a state in South India, has prioritized welfare schemes and gained over a decade of experience in implementing PFHIS. Kerala’s journey began with pilots of the RSBY scheme in Kollam and Alappuzha districts in 2008 [27]. The scheme was scaled up to all 14 districts of the state in the same year with further addition of eligible beneficiaries under the scheme [27]. Families belonging to the BPL category listed by the Central government were provided coverage under the RSBY scheme, while families listed by the state were covered under the Comprehensive Health Insurance Scheme (CHIS) [27]. The option for Above Poverty Line (APL) families in the state to get covered under this health insurance scheme was launched during the initial years of implementation of CHIS, where these families had to pay a premium to enjoy the benefits of the scheme [28], this facility was discontinued in later years. In 2011, the Kerala government introduced an additional support amount of Rs.70000/- (∼USD 850) to RSBY and CHIS eligible families seeking care for chronic disease conditions relating to heart, kidney, liver, and trauma care [29].Footnote 3

In 2017, the state implemented the Senior Citizens Comprehensive Health Insurance Scheme (SCHIS) which provided an additional coverage of Rs. 30000/- (∼USD 364.88) for hospitalization of people aged above 60 years beyond [32]. Apart from the PFHIS targeting the poor and informal sector in the state, Kerala also implements the Employees State Insurance Scheme (ESIS) targeting workers in the formal sector and the Central Government Health Scheme (CGHS), which caters to civil servants/ those in government service [33].

Despite the state having a decade-long experience in implementing PFHIS, the burden of OOPE in the state remains large [34,35,36]. The recent National Health Accounts (NHA 2018–19) indicate that Kerala has the highest OOPE on health at Rs. 6,772 per capita (∼USD 82) at the point of receiving health care by households when compared with other states in the country [37]. National Sample Survey (NSO) 75th round also found higher out-of-pocket medical expenses (Rs.4,469, USD 54) and in the private sector hospitals (Rs.28,775, USD 350) in Kerala when compared with other Indian states [38]. This suggests that Kerala follows the national trend of PFHIS increasing service utilisation and not reducing OOPE.

As part of a larger health systems study, we carried out an analysis of primary household survey data to determine how PFHIS coverage relates to service utilisation and expenditure comparing the insured to the uninsured. The main objective of this study was to identify the factors that contribute to PFHIS coverage and socio-economic inequalities in its coverage in Kerala. We further analysed how hospitalisation and out-of-pocket expenditure on hospitalisation were distributed by PFHIS coverage across public and private health facilities, as well as socio-demographic and economic subgroups in the state.

Materials and methods

Study setting

A cross-sectional household survey was conducted in four districts of Kerala as part of a larger health systems research study from July–October 2019. All fourteen districts of the state were grouped into four categories based on an index generated using selected health indicators and data on determinants of health sourced from the National Family Health Survey (NFHS 2015–16). One district per group was randomly chosen, and one Family Health Centre (FHC) and one Primary Health Centre (PHC) in that district were randomly selected. Household level data collection was conducted in the institutional catchment areas following a multi-stage random sampling. Detailed Information on data collection, household survey methods and sampling size calculation is reported elsewhere [39].

Study tools

We gathered information from 3,234 households and the questionnaire consisted of various sections covering individual demographics, health information, hospitalization, outpatient care, and out-of-pocket expenses. Information on selected indicators were collected using data from different subsamples. The indicators selected in this study are categorized into following: (i) total population covered by any Insurance (ii) insurance coverage by type of insurance, (iii) choice of inpatient care by insured and uninsured population, and (iv) mean and median out-of-pocket expenditure (OOPE) for hospitalization by insured and uninsured population.

Data on insurance coverage was obtained from 13,064 individuals by asking them whether they were covered or not covered under any type of insurance. Participants who were covered under any insurance scheme were asked to specify the scheme in which they were enrolled (PFHIS (RSBY/CHIS/AB-PMJAY/KASP), Central Government Health Insurance Schemes (CGHS,ESIS,ECHS etc.), State Government Health Insurance scheme for employees (MEDISEP), community health insurance, health insurance provided by a micro finance institution, health insurance provided by private employer, private health insurance, or others). We analysed 13,054 cases but had to exclude 10 transgenderFootnote 4 persons in our sample as we were underpowered to make any inferences about this population subgroup. We categorized the extent of health insurance coverage under three groups; population covered under PFHIS, population covered under private or community based insurance, and population not covered by any insurance. A total sample of 11,832 people (excluding 1222 cases of non-PFHIS coverage) of individuals covered under PFHIS were included for this analysis.

Information regarding inpatient care was obtained from 1055 participants who said they had experienced hospitalization at any point 365 days prior to the survey. From these individuals, we collected data on (i) nature of ailment, (ii) type of care and (iii) medical and non-medical expenditures incurred for inpatient visits. We excluded 104 individuals who were covered under non-PFHIS and 951 cases of those who were covered by PFHIS and not covered by any insurance are included for this analysis.

Variables used in this study

Outcome variable

PFHIS coverage was the primary outcome variable for this study which was created using the information from response give by participants on their status of enrolment under any insurance schemes. For this analysis we excluded individuals covered by any private and other social health insurance schemes, as they were small proportion (2.74% in CGHS, ESIS, ECHS etc., 3.03% in State Government Health Insurance scheme for employees, 3.29% in community health insurance, 0.08% in health insurance provided by a micro finance institution, 0.01% in health insurance provided by private employer, and 0.22% private health insurance, or others) of our overall sample.

Therefore, we were comparing the population covered by PFHIS to those not covered by any health insurance.

Another outcome variable was Out- of -Pocket expenditure (OOPE) on hospitalization. Information on OOPE was collected as a part of hospitalization within a reference period of 365 days prior to the survey. Information was collected across nine sub-components: Service fee (includes doctors’ fees/ bed charges/ OT charges), diagnostic tests, medicines & consumables (from the hospital/clinic visited or from outside), lodging of the escort/attendant, transportation costs for patient, informal payments, and other medical expenses (attendant charges, expense for physiotherapy, personal medical devices, blood, and oxygen). The OOPE was derived from the total expenditure minus reimbursement.

Independent variable

Following convention, we included sex (male, female), marital status (never married, currently married, currently not married), religion (Hindu, Muslim, Others (Christian, Sikhs, Jain, and others.)), caste (Scheduled Caste [SC], Scheduled Tribe [ST], Other Backward Caste [OBC], Other),Footnote 5 and household wealth quintile (poorest, poorer, middle, richer, richest), status of hospitalization in the past year and sector of hospitalization (no or yes and for yes, whether in public or private sector).

To determine the economic status of households, a wealth index was used. This index was established by considering various economic indicators such as household assets, access to safe water and sanitation, and land ownership. The data was separated into dichotomous variables, and principal component analysis (PCA) was applied to assign weights to each indicator. The resulting wealth index was categorized into five quintiles ranging from the poorest to the richest [42]. Hospitalization in public and private hospitals was determined by a question which asked hospitalised individuals “where did you seek care?”. Public hospitalization includes Sub centre/ASHA/AWW etc., PHC, FHC, CHC, Sub District/Taluk Hospital, District Hospital, Medical College Hospital, ESI/ECHS/ CGHS Hospital, General Hospital, Women and Child Hospital, Government supported/subsidised/Jan dhan/Karunya pharmacies, Public Ayurveda facility, Public Homeopathy facility and Other public health facility. Private hospitalization includes private doctor/ clinic, private nursing home, private hospital, charitable/ Trust Hospital, private multi/ super specialty hospital, private medical college, private pharmacy, private lab, Registered Medical Practitioner, Traditional healer, private Ayurveda doctor, private Ayurveda facility, private Homeopathic doctor, private Homeopathic facility, and other private health facilities.

Analysis

The analysis approach used both descriptive and statistical analyses, including bivariate and multivariate analyses. Descriptive statistics displayed the distribution of participants according to independent and outcome variables. Categorical variables were expressed in frequencies and proportions, with all proportions calculated after eliminating missing data.

We utilized bivariate analysis to explore the correlation between independent variables and PFHIS coverage, the outcome variable. Furthermore, we employed multivariable logistic regression analyses to investigate the connection between independent and dependent variables. To conduct multivariate analyses, the regression model included significant variables from the bivariate analysis (p < 0.05) such as gender, marital status, hospitalization in the past year, wealth quintile, social group, and religion. This was done to control any potential confounding factors between them. The findings of the logistic regression study provided estimates of odds ratios, adjusted and unadjusted, based on sociodemographic characteristics, accompanied by 95% confidence intervals.

To access the socioeconomic inequality in PFHIS coverage in Kerala, concentration curve (CC), relative concentration index (RCI) and slope index of inequality (SII) were used. RCI was used to measure relative inequality and SII was used to measure absolute inequality [43,44,45]. The SII is a measure of the difference between predicted health indicator values for the richest and poorest wealth quintiles. It accounts for the entire distribution of the stratification variable using an appropriate regression model. The goal is to ensure accurate and fair assessment of the health indicator differences across socioeconomic groups [43, 45, 46]. The calculation of SII is generally based on a linear regression model. However, the logistic regression model is more suitable for its computation. This is because it is typically used to assess the coverage of indicators and the prevalence of health outcomes. Additionally, it avoids making linear predictions that fall outside the expected interval of a proportion, which ranges from 0 to 100 [43]. In terms of proportions, the absolute difference between the group and the SII falls within the range of -100 to 100 percentage points. Values of SII close to zero mean there is no inequality, negative values revealed that the indicator is concentrated in disadvantaged households, while a positive value of SII indicates that the indicator is concentrated in the most advantaged groups.

A relative summary measure is unique because it lacks units, making it easier to compare different indicators. The RCI value is equivalent to twice the area between a diagonal line representing perfect equality among groups and the curve that shows the coverage for each cumulative percentage of the population studied. If coverage is higher among the wealthiest individuals in the top quintile, the area generated is below the diagonal line. Conversely, if coverage is higher among the poorest individuals in the bottom quintile, the area generated is above the diagonal line [47]. The RCI values range from -1 to + 1, with zero representing equality. The further the values are from zero, the greater the relative inequality [43, 44, 48]. In our study, we multiplied the SII and RCI results by 100 to make them easier to visualize in tables and graphs, with a range of -100 to + 100.

Further, we analyzed the proprotions of hospitalized individuals by PFHIS coverage according to gender, marital status, hospitalization in the past one year and by wealth quintile, social group, and religion. We have also estimated mean and median OOPEfor hospitalization among those covered by PFHIS and individuals not covered by any insurance.

The statistical analyses were performed using Stata®17 MP version (StataCorp LLC, Lakeway Drive College Station, Texas, USA), with the relevant sampling weight variables applied in the dataset.

Ethics approval

The Institutional Ethics Committee of the George Institute for Global Health granted approval for the study (Project Number 05/2019). Additional permissions were obtained from Department of Health and Family Welfare (DHFW) Kerala. While conducting the study, each health facility and concerned local self-government body was appraised about the purpose of the study. Participants provided written consent and data was stored securely on password-protected servers.

Results

Participant characteristics

The study participants' socio-demographic characteristics are summarized in Table 1. About 53% of our sample comprised females and 47% comprised males (in addition to this, we had a sample of 10 trans individuals whom we could not include in subsequent analyses). Around 55% respondents were currently married. More than one -third of the participants belonged to the bottom two quintiles (poorest and poorer). About more than three-fifths belonged to the OBC category (62.8%). Most of the respondents belonged to Hindu religion (65%) followed by Muslims (18.5%) and Christian or others (16.5%). It was observed that about 8.2% respondents had been hospitalized in the previous year.

Association between PFHIS coverage and participants characteristics

Table 2 presents the percentage distribution of respondents by PFHIS coverage according to selected background characteristics. Table 2 also present the results of association between PFHIS coverage and background characteristics of participants. Overall, equal proportion of respondents were covered by PFHIS and not covered by any health insurance /schemes in Kerala. Bivariate analysis of PFHIS coverage by gender shows that a slightly greater proportion of females (51.3% females vs 49% males) was covered by PFHIS. Adjusted analysis also showed that females respondents had significantly higher odds [AOR: 1.17, 95% CI: 1.08, 1.26] of being covered by PFHIS than males’ counterparts. Never married respondents had significantly lower odds [AOR: 0.82, 95%CI: 0.73, 0.88] of being covered by PFHIS than the currently married respondents. A negative gradient was observed in the PFHIS coverage among respondents moving from poorest wealth quintile (57.5%) to richest wealth quintile (37%). Adjusted analysis also showed that odds of being covered by PFHIS decreased from poorest wealth quintile to richer wealth quintile, however, respondents belonging to the poorest [AOR:2.21, 95%CI: 1.94, 2.51], poorer [AOR: 2.09, 95%CI: 1.85, 2.37], middle [AOR: 2.06, 95%CI: 1.82, 2.34] and richer wealth quintile [ AOR: 1.67, 95%CI: 1.48, 1.89] of households had significantly greater odds of being covered by PFHIS than the richest wealth quintile. A greater proportion of respondents belonging to SC group (60.7%) were covered by PFHIS followed by Others (51.0%), OBC (48.8%), and ST(45.7%). Respondents belonging to SCgroup had significantly higher odds [AOR: 1.29, 95%CI: 1.10, 1.51] of being covered by PFHIS after controlling for other variables in the logistic regression analysis. Respondents belonging to ST and OBC caste group had significantly lower odds of being covered by any health insurance. PFHIS coverage was higher among respondents belonging Hindu (53.7%), followed by Muslim (44.9%) and Christian & Others religious group (43.1%). It was found that respondents belonging to Muslim [AOR: 0.76, 95%CI: 0.69, 0.84] and Christian or other religious groups (AOR: 0.65, 95%CI: 0.58, 0.73] had significantly lower odds of being covered by PFHIS. Respondents who were hospitalized in the past year had 22% higher odds [AOR:1.22, 95%CI: 1.07, 1.40] of being covered by PFHIS than those not hospitalised.

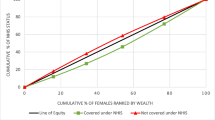

Inequalities in PFHIS coverage

Table 3, Figs. 1 and 2 shows the absolute (SII), and relative (CIX) measures of economic inequality for PFHIS coverage by socio-demographic characteristics. Overall, negative magnitude of RCI [-16.8% (95%CI: -25.3, -8.4)] and SII [-21.5% (95%CI: -36.1, -7.0)] suggests a higher concentration of PFHIS coverage among the poor. Absolute and relative economic inequality in PFHIS coverage was higher in females [SII: -26.7% (95%CI: -37.8, -15.6); RCI: -18.2% (95%CI: -26.3, -10.1)] as compared to males [SII: -21.5% (95%CI: -36.1, -7.0); RCI: -15.2% (95%CI: -25.5, -4.9)]. Absolute and relative economic inequality in PFHIS coverage was significantly higher among those who were hospitalized in the past year [SII: -40.4% (95%CI: -63.9, -16.8); RCI: -28.8% (95%CI: -45.7, -12.1)] as compared to those who were not hospitalised. Among SC and ST sub-groups, economic inequality was not significant. Other (majority) social groups had higher absolute [SII: -29.4% (95%CI: -51.1, -7.7)] and relative economic inequality [RCI: -19.7% (95%CI: -34.5, -4.5)] in PFHIS coverage as compared to other groups. Among Muslims, absolute [SII: -35.1% (95%CI: -54.2, -16.0)] and relative economic inequality [RCI: -22.6% (95%CI: -35.7, -9.5)] was highest compared to Hindus and Other religious groups.

Concentration curve for PFHIS coverage in Kerala

Slope index of inequality for PFHIS coverage in Kerala

Hospitalization by PFHIS coverage

Table 4 presents the distribution of respondents hospitalised in the past year by PFHIS coverage according to their socio-demographic characteristics. A total of 55.7% of respondents who were hospitalized were covered by PFHIS. Compared to females, males who were hospitalized in the past year had higher PFHIS coverage (59.7% vs. 52.4%). Respondents who were hospitalised in the past year from the poorest wealth quintile (68.0%) had the highest PFHIS coverage, followed by poorer (60.2%), middle (57.9%), richer (47.0%) and richest wealth quintile (41.1%). PFHIS coverage was highest among SC respondents hospitalised in the past year (64.7%), followed by OBC (55.2%). Hindu respondents (60.4%) had higher PFHIS coverage compared to Muslim (50.2%), Christian and other religious groups (44.1%) who were hospitalised in the past year. Notably, respondents hospitalised in public facilities (62.9%) had higher PFHIS coverage compared to respondents hospitalised in private facilities (48.3%).

Out-of-pocket expenditure for hospitalization

Table 5 presents the mean and median OOPE for hospitalisation among those covered by PFHIS and not covered by any insurance. Overall, PFHIS was associated with lower OOPE across all groups. The median OOPE for hospitalisation at private health facilities was INR 9000 (∼USD 10.96) among those covered by PFHIS, whereas it was INR 10500 (∼USD 127.91) at private health facilities among those not covered by insurance. Among those who covered by PFHIS, median OOPE was higher among males (INR 3300, ∼ USD 40.20) compared to females (INR 1900, ∼USD 23.15), whereas median OOPE was slightly higher among females (INR 6000, ∼USD 73.09) as compared to males (INR 5750, ∼USD 70.04) who were not covered by any insurance. The median OOPE for hospitalisation was higher among married participants as compared to other categories of marital status, weather covered by PFHIS (INR 3000, ∼USD 36.54) or not covered by any insurance (INR 6000, ∼USD 73.09). Median OOPE for hospitalisation was zero among SC groups, whether covered by PFHIS or not covered by any insurance. Among those covered by PFHIS, the median OOPE for hospitalisation among OBC social group (INR 2900, ∼USD 35.33) was comparatively higher than the other social caste group. Similarly, among those covered by PFHIS, the median OOPE was highest among Muslims (INR 5000, ∼USD 60.91), whereas, for those not covered by insurance, the median OOPE was highest among Christians and other religious groups (INR 8000, ∼USD 97.45). Median OOPE for hospitalisation was highest among the richest wealth quintile whether covered by PFHIS (INR 4600, ∼USD 56.04) or not (INR 9000, ∼USD 109.63). The payment threshold of INR 4600 (USD 56.04) was crossed by other wealth quintiles not covered by any insurance (i.e., richer (INR 6000, ∼USD 73.09) and poorer wealth quintiles (INR 5300, ∼USD 64.56)).

Discussion

PFHIS was intended to play an integral role in moving towards UHC. Our study found a substantial proportion of respondents covered under PFHIS in the state. This is consistent with the findings from the latest National Family Health Survey (NFHS-5) which reports more than 50% of households (51.5%) in the state with at least one member covered by health insurance [49]. A higher proportion of participants in the lowest quintiles (poorest, poor & middle) were found to be covered under PFHIS in the state, which is a feature of the design of the insurance and is to be expected. Across social groups, SC and OBC households had higher coverage, yet insurance coverage was found to be relatively lower among the ST households in the state. A study examining the impact of RSBY/CHIS scheme in the state reported that the most marginalized population in the state like the SC, households are left behind from getting enrolled under the scheme [50]. A study conducted by Neena et al. 2015, in Kerala reported similar findings [51]. This said, median costs incurred in this group with or without insurance was zero, suggesting mechanisms for financial protection likely exist for them independent of insurance (we discuss this more later).

NITI Aayog, the official “think tank” of Government of India, in their 2021 report on health insurance for India’s missing middle concluded that at least 30% of the Indian population was not covered under any health insurance, which is spreads across all income quintiles in urban and rural areas [52]. Results from a 2021 study by Singh and colleagues in India showed that states with higher penetration of PFHIS among richer quintiles have failed to cover disadvantaged populations [53]. Similar results have been seen in studies in LMICs: PFHIS enrolment often misses disadvantaged populations and is instead covering wealthier quintiles [54, 55]. Studies cite lack of awareness and political will as major reasons for low coverage of eligible populations [56, 57].

This is a dynamic area of policymaking as well. To universalise coverage, in 2020, the state of Kerala decided to converge all the Government sponsored health care schemes like Comprehensive Health Insurance Scheme-CHIS, Senior Citizen Health Insurance Scheme-SCHIS, Karunya Benevolent Fund-KBF. Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (PMJAY) and Karunya Arogya Suraksha Padhathi (KASP) [58, 59]. However, the beneficiary base for this converged scheme remains the same as for individual sub-schemes in 2023, meaning that eligible populations who were already left behind do not yet have an option to enrol and be covered. Apart from being an obvious area of policy making and/or adaptation, further study by way of evaluation or time-series analysis may shed light on how scheme convergence affects health seeking and health of populations (or not, as the case may be). This may lead to further insights on how both breadth and depth of coverage may be optimized. Moreover, research should explore community preferences and motivations for not utilising PFHIS, even if enrolled.

We found a considerable difference in hospitalization between males and females covered by PFHIS. A higher proportion of males sought care through PFHIS even when our study showed higher coverage of PFHIS among females in the state. The higher coverage of females under PFHIS is consistent with the findings of studies from LMICs [60,61,62]. The utilization pattern of PFHIS among females in Kerala needs to be further explored. Findings from a study in Tamil Nadu, nearby south Indian state showed higher enrolment coverage among females and significantly lesser utilization than males [63]. Another study in Tamil Nadu by Ramakrishnan and colleagues concluded that gender barriers at the household, community and programme level were associated with reduced uptake of hospitalisation among PHFIS females enrollees [64]. Further mixed methods research can shed light on whether/how barriers are shared or unique across these two southern states.

Our study also found that found that hospitalization through PFHIS was higher among populations belonging to the poorest quintile followed by poorer and middle. This is a positive sign suggesting that there is access to insurance among disadvantaged populations in the state. Studies from India and other countries have found that health insurance has increased the portability of seeking care and reduce delays [65,66,67,68,69]. Private sector facilities were found to be the most preferred among both insured and non-insured populations due to ease of access and perceived quality of care in Kerala [70]. Adding to this, since insured populations actually have the choice to choose between public and empanelled private facilities, [69] insured persons from the lowest socio-economic strata may be exercising this choice and choosing private sector facilities in greater numbers, as has been seen in other LMICs as well [71,72,73,74]. While analysing the share of hospitalization among public and private sector facilities, we found that participants hospitalized in public hospitals had higher chance of getting benefits through PFHIS (62.9% vs 48.3%). This can be attributed to the availability, access and equitable distribution of public and private empanelled healthcare facilities having specialities for which the population seek care. A study by Joseph and colleagues, found that more than half of the empanelled facilities under ABPMJAY were public sector facilities and only 14% of them offered care for all specialities covered under the scheme [75]. A study done in Chhattisgarh reported low distribution of empanelled private hospitals in disadvantaged districts,Footnote 6 where eligible population numbers were, as compared to public sector hospitals, which were evenly distributed in disadvantaged districts [76]. Equitable insurance coverage does not always ensure equitable access to healthcare, while it is dependent on the availability of service providers which needs to be taken care for achieving UHC. Greater analysis of foregone care using population-based studies could help shed light on this.

In our study we found that median OOPE for hospitalization among insured participants was marginally lower than those not covered by insurance for both sexes. However, higher median OOPE was observed among insured males, whereas uninsured females had higher slightly spending for hospitalization as compared to uninsured males. This is consistent with the findings of National Health Accounts 2018–19 which reports people in Kerala were reportedly spending 2.5 times more than those in other southern states of India [77]. Studies in LMICs have reported despite being covered by PFHIS, patients incur OOPE [55, 67, 68, 78,79,80,81]. This may be attributed to package design (which is focused on inpatient care only and even in that context, may not cover the entire gamut of expenses incurred) – this is another area that requires study using mixed methods. We also found zero OOPE reported by SC groups irrespective of their coverage under PFHIS. Apart from being covered under PFHIS, this may be attributed to the healthcare scheme implemented by the Scheduled Tribes Development Department which provides free diagnosis, treatment, medication, medical aids, transportation, food expenses and pocket money for bystanders during hospitalization [82, 83].

To summarize, PFHIS are tailormade to cover economically and socially disadvantaged sections of the society: it is therefore important to estimate their actual reach and coverage among eligible populations. This requires research to estimate the true denominators of eligible populations; one such exercise has been underway through the Kerala “poorest households” initiative, which may serve as a proxy for many (but not all) groups facing disadvantage [84]. Also, it is important to understand the experiences and pathways of catastrophic health expenditure, through which population which are pushed to impoverishment due to health expenditure and ensure these households are covered through PFHIS. It is also important to continue to monitor the availability and distribution of empanelled health care providers under PFHIS in the state, as well as the services coverage they offer, which are vital in ensuring access as well as financial risk protection.

Limitations

Our study revealed several important findings about the status of implementation of PFHIS in Kerala. However, there are some limitations that warrant mention. Our study measured self-reported coverage and expenses, which can lead to over- or underestimation because of recall bias. We did not gather or compute data on place of residence and thus did not examine rural–urban differences in health insurance coverage in the four districts: this could be explored further and will likely require differentiated sampling for urban and rural areas. As aforementioned, we were underpowered to look at differences in coverage, utilisation, and spending among trans persons in our sample. Future research should explore these population subgroups specifically to arrive at key drivers of under enrolment, under-utilisation, and expenditure.

Conclusion

Despite most of the participants being enrolled under PFHIS insurance in Kerala, our study found that OOP expenses continue to burden households across four districts of the state. While PFHIS seems to be appropriately targeting poorer populations, among the insured, the greatest costs are borne by populations with historical advantage. Among the uninsured, wealthier population subgroups were spending the greatest amount, raising questions about whether those in poorer income groups were forgoing care altogether or seeking care using cheaper, public avenues.

Availability of data and materials

All datasets used for supporting the conclusions of this paper are available from the corresponding author on request.

Notes

Individuals or households whose consumption expenditures fall below the poverty line of $1.90 per person per day are classified as "Below the Poverty Line (BPL)" and considered to be living in poverty.

On a family floater basis, the entire benefit package can be utilized by either one or all members of the family.

The state introduced another financial risk protection mechanism soon after this expansion, namely the Karunya Benevolent Fund (KBF). The KBF initiative was put in place by the Department of Lotteries and is funded by profits from the sale of Karunya weekly lotteries. It offers a one-time financial aid of 2 lakhs to families with an annual income below 3 lakhs who are dealing with high-cost health conditions [30, 31].

We asked each participant to self report their gender. We had a sample of 10 persons who identified as trans. Given this relatively small sample size and our analytical approach, we regrettably had to remove them from analysis.

Scheduled Tribe’ and ‘Scheduled Caste’ are the tribal and caste groups recognized by the President of India according to article numbers 341 and 342 of the Constitution of India [40]. ‘Backward Class’ is the term used by the Government of India to classify groups that are educationally or socially disadvantaged [41].

The vulnerability tertiles of the districts were determined by mapping the availability of public and private facilities per 100,000 enrolled population.

Abbreviations

- SDGs:

-

Sustainable Development Goals

- UHC:

-

Universal Health Coverage

- PFHIS:

-

Publicly Funded Health Insurance Schemes

- RSBY:

-

Rashtriya Swasthya Bhima Yojana

- OOPE:

-

Out-of-Pocket Expenditure

- BPL:

-

Below Poverty Line

- CHIS:

-

Comprehensive Health Insurance Scheme

- APL:

-

Above Poverty Line

- ESIS:

-

Employees State Insurance Scheme

- CGHS:

-

Central Government Health Scheme

- NHA:

-

National Health Accounts

- NSSO:

-

National Sample Survey Organization

- FHC:

-

Family Health Centre

- PHC:

-

Primary Health Centre

- PMJAY:

-

Pradhan Mantri Jan Arogya Yojana

- KASP:

-

Karunya Arogya Suraksha Paddathi

- MEDISEP:

-

Medical Insurance for State Employees and Pensioners

- SC:

-

Scheduled Caste

- ST:

-

Scheduled Tribe

- OBC:

-

Other Backward Class

References

Saksena P, Hsu J, Evans DB. Financial risk protection and universal health coverage: evidence and measurement challenges. PLoS Med. 2014;11(9):e1001701.

World Health Organization. SDG Target 3.8 | Achieve universal health coverage, including financial risk protection, access to quality essential health-care services and access to safe, effective, quality and affordable essential medicines and vaccines for all [Internet]. THE GLOBAL HEALTH OBSERVATORY Explore a world of health data. Available from: https://www.who.int/data/gho/data/themes/topics/indicator-groups/indicator-group-details/GHO/sdg-target-3.8-achieve-universal-health-coverage-(uhc)-including-financial-risk-protection. [cited 2023 Mar 8].

Barnes K, Mukherji A, Mullen P, Sood N. Financial risk protection from social health insurance. J Health Econ. 2017;55:14–29.

Ranjan A, Dixit P, Mukhopadhyay I, Thiagarajan S. Effectiveness of government strategies for financial protection against costs of hospitalization Care in India. BMC Public Health. 2018;18(1):501.

Garg S, Chowdhury S, Sundararaman T. Utilisation and financial protection for hospital care under publicly funded health insurance in three states in Southern India. BMC Health Serv Res. 2019;19(1):1004.

Ramprakash R, Lingam L. Publicly Funded Health Insurance Schemes (PFHIS): a systematic and interpretive review of studies: does gender equity matter? 2018.

Narayana D. Review of the Rashtriya Swasthya Bima Yojana. Econ Polit Wkly. 2010;45(29):13–8.

Government of India. Rashtriya Swasthya Bima Yojana| National Portal of India [Internet]. Rashtriya Swasthya Bima Yojana: health insurance for the poor. Available from: https://www.india.gov.in/spotlight/rashtriya-swasthya-bima-yojana. [cited 2023 Mar 9].

Garg S, Bebarta KK, Tripathi N. Performance of India’s national publicly funded health insurance scheme, Pradhan Mantri Jan Arogaya Yojana (PMJAY), in improving access and financial protection for hospital care: findings from household surveys in Chhattisgarh state. BMC Public Health. 2020;20(1):949.

Garg S, Bebarta KK, Tripathi N. Role of publicly funded health insurance in financial protection of the elderly from hospitalisation expenditure in India-findings from the longitudinal aging study. BMC Geriatr. 2022;22(1):572.

Harish R, Suresh RS, Rameesa S, Laiveishiwo PM, Loktongbam PS, Prajitha KC, et al. Health insurance coverage and its impact on out-of-pocket expenditures at a public sector hospital in Kerala, India. J Fam Med Prim Care. 2020;9(9):4956–61.

Joseph J, Sankar DH, Nambiar D. Empanelment of health care facilities under Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (AB PM-JAY) in India. PLoS One. 2021;16(5):e0251814.

Karan AK, Selvaraj S. Why publicly-financed health insurance schemes are ineffective in providing financial risk protection. econ polit wkly [Internet]. 2012;47(11). Available from: https://www.epw.in/journal/2012/11/special-articles/why-publicly-financed-health-insurance-schemes-are-ineffective. [cited 2023 Mar 9].

Malani A, Holtzman P, Imai K, Kinnan C, Miller M, Swaminathan S, et al. Effect of health insurance in india: a randomized controlled trial. Work Pap [Internet]. 2021. Available from: https://ideas.repec.org//p/hka/wpaper/2021-055.html. [cited 2023 Mar 9].

Reshmi B, Unnikrishnan B, Rajwar E, Parsekar SS, Vijayamma R, Venkatesh BT. Impact of public-funded health insurances in India on health care utilisation and financial risk protection: a systematic review. BMJ Open. 2021;11(12):e050077.

Sriram S, Khan MM. Effect of health insurance program for the poor on out-of-pocket inpatient care cost in India: evidence from a nationally representative cross-sectional survey. BMC Health Serv Res. 2020;20(1):839.

Karan A, Yip W, Mahal A. Extending health insurance to the poor in India: an impact evaluation of Rashtriya Swasthya Bima Yojana on out of pocket spending for healthcare. Soc Sci Med. 2017;181:83–92.

Ghosh S, Gupta ND. Targeting and effects of Rashtriya Swasthya Bima Yojana on access to care and financial protection. Soumitra Ghosh Nabanita Datta Gupta [Internet]. 2017;52(4). Available from: https://www.epw.in/journal/2017/4/special-articles/targeting-and-effects-rashtriya-swasthya-bima-yojana-access-care-and. [cited 2023 Mar 8].

Nandi S, Schneider H, Dixit P. Hospital utilization and out of pocket expenditure in public and private sectors under the universal government health insurance scheme in Chhattisgarh State, India: Lessons for universal health coverage. PLoS One. 2017;12(11):e0187904.

Philip NE, Kannan S, Sarma SP. Utilization of comprehensive health insurance scheme, kerala: a comparative study of insured and uninsured below-poverty-line households. Asia Pac J Public Health. 2016;28(1_suppl):77S–85S.

Prinja S, Chauhan AS, Karan A, Kaur G, Kumar R. Impact of publicly financed health insurance schemes on healthcare utilization and financial risk protection in India: a systematic review. PLoS One. 2017;12(2):e0170996.

Prinja S, Bahuguna P, Gupta I, Chowdhury S, Trivedi M. Role of insurance in determining utilization of healthcare and financial risk protection in India. PLoS One. 2019;14(2):e0211793.

Ravi S, Ahluwalia R, Bergkvist S. Health and morbidity in India (2004–2014) [Internet]. 2016. Report No.: Research Paper No. 092016. Available from: https://www.brookings.edu/research/paper-health-and-morbidity-in-india-2004-2014/. [cited 2023 Mar 8].

Fan VY, Karan A, Mahal A. State health insurance and out-of-pocket health expenditures in Andhra Pradesh, India. Int J Health Care Finance Econ. 2012;12(3):189–215.

Rao M, Katyal A, Singh PV, Samarth A, Bergkvist S, Kancharla M, et al. Changes in addressing inequalities in access to hospital care in Andhra Pradesh and Maharashtra states of India: a difference-in-differences study using repeated cross-sectional surveys. BMJ Open. 2014;4(6):e004471.

Sood N, Bendavid E, Mukherji A, Wagner Z, Nagpal S, Mullen P. Government health insurance for people below poverty line in India: quasi-experimental evaluation of insurance and health outcomes. BMJ. 2014;349:g5114.

Jisha CJ. The Comprehensive Health Insurance Scheme in Kerala (CHIS): an exploratory study in Kollam District. In: International public policy association [Internet]. GRENOBLE; 2015. Available from: https://www.ippapublicpolicy.org/file/paper/1435005314.pdf. [cited 2023 Mar 10].

Jayashree J. What the centre’s new health insurance scheme means for states that have their own [Internet]. The wire. 2018. Available from: https://thewire.in/economy/health-insurance-scheme-kerala-niti-aayog. [cited 2023 Mar 10].

The Indian Express. CHIS Plus a big hit in state [Internet]. The New Indian Express. 2011. Available from: https://www.newindianexpress.com/states/kerala/2011/nov/28/chis-plus-a-big-hit-in-state-314628.html. [cited 2023 Mar 10].

Karunya Benevolent Fund [Internet]. Available from: http://karunya.kerala.gov.in/. [cited 2022 Sep 1].

Indian Health Economics And Policy Health Economics And Policy Association (IHEPA) (jointly organised by IHEPA, IDSK and Azim Premji University) 5 Health Economics and Policy: Current - [PDF Document] [Internet]. vdocuments.net. Available from: https://vdocuments.net/indian-health-economics-and-policy-health-economics-and-policy-association-ihepa.html. [cited 2022 Sep 1].

Government of India. Chapter 12: Health Policy & Health Insurance: Annual Report 2018–19 | Ministry of Health and Family Welfare | GOI [Internet]. Ministry of Health & Family Welfare. 2019. Available from: https://main.mohfw.gov.in/basicpage/annual-report-2018-19. [cited 2023 Mar 10].

Madheswaran S, Sahoo AK. Out-Of-Pocket (OOP) Financial Risk Protection: The Role of Health Insurance. Work Pap [Internet]. 2015. Available from: https://ideas.repec.org//p/ess/wpaper/id7015.html. [cited 2023 Mar 10].

Bose M. State Health Accounts - Kerala, India. 2016.

Maya C. State tops in health-care spending. The Hindu [Internet]. 2016. Available from: https://www.thehindu.com/news/national/kerala/state-tops-in-healthcare-spending/article8530723.ece. [cited 2023 Mar 10].

Thayyil J, Jayakrishnan T. Morbidity and healthcare expenditure in Kerala. 2008.

National Health Accounts. National Health Accounts | National Health Systems Resource Centre [Internet]. National Health Systems Resource Centre. 2022. Available from: https://nhsrcindia.org/national-health-accounts-records. [cited 2023 Feb 13].

Government of India, Ministry of Statistics and Programme Implementation. Key Indicators of Social Consumption in India: Health [Internet]. New Delhi: National Statistics Office; 2019. (NSS 75th Round 2017–18). Report No.: NSS KI (75/25.0). Available from: https://www.mospi.gov.in/sites/default/files/publication_reports/KI_Health_75th_Final.pdf. [cited 2023 Mar 10].

Negi J, Nambiar D. Tracking the progress of primary care reforms in Kerala India: Findings from a baseline assessment. Euro J Public Health. 2020;30(Supplement_5):ckaa166.519.

MOPPP. Special Representation in Services for SC/ST. Department of Personnel and Training, Ministry of Personnel, Public grievances and Pensions, Government of India [Internet]. 2019. Available from: https://dopt.gov.in/sites/default/files/ch-11.pdf. [cited 2022 Nov 29].

MOSJE. Welfare of the Other Backward Classes. Ministry of Social Justice and Empowerment, Government of India [Internet]. 2020. Available from: https://socialjustice.gov.in/. [cited 2022 Nov 20].

Filmer D, Pritchett LH. Estimating wealth effects without expenditure data–or tears: an application to educational enrollments in states of India. Demography. 2001;38(1):115–32.

Barros AJD, Victora CG. Measuring coverage in MNCH: determining and interpreting inequalities in coverage of maternal, newborn, and child health interventions. PLoS Med. 2013;10(5):e1001390.

Harper S, Lynch J. Methods for Measuring Cancer Disparities - Relevant to Healthy People 2010 Objectives - SEER Publications [Internet]. Bethesda (Maryland): National Cancer Institute; 2005. Available from: https://seer.cancer.gov/archive/publications/disparities/index.html. [cited 2022 Aug 3].

Harper S, Lynch J. Selected Comparisons of Measures of Health Disparities - SEER Publications [Internet]. Bethesda (Maryland): National Cancer Institute; 2007. Available from: https://seer.cancer.gov/publications/disparities2/index.html. [cited 2022 Aug 4].

da Silva ICM, Restrepo-Mendez MC, Costa JC, Ewerling F, Hellwig F, Ferreira LZ, et al. Measurement of social inequalities in health: concepts and methodological approaches in the Brazilian context. Epidemiol E Serv Saude Rev Sist Unico Saude Bras. 2018;27(1):e000100017.

Dulgheroff PT, da Silva LS, Rinaldi AEM, Rezende LFM, Marques ES, Azeredo CM. Educational disparities in hypertension, diabetes, obesity and smoking in Brazil: a trend analysis of 578 977 adults from a national survey, 2007–2018. BMJ Open. 2021;11(7):e046154.

Bann D, Fluharty M, Hardy R, Scholes S. Socioeconomic inequalities in blood pressure: co-ordinated analysis of 147,775 participants from repeated birth cohort and cross-sectional datasets, 1989 to 2016. BMC Med. 2020;18(1):338.

Kerala.pdf [Internet]. Available from: http://rchiips.org/nfhs/NFHS-5Reports/Kerala.pdf. [cited 2022 Aug 2].

RSBYCHIS.pdf [Internet]. Available from: https://spb.kerala.gov.in/sites/default/files/inline-files/RSBYCHIS.pdf. [cited 2022 Aug 4].

Philip NE, Kannan S, Sarma SP. Utilization of Comprehensive Health Insurance Scheme, Kerala: a comparative study of insured and uninsured below-poverty-line households. Asia Pac J Public Health. 2016;28(1_suppl):77S–85S.

NITI Aayog. Health Insurance for India’s Missing Middle [Internet]. 2021. Available from: https://www.niti.gov.in/sites/default/files/2021-10/HealthInsurance-forIndiasMissingMiddle_28-10-2021.pdf. [cited 2023 Mar 27].

Singh V, Garg A, Laha AK, O’Neill S. Publicly financed health insurance schemes and horizontal inequity in inpatient service use in India. Asia Pac J Health Manag. 2021;16(1):52–63.

Anjorin SS, Ayorinde AA, Abba MS, Mensah D, Okolie EA, Uthman OA, et al. Equity of national publicly funded health insurance schemes under the universal health coverage agenda: a systematic review of studies conducted in Africa. J Public Health. 2022;44(4):900–9.

Osei Afriyie D, Krasniq B, Hooley B, Tediosi F, Fink G. Equity in health insurance schemes enrollment in low and middle-income countries: a systematic review and meta-analysis. Int J Equity Health. 2022;21(1):21.

Thakur H. Study of awareness, enrollment, and utilization of Rashtriya Swasthya Bima Yojana (National Health Insurance Scheme) in Maharashtra. India Front Public Health. 2015;3:282.

Kusuma YS, Pal M, Babu BV. Health insurance: awareness, utilization, and its determinants among the urban poor in Delhi, India. J Epidemiol Glob Health. 2018;8(1–2):69–76.

Karunya Arogya Suraksha Padhathi – sha [Internet]. Available from: https://sha.kerala.gov.in/karunya-arogya-suraksha-padhathi. [cited 2022 Aug 10].

Karunya Arogya Suraksha Padahathi, State Health Agency Kerala. Schedules for Service Contract of AB-PMJAY-KASP [Internet]. Department of Health and Family Welfare, Government of Kerala; 2020. Available from: https://arogyakeralam.gov.in/wp-content/uploads/2020/03/Schedules.pdf. [cited 2022 Jun 9].

Escobar ML, Griffin CC, Shaw RP. The Impact of Health Insurance in Low- and Middle-Income Countries [Internet]. 2010. Available from: https://www.brookings.edu/wp-content/uploads/2016/07/theimpactofhealthinsurance_fulltext.pdf. [cited 2023 Mar 28].

Hooda SK. Penetration and coverage of government-funded health insurance schemes in India. Clin Epidemiol Glob Health. 2020;8(4):1017–33.

Amu H, Seidu AA, Agbaglo E, Dowou RK, Ameyaw EK, Ahinkorah BO, et al. Mixed effects analysis of factors associated with health insurance coverage among women in sub-Saharan Africa. PLoS One. 2021;16(3):e0248411.

Ramprakash R, Arun J. Gender inequity in utilisation of publicly funded health insurance schemes: findings based on insurance data from a Southern Indian State --Is there a difference in utilisation of state sponsored health insurance between men and women? Asia Pacific Journal of Health Management. 2021;16:Special issue.

RamPrakash R, Lingam L. Why is women’s utilization of a publicly funded health insurance low?: a qualitative study in Tamil Nadu, India. BMC Public Health. 2021;21(1):350.

Chomi EN, Mujinja PG, Enemark U, Hansen K, Kiwara AD. Health care seeking behaviour and utilisation in a multiple health insurance system: does insurance affiliation matter? Int J Equity Health. 2014;13(1):25.

Al-Hanawi MK, Mwale ML, Kamninga TM. The effects of health insurance on health-seeking behaviour: evidence from the Kingdom of Saudi Arabia. Risk Manag Healthc Policy. 2020;13:595–607.

Sood N, Wagner Z. Impact of health insurance for tertiary care on postoperative outcomes and seeking care for symptoms: quasi-experimental evidence from Karnataka, India. BMJ Open. 2016;6(1):e010512.

Reshmi B, Unnikrishnan B, Rajwar E, Parsekar SS, Vijayamma R, Venkatesh BT. Impact of public-funded health insurances in India on health care utilisation and financial risk protection: a systematic review. BMJ Open. 2021;11(12):e050077.

Singh V, Garg A. Income inequity in the utilisation of inpatient services : Effects of publicly financed health insurance schemes. 2022. [cited 2023 Sept 16]. Available from: https://www.epw.in/journal/2022/28/special-articles/income-inequity-utilisation-%C2%A0inpatient-services.html.

Jana A, Basu R. Examining the changing health care seeking behavior in the era of health sector reforms in India: evidences from the National Sample Surveys 2004 & 2014. Glob Health Res Policy. 2017;2:6.

Erlangga D, Suhrcke M, Ali S, Bloor K. The impact of public health insurance on health care utilisation, financial protection and health status in low- and middle-income countries: a systematic review. PLoS One. 2019;14(8):e0219731.

van Hees SGM, O’Fallon T, Hofker M, Dekker M, Polack S, Banks LM, et al. Leaving no one behind? Social inclusion of health insurance in low- and middle-income countries: a systematic review. Int J Equity Health. 2019;18(1):134.

Thuong NTT, Huy TQ, Tai DA, Kien TN. Impact of health insurance on health care utilisation and out-of-pocket health expenditure in Vietnam. BioMed Res Int. 2020;2020:e9065287.

Tungu M, Amani PJ, Hurtig AK, Dennis Kiwara A, Mwangu M, Lindholm L, et al. Does health insurance contribute to improved utilization of health care services for the elderly in rural Tanzania? A cross-sectional study. Glob Health Action. 2020;13(1):1841962.

Joseph J, Sankar DH, Nambiar D. Empanelment of health care facilities under Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (AB PM-JAY) in India. PLoS One. 2021;16(5):e0251814.

Nandi S, Schneider H, Garg S. Assessing geographical inequity in availability of hospital services under the state-funded universal health insurance scheme in Chhattisgarh state, India, using a composite vulnerability index. Glob Health Action. 2018;11(1):1541220.

National Health Accounts Technical Secretariat, National Health Systems Resource Centre, Ministry of Health and Family Welfare, Government of India. National Health Accounts Estimates for India, 2018–19 [Internet]. 2022. Available from: https://nhsrcindia.org/sites/default/files/2022-09/NHA%202018-19_07-09-2022_revised_0.pdf. [cited 2023 Mar 28].

Al-Hanawi MK, Mwale ML, Qattan AMN. Health insurance and out-of-pocket expenditure on health and medicine: heterogeneities along income. Front Pharmacol [Internet]. 2021;12. Available from:https://doi.org/10.3389/fphar.2021.638035. [cited 2022 Sep 2].

Muraleedharan M, Chandak AO. Emerging challenges in the health systems of Kerala, India: qualitative analysis of literature reviews. J Health Res. 2021;36(2):242–54.

Nandi S, Schneider H, Dixit P. Hospital utilization and out of pocket expenditure in public and private sectors under the universal government health insurance scheme in Chhattisgarh State, India: Lessons for universal health coverage. PLoS One. 2017;12(11):e0187904.

Sriram S, Khan MM. Effect of health insurance program for the poor on out-of-pocket inpatient care cost in India: evidence from a nationally representative cross-sectional survey. BMC Health Serv Res. 2020;20(1):839.

George MS, Davey R, Mohanty I, Upton P. “Everything is provided free, but they are still hesitant to access healthcare services”: why does the indigenous community in Attapadi, Kerala continue to experience poor access to healthcare? Int J Equity Health. 2020;19(1):105.

Scheduled Tribes Development Department. Healthcare Schemes [Internet]. 2023. Available from: https://www.stdd.kerala.gov.in/healthcare-schemes. [cited 2023 Mar 28].

Reporter S. Survey to identify 5 lakh poorest families in Kerala. The Hindu [Internet]. 2021. Available from: https://www.thehindu.com/news/national/kerala/survey-to-identify-5-lakh-poorest-families-in-kerala/article34744783.ece. [cited 2023 Apr 19].

Acknowledgements

We are grateful to Ms. Jyotsna Negi, who supported us with the initial analysis for this study. We acknowledge our research colleagues at the George Institute for Global Health, India for their valuable comments and suggestions.

Notes

⦁ Survey weights were used to cater for different selection probabilities in different blocks of the survey and to adjust for household non-response and individual non-response. Survey weights were calculated based on sampling probabilities separately for each sampling stage. The final sampling weights were normalized to give a total number of weighted cases that equals the total number of unweighted cases. Normalization was done by multiplying the sampling weight by the estimated total sampling fraction obtained from the survey for household weights and individual weights.

⦁ For caste and religion groups, we carried out a separate analysis by grouping ‘general’ caste category with prefer not to say/don’t know as well as by grouping ‘other religious group’ with prefer not to say/don’t know. In all analyses, results were similar to those presented here.

Funding

We wish to indicate that this work was supported by the Wellcome Trust/DBT India Alliance Fellowship (https://www.indiaalliance.org) Grant number IA/CPHI/16/1/502653) awarded to Dr. Devaki Nambiar. The funder had no role in study design, data collection and analysis, decision to publish, or preparation of the manuscript. The funder provided support in the form of salaries and research materials and field work support for authors DN, HS, JN and JJ but did not have any additional role in the study design, data collection and analysis, decision to publish, or preparation of the manuscript. The specific roles of these authors are articulated in the ‘author contributions’ section.

Author information

Authors and Affiliations

Contributions

Conceptualization: Jaison Joseph. Methodology: Jaison Joseph, Santosh Kumar Sharma, Hari Sankar D, Devaki Nambiar. Formal analysis and investigation: Santosh Kumar Sharma. Writing—original draft preparation: Jaison Joseph, Hari Sankar D, Santosh Kumar Sharma. Writing—review and editing: Jaison Joseph, Hari Sankar D, Santosh Kumar Sharma, Devaki Nambiar. Funding acquisition: Devaki Nambiar. Supervision: Devaki Nambiar.

Corresponding author

Ethics declarations

Ethics approval and consent to participate

Ethics approval of the study was received from the institutional ethics committee of George Institute for Global Health (Project Number 05/2019). All participants gave written informed consent before taking part in the study including Illiterate participants in the survey who were read out and explained the consent form in the local language. Thereafter, they were able to sign their names. The ethics committee that approved the study also approved this procedure of obtaining written informed consent from these participants. All methods were carried out in accordance with relevant guidelines and regulations.

Consent for publication

Not applicable.

Competing interests

The authors declare no competing interests.

Additional information

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/. The Creative Commons Public Domain Dedication waiver (http://creativecommons.org/publicdomain/zero/1.0/) applies to the data made available in this article, unless otherwise stated in a credit line to the data.

About this article

Cite this article

Sharma, S.K., Joseph, J., D, H.S. et al. Assessing inequalities in publicly funded health insurance scheme coverage and out-of-pocket expenditure for hospitalization: findings from a household survey in Kerala. Int J Equity Health 22, 197 (2023). https://doi.org/10.1186/s12939-023-02005-2

Received:

Accepted:

Published:

DOI: https://doi.org/10.1186/s12939-023-02005-2