Abstract

Background

In Togo, about half of health care costs are paid at the point of service, which reduces access to health care and exposes households to catastrophic health expenditure (CHE). To address this situation, the Togolese government introduced a National Health Insurance Scheme (NHIS) in 2011. This insurance currently covers only employees and retirees of the State as well as their dependents, although plans for extension exist. This study is the first attempt to examine the extent to which Togo’s NHIS protects its members financially against the consequences of ill-health.

Methods

Data was obtained from a cross-sectional representative households’ survey involving 1180 insured households that had reported illness in the household in the 4 weeks preceding the survey or hospitalization in the 12 months preceding the survey. The incidence and intensity of CHE were measured by the catastrophic health payment method. A logistic regression was used to analyse determinants of CHE.

Results

The results indicate that the proportion of insured households with CHE varies widely between 3.94% and 75.60%, depending on the method and the threshold used. At the 40% threshold, health care cost represents 60.95% of insured households’ total monthly non-food expenditure. This study showed that the socioeconomic status, the type of health facility used, hospitalization and household size were the highest predictors of CHE. Whatever the chosen threshold, care in referral and district hospitals significantly increases the likelihood of CHE. In addition, the proportion of households facing CHE is higher in the lowest income groups. The behaviour of health care providers, poor quality of care and long waiting time were the main factors leading to CHE.

Conclusion

A sizable proportion of insured households face CHE, suggesting gaps in the coverage. To limit the impoverishment of insured households with low income, policies for free or heavily subsidized hospital services should be considered. The results call for an equitable health insurance scheme, which is affordable for all insured households.

Similar content being viewed by others

Background

About 150 million households worldwide face catastrophic health expenditure (CHE) annually, and some 100 million were driven into poverty because of health care costs, according to the World Health Organization (WHO) estimates about a decade ago [1]. These numbers were bound to increase over the last decade in the absence of major changes in the health financing system. Indeed, the fifty-eighth World Health Assembly made a call to “plan the transition to universal coverage of population” which theoretically should decrease exposure to CHE. This call resonates in Sub-Saharan Africa (SSA), where households’ protection from the consequences of health shocks is a major concern because of the importance of household out-of-pocket payments (OOP) at the point of service as a means of financing the health system [2].

Recently, considerable literature has emerged around the theme of health insurance, universal coverage and CHE. Wagstaff and Doorslaer [3] have shown that the incidence and intensity of “catastrophic” payments—both in terms of pre-payment income as well as ability to pay—were reduced between 1993 and 1998, and that both incidence and intensity of “catastrophe” became less concentrated among the poor in Vietnam as a result of change in implementation of insurance policy. Recently, Kusi et al. [4] found that the Ghanaian national health insurance scheme has significantly reduced out-of-pocket (OOP) payments and offered financial protection against CHE for insured individuals and their households. Also, it was found that Rwanda Mutual Health Insurance Scheme led to a fourfold decrease in incidence of CHE [5]. Other studies have also shown that a well-functioning prepayment system has a strong potential to improve financial protection against illness [6,7,8]. In contrast, a few studies have suggested that insurance is not a panacea against CHE. According to Ekman [9], health insurance did not provide financial protection against the risk of catastrophic payments in Zambia using 1998 data; on the contrary, insurance was found to increase such risk. China’s New Cooperative Medical System program between 2004 and 2007 clearly did not meet one of its key goals of providing insurance against catastrophic illnesses [10].

In West Africa, the introduction of insurance and fees waiving schemes has not shielded all households from substantial out of pocket expenditure. In Nigeria, despite the implementation of the National Health Insurance Scheme (NHIS) to protect families from the financial hardship, a study based on Oyo State has shown low uptake and significant CHE among the poorest quintile [11]. In Mali, the State implemented a fee waiver for Caesarean sections and a maternity referral-system; however those policies fail to eliminate financial obstacles for remote households so that women who underwent Caesareans continue to incur catastrophic expenses [12]. Also, studies in Burkina Faso showed that rich enrolees in the Community-Based Health Insurance Programs used more health care and faced less CHE than poor enrolees [13,14,15].

In Togo, a West African country, neighbour to Burkina Faso, Ghana and Benin, household contributions to total health expenditures accounted for 48.6% in 2012 [16]. This proportion is more than twice as high as the 15%–20% threshold recommended by the WHO [17, 18]. To address the substantial out-of-pocket payments and thus the CHE problem, the Togolese government introduced a National Health Insurance Scheme (NHIS) in 2011. The establishment of the NHIS in 2011 is a major step by the Togolese government to address the perverse problems of the “cash and carry” system. However, in practice, insured households experience difficulties accessing care with their NHIS because of the health professionals’ and facilities’ reluctance to deal with the insurance’s heavy administrative procedures and delayed reimbursement [19]. In addition, the NHIS covers only a predetermined list of medications or formulations at pre-set prices to contain cost; thus, reducing patients and their providers’ options. Oftentimes, listed drugs are stocked out, prices changed [19] without due notice. A satisfaction survey of NHIS enrolees conducted in 2015, revealed a list of issues: dissatisfaction with management of chronic diseases, coverage exclusion, long waiting times, informal payments to providers, and the heavy claim procedures [20].

In this context, it may be possible that insured households still face important OOP leading to CHE. This paper seeks to examine the incidence and intensity of catastrophic payments and determinants of CHE among households insured NHIS in Togo. Empirical evidence on CHE and its determinants among insured households may provide useful information to policy makers to improve services offered by Togo’s compulsory health insurance scheme. This paper also adds to the growing body of international research which seeks to examine the incidence and intensity of catastrophic payments and its determinants for the achievement of meaningful universal coverage [21,22,23,24]. This paper is part of a series of studies on influence of health insurance on households’ economic well-being.

Overview of Togo’s National Health Insurance Scheme (NHIS)

Since 2010, Togo implemented a new approach to national planning for health. A new National Health Policy and a National Health Development Plan for 2012–2015 was drafted in 2011 [25]. Along the same lines, legislation calling for the establishment of a national health insurance scheme targeting civil servants, central administration staff, local collectivities, para-public agencies, and retired public sector workers was passed in 2011 [26]. Fees for caesarean sections were waived, the same year [26]. In 2012, the National Health Insurance Scheme (NHIS), began paying for the health services, covering approximately 300,000 people [25]. The scheme is managed by the National Institute of Health Insurance (INAM). NHIS aims to provide quality health care along with financial protection to enrolled households by covering risks associated with diseases, non-occupational accidents and maternity. NHIS is a mandatory health insurance which covers civil servants, civil servant retirees, and up to five dependents—spouse and four children aged 21 or under. The rate of coinsurance paid by members varies depending on the type of service [27]. Coverage of the private and informal sectors through NHIS has not begun yet. The care package covers different proportions of costs depending on the condition/disease. For instance, the NHIS covers 80% of the cost of general and specialized consultations, pharmaceutical medicines, laboratory tests and medical imaging, nursing care, orthopaedic-devices; 90% of surgeries and other inpatient care and 100% of pregnancy and childbirth care. Family planning commodities and services are not covered. This mandatory health insurance scheme is financed by monthly premium contributions set at 7% of the basic monthly salary split equally between the state employer and the main insured person. Services in public health facilities are covered by INAM; private health facilities, pharmacies, and eye care facilities can apply for accreditation [27]. It is estimated that in 2016, 196 private facilities were accredited [25].

Methods

Measuring catastrophic health expenditure (CHE)

Various methods have been used to evaluate the importance of health expenditure with respect to the total household income, household expenditure, household consumption, and household expenditure net of spending on basic necessities. Each method has its advantages and drawbacks [3, 28,29,30].

Two approaches of CHE were used in this study: capacity to pay (CTP), and total expenditure. CTP is defined as the share of household expenditure net of spending on basic necessities [3, 28,29,30,31]. In our study, we used food expenditure at subsistence level as a proxy for basic necessities [28, 31]. Two indicators were used: the catastrophic payment headcount (incidence) and the catastrophic payment gap (intensity). The catastrophic payment gap captures the average severity of payment above the catastrophic threshold [31].

Statistical analyses

Variables

The variables (listed below) and computational steps to generate them are summarised here:

-

Q = Total expenditure of household

-

T = Household out of pocket payment for health care

-

D(Q) = Total food expenditure of household

-

Y = Household’s capacity to pay

-

z = A specific threshold (from 5% to 40%). It represents the point at which the absorption of households’ resources by health care is considered to impose a severe disruption to their living standards [28].

-

H = Incidence of CHE (catastrophic payment headcount)

-

OOPratio = Ratio of out of pocket health expenditure to total household’s expenditure

-

E = Indicator variable which equals 1 if a household (i) is classified as having incurred CHE

-

G = Catastrophic payment overshoot

-

MPO = Mean positive overshoot

-

N = Sample size

Steps

Step 1

Compute household’s capacity to pay by subtracting total food expenditure of household from total expenditure of household:

Step 2

OOP health payments share of household capacity to pay is defined as the ratio of OOP payments to the household’s capacity to pay:

Step 3

The CHE is computed as a binary = 1 if household incurred catastrophic expenditure, and 0 otherwise. For a given threshold z(from 5% to 40%), the CHE would be obtained as follow:

Step 4

The incidence of CHE (catastrophic payment headcount) is measured as the proportion of the sampled households whose OOP health expenditure as a fraction of their total non-food expenditures exceeds the specified threshold (z). The catastrophic payment headcount is estimated as: 92560995

Step 5

The catastrophic payment overshoot which measured the intensity of the catastrophic OOP health expenditure is estimated as:

\( G=\frac{1}{N}\sum \limits_{i=1}^N{O}_i \) with O i = E i (T i [Q − D(Q)] ≻ z).

Step 6

The MPO which measures the mean overshoot among households making CHE at a specified threshold in the sample is estimated by related the incidence (H)and the intensity or overshoot (G). The MPO is calculated as follow:

To check the robustness of the results obtained using the above methodology, we use the total expenditure approach. All indicators above can also be defined with total expenditure of household (Q)as denominator.

Measuring determinants of CHE

The logistic regressions model [32] was used to analyse the determinants of CHE. The dependent variable takes the value of 1 if health care costs as a share of CTP exceed the threshold level (i.e. if the household experienced catastrophic health expenditure) and 0 otherwise.

Explanatory variables chosen

With regards to the explanatory variables, the literature suggests that the likelihood of a household incurring CHE is a function of its socio - demographic characteristics such as the size, age of head of household, household head’s educational level, place of residence, health status of household members, economic status of the household, and type of health facility used [4, 7, 8, 33,34,35]. Kusi et al. [4] showed that, in Ghana, households which experienced hospitalisation of a member were over 7.0 times more likely than those without hospitalisation to incur CHE. In Iran, 42.6% of hospitalized subjects encountered catastrophic health expenditure [36]. Studies showed that hospitalization, household members with chronic illness and poverty status of the household are the major factor determining the financial catastrophe related to ill health [4, 36, 37]. The likelihood of facing CHE were 4.4. and 27 times higher among households having chronically illness persons and those that had case of hospitalization, in Georgia [37]. Along the same lines, Buigut et al. [6] support that health expenditure depends on the type of illness and where health service is sought.

In this study, owing to multicollinearity, the explanatory variables used were: type of illness, health status of household members, hospitalization, type of health facility used, household size, age of head of household, and income quintile. We expected the hospitalization and health status of household members (chronic illness) to be positively correlated with catastrophic expenditure. We assumed that households facing catastrophic expenditure are affected by type/place of treatment they receive [4, 34, 37]. Moreover, we hypothesized that household size and age of head of household affect positively CHE. Studies have shown that, in Burkina Faso, only household size, among households characteristics had a positive association with CHE at 30% and 40% threshold level [34]. It has been demonstrated also that catastrophic expenditure were more common among the households who had more elderly people [38] as individuals spend more on healthcare with increasing age [39, 40]. All these variables are described in Table 1.

Sampling and data collection

This paper used the cross-sectional representative insured household survey data of monitoring of NHIS project implemented by the Centre de Recherche et de Formation en Economie et Gestion (CERFEG) in partnership with African Population and Health Research Center (APHRC).

Study area

In Togo, a West African country, the incidence of poverty varies from 33% in Lomé-commune the capital city to 91% in the Northern Savanah region [41]. The country is divided into 6 administrative health regions, comprising forty (40) health districts and more than 882 peripheral health units. Lomé-Commune comprises about a quarter of the national population (24%), but three-quarter (76%) of private health facilities and physicians (74%) and the highest concentration of insured households (40%) [42].

Sample size

To define the sample size for data collection, we used the Lwanga and Lemeshow approach [43]. With a 95% confidence interval for a difference in proportions, sample size is given by:

Where p1 represents the incidence of CHE among publicly insured households, andp2the incidence of CHE among privately insured households. n1 and n2 are the groups sample size.

We relied on several recent studies carried out in developing countries to estimate the true proportion of p1 and p2. Barros et al. [44] found that among households with private insurance in Brazil, CHE varied from 2% to 16%. In twelve Latin American and Caribbean countries, the percent of households with CHE ranged from 1 to 25% [45]. In Ghana, Togo’s western neighbour which shares many of the same ethnic groups and potentially the same health behaviour, the incidence of CHE among fully insured households which sought healthcare from national health insurance system was 6.0% [4]. In contrast, Onwujekwe et al. [46] showed that about 27% of insured households incurred CHE, in four local government areas in southeast Nigeria. We therefore conservatively hypothesize that the CHE among the public and private insured households are respectively around 25% and 15% in Togo.

With absolute precision of 5%, the required sample size is 484 in each group, thus 968. We increased the sample size by 22% to account for sampling errors, mistakes in filling questionnaires and data entry mistakes, as well as fair management of interviewers (number of interviews per person). The final sample interviewed was 1180 insured households.

Data collection

We designed a questionnaire based on the World Health Survey 2002 and the latest Togo’s 2013 Demographic Health Survey questionnaires. Trained interviewers conducted in-person face-to-face interviews. To minimise recollection errors, data were collected exclusively from insured households with at least one case of illness in the 4 weeks preceding the survey or at least one case of hospitalization the 12 months preceding the survey.

Lomé-Commune is organized in 5 health districts with different population size and density. To obtain a representative sample of Lome-Commune, we accounted for density by district as determined by the latest Togo Population and Housing Census [47]. The numbers of insured households surveyed in each district are respectively 36, 490, 264, 84, and 306. In each district, we randomly chose a street and sent interviewers along the road. They went into every household and interviewed only the consenting heads of insured households or their spouses in May 2016. This study focused only on 578 households insured with NHIS.

Main variables construction

Data collected included health utilization and spending, household income and expenditure, education, occupation and marital status, gender, age, and other socioeconomic background information about insured households. We used the exchange rate of 16 May 2016 which is the middle of the month and is about the average of the period 1 USD = 579 XOF.

Appropriate reference periods were used to collect the expenditure data. All expenditures were adjusted in the same unit of 4 weeks. For example, during data collection, the reference period for clothing, shoes, maintenance and major repair expenses was the 3 months preceding the survey, while that of expenses such as electricity, water, etc. was 1 month preceding the survey [6]. This difference in reference period is explained by the fact that electricity and water bills tend to be incompressible and are paid monthly, while expenses for clothing and shoes are more discretionary and much less regular. Thus, we divided clothing expenditure by three. With regards to food expenditures, we first collected details on the previous day food consumption, then all information on food expenses for the previous 7 days preceding the survey [6]. We then extrapolated the weekly food consumption expenditures to 4 weeks. Food expenditure include cereals, vegetables, tubers, fruits, spices, fish, meat, oil and fat, milk and eggs, restaurant meals, etc. As for health expenditure, collected information includes expenses for medicines and vaccines, diagnostic and laboratory tests fees, consultation and treatment costs, hospitalization fees, cost of visits to traditional healers, transport, and other expenses related to outpatient care over the last 4 weeks preceding the survey; similar expenses were collected for hospitalization but with a year reference period.

Results

Descriptive statistics

Socio-demographic characteristics of the insured households

Table 2 summarizes socio-demographic characteristics of the sample. Most insured households were headed by men (72.39%) who were married (84.99%) and aged between 18 and 49 years (86.11%). About six out of ten household heads of households in our sample had some university level education (59.23%), while 29.89% had dropped out of high school. For a smaller percentage, the highest education levels were junior high school (7.93%) and primary education (2.21%). Most households had between 2 and 4 persons (45.05%), followed by households consisting of 5 or 6 persons (23.06%), households consisting of 1 or 2 persons (17.16%) and finally, households consisting of more than 6 persons (12.73%).

The distribution of NHIS beneficiaries by wealth quintile shows that the households in the lower wealth quintiles represent around 33.37%; the tops quintiles are around 50% of insured households. The analysis of the income level by quintile reveals startling inequalities: insured households belonging to the fifth highest quintile have an average annual income per capita almost 4 times as high as that of the lowest quintile.

Diseases/conditions, provider of health care and distribution of expenses

Malaria was the main and the most frequently reported disease (46.18%), followed by infections and injuries (6.45%), intestinal worms (5.69%), and hypertension (4.93%). Other reported diseases included diarrhoea (3.04%), respiratory diseases/pneumonia (3.04%), and diabetes (2.28) (Table 3). These results seem to be consistent with Togo’ national health statistics. In Togo, the most frequently reported disease are malaria (44.9%), infections and injuries (8.4%), intestinal worms (4.9%), hypertension (1.8%) [48] in 2015.

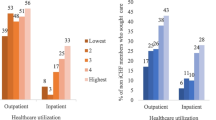

About 29.93% of insured households used self-medication in case of illness. About a quarter (23.98%) received care from district hospitals and 14.50% from referral hospitals. However, it should be emphasized that more than half (50.93%) of the insured households used public health facilities compared to 15.80% who used private ones. Finally, a small proportion (3.16%) had recourse to traditional healers.

The mean monthly expenditures of insured households were at 310, 881.5 FCFA (or 536.928 USD using the average value for the period reference). The mean OOP, including medical and non-medical expenditures, was 29, 434.2 FCFA (50.836 USD) or about 9.47% of the total expenditures. The average health expenditure per household represents 14.41% of total expenditure net of food spending.

Incidence and severity of CHE among insured households

Table 4 presents the incidence (headcount) and intensity (overshoot) of CHE. For sensitivity analysis, we varied the threshold from 5% to 40%. The 29% of the sample who used self-medication decided themselves to support OOP. Thus, they are excluded from the household facing CHE.

In model 1, we used the capacity to pay (total monthly non-food expenditure) as a reference. The proportion of insured households facing CHE decreased from 75.60% to 9.71% as the threshold increases from 5% to 40%. The mean positive overshoots (MPOs) shows that the insured households facing CHE at the 30% threshold on the average spent 52.03% (30% + 22.03%) of their total monthly non-food expenditure on health care. For households incurring CHE at the 40% threshold, health care cost represents 60.95% (40% + 20.95%) of their total monthly non-food expenditure. These households incurring CHE at the 40% threshold represent about 9.71% of the sample.

Using monthly expenditure, we found a similar trend as observed in Model 2 but with smaller magnitudes. The proportion of households facing CHE decreased from 64.30% to 3.94%, as the threshold increased from 5% to 40%. At the 40% threshold, households with CHE spent 66.08% of their total monthly non-food expenditure on health care.

Comparing retirees and the still-employed by the government, the concentration index was 0.0063 indicating a very slight inequality between both groups.

Determinants of catastrophic health expenditure

In this section, we analyse factors associated with CHE among insured households with a logistic regression. First, we examined Variance Inflation Factors (VIF) for multicollinearity in our sample. The largest VIF was 8.74 and the mean VIF was around 1.98, which does not suggest high multicollinearity. We used the Hosmer-Lemeshow to test assess goodness of-fit [49] and found it satisfactory (Table 5). In conformity with WHO’s approach [1, 50], we estimated the model 1 with OOP as percent of total monthly non-food expenditure with thresholds of 10, 20, 30, and 40%.

The results indicate that hospitalization significantly impacts the likelihood of experiencing CHE across all thresholds. But other socio-demographic characteristics such as household size and income indicate mixed results. At 10%, any increase in household size by one leads to an increase in the likelihood of CHE by 14% but at 40%, the direction of the association is significantly opposite. Similarly, the impact of the household wealth quintile on CHE is mixed. We found statistically significant results at the 30% threshold where households in the two lowest quintiles face a higher likelihood of CHE. The signs of the coefficients show that the likelihood of CHE is higher among households in lowest incomes group, and that this likelihood decreases as the income increases.

In other words, the likelihood of CHE increases with hospitalization and decreases with income. Similarly, the likelihood of CHE increases significantly with access to hospital care. At the lower thresholds of 10 and 20%, the likelihood of CHE is higher in referral hospitals and district hospitals, compared to private health facilities. At 30% and 40% thresholds, only the use of referral hospitals and district hospitals positively affects CHE. Whatever the chosen threshold, care in referral and district hospitals significantly increases the likelihood of CHE. Furthermore, recourse to traditional healers significantly increases OOP with a higher likelihood compared to private health facilities.

Discussion

This study is probably the first to attempt to examine the extent to which Togo’s national health insurance system protects its members financially against ill-health. The results suggest that a substantial proportion of insured households still face CHE, but the incidence of CHE is sensitive to the method and the threshold used.

At the 10% threshold, the proportion of insured households which faced CHE was 54.60%. At the 40% threshold (commonly used in the literature), this proportion fell to 9.71%. This incidence of CHE is well above similar studies carried out in Ghana (6.00%), India (4.8%), Vietnam (4.2%), and Nepal (4.56%) [4, 7, 51, 52]. These results are particularly concerning since at 30% and 40% thresholds, health care cost represents 55.03% and 60.95% of the households’ total monthly non-food expenditure respectively. These high proportions of households’ non-food expenditure allocated to health care could result from asset sales, reduction of savings, indebtedness and impoverishment of insured households in Togo [24, 53,54,55]. We hypothesize that the high proportion of CHE may also be due to several factors: some conditions or formulations of prescription are excluded; also, some insured households may be paying out-of-pocket rather than asserting their insurance right, as providers devote more time and energy to those uninsured patients who pay cash the costs of health care directly rather than those with insurance who required heavy administrative procedures before reimbursement.

Regarding determinants of CHE, this study showed that socioeconomic status, type of health service sought, hospitalization, and household size are the main determinants of CHE.

One interesting finding is that the importance of household income in predicting CHE. CHE decline as income rises, regardless of the threshold used. These results are consistent with those of Su et al. [34] who showed that in Nouna District in Burkina Faso (Togo’s northern neighbour), the proportion of households facing CHE is higher in the lowest income groups, whatever the threshold used. These results are also in agreement with those obtained by Buigut et al. [6] who showed that in Kenya, households in the highest income tertile were less likely to experience CHE compared to those in the lowest income tertile. Considering the higher proportion of poorer households’ income or consumption allocated to food, any small expenditure on health can be financially disastrous to them. It is thus difficult for the poorest of the poor to divert resources from basic needs [56]. We could conclude that high income level affords some protection against CHE [57,58,59]. These results suggest that, to limit the impoverishment of insured households with low incomes, policies of free or highly subsidized hospital care should be considered, at least for the poor. The results call for an equitable health insurance scheme and affordable for all insured households [6].

The importance of the household size is mixed. At the 10% threshold, the results suggest that the household size increases the likelihood of the CHE occurrence. Large households are significantly associated with high CHE in other studies as well [33, 34, 60]. However, at the 40% threshold, the results are inversed. In Kenya, Buigut et al. [6] found that increase in the household size decreases probability of CHE.

Another important finding was that hospitalization significantly increases the likelihood of CHE. The likelihood of CHE is low among insured households without hospitalization, irrespective of the chosen threshold. These results matched of those of Anbari et al. [36] who found that hospitalization was one of the highest predictors of facing CHE, in Iran. There are several possible explanations for these results. First, more severe illnesses require hospitalization and patients might require medication or formulation that are not covered by the insurance or that providers do not offer at the listed prices, requesting the difference from the patient. Moreover, hospitalization increases transport cost for the family members and thus direct non-medical spending. Third, the fee-for-service structure of the insurance may favour supplier-induced demand that raises expenses including those not covered by the insurance. Indeed, the relationship between care provider and patient is characterized by asymmetric information, the care provider may increase the demand for care and therefore the increase in the financial burden borne by the patient. These results corroborate those of Mbaye et al. [61] and Haddad et al. [62] who studied the policies of subsidized C-section childbirths in Senegal and in Benin respectively. In those two countries in order to protect families against CHE, costs associated with C-section deliveries are subsidized by the State, while those of normal delivery are not. The authors found an increase in the likelihood of C-sections in Senegal and an increase in the hospital length of stay in Benin. Those changes generate additional revenues for providers and contribute to higher costs for both insurer and insured. These results suggest a need for improvement of the NHIS’s implementation in terms of strengthening functions and the means of regulation and control.

It is interesting to note the significant association between the type of health care facility and CHE. The likelihood of CHE is higher with care in referral and district facilities which are publicly owned and are expected to be more affordable than the private health facilities. A possible explanation might be that patients in referral hospitals are sicker and receiving specialized and expensive care including: emergency or intensive care, surgery services etc. These referral hospitals care for most serious or severe cases across the country. We however hypothesize that one of the key explanations is the behaviour of health care providers towards insured households (care provider/patient relationship). It is generally found that care providers devote more time and energy to uninsured patients who pay the costs of health care directly rather than those with an insurance which requires cumbersome administrative procedures before reimbursement. Thus, in order to receive any immediate and comprehensive care, good quality health care and more attention, some insured households prefer OOP to asserting their insurance right. These results suggest, firstly, the need to sensitize health care providers on issues of equity in access to health care and the impact of health care cost on household impoverishment, particularly poor households. Additionally, the relationship between the NHIS, health facilities, and health care providers must be reviewed and improved, by taking into account the constraints and challenges facing health care providers.

It is interesting to note that longer distance to seek health care contribute to high CHE due to transport cost. This result may be explained by the fact that transport cost is not included in the benefit package of the NHIS. Any policies reducing the physical barrier to health care could help reduce the CHE [4].

Finally, the households’ health care seeking behaviour may also affect the cost of treating the disease, as fall back to traditional healers significantly increases the likelihood of CHE, particularly for low-income households. As in Ghana [4], a possible explanation might be that traditional healers’ care is not covered by NHIS. Given the importance of this sub-sector, the State should consider the possibility of a health insurance system extending its services to practitioners of alternative medicine recognized or approved by the State [4].

Limitation

This study has some limitations. The expenditure data used to measure the different indicators were self-reported and not verifiable with other administrative sources. Moreover, the recall period of health expenditure data was 4 weeks, much longer than the two recommended 2 weeks for outpatient but less than 3 months or a year used for other studies [6, 63]. So, we cannot ignore the potential for measurement error in the assessment of OOP and CHE. Furthermore, because of the problem of multicollinearity, it was impossible to analyse the relationship between gender, educational level, marital status and CHE. We assumed that educational level and marital status could be approximated by the level of income and household size.

Despite these limitations, this study has several strengths. It was based on a random sampling of insured households which help with generalizability; it provided useful information on gaps in coverage among insured households and raised other questions. For instance, further studies should compare incidence and determinants of CHE among households with different types of insurance, NHIS and other private insurance.

Conclusion

By examining the incidence and intensity of CHE and by identifying the main factors associated with CHE, this study aims at analysing financial protection against the disease risk of households insured by NHIS in Togo.

Our results indicate that households enrolled in the State mandatory scheme for its employees and their dependent NHIS are not fully protected against CHE. Factors such as hospitalization, type of health facility used, household income, and household size are significantly associated with CHE. Several policy implications emerge from our study.

-

(i)

Medical care fee exemption or heavier subsidies for low-income insured households should be considered to ensure affordability and equity for all insured households

-

(ii)

The relationship between the state compulsory insurance, care providers and patients should be re-examined in order to reduce asymmetric information and provide better quality health care at a lower price.

Abbreviations

- APHRC:

-

African Population and Health Research Center

- CERFEG:

-

Centre de Recherche et de Formation en Economie et Gestion

- CHE:

-

Catastrophic health expenditure

- CTP:

-

Capacity to pay

- MPO:

-

Mean positive overshoot

- NHIS:

-

National health insurance scheme

- OOP:

-

Out-of-pocket payments

- SSA:

-

Sub-Saharan Africa

- VIF:

-

Variance inflation factors

- WHO:

-

World Health Organization

References

WHO. Health financing for universal coverage. Technical brief for policy-makers: designing health financing systems to reduce catastrophic health expenditure. Geneva: World Health Organisation; 2005.

Leive A, Xu K. Coping with out-of-pocket health payments: empirical evidence from 15 African countries. B World Health Organ. 2008;86(11):849–856C.

Wagstaff A, Doorslaer EV. Catastrophe and impoverishment in paying for health care: with applications to Vietnam 1993–1998. Health Econ. 2003;12(11):921–33.

Kusi A, Hansen KS, Asante FA, Enemark U. Does the National Health Insurance Scheme provide financial protection to households in Ghana? BMC Health Serv Res. 2015;15:331.

Saksena P, Antunes AF, Xu K, Musango L, Carrin G. Mutual health insurance in Rwanda: evidence on access to care and financial risk protection. Health Policy. 2011;99(3):203–9.

Buigut S, Ettarh R, Amendah DD. Catastrophic health expenditure and its determinants in Kenya slum communities. Int J Equity Health. 2015;14:46.

Chuma J, Maina T. Catastrophic health care spending and impoverishment in Kenya. BMC Health Serv Res. 2012; https://doi.org/10.1186/1472-6963-12-413.

Nguyen HT, Rajkotia Y, Wang H. The financial protection effect of Ghana National Health Insurance Scheme: evidence from a study in two rural districts. Int J Equity Health. 2011;10:4.

Ekman B. Catastrophic health payments and health insurance: some counterintuitive evidence from one low-income country. Health policy. 2007;83(2):304–13.

Yi H, Zhang L, Singer K, Rozelle S, Atlas S. Health insurance and catastrophic illness: a report on the new cooperative medical system in rural China. Health Econ. 2009;18(S2):S119–27.

Ilesanmi OS, Adebiyi AO, Fatiregun AA. National health insurance scheme: how protected are households in Oyo state, Nigeria from catastrophic health expenditure? Int J Health Policy Manag. 2014;2(4):175.

Arsenault C, Fournier P, Philibert A, Sissoko K, Coulibaly A, Tourigny C, Traoré M, Dumont A. Emergency obstetric care in Mali: catastrophic spending and its impoverishing effects on households. B World Health Orga. 2013;91(3):207.

Gnawali DP, Pokhrel S, Sié A, Sanon M, De Allegri M, Souares A, Dong H, Sauerborn R. The effect of community-based health insurance on the utilization of modern health care services: evidence from Burkina Faso. Health Policy. 2009;90(2):214–22.

Parmar D, De Allegri M, Savadogo G, Sauerborn R. Do community-based health insurance schemes fulfil the promise of equity? A study from Burkina Faso. Health Policy Plann. 2013;29(1):76–84.

Umeh CA, Feeley FG. Inequitable access to health care by the poor in community-based health insurance programs: a review of studies from low- and middle-income countries. Glob Health Sci Pract. 2017;5(2):299–314.

Adogli K, Pagnan E. Le système de protection sociale en santé au Togo: COPOAMI; 2015. http://www.coopami.org/fr/coopami/formation%20coopami/2015/pdf/2015090306.pdf. Accessed 19 May 2017.

Adisa O. Investigating determinants of catastrophic health spending among poorly insured elderly households in urban Nigeria. Int J Equity Health. 2015;14:79.

Xu K, Jeong HS, Saksena P, Shin JW, Mathauer I, Evans D. World health report. Exploring the thresholds of health expenditure for protection against financial risk. Geneva: World Health Organization; 2010. p. 328–33.

INAM. Genèse-Défis-perspectives: INAM; 2012. Accessed 10 May 2017.

Bakai TA, Ekouevi DK, Takassi OE, Thoma A, Kassankognon Y, Goilibe K. Satisfaction des bénéficiaires de l’Assurance Maladie Obligatoire dans la commune de Lomé (Togo). 2016. http://manifestations.univ-lome.tg/index.php/JSIL2016/jsilul2016/paper/view/222. Accessed 8 Dec 2016.

Kwon S. Thirty years of national health insurance in South Korea: lessons for achieving universal health care coverage. Health Policy Plan. 2009;24(1):63–71.

Richardson E, Roberts B, Sava V, Menon R, Mckee M. Health insurance coverage and health care access in Moldova. Health Policy and Plan. 2011; https://doi.org/10.1093/heapol/czr024.

Sarpong N, Loag W, Fobil J, Meyer CG, Adu-Sarkodie Y, May J, Schwarz NG. National health insurance coverage and socio-economic status in a rural district of Ghana. Tropical Med Int Health. 2010;15(2):191–7.

Schneider P. Why should the poor insure? Theories of decision-making in the context of health insurance. Health Policy and Plan. 2004;19(6):349–55.

USAID. Health financing profile: Togo - African strategies for health. http://www.africanstrategies4health.org/uploads/1/3/5/3/13538666/country_profile_-_togo_-_us_letter.pdf. Accessed 6 Sept 2017.

World Bank. Togo: towards a national social protection policy and strategy. Africa Region: Human Development Department, Social Protection Unit; 2012. https://openknowledge.worldbank.org/handle/10986/19004?show=full. Accessed 6 Sept 2017.

Wright J, Bhuwanee K, Patel F, Holtz J, Van Bastelaer T, Eichler R. Financing of universal health coverage and family planning: a multi regional landscape study and analysis of select west African countries: Togo: United States Agency for International Development; 2017. https://www.hfgproject.org/financing-universal-health-coverage-family-planning-multi-regional-landscape-study-analysis-select-west-african-countries-togo/. Accessed 6 Sept 2017.

O'Donnell O, Van Doorslaer E, Wagstaff A, Lindelow M. Analyzing health equity using household survey data: a guide to techniques and their implementation. Washington, DC: World Bank; 2008. https://openknowledge.worldbank.org/handle/10986/6896. Accessed 8 Dec 2016.

Wagstaff A. Measuring financial protection in health. Washington, DC: World Bank; 2008. http://elibrary.worldbank.org/doi/abs/10.1596/1813-9450 4554. Accessed 14 Jan 2017.

Xu K, Evans DB, Kawabata K, Zeramdini R, Klavus J, Murray C. Household catastrophic health expenditure: a multicountry analysis. Lancet. 2003;362(9378):111–7.

Sun X, Jackson S, Carmichael G, Sleigh AC. Catastrophic medical payment and financial protection in rural China: evidence from the new cooperative medical scheme in Shandong Province. Health Econ. 2009;18:103.

Greene WH. Econometric analysis. 5th ed. New Jersey: Pearson Education; 2003.

Li Y, Wu Q, Xu L, Legge D, Hao Y, Gao L, Ning N, Wang G. Factors affecting catastrophic health expenditure and impoverishment from medical expenses in China: policy implications of universal health insurance. Bull World Health Organ. 2012;90:664–71.

Su TT, Kouyaté B, Flessa S. Catastrophic household expenditure for health care in a low-income society: a study from Nouna District. Burkina Faso Bull World Health Organ. 2006;84(1):21–7.

Xu K, Jeong HS, Saksena P, Shin JW, Mathauer I, Evans D. World health report. Financial risk protection of national health insurance in the Republic of Korea: 1995–2007. Geneva: World Health Organisation; 2010.

Anbari Z, Mohammadbeigi A, Mohammadsalehi N, Ebrazeh A. Health expenditure and catastrophic costs for inpatient and outpatient care in Iran. Int J Prev Med. 2014;5(8):1023.

Gotsadze G, Zoidze A, Rukhadze N. Household catastrophic health expenditure: evidence from Georgia and its policy implications. BMC Health Serv Res. 2009;9(1):69.

Van Minh H, Phuong NT, Saksena P, James CD, Xu K. Financial burden of household out-of pocket health expenditure in Viet Nam: findings from the National Living Standard Survey 2002–2010. Soc Sci Med. 2013;96:258–63.

Abolhallaje M, Hasani SA, Bastani P, Ramezanian M, Kazemian M. Determinants of catastrophic health expenditure in Iran. Iranian journal of public health. 2013;42(Supple1):155.

You X, Kobayashi Y. Determinants of out-of-pocket health expenditure in China. Appl Health Econ Health. 2011;9(1):39–49.

IMF. Togo strategy for boosting growth and promoting employment (SCAPE): IMF country report no. 14/225. Washington, D.C: International Monetary Fund; 2014. https://www.imf.org/external/pubs/ft/scr/2014/cr14224.pdf. Accessed 8 Dec 2016.

Ministère de la santé. Plan National de Développement Sanitaire du Togo 2012–2015. Lomé: Ministère de la Santé; 2012. http://www.who.int/fctc/reporting/party_reports/togo_annex3_national_health_development_plan_2012_2015.pdf. Accessed 16 Mar 2016.

Lwanga SK, Lemeshow S, WHO. Sample size determination in health studies: a practical manual. Geneva: World Health Organisation; 1991.

Barros AJ, Bastos JL, Dâmaso AH. Catastrophic spending on health care in Brazil: private health insurance does not seem to be the solution. Cadernos de saude publica. 2011;27:s254–62.

Knaul FM, Wong R, Arreola-Ornelas H, Méndez O, Bitran R, Capino AC, et al. Household catastrophic health expenditures: a comparative analysis of twelve Latin American and Caribbean countries. Salud Publica Mex. 2011;53:s85–95.

Onwujekwe O, Hanson K, Uzochukwu B. Examining inequities in incidence of catastrophic health expenditures on different healthcare services and health facilities in Nigeria. PLoS One. 2012;7:e40811.

DGSCN. Togo population and housing census 2010. Lomé: DGSCN; 2011. http://www.stat-togo.org/nada/index.php/catalog/2. Accessed 16 Mar 2016.

Ministère de la Santé. Principaux indicateurs de santé 2015. http://www.sante.gouv.tg/sites/default/files/documents/principaux_indicateurs_2015.pdf. Accessed 6 Sept 2017.

Hosmer DW, Lemeshow S. Multiple logistic regression. 2nd ed: Applied Logistic Regression; 2000. p.31-46.

O’Donnell O, van Doorslaer E, Rannan-Eliya R, Somanathan A, Garg CC, Hanvoravongchai P, et al. Explaining the incidence of catastrophic expenditures on health care: comparative evidence from Asia: EQUITAP (5); 2005. www.equitap.org/publications/docs/EquitapWP5.pdf

Devadasan N, Criel B, Van Damme W, Ranson K, Van der Stuyft P. Indian community health insurance schemes provide partial protection against catastrophic health expenditure. BMC Health Serv Res. 2007;7:1.

Hoang VM, Oh J, Tran TA, Tran TG, Ha AD, Luu NH, Nguyen TK. Patterns of health expenditures and financial protections in Vietnam 1992-2012. J Korean Med Sci. 2015;30:S134–8.

Baeza CC, Packard TG. Beyond survival: protecting households from health shocks in Latin America. Washington, DC: The World Bank and Stanford University Press; 2006.

McIntyre D, Thiede M, Dahlgren G, Whitehead M. What are the economic consequences for households of illness and of paying for health care in low-and middle-income country contexts. Soc Sci Med. 2006;62(4):858–65.

Russell S. The economic burden of illness for households in developing countries: a review of studies focusing on malaria, tuberculosis, and human immunodeficiency virus/acquired immunodeficiency syndrome. Am J Trop Med Hyg. 2004;71(2 Suppl):147–55.

Kimani DN, Mugo MG, Kioko UM. Catastrophic health expenditures and impoverishment in Kenya. Eur Sci J. 2016;12(15):434-52.

Berki S. A look at catastrophic medical expenses and the poor. Health Aff. 1986;5(4):138–45.

Merlis M. Family out-of-pocket spending for health services: a continuing source of financial insecurity. New York: Commonwealth Fund; 2002. http://www.commonwealthfund.org/publications/fund-reports/2002/jun/family-out-of-pocket-spending-for-health-services%2D-a-continuing-source-of-financial-insecurity. Accessed 16 Mar 2016.

Waters HR, Anderson GF, Mays J. Measuring financial protection in health in the United States. Health policy. 2004;69(3):339–49.

Brinda EM, Andrés RA, Enemark U. Correlates of out-of-pocket and catastrophic health expenditures in Tanzania: results from a national household survey. BMC Int Health Hum Rights. 2014;14:1.

Mbaye EM, Dumont A, Ridde V, Briand V. « En faire plus, pour gagner plus»: la pratique de la césarienne dans trois contextes d'exemption des paiements au Sénégal. Santé publique. 2011;23(3):207–19.

Haddad S, Ridde V, Bekele Y, Queuille L. Plus les coûts sont subventionnés, plus les femmes du Burkina Faso accouchent dans les centres de santé. Accès financier aux services de santé. 2011; http://www.hha-online.org/hso/financing/knowledge.

Lu C, Chin B, Li G, Murray C. Limitations of methods for measuring out-of-pocket and catastrophic private health expenditures. Bull World Health Organ. 2009;87(3):238–244D.

Acknowledgements

The authors would like to thank the International Development and Research Center (IDRC) and the African Population and Health Research Center (APHRC) for the technical support provided to them during the research work. The authors express their gratitude to their hosting organization, the African Population and Health Research Center.

Funding

No funding was received for the present study.

Availability of data and materials

The data supporting the conclusions of this article are available at the Directorate of Research data repository of the University of Lomé and can be obtained with a written permission.

Author information

Authors and Affiliations

Contributions

EHA designing and planning of study, data collection, data analysis, and manuscript preparation. DA contributed in the data collection, data analysis, and manuscript preparation. Both authors read and approved the final manuscript.

Corresponding author

Ethics declarations

Ethics approval and consent to participate

Ethical approval for the survey was obtained from the Institutional Review Board of the Directorate of Scientific and Technical Research (DRST) of the University of Lomé (Togo) with a certified protocol number 075/MESR/SG/DRST/16. In every household, the interviewer explained the purpose of the questionnaire and study and asked whether the respondent was interested in hearing more and, may be, in participating. If the respondent agreed to participate in the survey, the interviewer collected his written informed consent. A copy of the informed consent is kept for the integrity of the research. The information collected in the survey was solely used for research purposes and never have the name and residence of the respondents been disclosed to a third person.

Consent for publication

Not applicable.

Competing interests

The authors declare that they have no competing interests.

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution, and reproduction in any medium, provided you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. The Creative Commons Public Domain Dedication waiver (http://creativecommons.org/publicdomain/zero/1.0/) applies to the data made available in this article, unless otherwise stated.

About this article

Cite this article

Atake, EH., Amendah, D.D. Porous safety net: catastrophic health expenditure and its determinants among insured households in Togo. BMC Health Serv Res 18, 175 (2018). https://doi.org/10.1186/s12913-018-2974-4

Received:

Accepted:

Published:

DOI: https://doi.org/10.1186/s12913-018-2974-4