Abstract

Background

One of the key functions and ultimate goals of health systems is to provide financial protection for individuals when using health services. This study sought to evaluate the level of financial protection and its inequality among individuals covered by the Social Security Organization (SSO) health insurance between September and December 2023 in Iran.

Methods

We collected data on 1691 households in five provinces using multistage sampling to examine the prevalence of catastrophic healthcare expenditure (CHE) at four different thresholds (10%, 20%, 30%, and 40%) of the household’s capacity to pay (CTP). Additionally, we explored the prevalence of impoverishment due to health costs and assessed socioeconomic-related inequality in OOP payments for healthcare using the concentration index and concentration curve. To measure equity in out-of-pocket (OOP) payments for healthcare, we utilized the Kakwani progressivity index (KPI). Furthermore, we employed multiple logistic regression to identify the main factors contributing to households experiencing CHE.

Findings

: The study revealed that households in our sample allocated approximately 11% of their budgets to healthcare services. The prevalence of CHE at the thresholds of 10%, 20%, 30%, and 40% was found to be 47.1%, 30.1%, 20.1%, and 15.7%, respectively. Additionally, we observed that about 7.9% of the households experienced impoverishment due to health costs. Multiple logistic regression analysis indicated that the age of the head of the household, place of residence, socioeconomic status, utilization of dental services, utilization of medicine, and province of residence were the main factors influencing CHE. Furthermore, the study demonstrated that while wealthy households spend more money on healthcare, poorer households spend a larger proportion of their total income to healthcare costs. The KPI showed that households with lower total expenditures had higher OOP payments relative to their CTP.

Conclusion

The study findings underscore the need for targeted interventions to improve financial protection in healthcare and mitigate inequalities among individuals covered by SSO. It is recommended that these interventions prioritize the expansion of coverage for dental services and medication expenses, particularly for lower socioeconomic status household.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

One of the main objectives of health systems is to protect individuals from the financial hardships associated with healthcare expenses and prevent impoverishment due to health spending. However, studies show that this is not the case in many lower and middle income countries [1,2,3]. The World Bank’s (WB) “Voices of the Poor” report covering 50 countries revealed that poor health and illness due to the costs of receiving health services and income loss due to illness are among the main contributors to poverty [4]. Consequently, the World Health Organization (WHO) has emphasized financial protection as a key health system goal [5]. Regarding the importance of financial protection for individuals, the Universal Health Coverage (UHC), as outlined in Sustainable Development Goal (SDG) Target 3.8, aims to ensure people can access healthcare without experiencing financial hardship. This target is measured through two key indicators: 3.8.1, which focuses on the coverage of essential health services, and 3.8.2, which tracks the proportion of a country’s population experiencing catastrophic health spending [6]. Out-of-pocket (OOP) payments for healthcare can be catastrophic for households, especially the poor [7].

There are various approaches that can be used to measure the degree of financial protection in a health system. The WHO defines catastrophic healthcare expenditure (CHE) when a household spends on health services 40% or more of the household’s capacity to pay (CTP) [8]. The WB defines CHE if a household spends 10% or more of household income on health. Studies often use both methods, but the WHO’s approach is more commonly used [9,10,11]. Around the world, every year, over 150 million people face financial hardship due to OOP payment for healthcare, and about 100 million are pushed below the poverty line [12].

In Iran, the target of reducing the percentage of households facing CHEs to below 1% in the Economic, Social and Cultural Development Plans has not been achieved. As studies conducted in different parts of the country show, the percentage of households facing catastrophic health expenditures has been reported to be 8.3 to 15.3% [13,14,15,16,17]. This figure was 67.9% among households with a member suffering from cancer [18]. One of the main factors influencing the effectiveness of a health system in protecting citizens against health costs lies in the methods of collecting and financing health expenditures. Different countries use various approaches for healthcare financing. There are five main methods, including: (1) taxation, (2) social health insurance, (3) private health private insurance, (4) OOP payments, and (5) development assistant for health (DAH) [19]. Based on data from the WHO’s National Health Accounts for 2021, Iran allocated 6% of its GDP towards health spending. The WHO report shows that the primary sources for financing health expenditures in Iran were 55.2% from government budgets and basic health insurance plans, and 34.5% from OOP payments [20]. The OOP payments for healthcare as the second source of healthcare financing have two negative consequences. First, direct OOP payments at the time of receiving healthcare can lead to CHE for households. Second, OOP payments may exhibit regressivity, implying an unfair distribution of costs [2, 21]. This regressivity adversely affects equity in healthcare financing, measured by the Kakwani progressivity index (KPI). The KPI assesses whether OOP payments increase or decrease with income. If OOP payments increase as income rises, it indicates progressive OOP payments. If OOP costs increase as income decreases, it signals regressive OOP payments [22]. One study in Iran reported progressive OOP payments for urban residents based on a positive KPI, but regressive OOP payments for rural residents with a negative KPI [23]. Another study found a negative KPI for OOP for healthcare costs from 1991 to 2017 in Iran [24].

The Social Security Organization (SSO) in Iran provides health services to insured clients through two main ways, direct and indirect sectors. The SSO provides health insurance to over 44 million people, including formal sector employees and a large number of self-employed workers. The direct sector includes hospitals and clinics owned by the SSO that provide free treatment and medicines to patients. However, high demand leads to long wait times. In the indirect sector, the SSO has contracts with hospitals/medical centers affiliated with medical universities, private hospitals, labs, physicians’ offices, etc. to provide care to insured patients. Patients can pay fees to these providers. Financing for the SSO comes from insurance premiums paid by insured members and employers. The government also provides subsidies to the organization [25,26,27].

In the past five years, Iranian households have faced significant financial burden due to sanctions and high inflation. The average inflation rate has exceeded 30% over the past four years, while the annual increase in salaries and wages has been less than 20% [28]. Therefore, it is necessary to re-examine the level of financial protection against health costs and equity in health expenditures in order to design interventions tailored to the new conditions. To date, no published studies have assessed the extent of financial protection against CHE and its socioeconomic-related inequality among individuals insured through the SSO health insurance in Iran. To address this gap in the literature, we attempt to answer the following questions: What is the current status of financial protection for households covered by SSO health insurance in terms of CHE and impoverishment? Which socioeconomic group experiences the highest concentration of total health spending and CHE? And finally, is OOP payment for healthcare among SSO clients a regressive or progressive method? This information can help identify gaps in coverage and accessibility of healthcare for a large segment of the population. Assessing financial protection can guide policy recommendations to improve health insurance programs and ensure more equitable access to care.

Method and materials

Study setting, sample size, sampling method, and data collection tool

This study was conducted in Iran, a lower-middle income country, between September and December in 2023 [29]. At the time of the study, Iran comprises 32 provinces and has a population of approximately 89 million people. The study population consisted of all individuals covered by SSO health insurance in Iran. In 2022, the SSO provided health insurance to around 45 million Iranians, representing over 50% of the country’s population.

In this study, 1888 people insured by the SSO health insurance initially completed the questionnaire. After excluding incomplete questionnaires (shown in Figs. 1), 1691 respondents were included in the final analysis. The sampling process consisted of the following steps. First, Iran was divided into five regions (north, west, south, east, and center), and one province from each region was randomly selected. Then, within each selected province, four SSO agencies were randomly chosen based on geographical area to participate in the study. If a province had fewer than four SSO agencies, all agencies were included. Finally, in each province, one or two trained interviewers (public health bachelor students) conducted face-to-face interviews with SSO insured individuals visiting the selected agencies. Samples were included in the study in each agency through the convenience sampling method. The interviewers administered the questionnaire to complete the data collection. The five provinces included in the study were Tehran, Kermanshah, Yazd, Sistan-Baluchistan, and Golestan provinces.

Flow chart of final samples included in the analysis

To collect data, we used the WHO questionnaire adjusted based on the study objectives was used. This questionnaire includes three sections and its validity and reliability have been confirmed in the context of Iran [30]. The first part includes sociodemographic information on households covering the age, sex, and education level of the household head, household size, supplementary health insurance status, presence of members under 5 or over 65 years old, members with chronic diseases, living area, and household assets. The second part includes data on the utilization of outpatient and inpatient health services by household members in the past month and past year, respectively. Finally, the third part covers monthly household expenditures by type such as food, health, education, etc. A one-month recall period was used for total household expenditures and outpatient service utilization. A 12-month recall period was also used for inpatient service utilization. To estimate CHE, all cost variables were converted monthly.

Data analysis

Wealth index of household

Similar to previous studies [31, 32], a wealth index was used as a proxy for the socioeconomic status (SES) of households. A wealth score for each household was constructed using principal component analysis (PCA) [33] based on variables including the number of rooms per capita, type of house ownership, house size (in square meters), car ownership, and ownership of other goods (such as color TV, Internet, computers/laptops, cell phones, freezers, dishwashers, microwaves, vacuum cleaners, motorcycles, bicycles and heating/cooling systems. Additionally, two questions were posed about household trips within and outside the country in the past year. Finally, based on the wealth scores derived from the PCA, all households were categorized into five SES groups, ranging from the poorest (first SES quintile) to the wealthiest (fifth SES quintile).

Catastrophic healthcare expenditure (CHE)

To estimate the prevalence of CHE among insured individuals, the 40% threshold of non-food household spending was used according to WHO’s approach [8]. Based on this approach, if a household spends 40% or more of their non-food household capacity-to-pay (CTP) for health services, they have experienced CHE. It should be noted that some studies have used other thresholds when defining CHE, therefore thresholds of 30%, 20%, and 10% of household non-food spending capacity were also used to estimate the prevalence of CHE.

The following four steps were used to calculate CHE. First, to determine a household’s CTP, we subtracted food expenditure (considered subsistence spending) from the total monthly household expenditure. The remaining non-food expenditure was considered the CTP. We adjusted this value for household size using the following formula:

Where Eqhsizeh is the equalized household’s size, and β is set to 0.56 [8]. Second, we used the household’s share of food expenditure of total household expenditure to construct the poverty line (PL) as follows:

Here, Eqfoodh is the share of spending on food relative to the total household expenditure; Wh is the sampling weight of the households; foodh is the household’s food expenditure; and food45 – food55 is the mean food expenditure for sampled households spending 45–55% of their total expenditure on food. Third, the subsistence expenditure for each household was calculated using the following formula:

If subsistence expenditure was greater than the food expenditure for the household, we calculated the CTP of the household as follows:

If food expenditure was equal to or greater than subsistence expenditure for household h, we calculated the CTP as follows:

Fourth, to determine if a household experienced CHE, the following formula was used:

Where OOPHh shows OOP payment for healthcare for household h. If the OOP health payments were greater than or equal to 40% of the household CPT, the household was considered to be facing CHE. By inputting 0.3 into the formula, we can determine the prevalence of CHE at the 30% household capacity to pay threshold.

To identify factors associated with CHE among households insured by the SSO using the 40% threshold, and given that the outcome variable is binary (0 for households not facing CHE and 1 for households facing CHE), a multiple logistic regression model was employed. The explanatory variables entered into the logistic regression model included the head of household’s gender, age, education level, household economic status, health service utilization (outpatient, dental, inpatient and drug use), supplementary health insurance status, presence of members over 65 years and under 5 years in the household, members with chronic disease, and study area (supplementary 1).

Impoverishment

OOP payments for health care can be impoverishing if a household’s expenditure level is above the poverty line before paying for healthcare (pre-payment), but falls below the PL after paying for healthcare (post-payment) [34]. We used the following criteria to identify households that were impoverished due to OOP health spending [35]:

where \(\:{texp}_{\text{h}}\) is the total expenditure of household, \(\:{\text{s}\text{e}}_{\text{h}}\) shows the subsistence expenditure of household; \(\:{OOPH}_{h}\) is OOP payment for healthcare of household. Households are considered to have been pushed below the poverty line due to health expenditures when the difference between OOP payment for healthcare and total household expenditure is less than the household’s subsistence expenditures. In other words, by subtracting OOP payment for health from the total household expenditure, if the resulting amount is lower than the household’s subsistence expenditures, it indicates that the household has fallen below the poverty line.

Progressivity in OOP payment for healthcare

Similar to previous studies [22, 24], we measured equity in OOP payments for health care across households insured by the SSO using the Kakwani progressivity index (KPI). The KPI was calculated by the following formula [22, 23]:

Where Coop is the concentration index for OOP payments for healthcare and Gctp shows Gini coefficient for household CTP.

The concentration index (C) ranges from − 1 to + 1, Where a negative value indicates OOP payments are concentrated among poorer households, and a positive value indicates concentration among wealthier households. A value of 0 represents perfect equality. The Gini coefficient (G) ranges from 0 to 1, with higher values indicating greater CTP inequality. The KPI itself ranges from − 2 to 1, where a negative value indicates regressivity (an inverse relationship between OOP payments and household CTP), a positive value indicates progressivity (a direct relationship between OOP payments and CTP), and a value of 0 indicates proportionality.

Socioeconomic-related inequality in CHE and OOP payments for healthcare

We examined socioeconomic inequality in experiencing CHE and OOP payments for healthcare among households included in the study using the concentration curve and the concentration index (C) [32, 36]. The concentration curve plots the cumulative percentage of the samples ranked by a wealth score on the x-axis against the cumulative percentage of those experiencing CHE or OOP payments for healthcare on the y-axis. If the curve lies above (below) the line of equality, CHE or OOP payment for healthcare are more concentrated among poorer (wealthier) households. The C quantifies the degree of socioeconomic inequality. It is calculated as twice the area between the concentration curve and the equality line. C ranges from − 1 to 1, where a negative (positive) value means CHE or OOP payments for healthcare are more concentrated among the poor (rich). Since CHE is a binary variable, C was normalized by multiplying it by 1/(1-µ) as suggested by Wagstaff to account for the bounds [37].

Results

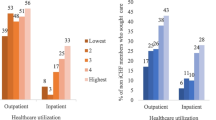

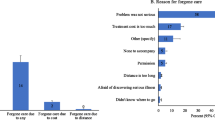

A total of 1691 households from five provinces of the country were included in the study. The results showed that the mean age of the household head was 44.5 years with a standard deviation of 15.2 years. Approximately 85.2% of household heads were male and the rest were female. 92.4% of households lived in urban areas and 7.6% lived in rural areas. About 16% of households had at least 1 member over 65 years old and approximately 41% of households had at least one member with a chronic disease such as hypertension, diabetes, etc. The descriptive characteristics of the studied households based on facing CHE are presented in Table 1. The mean monthly total health expenditure of households and mean food expenditure of households were 12,815,670 (50.8 LCU per US$) and 47,298,640 (187.4 LCU per US$) Iranian Rial (IRR), respectively; meaning that households insured by the SSO spend about 11% of their costs on health. The study results showed that at the 40% threshold, 15.7% (95% CI: 14.5–17.5%) of the studied households experienced CHE. The prevalence of CHE at the 10%, 20% and 30%, thresholds was 47.1%, 30.1%, and 20.1%, respectively. The results showed that the prevalence of CHE was higher for female-headed households compared to male-headed households (16.7% vs. 15.5%). The prevalence of CHE was around 14.3% among households with supplementary health insurance, while it was 17.1% among households without supplementary coverage. Households with members above 65 years old had a prevalence of 23.5%, and those with at least one member with chronic disease had a prevalence of 20.7%. The results showed that before accounting for health expenditures, 12.5% of the participant’s households were below the PL. After incorporating health spending, this figure increased to 20.4%; meaning that around 7.9% of the samples were impoverished due to health expenditures.

The results for the most important factors affecting CHE based on multiple logistic regression are shown in Table 2. As indicated in the table, the head of household’s age, place of residence, household economic status, use of dental services, use of medicine (any type of medicines without their cost), and province of residence were among the most important factors influencing CHE among the studied households. For example, regarding the use of dental services, the results showed that the likelihood of experiencing CHEs was about 65% higher among households that used dental services compared to those that did not use such services in the past month. Our study also revealed that the adjusted odds ratio (AOR) for the wealthiest households is less than 1, specifically 0.56, indicating a negative correlation between the household wealth index and the likelihood of facing CHE. This means that the odds of experiencing CHE are 56% lower for the wealthiest households compared to the poorest households.

Based on socioeconomic status, the poorest households had a prevalence of 21.4%, while prevalence of CHE among the richest households was 15.4%. The results on socioeconomic inequality in health expenditures and CHE among the households included in the study are shown in Table 3 (concentration index) and Fig. 2 (concentration curve). As indicated in Table 3, health expenditures were concentrated among households with higher socioeconomic status (positive sign of CI). In other words, individuals with higher economic status spend more on health services compared to households with lower economic status (12.3% vs. 10.7% of total household costs). Regarding facing CHE, the results also showed that CHE is more concentrated among households with lower socioeconomic status. The concentration curve for CHE lies above the line of equality (Fig. 2A), indicating that CHE is concentrated among poorer households. In contrast, the concentration curve for household health costs lies below the equality line (Fig. 2B), showing that health spending is concentrated among wealthier households.

The concentration curve for CHE (A) and household health cost (B) among households included in the study

The KPI for OOP health payments among households insured by the SSO was negative and equal to -0.2874. This indicates that OOP health payments were regressive, meaning payments were not proportional to households’ CTP. There was an inverse relationship between OOP payments and total household expenditures- households with lower total expenditures had higher OOP payments relative to their CTP.

Discussion

This study sought to assess the financial protection provided against CHE for individuals covered by the SSO health insurance program in Iran in 2023. In addition, we evaluated inequalities in exposure to CHE across different groups covered by SSO health insurance. Our study showed that insured households spend about 11% of their total expenditure on health care. At the 40% CTP threshold, approximately 16% of studied households faced CHE, and around 7.9% of them were impoverished due to health costs. Various studies have examined the prevalence of CHE among households and different socioeconomic groups in Iran, yielding highly heterogeneous findings for several reasons. For instance, Shojaei et al. [38] conducted a study among hospitalized patients in a hospital in Mashhad, finding the prevalence of CHE to be 81% before and 67% after the implementation of the health transformation plan. Another study focused on marginalized households in Tehran, revealing that the prevalence of CHE in 2015 was 30%, compared to 13% and 12% in 2003 and 2008 [17]. A study on COVID-19 patients in Semnan reported a 61% incidence of CHE [39]. Asafzadeh et al. found that 24% of the studied households in Qazvin faced CHE [40]. Ghodousi-Nejad et al. [41] observed a 24% incidence of CHE in their studied households. Heidarzadeh et al. [42] concluded that 29% of studied households faced CHE. Rezaei et al. [43] discovered that households in 2017 spent around 10% of their budget on health, with catastrophic spending prevalence of 25.5%, 9.10% and 16.22% at the 40%, 30% and 20% thresholds, respectively. Fakhrezad et al. [44] found that around 9% of households in Hamedan faced catastrophic costs. Hedayati et al. [45] in a review of 112 studies, reported a prevalence of 2.3% of CHE in Iran. There are many reasons for the heterogeneity between studies, including differences in the study population. Other key factors are sample size, survey instruments, CHE’s threshold, and study year. Studies conducted in recent years and the current study have generally reported a higher prevalence of CHE. This could be attributed to two key factors. First, increased health service tariffs have led to higher OOP payments for healthcare. Second, sharply rising living costs for households due to currency variation and economic sanctions have reduced households’ capacity to pay. The average inflation rate in Iran from 2019 to 2022 was approximately 39.3% [28].

With regards to the main drivers of CHE, our study found the head of household’s age, place of residence, household economic status, use of dental services, use of medicine, and province of residence were the main determinants of CHE. A study conducted by Nooraei Motlagh et al. [46] in 2012 identified the use of dental and inpatient services to be the most important factors affecting CHE. Other contributing factors were having a member over 65 years old, having a low education, having a female household head, and lacking insurance coverage. Rezapour et al. [47] demonstrated that age over 60, inpatient care use, and informal payments were key determinants of CHE. Another study identified rural residence, income, the number of employed members, and marital status as the main factors [44]. Shokri et al. [48] investigation involving 2000 households in five provinces of Iran, found that about 9% faced CHE, with the main factors being female head, inpatient care use, dental care, a disabled member, and economic status. Piroozi et al. [49] found older age, female gender, marital status, socioeconomic status, residence, and inpatient care use as the main determinants of CHE among households with type 2 diabetes. Our study, along with previous research, indicates that increased use of inpatient and dental services leads to a significant rise in CHE. We observed that the likelihood of catastrophic spending was about 65% higher among households using dental services versus those not using them. Dental care is among the most expensive services in Iran and is not fully covered by insurers, making it a key driver of catastrophic costs. This signifies that policymakers should enhance coverage of these services and determine which aspects should be covered by basic and supplementary insurance to reduce catastrophic spending.

Our study found inequality in health expenditures and exposure to CHE across income groups. Specifically, our study indicated that there was pro-rich inequality in health spending- wealthier households spent more on healthcare than poorer households in absolute terms. However, inequality in facing CHE was pro-poor- poorer households were more likely to incur CHE compared to wealthier households. The KPI for OOP payments for healthcare financing was also negative, indicating regressivity, where the poor contributed a higher fraction of their CTP. In a study published in 2020, Rezaei and Hajizadeh [32] demonstrated a high prevalence of CHE among households with lower economic status (the concentration index was found to be -0.17). A study in China, analyzing 3,217 households in 2008 and 13,085 households in 2013, indicated a greater concentration of CHE among the poor [50]. Furthermore, a study conducted among households in Hamedan province, Iran, revealed a concentration index of -0.163 for CHE, indicating that poorer households are more vulnerable to these expenses [51]. The findings of other studies conducted in Iran and other countries regarding equity in healthcare financing through OOP payments align with the result of our study. A study by Rezaei et al. [24] demonstrated that the KPIs for 5 years from 1991 to 2017 for OOP payments were consistently negative, indicating a regressive nature of OOP payments for healthcare services, with a greater burden falling on socially and economically disadvantaged households. In another study conducted in Iran, the authors concluded that direct household payments for government healthcare services are inequitable based on household income variables [52]. Yara Ahmed and et al. found the Egyptian health care system to be regressive, with an overall Kakwani index of -0.079 [53]. Studies across countries, regardless of their economic conditions, have shown that OOP payments for health services represent a regressive health financing mechanism. One study calculated a regressive Kakwani index for OOP spending on healthcare services in Canada, indicating these payments are a regressive financing mechanism [22].

The study highlights two important points as follows: The results from this study and other studies conducted in Iran and other countries have shown that governments and insurance organizations such as the SSO should not rely on OOP payments for health services as an efficient and equitable method. Instead, they should try to move towards health financing models that pool funds and spread financial risk across the population rather than relying solely on out-of-pocket payments by individuals at the point of care. This would better protect patients and insurees from health costs and prevent household impoverishment and bankruptcy due to health expenditures. Second point is that inpatient and outpatient services do not play a significant role in CHE among SSO insurees. This is unlike studies done in the country with other insurance organizations, which show the level and depth of coverage for inpatient and outpatient services in the SSO is at an appropriate level. Insured patients of the SSO mainly use the organization’s own healthcare facilities. At these facilities, patients pay little or no fees for services. As a result, SSO insurees have good financial protection for these healthcare services.

Study limitations

There are certain limitations to be taken into account when interpreting the findings of this study. Firstly, the study design was cross-sectional, which means we cannot establish a cause-and-effect relationship between experiencing CHE and its determinants. Additionally, in this study, information was obtained through self-reporting from individuals, which introduces the possibility of recall bias regarding household expenses, healthcare costs, and the types of health services utilized. However, we made efforts to mitigate this bias by minimizing the recall period (30 days for reported data). Last limitation of this study is that it only included households covered by the SSO health insurance. By focusing solely on insured households, we were unable to evaluate the unmet needs and financial hardship related to healthcare costs among uninsured households. Future studies should include both insured and uninsured households to provide a more comprehensive assessment of financial protection across the whole population.

Conclusion

Our study showed that insured households by the SSO spend more than 10% of their household expenses on healthcare, with the majority of the expenditure allocated to dental services and medicines. Additionally, approximately 15% of the households studied experience CHE. Factors such as dental service utilization, drug service utilization, age of the household head, and household socioeconomic status were found to be significant determinants of the prevalence of CHE. Furthermore, CHEs were observed to be more concentrated among households with lower socioeconomic status, and the use of a direct payment method for financing healthcare costs based on household payment capacity was not equitable. Therefore, it is recommended that the organization take steps toward increasing financial protection for households under social insurance by mobilizing new financial resources, reducing costs, or increasing insurance coverage to expand access to dental and pharmaceutical services. Undoubtedly, expanding insurance coverage for these two types of services will lead to a significant reduction in OOP payments and, consequently, a decline in the prevalence of catastrophic and impoverishing health expenditures.

Data availability

“The datasets generated and analyzed during the current study are available from the corresponding author upon reasonable request”.

References

Saksena P, Hsu J, Evans DB. Financial risk protection and universal health coverage: evidence and measurement challenges. PLoS Med. 2014;11(9):e1001701.

Wagstaff A. Measuring financial protection in health. World Bank; 2008.

Waters HR, Anderson GF, Mays J. Measuring financial protection in health in the United States. Health Policy. 2004;69(3):339–49.

Narayan D. Voices of the poor: can anyone hear us? World Bank; 2000.

Murray CJ, Frenk J. A framework for assessing the performance of health systems. Bull World Health Organ. 2000;78:717–31.

Organization WH. Tracking universal health coverage: 2023 global monitoring report. World Health Organization; 2023.

Organization WH. Health Systems; Universal health coverage. World Health Organization: Geneva, Switzerland.; 2019.

Xu K, Evans DB, Kawabata K, Zeramdini R, Klavus J, Murray CJ. Household catastrophic health expenditure: a multicountry analysis. Lancet. 2003;362(9378):111–7.

Kronenberg C, Barros PP. Catastrophic healthcare expenditure–drivers and protection: the Portuguese case. Health Policy. 2014;115(1):44–51.

Proaño Falconi D, Bernabé E. Determinants of catastrophic healthcare expenditure in Peru. Int J Health Econ Manage. 2018;18:425–36.

Ravangard R, Jalali FS, Bayati M, Palmer AJ, Jafari A, Bastani P. Household catastrophic health expenditure and its effective factors: a case of Iran. Cost Eff Resource Allocation. 2021;19(1):59.

Xu K, Evans DB, Carrin G, Aguilar-Rivera AM, Musgrove P, Evans T. Protecting households from catastrophic health spending. Health Aff. 2007;26(4):972–83.

Soofi M, Rashidian A, Aabolhasani F, Sari AA, Bazyar M. Measuring the Exposure of Households to Catastrophic Healthcare Expenditures in Iran in 2001: the World Health Organization and the World Bank’s Approach. Hosp J. 2013;12(2).

Ghiasvand H, Gorji HA, Maleki M, Hadian M. Catastrophic health expenditure among Iranian rural and urban households, 2013–2014. Iran Red Crescent Med J. 2015;17(9).

Moradi G, Bolbanabad AM, Abdullah FZ, Safari H, Rezaei S, Aghaei A, et al. Catastrophic health expenditures for children with disabilities in Iran: a national survey. Int J Health Plann Manag. 2021;36(5):1861–73.

Kavosi Z, Rashidian A, Pourmalek F, Majdzadeh R, Pourreza A, Mohammad K, et al. Measuring household exposure to catastrophic health care expenditures: a longitudinal study in Zone 17 of Tehran. Hakim J. 2009;12(2):38–47.

Kazemi-Galougahi MH, Dadgar E, Kavosi Z, Majdzadeh R. Increase of catastrophic health expenditure while it does not have socio-economic anymore; finding from a district on Tehran after recent extensive health sector reform. BMC Health Serv Res. 2019;19(1):1–12.

Kavosi Z, Delavari H, Keshtkaran A, Setoudehzadeh F. Catastrophic health expenditures and coping strategies in households with cancer patients in Shiraz Namazi hospital. 2014.

Dieleman J, Campbell M, Chapin A, Eldrenkamp E, Fan VY, Haakenstad A, et al. Evolution and patterns of global health financing 1995–2014: development assistance for health, and government, prepaid private, and out-of-pocket health spending in 184 countries. Lancet. 2017;389(10083):1981–2004.

World-Health-Organization. Global Health Expenditure Database 2024. https://apps.who.int/nha/database/country_profile/Index/en

Fakhri M, Juni MH, Rosliza A. Assesing progressivity of out-of-pocket expenditures for Healthcare: evidence from households in Malaysia. Int J Public Health Clin Sci (IJPHCS). 2019.

Edmonds S, Hajizadeh M. Assessing progressivity and catastrophic effect of out-of-pocket payments for healthcare in Canada: 2010–2015. Eur J Health Econ. 2019;20:1001–11.

Almasiankia A, Kavosi Z, Keshtkaran A, Jafari A, Goodarzi S. Equity in health care financing among Iranian households. Shiraz E-Medical J. 2015;16:11–2.

Rezaei S, Woldemichael A, Ebrahimi M, Ahmadi S. Trend and status of out-of-pocket payments for healthcare in Iran: equity and catastrophic effect. J Egypt Public Health Assoc. 2020;95(1):29.

https://landinfo.no/wp-content/uploads/2020/08/Report-Iran-Welfare-system-12082020.pdf

Doshmangir L, Bazyar M, Rashidian A, Gordeev VS. Iran health insurance system in transition: equity concerns and steps to achieve universal health coverage. Int J Equity Health. 2021;20(1):37.

Davari M, Haycox A, Walley T. The Iranian health insurance system; past experiences, present challenges and future strategies. Iran J Public Health. 2012;41(9):1.

https://blogs.worldbank.org/opendata/new-world-bank-country-classifications-income-level-2022-2023

Kavosi Z, Rashidian A, Pourreza A, Majdzadeh R, Pourmalek F, Hosseinpour AR, et al. Inequality in household catastrophic health care expenditure in a low-income society of Iran. Health Policy Plann. 2012;27(7):613–23.

Giang NH, Vinh NT, Phuong HT, Thang NT, Oanh TTM. Household financial burden associated with healthcare for older people in Viet Nam: a cross-sectional survey. Health Res Policy Syst. 2022;20(Suppl 1):112.

Rezaei S, Hajizadeh M. Measuring and decomposing socioeconomic inequality in catastrophic healthcare expenditures in Iran. J Prev Med Public Health. 2019;52(4):214.

Vyas S, Kumaranayake L. Constructing socio-economic status indices: how to use principal components analysis. Health Policy Plann. 2006;21(6):459–68.

Wagstaff A, Doorslaer E. Catastrophe and impoverishment in paying for health care: with applications to Vietnam 1993–1998. Health Econ. 2003;12(11):921–33.

Mehdizadeh P, Daniyali H, Meskarpour-Amiri M, Dopeykar N, Uzi H. Catastrophic and impoverishing health expenditures and it’s affecting factors among health staffs in Iran: a case study in Tehran. Med J Islam Repub Iran. 2019;33:120.

O’Donnell O, O’Neill S, Van Ourti T, Walsh B. CONINDEX: Stata module to perform estimation of concentration indices. 2022.

Wagstaff A. The concentration index of a binary outcome revisited. Health Econ. 2011;20(10):1155–60.

Shojaei S, Yousefi M, Ebrahimipour H, Valinejadi A, Tabesh H, Fazaeli S et al. Catastrophic health expenditures and impoverishment in the households receiving expensive interventions before and after health sector evolution plan in Iran: evidence from a big hospital. Koomesh. 2018;20(2).

Gheinali Z, Moshiri E, Tavani ME, Haghi M, Gharibi F. Catastrophic health expenditures in hospitalized patients with delta variant of COVID-19: a cross-sectional study. Health Promotion Perspect. 2023;13(1):68.

Asefzadeh S, Alijanzadeh M, Gholamalipour S, Farzaneh A. Households encountering with catastrophic health expenditures in Qazvin. Iran Health Inform Manage. 2013;10(1):146–53.

Ghoddoosinejad J, Jannati A, Gholipour K, Baghestan EB. Households encountering with catastrophic health expenditures in Ferdows, Iran. J Egypt Public Health Assoc. 2014;89(2):81–4.

Heidarzadeh A, Negari Namaghi R, Moravveji A, Farivar F, Naghshpour P, Roshan Fekr F et al. Out-of-pocket and catastrophic health expenditure in Iran. J Public Health. 2023:1–7.

Rezaei S, Hajizadeh M. Measuring and decomposing socioeconomic inequality in catastrophic healthcare expenditures in Iran. J Prev Med Public Health. 2019;52(4):214–23.

Fakhrzad M, Fazaeli AA, Hamidi Y. Determinants of Catastrophic Health expenditures: a study in Hamedan, Iran. J Health Sci Surveillance Syst. 2023;11(2):302–7.

Hedayati M, Masoudi Asl I, Maleki M, Fazaeli AA, Goharinezhad S. The variations in Catastrophic and Impoverishing Health expenditures, and its determinants in Iran: a scoping review. Med J Islam Repub Iran. 2023;37:44.

Nouraei Motlagh S, Rezapour A, Lotfi F, Adham D, Sarabi Asiabar A. Investigating adverse effects of health expenditures in households of deprived provinces. J Health. 2017;8(4):425–35.

Rezapour A, Ebadifard Azar A, Asadi S, Bagheri Faradonbeh S, Toofan F. Estimating the odd-ratio of factors affecting households’ exposure to catastrophic and impoverishing health expenditures. J Military Med. 2016;18(1):355–61.

Shokri A, Bolbanabad AM, Rezaei S, Moradi G, Piroozi B. Has Iran achieved the goal of reducing the prevalence of households faced with catastrophic health expenditure to 1%? A national survey. Health Sci Rep. 2023;6(4):e1199.

Piroozi B, Mohamadi-Bolbanabad A, Moradi G, Safari H, Ghafoori S, Zarezade Y et al. Incidence and intensity of catastrophic health-care expenditure for Type 2 diabetes mellitus care in iran: determinants and inequality. Diabetes, Metabolic Syndrome and Obesity. 2020:2865-76.

Xu Y, Gao J, Zhou Z, Xue Q, Yang J, Luo H, et al. Measurement and explanation of socioeconomic inequality in catastrophic health care expenditure: evidence from the rural areas of Shaanxi Province. BMC Health Serv Res. 2015;15:256.

Vahedi S, Rezapour A, Khiavi FF, Esmaeilzadeh F, Javan-Noughabi J, Almasiankia A, et al. Decomposition of socioeconomic inequality in catastrophic health expenditure: an evidence from Iran. Clin Epidemiol Global Health. 2020;8(2):437–41.

Kazemian M, Abolhallaj M, Nazari H. Assessment of equity in public health care financing in 2013. مجله باليني پرستاري و مامايي. 2017;6(1).

Ahmed Y, Ramadan R, Sakr MF. Equity of health-care financing: a progressivity analysis for Egypt. J Humanit Appl Social Sci. 2021;3(1):3–24.

Acknowledgements

We would like to express our sincere gratitude to the Social Security Research Institute for providing financial support for this research project.

Funding

This study was supported by a grant from the Social Security Research Institute (no: 2014012611). The funding organization played no role in the study design, data collection, analysis and interpretation of findings, or writing of the manuscript.

Author information

Authors and Affiliations

Contributions

S.R., M.K., and MA.MG., developed the idea and analyzed the data. S.R., E.B., N.B., A.B., M.P. and Sh.S., collected the data and drafted the initial report. H.B. critically reviewed the paper, offering comments on the first draft. H.B., E.B., E.B., and S.R. collaborated on implementing the revisions and producing the final edition of the manuscript. All authors read and approved the final draft of the paper.

Corresponding author

Ethics declarations

Ethics approval and consent to participate

The study protocol was approved by the Social Security Research Institute, which granted permission to access and utilize the data for this analysis (no. 2014012611). The research protocol was reviewed and approved by the Research Deputy of Kermanshah University of Medical Sciences, with the approval number IR.KUMS.REC.1403.238. Informed consent was obtained in written format from all study participants. For illiterate participants in this study, written informed consent forms were collected from their legal guardians. The consent form included detailed information about the nature and purpose of the study, the voluntary nature of participation, and the right to withdraw from the study at any time.

Consent for publication

Not applicable.

Competing interests

The authors declare no competing interests.

Additional information

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Electronic supplementary material

Below is the link to the electronic supplementary material.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License, which permits any non-commercial use, sharing, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if you modified the licensed material. You do not have permission under this licence to share adapted material derived from this article or parts of it. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by-nc-nd/4.0/.

About this article

Cite this article

Rezaei, S., Karimi, M., Soltani, S. et al. Household financial burden associated with out-of-pocket payments for healthcare in Iran: insights from a cross-sectional survey. BMC Health Serv Res 24, 1062 (2024). https://doi.org/10.1186/s12913-024-11477-z

Received:

Accepted:

Published:

DOI: https://doi.org/10.1186/s12913-024-11477-z