Abstract

Background

Out-of-pocket payments are the major significant barrier in achieving universal health coverage, particularly in developing countries' rural communities. In 2011, the Ethiopian government launched a pilot community-based health insurance (CBHI) scheme with the goal of increasing access to modern health care services and providing financial security to households in the informal sector and rural areas. The main objective of this study is to estimate willingness to pay (WTP) for CBHI scheme and factors that influence it among rural households in the South West Shoa Zone.

Methods

A household-level cross-sectional study was conducted to examine the WTP for the CBHI scheme and factors associated with it in rural communities of South West Shoa Zone. The study used a sample of 400 rural households. Systematic random sampling was employed during household selection, and double-bounded contingent valuation method was used to estimate WTP for the CBHI scheme.

Results

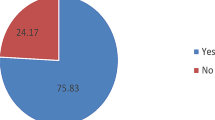

About 65 percent of the households are willing to pay for CBHI scheme. Moreover, the study found that the households were willing to pay 255.55 Birr per year on average. The result of the study also revealed that amount of bid, household income, family size, household head's education, household health status, membership to community-based health insurance scheme, membership in any association, and awareness about the scheme are factors that are significantly associated with WTP for the scheme.

Conclusions

Households are willing to pay a higher price than the policy price. Therefore, setting a new premium that reflects households' willingness to pay is highly valuable to policymakers. Social capital and awareness about CBHI scheme play an important role in influencing WTP. Thus, the study suggests that local communities need to strengthen their social cohesion and solidarity. It is also necessary to create awareness about the CBHI’s benefits.

Similar content being viewed by others

Introduction

Achieving good health and well-being is one of the essentials for achieving Sustainable Development Goals [1]. As a result, developing countries have increased their efforts to achieve universal health coverage [2, 3]. The universal health coverage is defined as “everyone, regardless of their ability to pay, should be able to get the services they need without financial hardship” [4].

Health insurance is one of the options for achieving universal health coverage. It is a legal arrangement that protects insured individuals against the costs of medical services covered by the health insurance plan. Health insurance works best when the risk pools are large and the healthy can subsidize the sick [5]. There are four types of health insurance, depending on financial sources and characteristics: national health insurance, social health insurance, private insurance, and community-based health insurance [5]. National health insurance is a sort of government-managed insurance that covers all citizens and is supported by general taxation. Mandatory earmarked payroll contributions are used to fund social health insurance, and contributions and specified medical benefits are directly linked. Private voluntary insurance is commercial insurance administered by private for-profit companies, with premiums based on the purchaser's risk rather than his or her ability to pay.

CBHI is a non-profit organization founded on the principles of social solidarity and designed to safeguard households in the informal urban sector and rural areas from the catastrophic effects of out of -pocket medical expenses [6,7,8,9]. The ultimate purpose of CBHI is to achieve health system goals such as improving health status, health equity, health system responsiveness, and fairness in financial contribution [10]. Simplicity, accessibility, self-management, and complementing the public effort are all typical characteristics of CBHI schemes [8].

The Ethiopian health care system suffers from high reliance on out-of- pocket payments [11]. In Ethiopia, the bulk of healthcare spending (i.e., about 53%) came from household out-of-pocket payments, and 40% was contributed by the federal and regional governments [12]. Out-of-pocket payment has catastrophic effects, especially for households who mainly engage in agriculture and informal economies, which are characterized by less job security, lower incomes and absence of access to a range of social benefits [13, 14]. In 2011, the Ethiopian government launched a pilot community-based health insurance (CBHI) scheme with the goal of increasing access to modern health care services and providing financial security to households in the informal sector and rural areas [15, 16]. CBHI scheme is the best policy instrument to finance health care which can mitigate catastrophic health care expenditure, and can improve access to health care services in rural communities of Ethiopia [17, 18]. However, developing CBHI scheme, from a policy perspective, is relevant only if there is willingness to pay (WTP) for it [19].

In Ethiopia, only few studies have been done on WTP for community-based health care prepayment scheme among rural households of Ethiopia [20,21,22]. The study by [20] tried to estimate how much a household is willing to pay for CBHI scheme. However, they employed linear regression equation model in the presence of significant fraction of the observations with zero value for the dependent variable (WTP). In this case, standard Ordinary Least Square technique results in biased and inconsistent parameter estimates [23]. Even though the study conducted by [21] employed better regression model (i.e., interval regression model) as compared to the former one, the hypothetical market scenario choice set developed by them lacks clarity, and the findings may not apply in different contexts. Therefore, this study aims to fill these gaps through estimating WTP for CBHI scheme and identifying factors that associated with it among rural households in the South West Shoa Zone.

Materials and methods

Description of the study area

South West Shoa zone is one of the central zones of Oromia region which is located at a longitude of 370 05’ to 38046’ from West to East and at a latitude of 8016’ to 9056’ from North to South. Like other zones of Oromia region, 90% of people of the zone live in rural areas, and they depend mainly on agriculture as their livelihood. Agriculture in the zone contributes enormous benefits to the people of the zone in particular and to the Ethiopian people in general. It is a source of food, source of income, raw-materials for agro-industries, and provides employment opportunity for rural households and their family members. The zone has abundant natural resources, especially watersheds and water resources. There are big rivers, streams, lakes and underground waters resulting in high potential irrigation in the zone. Even though it is traditional, irrigation is highly practiced in South West Shoa Zone.Footnote 1

Sample size and sampling technique

The target population of this study is rural households living in South West Shoa zone. This study covered all woredasFootnote 2 because the researchers expected too much variation in WTP among households. This study used a simplified formula provided by Yamane (1967) to determine the sample size at 95% confidence level and 5% degree of variability (Israel, 2012). In addition, 5% level of precision was used in order to get the sample size which represents a true population. The sample size determination formula provided by Yamane (1967) is as follows [24].

where \(\mathrm{n}\) is the sample size, \(\mathrm{N}\) is total number of farm households in South West Shoa Zone and

\(\mathrm{e}\)

is the level of precision. According to report obtained from South West Shoa Zone Bureau of Agriculture and Natural Resource, there are 151,315 farm households in South West Shoa Zone in 2017. This study assumed that the level of precision is 5%.

\(\mathrm{n}=\frac{\mathrm{151,315}}{1 +\mathrm{ 151,315}{(0.05)}^{2}}\cong\) 400 farm households.

We applied systematic random sampling during the household selection process. First, we decided the sampling interval by dividing the total households in the zone by determined sample size, which came to around 378. Next, we contacted kebeleFootnote 3 health extension workers to get a list of all households in each selected kebele. Finally, we employed systematic random sampling with the use of an interval 378 during household selection. Accordingly, one household was selected out of 378 households in each selected kebele, totaling 400 households.

Sources of data and method of data collection

This research relies heavily on primary data. A questionnaire was used to collect primary data from a sample of farm households. Heads of farm households were interviewed by trained enumerators. This study's questionnaire consists of two sections. The first section of the questionnaire asks about farm households' demographic and socioeconomic characteristics, as well as their perceptions and awareness about CBHI scheme. The second section of the questionnaire covers the CBHI scheme's contingent valuation scenario as well as different WTP questions.

In the study, the double-bounded dichotomous choice format of CVM was used to elicit households' WTP for the CBHI scheme. Before conducting survey, focus group discussion (FGD) was conducted to generate initial bids. Figure 1 shows the double-bounded bidding technique used to elicit respondents' WTP in the study area. Three levels of the initial bid (Birr 100, Birr 200, and Birr 300) were established. The level of follow up bid depends on the response to the initial bid. If the respondent accepts the proposed initial bid, the follow-up bid becomes the initial bid plus half of the initial bid. On the other hand, if the initial bid is rejected, the follow-up bid becomes the initial bid minus half of the initial bid. Thus, Birr 50, Birr 100, and Birr 150 are the lower follow-up bids, whereas Birr 150, Birr 300, and Birr 450 are the higher follow-up bids.

Double-bounded bidding technique

Finally, we observed four joint responses when the sample households were asked the initial and follow-up bid questions: yes-yes, yes–no, no-yes, and no–no.

Model specification

Seemingly unrelated bivariate probit model is used to estimate mean willingness to pay (MWTP) and identify factors that significantly influence rural households' WTP for the CBHI scheme. Let \({\mathrm{t}}^{1}\) denotes the initial bid and \({\mathrm{t}}^{2}\) the second bid. If \({\mathrm{WTP}}_{1\mathrm{i}}\) represents discrete response to the initial bid, and \({\mathrm{WTP}}_{2\mathrm{i}}\) is the discrete response to the follow-up following [25], the seemingly unrelated bivariate probit model can be specified as follows;

\({\mathrm{WTP}}_{1\mathrm{i}}=1\) if \({{\mathrm{WTP}}_{1\mathrm{i}}}^{*}\ge {{\mathrm{t}}_{\mathrm{i}}}^{1}\)

\({\mathrm{WTP}}_{1\mathrm{i}}=0\) if \({{\mathrm{WTP}}_{1\mathrm{i}}}^{*}<{{\mathrm{t}}_{\mathrm{i}}}^{1}\)

\({\mathrm{WTP}}_{2\mathrm{i}}=1\) if \({{\mathrm{WTP}}_{2\mathrm{i}}}^{*}\ge {{\mathrm{t}}_{\mathrm{i}}}^{2}\)

\({\mathrm{WTP}}_{2\mathrm{i}}=0\) if \({{\mathrm{WTP}}_{2\mathrm{i}}}^{*}<{{\mathrm{t}}_{\mathrm{i}}}^{2}\)

E \(\left({\upvarepsilon }_{1\mathrm{i}} |{\mathrm{X}}_{1\mathrm{i}},{\mathrm{X}}_{2\mathrm{i}} \right)=\mathrm{E}\left({\upvarepsilon }_{2\mathrm{i}} |{\mathrm{X}}_{1\mathrm{i}},{\mathrm{X}}_{2\mathrm{i}} \right)=0\)

This study used Krinsky and Robb approach to calculate the MWTP for the CBHI scheme since this approach takes the significance level into account when computing the MWTP.

Results

Socio-economic and demographic characteristics of households

Table 1 shows the descriptive statistics for the variables, with a focus on the mean, minimum, maximum, and standard deviation for continuous variables, and the percentage for categorical variables. The sample respondents' average household head age was 47 years old. On average, the heads of the sample households attended about 5 years in school, which is equivalent to a primary education in the current education system of Ethiopia. Furthermore, around 67 percent of the sample household heads were found to be literate. Male-headed and married households made up about 86 percent and 88 percent of the sample households, respectively. The sample respondents' average household size was around 6, implying that each household had roughly 6 people residing in it.

When the survey was conducted, 65 percent of the sample households faced illness in the previous three months. Table 1 reveals that only 52 percent of the sampled households were members of the CBHI program, but about 90 percent of them were aware of its benefits.

Descriptive analysis of response to bids

As presented in Table 2, the sample households' average open ended WTP is approximately Birr 223, with a zero minimum and Birr 500 maximum values. When compared to socio-economic variables like income, expenditure, and saving, the open ended WTP shows less variation across households.

Table 2 indicates that majority of the sample households are willing to pay the initial bids. Nearly 65 percent of those surveyed answered yes to the initial contingent valuation question and 66 percent of them answered yes to the follow up bid question. On the other hand, about 35 percent of households in the sample refuse to pay the first bid, and 34 percent refuse to pay the follow up bid question.

Together, the responses to the initial and follow-up bids form four possible joint responses. These responses are no–no, no-yes, yes–no and yes-yes. Therefore, households are assigned to one of these responses, and Table 3 summarizes the frequency distribution of the joint responses.

For different groupings of sample households, the proportion of households with positive response to bids varies. Households can be classified into different groups based on a variety of socio-economic attributes. The chi-square test for discrete variable shows households that are literate, members of the CBHI scheme, members of any association, aware of the CBHI scheme, and have a position in the community have a higher proportion of households willing to pay the initial bid than their counterparts (see Table 4).

When employing contingent valuation data, it is critical to ensure that individuals are sensitive to the bid amount; that is, we expect that as the bid value increases, the proportion of respondents with positive response decreases. Figure 2 indicates that the proportion of households with positive response decreases as the bid amount increases. Besides, there is no region where the vertical lines in the bars overlap, implying that the proportion of positive response differs across the level of bids and the difference is significant.

Confidence interval bar graph for response to initial bids

WTP for CBHI scheme and factors associated with it

Table 5 reports estimates of seemingly unrelated bivariate probit. The Wald test rejected the null hypothesis that all regression coefficients are simultaneously equal to zero [\({\upchi }^{2}(26)=126.10\);\(p>{\upchi }^{2}=0.000\)]; implying that the model is of good fit. The correlation coefficient between response to the initial and follow up bids (Rho = -0.0094) is found to be statistically insignificant, as evidenced by the \(P\) > \({\upchi }^{2}\) value of 0.961. This means that the initial bid response and the follow-up bid response are uncorrelated. As a result, estimation of seemingly unrelated bivariate probit model and equation-by-equation estimation of probit models provide the same result.

Following important empirical literatures, thirteen explanatory variables were used in seemingly unrelated bivariate probit regression to determine their effect on WTP for the CBHI scheme. Eight of these variables are statistically significant in influencing the response to the initial bid (see Table 5), which is the focus of our analysis. These variables are amount of bid, household income, family size, household head's education, household health status, membership to community-based health insurance scheme, membership in any association, and awareness about the scheme. While the amount of bid, family size, and household head's education level have a negative effect on the WTP for the CBHI scheme, household income, illness experience, CBHI membership, membership in any association, and awareness about the scheme have a positive effect.

We also calculated the WTP of households for the CBHI scheme following a seemingly unrelated bivariate probit regression. The MWTP for the CBHI scheme was calculated using the Krinsky and Robb method (see Table 6). To assess whether the MWTP estimates obtained by the Krinsky and Robb approach are adequate, the study compared them to the mean of open ended WTP.

The researcher must decide which MWTP to use if sets of MWTP are obtained in order to establish the value of the service in issue [26]. The MWTP computed from the first equation is chosen for different sensible reasons. First, the MWTP calculated from the first equation is close to the mean WTP of a contingent valuation question with an open-ended format (Birr 222.69). Second, the MWTP obtained from the first equation has a smaller variance as indicated by range. Third, the second equation employs household’s response to follow-up bid (as dependent variable), which is sensitive to bias because the household uses the first bid’s clue to make his WTP decision for the follow-up bid. Therefore, on average, the sample household in the study area is willing to pay Birr 255.55 per year (see Table 6). Therefore, multiplying the MWTP by the whole target population yields the welfare gain of Birr 38,668,548 per year.

Discussion

The purpose of this study is to determine the WTP for CBHI and associated factors among households in South West Shoa Zone, Central Ethiopia. Around 65 percent of the households were willing to pay the first bid that was allocated to them at random. We found that households are willing to pay about 256 Birr per year. However, the Ethiopian government set the insurance premium at 240 Birr per household per year. This implies that the households are willing to pay a higher price than the policy price. This gives policymakers an important insight; they need to revise the current premium and set a new premium that reflects the households' willingness to pay.

In contingent valuation, the bid amount is expected to have a negative impact on the WTP. Table 5 (column 2) shows that when the bid amount rises, the probability of willing to pay the initial bid falls. This result is similar to that of [21] who found that as the price of health insurance increases, households are less willing to pay for CBHI scheme.

According to economic theory, the demand for necessities such as health insurance rises as the households' income rises. However, the change in demand in response to change in income is very small. The finding of this study suggests that when household income rises, the probability of willing to pay the initial bid rises as well. This result was iterated by [27,28,29,30], who indicated that demand for health care services, including health insurance, is income inelastic.

The study reveals that family size has a negative effect on the probability of WTP for the CBHI scheme, which is unexpected finding that contradicts many other studies. It means that households with a larger family size are less likely to be willing to pay than those with a smaller family size. One probable explanation is that households with a higher family size have higher non-health consumption expenditure like food, energy, and so on. In this situation, these groups of households spend less on modern health care services, such as health insurance.

A positive relationship between educational level and WTP was expected, but this study reveals that education has a significant negative effect on WTP. Despite the fact that this result contradicts many other findings, it is supported by [31].

Households in the study area, who are members of the CBHI scheme, are paying a premium decided by the government. Their WTP has not been taken into account by the government when determining this premium, indicating that the premium set by the government and households’ WTP for the CBH scheme are not equal. Since member households are aware of the scheme's benefits, it is believed that they would be more willing to pay than non-member households. This study's findings support this notion, indicating that membership in the CBHI scheme increases the probability of WTP for it.

The existence of health problems serves as the foundation for the provision of health care services and, as a result, health insurance. Because most people are risk averse, they are willing to join and pay for the CBHI scheme in order to avoid health-related risks. In particular, those who face illness frequently incur high out-of-pocket payments, hence they are more likely to join and pay for CBHI scheme. In this research, it also found that households who faced illness in the last three months are more willing to pay for the scheme than those who did not.

In rural areas membership in farmers' association builds social cohesion and solidarity, which are fundamental elements of social capital. The social capital facilitates collective action, which in turn, enhances WTP for CBHI scheme. As expected, regression result in this study indicates that WTP is positively influenced by social capital. Being a member of any association increases the likelihood of WTP for the CBHI scheme. This finding is consistent with many previous studies [32,33,34].

In the decision-making process, information, or knowledge, is very essential. In this study, WTP for the CBHI scheme shows a significant relationship with respondent’s awareness of the scheme. Households who are aware of the CBHI scheme are more willing to pay for it than those who are not. This might be due to the fact that households who are able to understand the catastrophic effects of out-of-pocket payments and benefits of joining the CBHI scheme are ready to join and pay for it. This finding is supported by research undertaken in Ethiopia [35], Nigeria [36, 37] and Cameron [19].

Conclusion and policy implications

The results of the study have important implications. First, households are willing to pay a higher price than the policy price. This gives policymakers an important insight; they need to revise the current premium and set a new premium that reflects the households' willingness to pay. Second, social capital attributes such as membership in CBHI scheme and membership in any association play a vital role in WTP for CBHI scheme. Therefore, the local communities need to strengthen their social cohesion and solidarity. Third, especially in rural areas, it is critical to create awareness about the CBHI scheme's benefits. Finally, it is important to account the differences in WTP for CBHI schemes that appear across various groups when determining the amount of premium.

Strengths and Limitations of the Study

The strength of this study is its large sample size and high response rate. Besides, it used double-bounded dichotomous choice format of CVM, which is more efficient than the single-bounded method. However, the study relies on cross-sectional data, which is ineffective in revealing unobserved factors influencing the WTP of the households. Moreover, the responses may be biased which can overestimate or underestimate the results of WTP.

Availability of data and materials

The data will be available from Open Science Framework data repository, titled CBHI_data. xlsx with a link https://osf.io/edn5b

Notes

The socio-economy profile of the zone is obtained from South West Shoa Zone Bureau of Agriculture and Natural Resource (2017).

Woreda is the third -level of the administrative division of Ethiopia – after zone and regional state.

Kebele is the smallest administrative unit in Ethiopia’s government structure – after woreda.

References

United Nations (UN). The 2030 Agenda and the Sustainable Development Goals: An opportunity for Latin America and the Caribbean. Santiago: LC/G.2681-P/Rev. 2018.

Cotlear D, Nagpal S, Smith O, Tandon A, Cortez R. How 24 developing countries are implementing universal health coverage reforms from the bottom up. 2015.

Wagstaff A, Neelsen S. Comprehensive assessment of universal health coverage in 111 countries: a retrospective observational study. Lancet Glob Health. 2020;8(1):e39-49.

Boerma T, Eozenou P, Evans D, Evans T, Kieny M-P, Wagstaff A. Monitoring progress towards universal health coverage at country and global levels. PLoS Med. 2014;1(9):1–8.

Wang H, Switlick K, Ortiz C, Zurita B, Connor C. Health Insurance Handbook. How to make it work. World Bank Working Paper; No. 219. 2012.

Ahuja R, Jütting J. Are the poor too poor to demand health insurance? J Microfinance. 2004;6(1):1–20.

Carrin G, Waelkens M-P, Criel B. Community-based health insurance in developing countries: a study of its contribution to the performance of health financing systems. Tropical Med Int Health. 2005;10(8):799–811.

Tabor SR. Community-based health insurance and social protection policy social protection discussion paper series; 0503. 2005.

Jacobs B, Bigdeli M, van Pelt M, Ir P, Salze C, Criel B. Bridging community-based health insurance and social protection for health care – a step in the direction of universal coverage? Tropical Med Int Health. 2008;13(2):140–3.

World Health Organization (WHO). Health systems financing the path to universal coverage the world health report. 2010.

Federal Democratic Republic of Ethiopia Ministry of Health (FMoH). Ethiopia’s Fifth National Health Accounts 2010/2011. 2014.

Shigute Z, Mebratie AD, Sparrow R, Alemu G, Bedi AS. The effect of Ethiopia’s community-based health insurance scheme on revenues and quality of care. Int J Environ Res Public Health. 2020;17:1–17.

Meghan S. Micro-Finance Health Insurance in Developing Countries. Wharton Research Scholars Journal. 2010.

Bacchetta M, Ernst E, Bustamante JP. Globalization and Informal Jobs in Developing Countries. 2009.

Feleke S, Mitiku W, Zelelew H, Ashagari TD. Ethiopia’s Community-based Health Insurance A Step on the Road to Universal Health Coverage. 2015.

Yilma Z, Mebratie A, Sparrow R, Dekker M, Alemu G, Bedi AS. Health risk and insurance: impact of Ethiopia’s community based health insurance on household economic welfare. The World Bank Econ Rev. 2015;29:S164–73.

Mebratie AD, Sparrow R, Alemu G, Bedi AS. Community-Based Health Insurance Schemes A Systematic Review. 2013.

Dibaba A, Hadis M, Ababor S, Assefa Y. Improving Health Care Financing in Ethiopia: An Evidence Brief for Policy. 2014.

Donfouet HPP, Mahieu P-A. Community-based health insurance and social capital: a review. Health Econ Rev. 2012;2(5):1–5.

Kebede A, Gebreslassie M, Yitayal M. Willingness to pay for community-based health insurance among households in the rural community of Fogera District, North West Ethiopia. Int J Econ Finance Manage Sci. 2014;2(4):263–9.

Entele BR, Emodi NV. Health insurance technology in Ethiopia: willingness to pay and its implication for health care financing. Am J Public Health Res. 2016;4(3):98–106.

Kado A, Merga BT, Adem HA, Dessie Y, Geda B. Willingness to pay for community-based health insurance scheme and associated factors among rural communities in gemmachis district. Eastern Ethiopia ClinEcon Outcomes Res. 2020;12:609–18.

Greene WH. Econometric Analysis, Eighth Edition Pearson Education inc. 2018.

Israel GD. Determining Sample Size. Agricultural Education and Communication Department, Florida Cooperative Extension Service, Institute of Food and Agricultural Sciences, University of Florida, USA. 2012.

Verbeek M. A guide to modern econometrics: 2nd. edition. John Wiley & Sons, Limited. 2004.

Haab TC, McConnell KE. Valuing Environmental and Natural Resources: The Econometrics of Non-market Valuation. Glensanda House, Montpellier Parade, Cheltenham, Glos GL50 1UA, UK: Edward Elgar Publishing Limited. 2002.

Ringel JS, Hosek SD, Vollaard BA, Mahnovski S. The Elasticity of Demand for Health Care A Review of the Literature and Its Application to the Military Health System. National Defense Research Institute. 2002.

Binnendijk E, Dror DM, Gerelle E, Koren R. Estimating Willingness-to-Pay for health insurance among rural poor in India by reference to Engel’s law. Soc Sci Med. 2013;76:67–73.

Lawanson AO, Ibrahim MN. Willingness to pay for community health insurance: a study of Hygeia operations in Shonga and Afon communities in Kwara State. Afr J Health Econ. 2015;4(1):1–15.

Goodman S. The Income Elasticity of Demand for Health Insurance. [Berkeley]: University of California, Department of Economics. 2017.

Ahmed S, Hoque ME, Sarke AR, Sultana M, Islam Z, Gazi R, et al. Willingness-to-pay for community-based health insurance among informal workers in Urban Bangladesh. PLoS ONE. 2016;11(2):1–16.

Zhang L, Wang H, Wang L, Hsiao W. Social capital and farmer’s willingness-to-join a newly established community-based health insurance in rural China. Health Policy. 2006;76:233–42.

DonfouetEssombèMahieu HPPJ-REP-A, Malin E. Social Capital and Willingness-to-Pay for Community-Based Health Insurance in Rural Cameroon. Global J Health Sci. 2011;3(1):142–9.

Ko H, Kim H, Yoon C-G, Kim C-Y. Social capital as a key determinant of willingness to join community-based health insurance: a household survey in Nepal. Public Health. 2018;160:52–61.

Minyihun A, Gebregziabher MG, Gelaw YA. Willingness to pay for community-based health insurance and associated factors among rural households of Bugna District. Northeast Ethiopia BMC Res Notes. 2019;12(55):1–7.

Onwujekwe O, Okereke E, Onoka C, Uzochukwu B, Kirigia J, Petu A. Willingness to pay for community-based health insurance in Nigeria: do economic status and place of residence matter? Health Policy Plan. 2010;25(2):155–61.

Ogundeji YK, Ohiri K, Butawa NN. Factors influencing willingness and ability to pay for social health insurance in Nigeria. PLoS ONE. 2019;14(8):1–10.

Acknowledgements

We deeply express our gratefulness to Ambo University for providing financial support, without which this research would not have been possible. Our sincere gratitude and special thanks also go to the South West Shoa Health Office. We would also like to express our gratitude to the health extension workers who participated in the study as enumerators.

Funding

This research was funded by Ambo University. The views expressed in the paper, however, are those of the authors and do not reflect that of the University.

Author information

Authors and Affiliations

Contributions

Mebratu Negera conceived the initial idea, developed the proposal, and offered it to Ambo University's Woliso Campus's research and community service director. Both authors were involved in the data collection supervision. Mebratu Negera was in charge of encoding, analyzing, and writing the paper. The authors read and approved the final manuscript.

Corresponding author

Ethics declarations

Ethics approval and consent to participate

The study was reviewed and approved by the Ambo University Woliso Campus Ethical Review Committee. Official permission letters were also received from the South West Shoa Health Office as well as the health offices of the woredas under inquiry. After being informed about the study's purpose and importance, informed consent was obtained from all participants. The interview was conducted in accordance with the given norms and regulations. The respondent's name was not included in the questionnaire, and the data was kept anonymous at all stages of the research.

Consent for publication

Not applicable.

Competing interests

The authors declare that they have no known competing financial interests or personal relationships that could have appeared to influence the work reported in this paper.

Additional information

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary Information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/. The Creative Commons Public Domain Dedication waiver (http://creativecommons.org/publicdomain/zero/1.0/) applies to the data made available in this article, unless otherwise stated in a credit line to the data.

About this article

Cite this article

Negera, M., Abdisa, D. Willingness to pay for community based health insurance scheme and factors associated with it among households in rural community of South West Shoa Zone, Ethiopia. BMC Health Serv Res 22, 734 (2022). https://doi.org/10.1186/s12913-022-08086-z

Received:

Accepted:

Published:

DOI: https://doi.org/10.1186/s12913-022-08086-z