Abstract

This study examines the impact of intellectual capital (IC) on the financial performance (FP) of Indian public sector banks (IPSBs) between 2010 and 2021. This paper utilizes the modified value-added intellectual coefficient (MVAIC) approach to measure IC. It employs a panel data estimation approach, specifically the generalized method of moments (GMM), to investigate the connection between IC and the FP of public sector banks in India. The findings indicate that IC, along with its sub-elements of human capital (HC), capital employed (CE), structural capital (SC), and Relational capital (RC) have a notable positive or negative influence on various FP indicators, including return on assets (ROA), return on equity (ROE), return on capital employed (ROCE), earnings per share (EPS), and market performance (Tobin’s Q). Furthermore, the combined IC, as evaluated through the modified value-added intellectual coefficient (MVAIC), has a notable and favorable impact on ROA and ROE. The leverage variable exhibits a negative and significant impact on the financial indicators, indicating that an increase in debt leads to a decrease in the bank’s value. This study aims to assist stakeholders and policymakers in identifying the key elements of IC and determining an appropriate distribution among them to achieve sustainable FP and value generation in Indian IPSBs.

Similar content being viewed by others

Introduction

Due to innovation, improvement, and a consistently changing business environment, the efficient and effective utilization of intangible and tangible assets is essential to organizations’ success and sustainable growth (Khalique et al. 2019). Knowledge-intensive firms consider intellectual capital (IC) to be the most vital strategic asset for assessing and evaluating firm performance. The resource-based theory states that businesses that are in possession of “strategic resources” enjoy significant competitive advantages over those who are not in possession of such resources (Wernerfelt 1984). Currently, the scale of an organization is irrelevant, but effectively and efficiently making use of its resources can improve its profitability and sustainability. Particularly in the service sector, intangible assets such as IC have received immense support and emerged as one essential strategic assets for sustainable competitive advantage (Cohen et al. 2014; Janošević et al. 2013; Khalique et al. 2011). The banking sector is universally acknowledged as one of the country’s most significant service sectors, and its role in economic growth is widely recognized. IC is recognized as one of the banking industry’s most valuable and strategic assets (Mention and Bontis 2013). To understand and measure its impact on organizational success, market, and FP the topic has drawn the interest of both academics and professionals.

IC is often classified as non-tangible assets that have a positive impact on a company’s performance but are not recorded on its balance sheet (Ozkan et al. 2017). The majority of academics acknowledge that evaluating IC pertains to measuring HC, CE, RC, and SC efficiencies when employing a monetary-based approach (Barak and Sharma 2023; Bayraktaroglu et al. 2019; Chowdhury et al. 2018; Kweh et al. 2022; Nazari and Herremans 2007; Pulic 1998, 2004; Smriti and Das 2018; Xu and Wang 2019). Researchers have demonstrated that IC contributes a significant part in improving the overall profitability of businesses. The management of a company will be able to increase the company’s FP if they appropriately manage the IC of the company (Asare et al. 2021; Chowdhury et al. 2018; Inkinen 2015; Khalique et al. 2019; Kweh et al. 2022; Le et al. 2022; Xu and Li 2019).

The transitions from an economy based on manufacturing to a knowledge and digital economy in developed countries highlight the benefits of IC (Forte et al. 2017). Developing nations like India need to draw attention to the vital role of the IC in revolutionizing their economies. This requirement can best be understood by first providing a concise overview of India. In just the past decade and a half, India’s economy has risen from the 10th to the 5th largest on a global scale (Rao et al. 2023). Despite the world economy functioning in an exceedingly unfavorable macroeconomic climate and the COVID-19 effect, the Indian economy is predicted to increase by 7% year on year in the current fiscal 2023–2024. The union budget’s initiatives to boost capital spending on infrastructure development, health, education, support for the green economy, and fortification of financial markets are anticipated to boost employment and speed growth in the economy, as highlighted in the budget 2023–2024. Due to the increasing adoption of digital devices, infrastructure changes, and India’s history of frugal innovation, the speed of development in India’s financial system can grow more rapidly than in other countries.

India is emerging as a South Asian nation with tremendous economic growth and development, with major trade engagements with SAARC nations such as the Preferential trading agreement in 1994 (SAFTA), the ASEAN-India Trade in goods agreement in 2009 (AITGA), the Indo-Sri Lanka free trade agreement in 1998 (ISFTA), and the South Asian free trade agreement in 2004 (SAFTA), the Indo Myanmar border trade agreement in 2009, India’s economy is now highly intertwined with regional and global economies (Sahoo and Sethi 2023). According to the World Competitive Index 2022, India’s economy has risen more dramatically than any other ASEAN member, moving up six places, from 43rd to 37th. India, ranked 7th, has retained its status as one of the top 10 countries worldwide for foreign direct investment, as stated in the World Investment Report released by the United Nations Conference on Trade and Development (UNCTAD) (Kanmony 2023).

India’s banking industry contributes significantly to the country’s overall economic expansion. In the year 2022, the overall value of all assets held within the banking industry reached a new high of 2.67 trillion US dollars. IC constitutes the most vital of all financial organizations. Financial institutions rely heavily on intangible assets like customer and employee connections and other forms of IC. Banks and other financial institutions are sometimes described as “knowledge-intensive” (Buallay et al. 2020). Both academics and industry professionals are particularly concerned about the strategic importance of IC, and they are unanimous in their belief that IC becomes an essential bank asset that influences the long-term performance of banks (Mondal and Ghosh 2012). The academic community has a few studies on IC in the banking industry. As a result, it is essential to investigate the relationship between IC and banks’ FP.

This research seeks to address the shortcomings in the existing literature about the ongoing discussions surrounding the impacts of MVAIC, its constituents, and FP, which have shown mixed results. We utilize the MVAIC model to assess the IC performance of 23 public sector banks operating in India from 2010 to 2021. Next, we analyze the linkage between IC and financial success to identify the components that have the greatest impact on profitability in India.

This study enhances the existing body of understanding by offering insights into the assessment of IC performance in the Indian banking industry. Additionally, it identifies the potential impact of IC on the FP of banks following the merger decisions made by the Indian government. This research further enhances the existing body of research on the factors that influence the profitability of banks. It not only enhances the profitability of banks but also aids policymakers in achieving their financial stability objectives. To address potential issues of endogeneity and account for the volatile nature of banking revenues, we utilize the generalized method of moments (GMM) model. This approach, which has not been extensively employed in previous studies, ensures the reliability and robustness of our estimation results.

With little prior research on the topic, this study fills a gap by analyzing the IC management and assessment practices of Indian public sector banks. The results of the unbalanced panel data analysis, conducted using the generalized method of moments (GMM), and accounting for potential heteroscedasticity and endogeneity difficulties in the variables, demonstrate that the combined intellectual capital (MVAIC) is positively and significantly associated with the financial performance indicators. Among the components of IC, human capital (HC) shows a particularly strong positive association. Therefore, it is essential to provide consideration to the HC through efficient management.

The subsequent sections of this work are organized as follows: following the introduction, the “Literature review” provides a comprehensive assessment of the intellectual literature. The “Research methodology” section outlines the research methodology. The “Empirical results and analysis” and “Discussion” sections, respectively, include information on the empirical findings, analysis, and discussion and encompass the consequences and limitations of the research.

Literature review

Understanding and assessing intellectual capital (IC)

The ability of a company to develop, utilize, and evaluate its intangible resources to generate value is referred to as IC. This capability helps in the expansion of the company’s operations and performance (Dean and Kretschmer 2007). Many academics agree that the term “intellectual capital” is utilized in a variety of contexts to denote intangible resources in a variety of ways. According to Ruckdeschel (1998), IC is an intangible value created for people and resources. The total amount of information a firm may utilize to run a business and generate value for itself is known as IC (Zeghal and Maaloul 2010).

IC is defined as “intellectual resources, knowledge, expertise, assets, and information that can be used to create value,” according to (Dumay et al. 2015). The dynamic component of IC is reflected in the competitive advantages of the company that result either from the knowledge-based assets or the manner they are produced (Pirozzi and Ferulano 2016). The most revealing indicator of IC lies in the difference between a company’s book value and its market value (Maditinos et al. 2011).

Intellectual capital and its elements

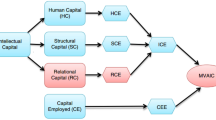

Clearly, IC is best understood as knowledge captured in an understandable form that can be used by organizations to generate value. IC is a collection of knowledge-based intangible resources that a company possesses and can manage effectively to gain a competitive advantage. Academicians typically divide the term “IC” into four categories: “human capital,” “capital employed,” “structural capital,” and “relational capital” to define it more clearly (Cohen et al. 2014; Kapoor and Saihjpal 2022; Smriti and Das 2018; St-Pierre and Audet 2011; Weqar et al. 2020; Xu and Wang 2019).

Human capital (HC) is acknowledged as the key component of IC and consists of the knowledge, talent, expertise, abilities, education, and talents of an organization’s personnel that can enhance the performance of the organization (Cohen et al. 2014; Mention and Bontis 2013; Weqar et al. 2020; Zheng et al. 2022). IC relates to the capability to solve problems creatively, although a personnel education and skillset are the primary determinants of their competency (Meles et al. 2016). Employees contribute significantly to building and maintaining a competitive advantage (Rowlands 2018). Effective human resource management strategies directly impact HC development because they influence employee skill sets.

Structural capital (SC) supports human resources to leverage its knowledge. SC primarily encompasses organizational culture and infrastructure. SC is held by the corporation which includes strategies, information systems and datasets, structures, routines, methods, and procedures that support operations, innovation, and organizational efficiency (Cohen et al. 2014; Meles et al. 2016; Mention and Bontis 2013; Sardo and Serrasqueiro 2017). The capacity of an organization to communicate with its stakeholders (such as government, rival businesses, clients, trade groups, and suppliers) and the knowledge ingrained in these connections are referred to as relational capital (RC) (Cohen et al. 2014; Inkinen 2015; Mention and Bontis 2013; Sardo and Serrasqueiro 2017). In general, a corporation needs to maintain RC, over time to strengthen its connections with its stakeholders to approach new resources (Meles et al. 2016). The capital employed (CE) metric measures the output produced by a corporation for each monetary unit spent on manpower (Xu and Wang 2019). CE is referred to as the efficiency of both financial and physical resources (Poh et al. 2018).

Several models are created to assess IC. The following is a list of these techniques. Intangible Assets Monitor (Sveiby 1997), value-added intellectual coefficient (Pulic 1998, 2000), modified value-added intellectual coefficient (Ulum 2015), Tobin’s Q (Mourtisen et al. 2012), Balanced Scorecard (Kaplan et al. 1996), Skandia Navigator (Edvinsson and Malone 1997), Technology broker (Annie 1996), Economic value added and market value added (Chen Goh 2005a). The VAIC model is used by the majority of researchers in comparison to alternative IC assessments due to its accessibility, which enables efficient comparison across companies or nations (Chen Goh 2005a; Kapoor and Saihjpal 2022; Kasoga 2020; Le et al. 2022; Phusavat et al. 2011; Poh et al. 2018; Pulic 2004; Sardo and Serrasqueiro 2017; Soewarno and Tjahjadi 2020; Tran and Vo 2020). The VAIC model has drawbacks, such as ignoring RC and innovation capital, major elements of IC. So, in this article, we employed the MVAIC methodology to evaluate the effectiveness of IC because it is essential for a corporation to have better stakeholder relations given the intense market competition (Aybars and Oner 2022; Buallay et al. 2019, 2020; Montequín et al. 2006; Pal and Soriya 2012; Tiwari and Vidyarthi 2018; Tran and Vo 2020; Weqar et al. 2020; Xu and Wang 2019).

Intellectual capital and firm’s performance

The performance of banks is crucial for the economy as it catalyzes economic growth (Mohapatra et al. 2019). Initially, research on the relationship between IC and FP was primarily conducted in developed economies. However, there has been a significant increase in studies from emerging economies. Corporations now recognize the significance of investing in knowledge and IC to uphold and enhance their performance. Knowledge assets are crucial resources for achieving corporate success. The word “IC” commonly refers to intellectual assets, which are widely recognized as a crucial source of strategic advantage and value generation (Smriti and Das 2018).

Multiple empirical investigations have consistently found strong evidence of a positive relationship between IC and FP (Alhassan and Asare 2016; Anifowose et al. 2018; Dzenopoljac et al. 2017; Gupta and Raman 2021; Hamdan 2018; Innayah et al. 2020; Joshi et al. 2013; Meles et al. 2016; Nadeem et al. 2018; Oppong et al. 2019; Vishnu and Kumar Gupta 2014). Furthermore, other studies fail to demonstrate a significant association between the dependent and independent variables (Barathi Kamath 2007; Chu et al. 2011; Firer and Mitchell Williams 2003; Maditinos et al. 2011; Mehralian et al. 2012).

Additionally, it has been observed that not every aspect of IC holds the same level of importance in determining the organization’s performance (Bontis 1998). The studies conducted in different countries (Adesina 2019; Alipour 2012; Buallay et al. 2019; Chen Goh 2005a, b; Chen 2012; Forte et al. 2017; Hamdan 2018; Joshi et al. 2013; Le et al. 2022; Nadeem et al. 2018; Poh et al. 2018; Sardo and Serrasqueiro 2017; Ting et al. 2021; Tiwari and Vidyarthi 2018; Tran and Vo 2018; Vishnu and Kumar Gupta 2014; Weqar et al. 2020) demonstrate that HC and SC are the predominant and significant constituents of IC that impact FP.

Furthermore, additional studies investigating the impact of combined IC (MVAIC) on FP. Vishnu and Kumar Gupta (2014) and Maji and Goswami (2017) provide proof demonstrating a strong association between IC-MVAIC and firm performance in India. In their study, Farooque et al. (2023) investigated the association between IC-MVAIC and the FP of Islamic and conventional banks listed in GCC nations. They discovered that MVAIC is more effective in improving the profitability metrics of conventional banks compared to VAIC in Islamic banks. Xu and Liu (2020) and Tran and Vo (2020a) demonstrate that IC-MVAIC has a favorable impact on accounting-based firm performance in the South Korea and Vietnam markets, respectively. According to Bayraktaroglu et al. (2019), the different elements of IC efficiency play a moderating function in the connection between CE efficiency and profitability. Nimtrakoon (2015) demonstrates that IC-MVAIC has a favorable impact on business efficiency in various Asian nations. In a study conducted by Xu and Li (2019), it was found that there is a significant association between the IC-MVAIC and the accounting-based performance of both non-high-tech and high-tech companies in China. The study conducted by Zheng et al. (2022) suggests that enhancing IC efficiency has a beneficial impact on bank performance in Bangladesh.

It is recognized that there have been few studies conducted to investigate the impact of IC on the FP of the Indian banking industry. Many articles commonly employ a straightforward regression method to quantify the causal impact of IC on FP (Al-Musali and Ismail 2014; Weqar et al. 2021). Nevertheless, we employ an alternative methodology, namely GMM, to address the issues of endogeneity and account for the dynamic characteristics of bank earnings. This study has also encompassed the COVID-19 period, potentially shedding light on the impact of the pandemic on the FP of banks.

Research methodology

Data collection

The current research aims to explore the role of IC in the FP of Indian public sector banks (IPSBs). The data for IPSBs was compiled using financial statements from their annual reports and ProwessIQ, a database maintained by the Centre for Monitoring the Indian Economy (CMIE). Unbalanced panel data for the period 2010–2021 was collected from 23 banks (before and after the merger of banks) of public sector banks. After extracting all necessary data from “ProwessIQ,” it was discovered that several observations were missing. The yearly reports of the banks were searched manually to find the missing data. Banks were removed from the dataset that had missing values that could not be located even from annual reports.

Research methodology

To assess the impact of IC on FP, some scholars (Kasoga 2020; Meles et al. 2016; Isanzu 2015; Nawaz and Haniffa 2017) have employed the value-added intellectual coefficient (HC, SC, and CE) as proposed by Pulic (1998). Nevertheless, the VAIC model does have certain limitations. To address these limitations, the researchers devised the MVAIC framework, which incorporates a supplementary component of IC, referred to as Relational Capital (RC). RC encompasses a company’s interactions with various stakeholders, such as customers, vendor partners, creditors, shareholders, and marketing distributors. So in this research, the MVAIC technique (Bayraktaroglu et al. 2019; Buallay et al. 2020; Tran and Vo 2018; Weqar et al. 2020; Xu and Li 2019) is used to determine the effect of IC on FP. Capital employed efficiency (CEE), Human capital efficiency (HCE), relational capital efficiency (RCE), and structural capital efficiency (SCE) are the four independent variables used to describe the elements of IC and two control factors (firm size and leverage) have been used. Five dependent variables return on asset (ROA), return on equity (ROE), market performance (Tobin’s Q) or (TQ), earnings per share (EPS), and return on capital employed (ROCE), are employed as indicators of FP. Data of different elements of IC, dependent variables, and control variables have been collected from 2010 to 2021. Data series of different aforesaid variables are arranged into a balanced panel data format. The first stage of the estimate examines how each dependent variable is affected by the different components of IC (HC, CE, SC, and RC). The different elements of IC have also been used to examine the combined effect of IC (measured through MVAIC) on the FP of IPSBs. Initially, the values from descriptive statistics and the matrix of correlation between variables are calculated to comprehend the relationship and nature among the variables. Later, to check the stationarity of data, various panel unit root techniques are employed. First, stationary is checked at a level and then at first difference. The data series of multiple variables are stationary at first difference. Accordingly, we convert the data series of all the dependent, independent, and control variables into the first difference. The generalized method of moments (GMM) (Arellano and Bond 1991) is employed in this study to analyze how IC affects public sector banks’ FP.

Measurement of variables

Classification of intellectual capital

This research employs the MVAIC approach, which has been extensively utilized in prior empirical investigations for evaluating IC (Aybars and Oner 2022; Buallay et al. 2019; Tran and Vo 2020; Vidyarthi 2019; Weqar et al. 2020; Xu and Wang 2019). MVAIC is a combination of four performance variables. MVAIC has been calculated using the formula:

where HCE is the marginal impact of every unit of HC to value-added; SCE is the share of SC to generating value; CEE is the marginal contributions of every unit of monetary and physical capital to value-added; and RCE is the role of RC in generating value. The four elements of MVAIC have been calculated in the following order: HCE, SCE CEE, and RCE:

where VA is the value-added. VA is classified as the Operating profit plus employees’ cost, Depreciation, and Amortization. HC signifies total personnel expenditure. SC is computed by subtracting HC from VA. Both monetary and physical capital are denoted by CE. Marketing, sales, and advertising costs are used to calculate RC.

Dependent variables

This research applies return on assets (ROA), return on capital employed (ROCE), return on equity (ROE), market performance (Tobin’s Q or TQ), and earnings price per share (EPS) as proxies for banks’ financial performance indicators. To construct the model for this research, we first looked at other studies that had been done previously (Aybars and Oner 2022; Barak and Sharma 2023; Buallay et al. 2019; Kapoor and Saihjpal 2022; Kasoga 2020; Tran and Vo 2020; Weqar et al. 2020; Xu et al. 2020; Zheng et al. 2022):

Control variables

Leverage, which can be determined as the ratio of total outside liabilities to total assets, and Size, which can be approximated as the log of total assets, are used as proxies for bank characteristics. These two control factors were chosen because of their significant contributions to the company’s overall performance (Aybars and Oner 2022; Buallay et al. 2019; Kapoor and Saihjpal 2022; Weqar et al. 2020; Xu and Wang 2019).

Generalized method of moments (GMM) estimation

Regarding the valuation technique, most studies employ a straightforward regression technique to quantify the causal impact of IC on FP. For instance, Weqar et al. (2020) employ multiple linear regression analysis to examine the relationship between ROE, ROA, and ATO as dependent variables, and various components of VAIC. In a similar manner, Poh et al. (2018) utilize linear regression analysis to quantify the correlation between VAIC, its constituent elements, and FP. Nevertheless, the possible issue of endogeneity, as previously stated, might lead to biased and inconsistent estimation findings when using ordinary least squares (OLS). Therefore, Xu et al. (2023) employ a fixed-effects model to account for bank-specific variables at the individual level. While a fixed-effects model effectively manages unchanging unobserved traits, it is unable to account for variables that vary over time (Allison 2009). It is contended that this approach can generate a reliable estimation when we assume no association between unique errors and independent variables. Nevertheless, this assumption may be invalidated by time-varying unobservable factors (such as sudden financial stress) or reverse causality (where MVAIC influences financial success). In this research, we utilized the two-step GMM estimation technique, considering potential endogeneity issues.

The OLS estimation method, which assumes ni to be unrecognized and the existence of a correlation between predictor variables and unobservable characteristics (ni), remained biased in the presence of firm-specific effects (Hsiao 1985). If an error term (εit) is serially uncorrelated then the instrumental variable estimate method gives reliable findings. Arellano and Bond (1991) suggest the generalized method of the moment (GMM), assuming that the error term is serially uncorrelated. Within the group of instrumental variable estimators, GMM is the most effective technique (Honore and Hu 2004). Numerous earlier studies have found that two-step GMM is more effective than one-step estimation when the disturbances are anticipated to exhibit heteroscedasticity in big sample data with a reasonably long period (Arellano and Bond 1991; Blundell and Bond 2023).

The success of GMM estimation, however, is dependent on a few presumptions, including the validity of the other predictor variables and the lagged value of the dependent variable, as well as the absence of autocorrelation in the model’s error term. Arellano and Bond (1991) suggested three steps to achieve this. The first step is to determine whether the error component of the suggested model exhibits any autocorrelation. The test statistic has a conventional normal distribution under the null hypothesis that there is no serial connection. The second is to ensure that the error term in the GMM model is distributed as a standard normal under the null hypothesis of no serial correlation, and should not exhibit second-order autocorrelation. The third is the Sargan (1958) test for over-identifying limitations, sometimes known as J statistics. Under the null hypothesis of instrument validity, this evaluates the validity of the instruments and asymptotically distributed as Chi-square.

We propose five models to study the unique influence of each element of IC on each dependent variable. The following is the model equation:

The following are the GMM equations to investigate the combined effect of IC (MVAIC) on the FP of public sector banks:

where ROAit, ROEit, EPSit, TQit, and ROCEit are the different measures of profitability of IPSBs, it in year, εit is the error term, ni is the unrecognized firm-specific effects and nt is the time-specific effects. The variables remaining in the equations represent the various IC measures used as explanatory variables. MVAIC reflect the combined effect of different component of IC.

Empirical results and analysis

Table 1 summarizes the descriptive statistics for all dependent and independent variables. The value produced by HCE is 1.888 out of the four IC elements with the greatest mean value. When compared to the other components, the HCE makes up the majority of the average MVAIC value of 3.672. The average value of the three non-physical elements (HCE, RCE, and SCE) combined is 3.547, which is much higher than the average value of CEE, which is 0.128. This distinction suggests that non-physical assets create higher value creation for IPSBs than tangible ones. Similar outcomes were observed in earlier research (Ahmed et al. 2022; Alipour 2012; Kapoor and Saihjpal 2022; Maditinos et al. 2011; Mehralian et al. 2012; Vergauwen et al. 2007). The dependent variable’s EPS had a higher mean value, 18.919, indicating that banks are profitable and in a strong financial position. Following that, ROCE had a mean value of 1.391. Since TQ in this instance is less than 1, it can be assumed that the bank’s market value is lower than its book value. As a result, if the stock market value of the capital is lower than the book value, then replacing the capital will not be a prudent step as it would only result in its deterioration. The results of the Kasoga (2020) investigation are similar to this finding. Following it was ROE, with an average of 0.645, and ROA, with a low average of 0.074, indicating more assets used to produce a profit.

Karl Pearson’s method was adopted to perform correlation analysis shown in Table 2. None of the coefficients have a value of greater than 0.9, and significant association is absent in the sample (Field 2013; Hair et al. 2013; Pallant 2010; Tabachnick et al. 2013). Multicollinearity hence does not affect the estimation variables. The independent variables HCE, CEE, RCE, and MVAIC are positively correlated with the dependent variables ROA, TQ, and ROE. Whereas SCE has negatively correlated with ROA, ROE, TQ, and ROCE but is weakly positively related to EPS. The dependent variable ROCE is negatively correlated with the CEE, HCE, SCE, and MVAIC but positive association with RCE.

Unit root test

Using unit root tests we utilized the tests proposed by Levin et al. (2002) (LLC) in addition to two sets of Fisher-type tests employing ADF and Phillips-Perron (PP) as given by Choi (2001) and Maddala and Wu (1999).

Hypothesis (H0). There is a unit root, and the different variables’ data series are not stationary.

Hypothesis (H1). There is no unit root, and the different variables’ data series are stationary.

The results of a panel unit test with five dependent, five independent, and two control variables are displayed in Table 3. The findings show that every variable is stationary at the first difference. We accept the alternative hypothesis as all the variables are stationary at first difference. Therefore, the null hypothesis is rejected as the variables are not stationary.

Empirical results using the generalized moments method

The results of GMM estimation using the five dependent variables and different components of IC as independent variables are presented in Table 4. The outcome of ROA reflects that the lagged value of a dependent variable significantly affects the dependent variable. The components of IC, namely, capital employed efficiency (CEE), and structural capital Efficiency (SCE) are observed to be significant at a 1% level (p value < 0.05) and demonstrate a negative association with ROA (Mohapatra et al. 2019; Muhammad and Ismail 2009; Sardo and Serrasqueiro 2017; Ting et al. 2021). The leverage, a control variable, has shown a significant value. The negative association between CEE, SCE, and ROA indicates that IPSBs are not operating efficiently. However, human capital efficiency (HCE) and ROA reflect a positive significant relationship (Adesina 2019; Buallay et al. 2019; Forte et al. 2017; Le et al. 2022; Sardo and Serrasqueiro 2017; Ting et al. 2021; Tran and Vo 2018; Weqar et al. 2020; Xu et al. 2020). The findings contradict those of Firer and Mitchell Williams (2003) and Kasoga (2020) who discovered that HCE had a negative effect on the FP of organizations. In this instance, the lagging value of the dependent variable is statistically significant. Significant first-order correlation indicates serial correlation or autocorrelation in the model. However, second-order correlation is not substantial, indicating that autocorrelation is not a problem. The Sargan test (p value > 0.05) indicates the validity of instruments and they are uncorrelated with residual. The first model is a suitable fit for examining the effect of IC on ROA.

In the second model, ROE is a dependent variable. Just like the previous model, the lag value of ROE is found to be a significant determinant of ROE. The variables, namely, CEE, and SCE, the components of IC, exhibit a negative significant effect on ROE. Contrary, the HCE reflects a positive significant effect on ROE (Buallay et al. 2020; Sardo and Serrasqueiro 2017; Tran and Vo 2018; Xu et al. 2020; Xu and Wang 2019). The p value > 0.05 of the Sargan test reflects that the instruments used in the study are valid and uncorrelated with error terms. This model’s first-order correlation indicates that autocorrelation is not an issue (p value > 0.05).

The third model deals with EPS as the dependent variable; the empirical findings of this model are like the earlier two models in that CEE and SCE reflect a substantial negative effect on EPS. The HCE depicts the positive significant effect on EPS. But then, relational capital efficiency (RCE) is a new significant determinant of EPS (p ≤ 0.05). The lag value of EPS is also a significant determinant of EPS.

In the fourth model Tobin’s Q (TQ), the variables CEE and HCE are the significant determinants of dependent variables along with the lag value of TQ. In this model, CEE has a positive association with TQ (Kapoor and Saihjpal, 2022) but HCE has a negative correlation with TQ (Dzenopoljac et al. 2017; Kapoor and Saihjpal 2022; Kasoga 2020). This suggests that the market value of the bank over time is favorably influenced by the CEE whereas, HCE influences negatively. In the last model, HCE and RCE demonstrate a positive significant effect on ROCE. In contrast, CEE, and SCE, along with the lag of ROCE, reflect a substantial negative effect on ROCE. Since the values of the Sargan test in both models are 21.227 and 17.564, respectively, and the p value is more than 0.05, we cannot reject the null hypothesis, showing that the instruments are valid and uncorrelated with residual. In the fourth model, the first-order and second-order correlations are insignificant, and serial correlation is not an issue. Similarly, the second-order correlation in the final model is not significant.

Table 5 displayed the combined effect of IC and lag of own dependent variables on the different dependent variables. Modified value-added intellectual capital (MVAIC) positively impacts ROA (Buallay et al. 2020; Weqar et al. 2020; Xu and Wang 2019), ROE (Buallay et al. 2020), EPS, and ROCE. This indicates that IC makes an important contribution to the improvement of bank performance and the creation of value for IPSBs. In contrast, the MVAIC negatively affects TQ. Leverage of a control variable reflects the negative significant impact on all five dependent variables (ROA, ROE, EPS, TQ, and ROCE). In all five models, the p value associated with the Sargan test or J statistics is greater than 0.05. It means all five models meet the conditions over identified restrictions. This also means that all the variables, including the lag of their variables, are valid instruments and uncorrelated with the error term. As the corresponding p value is greater than 0.05, there is no issue with the first-order and second-order correlation in the case of TQ and ROCE. The first-order correlation in the case of ROA is serially correlated with the error term, however, the second-order correlation is not serially associated with the error term and there is no serial correlation. Similarly, in the case of ROE and EPS, there is no second-order serial. Overall, we can conclude that IC has a substantial positive influence on public sector banks and that all the generated models are accurate predictors of the FP of Indian PSBs.

Discussion

Underpinned by the GMM estimation the current study aims to examine the role of intellectual capital (IC) on the financial performance (FP) of Indian public sector banks (IPSBs). The study used the MVAIC model using four elements of IC, these elements are capital employed (CE), human capital (HC), structural capital (SC), and relational capital (RC). These proxies are employed to represent different elements of IC. The different indicators have been used to represent the financial performance. These five FP parameters are utilized as dependent variables, they are return on assets (ROA), return on equity (ROE), return on capital employed (ROCE), Tobin’s Q (TQ), and Earning price per share (EPS). The study also used two control variables leverage and size. The data of all variables have been collected for the period 2010 to 2021. Initially, descriptive statistics and a matrix of correlation coefficients of different factors are computed to know the nature of the data and the existence of a problem of multicollinearity. Later stationarity of different variables is examined using the unit root techniques. First, the stationarity of all variables is investigated at a level. Since none of the variables is observed to be stationary at level. So, on examining the first difference the data series of all the variables are found to be stationary. Accordingly, the data series of multiple variables are converted into the first difference. Later GMM technique is applied to examine the effect of IC on the FP of Indian public sector banks. GMM estimation is preferred over linear panel least square (Anifowose et al. 2018; Farooque et al. 2023; Tiwari and Vidyarthi 2018; Zheng et al. 2022). As GMM techniques remove the problem of endogeneity. In the GMM technique lag of the dependent variable is used as an independent variable along with other independent variables. According to the GMM technique, there is a need to fulfill certain assumptions. These assumptions are the lag of the dependent variable should be a significant variable along with other independent variables. All the instruments should be valid and should not be correlated with residuals. There should not be a problem of first-order and second-order autocorrelation.

The results of this study indicate that the HCE is the primary driver of financial performance in Indian public sector banks, which is consistent with other studies (Adesina 2019; Nadeem et al. 2018; Ting et al. 2021; Weqar et al. 2021) but not in line with the result (Rehman et al. 2022). This is because the nation is still developing and its banking system is not fully established. The finding demonstrates that the development of HC is essential to the banks’ ability to expand sustainably. A corporation with strong human resources would perform better and be more creative and innovative. FP was negatively impacted by SCE and CEE, although market performance (TQ) showed a statistically significant and favorable association with CEE. According to studies by Ozkan et al. (2017) and Ginesti et al. (2018), there is a strong and negative relationship between CEE and SCE and financial performance metrics. However, market performance (TQ) has a statistically significant and positive association with CEE.

The inverse correlation between CEE and SCE and the financial performance metrics highlights the necessity for Indian public sector banks to prioritize the physical capital invested in the banks and strive to decrease their non-performing assets. Banks should also monitor their strategies, operations, procedures, and organizational efficiency to improve the bank’s profitability. In contrast, RCE shows a negative and strong correlation with EPS and a negligible relationship with all other financial performance metrics, except for ROCE. Lastly, we examined the impact of the control variables on financial performance and discovered that financial leverage has a considerable negative impact while size has a positive impact. As leverage or debt capital is increased it leads to a decline in the profitability of the public sector banks.

The overall impact of IC (MVAIC) has been shown to have a substantial positive influence on financial performance metrics, as evidenced by the studies conducted by Maji and Goswami (2017), Nimtrakoon (2015), Tran and Vo (2020), Vishnu and Kumar Gupta (2014), Xu et al. (2020) and Zheng et al. (2022). The results indicate that allocating resources to IC has a positive effect on the financial outcomes of Indian public sector banks. Leverage again shows a negative significant impact on financial performance. This may be due to the increase in debt enhancing the interest expenses. Moreover, financial risk also increases as we use more amount of debt capital. All the models developed using GMM reflect the good fit model. All the models fulfill the condition of a good fit model. J-statistic or Sargan test value is significant in all the cases which means all the models fulfill the over-identifying condition and the instruments used in the model are valid and not correlated with error terms.

Practical implications

The current study should have relevance for different stakeholders including the banking authorities, the government, society, and other stakeholders. Enhancing the profitability of IPSBs is a great challenge for banking authorities as well as for the government. This study highlights that CEE and SCE have a negative impact on profitability. There is a need to pay attention, to why CEE has a negative impact on profitability. It may be due to more proportion of debt capital in capital employed. There is a need to put a cap on debt capital to enhance financial performance. Similarly, the SCE also demonstrates the negative impact, there is also a need to reassess the investment made in infrastructure and cost involvement in strategy formulation.

The HCE has a substantial positive effect on FP. Government and banking authorities are urged to increase their investment in personnel training and development, skills, and expertise of their personnel to improve operational performance. The combined effect of IC shows a positive significant impact on different measures of FP metrics. It implies that policymakers are recommended to increase investment in the IC to maximize profits. The article also indicates that efficient administration of IC resources mitigates the adverse effects of detrimental shocks induced by crises such as the COVID-19 pandemic.

Societal implications

The study’s conclusions provide significant advantages for society. When Indian banking institutions possess high-quality infrastructure and technology, society will experience several advantages such as superior financial services, innovative banking initiatives, reduced borrowing costs, efficient resource utilization, economic expansion, and enhanced quality of life.

Theoretical implications

An analysis was conducted to carefully examine the contribution of this research to the existing knowledge database. The aim was to determine the relationship between financial success and IC. This enabled the Indian public sector banks to boost their IC, serving as a benchmark for maintaining a competitive and knowledge-driven environment. Bank authorities should enhance their efforts to ensure the inclusion of banks’ IC in their financial reports. This created knowledge is widely thought to assist academics and scholars in identifying the suitable measures of intellectual capital that serve as more accurate forecasters of value creation and an organization’s growth.

Implications for future researchers

Despite making every effort to conduct a thorough investigation in this research, it is not practicable to evaluate all the contributing aspects. Recognizing the constraints of the present research is crucial to propose additional research. The primary objective of this study was to investigate the impact of intellectual capital on the financial performance of Indian public sector banks. Firstly, the investigation solely encompassed banks that are owned by the government. Subsequent investigation could prioritize the examination of international and local rural, cooperative banks, payment, and small finance institutions. Secondly, this study just focuses only on the banking sector. Further research can explore other industries as well to validate the impact of intellectual capital on a company’s performance. Thirdly, future researchers may have the capability to integrate additional financial parameters that are pertinent to banks to undertake comprehensive analyses of intellectual capital and financial performance. Fourthly, this study employed the MVAIC approach to assess the efficacy of IC, thereby paving the way for future investigations to explore alternative methodologies such as the national IC index, the intangible assets monitor, the balanced scorecard, the technology broker, and the value-added intellectual coefficient (VAIC).

Data availability

The datasets used and analyzed in this study are disclosed in the paper.

References

Adesina KS (2019) Bank technical, allocative and cost efficiencies in Africa: the influence of intellectual capital. North Am J Econ Financ 48:419–433

Ahmed Z, Hussin MRA, Pirzada K (2022) The impact of intellectual capital and ownership structure on firm performance. J Risk Financ Manag 15(12):553

Alhassan AL, Asare N (2016) Intellectual capital and bank productivity in emerging markets: evidence from Ghana. Manag Decis 54(3):589–609

Alipour M (2012) The effect of intellectual capital on firm performance: an investigation of Iran insurance companies. Meas Bus Excell 16(1):53–66

Allison PD (2009) Fixed effects regression models. SAGE Publications, Los Angeles, CA

Al-Musali MAK, Ismail KNIK (2014) Intellectual capital and its effect on financial performance of banks: evidence from Saudi Arabia. Procedia Soc Behav Sci 164:201–207. https://doi.org/10.1016/j.sbspro.2014.11.068

Anifowose M, Abdul Rashid HM, Annuar HA, Ibrahim H (2018) Intellectual capital efficiency and corporate book value: evidence from Nigerian economy. J Intellect Cap 19(3):644–668. https://doi.org/10.1108/JIC-09-2016-0091

Annie B (1996) Intellectual capital, core asset for the third Millennium enterprise, vol 1. International Thompson Business Press, London, pp 19–33

Arellano M, Bond S (1991) Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. Rev Econ Stud 58(2):277–297

Asare N, Laryea MM, Onumah JM, Asamoah ME (2021) Intellectual capital and asset quality in an emerging banking market. Asian J Account Res 6(1):55–68. https://doi.org/10.1108/AJAR-05-2020-0034

Aybars A, Oner M (2022) The impact of intellectual capital on firm performance and value: an application of MVAIC on firms listed in Borsa Istanbul. Gazi J Econ Bus 8(1). https://doi.org/10.30855/gjeb.2022.8.1.004

Barak M, Sharma RK (2023) Investigating the impact of intellectual capital on the sustainable financial performance of private sector banks in India. Sustainability 15(2):1451. https://doi.org/10.3390/su15021451

Barathi Kamath G (2007) The intellectual capital performance of the Indian banking sector. J Intellect Cap 8(1):96–123. https://doi.org/10.1108/14691930710715088

Bayraktaroglu AE, Calisir F, Baskak M (2019) Intellectual capital and firm performance: an extended VAIC model. J Intellect Cap 20(3):406–425. https://doi.org/10.1108/JIC-12-2017-0184

Blundell R, Bond S (2023) Initial conditions and Blundell–Bond estimators. J Econ 234:101–110

Bontis N (1998) Intellectual capital: an exploratory study that develops measures and models. Manag Decis 36(2):63–76

Buallay A, Cummings R, Hamdan A (2019) Intellectual capital efficiency and bank’s performance: a comparative study after the global financial crisis. Pac Account Rev 31(4):672–694. https://doi.org/10.1108/PAR-04-2019-0039

Buallay A, Hamdan AM, Reyad S, Badawi S, Madbouly A (2020) The efficiency of GCC banks: the role of intellectual capital. Eur Bus Rev 32(3):383–404

Chen Goh P (2005a) Intellectual capital performance of commercial banks in Malaysia. J Intellect Cap 6(3):385–396. https://doi.org/10.1108/14691930510611120

Chen Goh P (2005b) Intellectual capital performance of commercial banks in Malaysia. J Intellect Cap 6(3):385–396

Chen L (2012) A mixed methods study investigating intangibles in the banking sector [PhD Thesis]. University of Glasgow

Choi I (2001) Unit root tests for panel data. J Int Money Financ 20(2):249–272. https://doi.org/10.1016/S0261-5606(00)00048-6

Chowdhury LAM, Rana T, Akter M, Hoque M(2018) Impact of intellectual capital on financial performance: evidence from the Bangladeshi textile sector. J Account Organ Change 14(4):429–454

Chu SKW, Chan KH, Yu KY, Ng HT, Wong WK (2011) An empirical study of the impact of intellectual capital on business performance. J Inf Knowl Manag 10(01):11–21. https://doi.org/10.1142/S0219649211002791

Cohen S, Naoum V-C, Vlismas O (2014) Intellectual capital, strategy and financial crisis from a SMEs perspective. J Intellect Cap 15(2):294–315

Dean A, Kretschmer M (2007) Can ideas be capital? Factors of production in the postindustrial economy: a review and critique. Acad Manag Rev 32(2):573–594

Dumay J, Guthrie J, Puntillo P (2015) IC and public sector: a structured literature review. J Intellect Cap 16(2):267–284

Dzenopoljac V, Yaacoub C, Elkanj N, Bontis N (2017) Impact of intellectual capital on corporate performance: evidence from the Arab region. J Intellect Cap 18(4):884–903

Edvinsson L, Malone M (1997) Intellectual capital. Harper Business, New York, NY

Farooque OA, AlObaid ROH, Khan AA (2023) Does intellectual capital in Islamic banks outperform conventional banks? Evidence from GCC countries. Asian Rev Account. https://doi.org/10.1108/ARA-12-2022-0298

Field A (2013) Discovering statistics using IBM SPSS statistics, (4th ed). SAGE, London

Firer S, Mitchell Williams S (2003) Intellectual capital and traditional measures of corporate performance. J Intellect Cap 4(3):348–360. https://doi.org/10.1108/14691930310487806

Forte W, Tucker J, Matonti G, Nicolò G (2017) Measuring the intellectual capital of Italian listed companies. J Intellect Cap 18(4):710–732

Ginesti G, Caldarelli A, Zampella A (2018) Exploring the impact of intellectual capital on company reputation and performance. J Intellect Cap 19(5):915–934

Gupta K, Raman T (2021) The nexus of intellectual capital and operational efficiency: the case of Indian financial system. J Bus Econ 91(3):283–302

Hair JF, Black WC, Babin BJ, Anderson RE (2013) Multivariate data analysis. Always learning. Pearson Education Limited, London, UK

Hamdan A (2018) Intellectual capital and firm performance: differentiating between accounting-based and market-based performance. Int J Islam Middle East Finance Manag 11(1):139–151

Honore BE, Hu L (2004) Estimation of cross sectional and panel data censored regression models with endogeneity. J Econ 122(2):293–316

Hsiao C (1985) Benefits and limitations of panel data. Econom Rev 4(1):121–174

Inkinen H (2015) Review of empirical research on intellectual capital and firm performance. J Intellect Cap 16(3):518–565. https://doi.org/10.1108/JIC-01-2015-0002

Innayah MN, Pratama BC, Hanafi MM (2020) The effect of intellectual capital towards firm performance and risk with board diversity as a moderating variable: study in ASEAN banking firms. J Dinamika Manaj 11(1):27–38

Isanzu JN (2015) Impact of intellectual capital on financial performance of banks in Tanzania. J Int Bus Res Mark 1(1):17–24. https://doi.org/10.18775/jibrm.1849-8558.2015.11.3002

Janošević S, Dženopoljac V, Bontis N (2013) Intellectual capital and financial performance in Serbia: intellectual capital in Serbia. Knowl Process Manag 20(1):1–11. https://doi.org/10.1002/kpm.1404

Joshi M, Cahill D, Sidhu J, Kansal M (2013) Intellectual capital and financial performance: an evaluation of the Australian financial sector. J Intellect Cap 14(2):264–285. https://doi.org/10.1108/14691931311323887

Kanmony JC (2023) Indian economy in the 75th year of its independence. J Econ 4(1):1–8

Kaplan RS, Norton DP (1996) The balanced scorecard: translating strategy into action. Language 11(322p), 23cm

Kapoor S, Saihjpal A (2022) Intellectual capital and performance of Indian companies: an empirical investigation. Int J Learn Intellect Cap 19(6):608. https://doi.org/10.1504/IJLIC.2022.126306

Kasoga PS (2020) Does investing in intellectual capital improve financial performance? Panel evidence from firms listed in Tanzania DSE. Cogent Econ Financ 8(1):1802815. https://doi.org/10.1080/23322039.2020.1802815

Khalique M, Isa AHBM, Nassir Shaari JA, Ageel A (2011) Challenges faced by the small and medium enterprises (SMEs) in Malaysia: an intellectual capital perspective. Int J Curr Res 3(6):398

Khalique M, Ramayah T, Tahir Ali Shah M, Iqbal Z (2019) Intellectual capital and financial performance of banks in Sialkot Pakistan. J Manag Sci 6(1):50–61. https://doi.org/10.20547/jms.2014.1906104

Kweh QL, Lu W-M, Tone K, Nourani M (2022) Risk-adjusted banks’ resource-utilization and investment efficiencies: does intellectual capital matter? J Intellect Cap 23(3):687–712. https://doi.org/10.1108/JIC-03-2020-0106

Le TD, Ho TN, Nguyen DT, Ngo T (2022) Intellectual capital—bank efficiency nexus: evidence from an emerging market. Cogent Econ Financ 10(1):2127485. https://doi.org/10.1080/23322039.2022.2127485

Levin A, Lin C-F, Chu C-SJ (2002) Unit root tests in panel data: asymptotic and finite-sample properties. J Econom 108(1):1–24

Maddala GS, Wu S (1999) A comparative study of unit root tests with panel data and a new simple test. Oxf Bull Econ Stat 61(S1):631–652. https://doi.org/10.1111/1468-0084.0610s1631

Maditinos D, Chatzoudes D, Tsairidis C, Theriou G (2011) The impact of intellectual capital on firms’ market value and financial performance. J Intellect Cap 12(1):132–151

Maji SG, Goswami M (2017) Intellectual capital and firm performance in India: a comparative study between original and modified value-added intellectual coefficient model. Int J Learn Intellect Cap 14(1):76–89

Mehralian G, Rajabzadeh A, Sadeh MR, Rasekh HR (2012) Intellectual capital and corporate performance in the Iranian pharmaceutical industry. J Intellect Cap 13(1):138–158

Meles A, Porzio C, Sampagnaro G, Verdoliva V (2016) The impact of the intellectual capital efficiency on commercial banks performance: evidence from the US. J Multinatl Financ Manag 36:64–74

Mention A, Bontis N (2013) Intellectual capital and performance within the banking sector of Luxembourg and Belgium. J Intellect Cap 14(2):286–309. https://doi.org/10.1108/14691931311323896

Mohapatra S, Jena SK, Mitra A, Tiwari AK (2019) Intellectual capital and firm performance: evidence from Indian banking sector. Appl Econ 51(57):6054–6067. https://doi.org/10.1080/00036846.2019.1645283

Mondal A, Ghosh SK (2012) Intellectual capital and financial performance of Indian banks. J Intellect Cap 13(4):515–530. https://doi.org/10.1108/14691931211276115

Montequín VR, Fernández FO, Cabal VA, Gutierrez NR (2006) An integrated framework for intellectual capital measurement and knowledge management implementation in small and medium-sized enterprises. J Inf Sci 32(6):525–538

Mourtisen J, Bukh PN, Burr B (2005) A reporting perspective on intellectual capital, Perspectives on Intellectual Capital, Vol 1. pp 69–81, https://doi.org/10.1016/B978-0-7506-7799-8.50010-3

Muhammad NMN, Ismail MKA (2009) Intellectual capital efficiency and firm’s performance: study on Malaysian financial sectors. Int J Econ Financ 1(2):206–212

Nadeem M, Gan C, Nguyen C (2018) The importance of intellectual capital for firm performance: evidence from Australia. Aust Account Rev 28(3):334–344

Nawaz T, Haniffa R (2017) Determinants of financial performance of Islamic banks: an intellectual capital perspective. J Islam Account Bus Res 8(2):130–142. https://doi.org/10.1108/JIABR-06-2016-0071

Nazari JA, Herremans IM (2007) Extended VAIC model: measuring intellectual capital components. J Intellect Cap 8(4):595–609. https://doi.org/10.1108/14691930710830774

Nimtrakoon S (2015) The relationship between intellectual capital, firms’ market value and financial performance: empirical evidence from the ASEAN. J Intellect Cap 16(3):587–618. https://doi.org/10.1108/JIC-09-2014-0104

Oppong GK, Pattanayak JK, Irfan M (2019) Impact of intellectual capital on productivity of insurance companies in Ghana: a panel data analysis with System GMM estimation. J Intellect Cap 20(6):763–783. https://doi.org/10.1108/JIC-12-2018-0220

Ozkan N, Cakan S, Kayacan M (2017) Intellectual capital and financial performance: a study of the Turkish banking sector. Borsa Istanb Rev 17(3):190–198. https://doi.org/10.1016/j.bir.2016.03.001

Pal K, Soriya S (2012) IC performance of Indian pharmaceutical and textile industry. J Intellect Cap 13(1):120–137

Pallant J (2011) A Step by Step Guide to Data Analysis Using the SPSS Program: Survival Manual, (4th ed) McGraw-Hill, Berkshire

Phusavat K, Comepa N, Sitko-Lutek A, Ooi K-B (2011) Interrelationships between intellectual capital and performance: empirical examination. Ind Manag Data Syst 111(6):810–829

Pirozzi MG, Ferulano GP (2016) Intellectual capital and performance measurement in healthcare organizations: an integrated new model. J Intellect Cap 17(2):320–350

Poh LT, Kilicman A, Ibrahim SNI (2018) On intellectual capital and financial performances of banks in Malaysia. Cogent Econ Financ 6(1):1453574. https://doi.org/10.1080/23322039.2018.1453574

Pulic A (1998) Measuring the performance of intellectual potential in knowledge economy. In: 2nd McMaster Word Congress on measuring and managing intellectual capital by the Austrian team for intellectual potential, pp 1–20

Pulic A (2000) VAICTM–an accounting tool for IC management. Int J Technol Manag 20(5–8):702–714

Pulic A (2004) Intellectual capital-does it create or destroy value? Meas Bus Excell 8(1):62–68

Rao DT, Sethi N, Dash DP, Bhujabal P (2023) Foreign aid, FDI and economic growth in South-East Asia and South Asia. Glob Bus Rev 24(1):31–47

Rehman AU, Aslam E, Iqbal A (2022) Intellectual capital efficiency and bank performance: evidence from Islamic banks. Borsa Istanb Rev 22(1):113–121

Rowlands J (2018) Deepening understandings of Bourdieu’s academic and intellectual capital through a study of academic voice within academic governance. Stud High Educ 43(11):1823–1836

Ruckdeschel C (1998) Intellectual capital: the new wealth of organizations by Thomas Stewart. Perform Improv 37:56–59

Sahoo M, Sethi N (2023) An empirical insight into the financial globalization–growth nexus via trade openness: evidence from select south Asian countries. Glob Bus Rev 24(2):317–334

Sardo F, Serrasqueiro Z (2017) A European empirical study of the relationship between firms’ intellectual capital, financial performance and market value. J Intellect Cap 18(4):771–788. https://doi.org/10.1108/JIC-10-2016-0105

Sargan JD (1958) The estimation of economic relationships using instrumental variables. Econometrica 26:393–415

Smriti N, Das N (2018) The impact of intellectual capital on firm performance: a study of Indian firms listed in COSPI. J Intellect Cap 19(5):935–964. https://doi.org/10.1108/JIC-11-2017-0156

Soewarno N, Tjahjadi B (2020) Measures that matter: an empirical investigation of intellectual capital and financial performance of banking firms in Indonesia. J Intellect Cap 21(6):1085–1106

St-Pierre J, Audet J (2011) Intangible assets and performance: analysis on manufacturing SMEs. J Intellect Cap 12(2):202–223

Sveiby KE (1997) The new organizational wealth: managing & measuring knowledge-based assets. Barrett-Kohler, San Francisco

Tabachnick BG, Fidell LS, Ullman JB (2013) Using multivariate statistics, vol 6. Pearson, Boston, MA

Ting IWK, Chen F-C, Kweh QL, Sui HJ, Le HTM (2021) Intellectual capital and bank branches’ efficiency: an integrated study. J Intellect Cap 23(4):840–863

Tiwari R, Vidyarthi H (2018) Intellectual capital and corporate performance: a case of Indian banks. J Account Emerg Econ 8(1):84–105. https://doi.org/10.1108/JAEE-07-2016-0067

Tran DB, Vo DH (2018) Should bankers be concerned with intellectual capital? A study of the Thai banking sector. J Intellect Cap 19(5):897–914

Tran NP, Vo DH (2020) Human capital efficiency and firm performance across sectors in an emerging market. Cogent Bus Manag 7(1):1738832. https://doi.org/10.1080/23311975.2020.1738832

Ulum I (2015) Intellectual capital disclosure: Suatu analisis dengan four way numerical coding system. J Akunt Dan Auditing Indones 19(1):39–50

Vergauwen P, Bollen L, Oirbans E (2007) Intellectual capital disclosure and intangible value drivers: an empirical study. Manag Decis 45(7):1163–1180. https://doi.org/10.1108/00251740710773961

Vidyarthi H (2019) Dynamics of intellectual capitals and bank efficiency in India. Serv Ind J 39(1):1–24. https://doi.org/10.1080/02642069.2018.1435641

Vishnu S, Kumar Gupta V (2014) Intellectual capital and performance of pharmaceutical firms in India. J Intellect Cap 15(1):83–99

Weqar F, Khan AM, Haque SMI (2020) Exploring the effect of intellectual capital on financial performance: a study of Indian banks. Meas Bus Excell 24(4):511–529. https://doi.org/10.1108/MBE-12-2019-0118

Weqar F, Khan AM, Raushan MA, Haque SI (2021) Measuring the impact of intellectual capital on the financial performance of the finance sector of India. J Knowl Econ 12:1134–1151

Wernerfelt B (1984) A resource-based view of the firm. Strateg Manag J 5(2):171–180

Xu J, Haris M, Irfan M (2023) Assessing intellectual capital performance of banks during COVID-19: evidence from China and Pakistan. Quant Financ Econ 7(2):356–370. https://doi.org/10.3934/QFE.2023017

Xu J, Li J (2019) The impact of intellectual capital on SMEs’ performance in China: empirical evidence from non-high-tech vs. high-tech SMEs. J Intellect Cap 20(4):488–509. https://doi.org/10.1108/JIC-04-2018-0074

Xu J, Liu F, Korea University Business School (2020) The impact of intellectual capital on firm performance: a modified and extended VAIC model. J Compet 12(1):161–176. https://doi.org/10.7441/joc.2010.01.10

Xu J, Wang B (2019) Intellectual capital performance of the textile industry in emerging markets: a comparison with China and South Korea. Sustainability 11(8):2354. https://doi.org/10.3390/su11082354

Zeghal D, Maaloul A (2010) Analysing value added as an indicator of intellectual capital and its consequences on company performance. J Intellect Cap 11(1):39–60

Zheng C, Islam MN, Hasan N, Halim MdA (2022) Does intellectual capital efficiency matter for banks’ performance and risk-taking behavior? Cogent Econ Financ 10(1):2127484. https://doi.org/10.1080/23322039.2022.2127484

Author information

Authors and Affiliations

Contributions

The first author was responsible for the conception, planning, and implementation of the study, as well as the statistical analysis. The interpretation of the results was assisted by the second author. All the authors have gone through the process of revising and reading the work and agreed on the current version of the manuscript.

Corresponding authors

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

This article contains no human participant investigations conducted by any of the authors.

Informed consent

This article contains no human participant investigations conducted by any of the authors.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Barak, M., Sharma, R.K. Does intellectual capital impact the financial performance of Indian public sector banks? An empirical analysis using GMM. Humanit Soc Sci Commun 11, 208 (2024). https://doi.org/10.1057/s41599-024-02702-5

Received:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41599-024-02702-5

- Springer Nature Limited