Abstract

This paper investigates the effects of taxation on income inequality in an unbalanced panel of 45 countries in Sub-Saharan Africa over the period 1980–2018. We use two-stage least squares and the instrumental variables quantile regression estimates. We find that taxation widens income inequality and that the increasing effects of taxation on income inequality are higher in the most unequal countries than in the least unequal ones. The paper provides evidence that countries in Sub-Saharan Africa should improve the progressivity of their tax systems, so that taxation policy can be used to reduce income inequality.

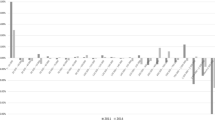

Source: Authors’ construction using data from UNU-WIDER (2021a)

Source: Authors’ construction based on data from UNU-WIDER (2021b)

Similar content being viewed by others

Notes

South Africa, Namibia, Botswana, Central African Republic, Comoros, Zambia, Lesotho, Swaziland, Guinea Bissau, and Rwanda.

Other drivers of income inequality have attracted the attention of social scientists. These include growth (Risso et al. 2013), human capital (Li and Yu 2014), globalization (Heimberger 2020), international trade (Huang et al. 2022), foreign direct investment (Pan-Long 1995), natural resource exploitation (Kim et al.2020), political regime (Bahamonde and Trasberg 2021), urbanization (Sulemana et al. 2019), inflation ( Al-Marhubi 1997), financial development/liberalization ( Koudalo and Wub 2022), employment/unemployment ( Björklund 1991), Economic freedom ( Compton et al. 2014) and remittances (Bang et al.2016).

Inequality in the region has received limited attention historically from a research, policy, and political perspective (Cornia et al. 2017).

The list of countries in the sample are Angola, Benin, Botswana, Burkina Faso, Burundi, Cabo Verde, Cameroon, Central African Republic (CAR), Chad, Comoros, Democratic Republic of Congo (DRC), Congo, Ivory Coast, Djibouti, Equatorial Guinea, Eritrea, Eswatini, Ethiopia, Gabon, Gambia, Ghana, Guinea, Guinea Bissau, Kenya, Lesotho, Liberia, Madagascar, Malawi, Mali, Mauritania, Mauritius, Mozambique, Namibia, Niger, Nigeria, Uganda,, Rwanda, Senegal, Sierra Leone, South Africa, Sudan, Tanzania, Togo, Zambia, and Zimbabwe.

This decision somewhat mitigates the problem of reverse causality since post-tax and transfer Gini coefficient vary "mechanically" and "economically" with the tax system while pre-tax and transfer Gini coefficient vary only through the endogenous responses of labour supply or the equilibrium effect on factor prices (Poterba 2007). We thank one anonymous reviewer for this suggestion.

This variable is used to approximate human capital. It better reflects the quality of human capital relative to the gross rate. Also, data are more available for this variable compared to the secondary and tertiary enrollment rates. In the choice of variables, we prioritize variables which have more observations than others while considering their relevancy in the literature and the context.

Because our period of study covers a relatively a long one (1980-2018, 38 years), our estimations should rely on the assumption that explanatory variables are stationary. We use the Fisher-type unit-root test based on augmented Dickey-Fuller tests. This is because xtunitroot fisher does not require strongly balanced data, and the individual series can have gaps. It fits well with the structure and the characteristics of our data: panel data with individual series having gaps. The results are presented in Table 7 in the Appendix 1. Total revenue, Total non-resource revenue, direct taxes, indirect taxes, trade openness, foreign direct investment, total natural resources rents, urbanization rate, inflation rate, public expenditure on education, remittances are statistically and significantly stationary at level at 1%. Gini coefficient, democracy, financial development, primary education, employment rate, GDP per capita are statistically and significantly stationary at first differences at 1%. We thank two anonymous referees for suggesting this test.

This variable has been used in previous literature as an instrument of institutional quality (Acemoglu et al. 2014) or finance (Beck et al. 2000). Legal origin variable can affect income inequality through social and political institutions rather than directly: for example, the rich elites who are adopting “extractive strategies” are in most countries with French legal origin. For example, La Porta et al. (1999) link the quality of government institutions to legal origins, with French legal origin having a negative effect on institutions.

For additional robustness checks, OLS with time fixed effects, cluster for years and cluster for countries, quantile regression, and instrumental variables with internal instruments are used.

individuals with wealth of USD 1 million or more.

OLS with time fixed effects, cluster for years and cluster for countries, quantile regression and instrumental variables with internal instruments produce qualitatively similar results.

Remittances do not significantly affect income inequality in SSA over the period 1980-2018.

References

Acemoglu, D., F.A. Gallego, and J.A. Robinson. 2014. Institutions, human capital, and development. Annual Review of Economics 6(1): 875–912.

Adam, A., P. Kammas, and A. Lapatinas. 2015. Income inequality and the tax structure: Evidence from developed and developing countries. Journal of Comparative Economics 43(1): 138–154. https://doi.org/10.1016/j.jce.2014.05.006.

Alavuotunki, K., M. Haapanen, and J. Pirttilä. 2019. The effects of the value-added tax on revenue and inequality. The Journal of Development Studies 55(4): 490–508. https://doi.org/10.1080/00220388.2017.1400015.

Al-Marhubi, F. 1997. A note on the link between income inequality and inflation. Economics Letters 55(3): 317–319. https://doi.org/10.1016/s0165-1765(97)00108-0.

Altunbaş, Y., and J. Thornton. 2018. The impact of financial development on income inequality: A quantile regression approach. Economics Letters 175: 51–56. https://doi.org/10.1016/j.econlet.2018.12.030.

Alvaredo, F., L. Chancel, T. Piketty, E. Saez, and G. Zucman. 2018. Rapport sur les inégalités mondiales. Laboratoire des inégalités mondiales. Retrieved from https://wir2018.wid.world/files/download/wir2018-summary-french.pdf-18/04/2022

Alves, J., and T. Silva. 2021. An empirical assessment of monetary policy channels in income and wealth disparities. Comparative Economic Studies 63: 432–449. https://doi.org/10.1057/s41294-021-00149-0.

Atkinson, A.B. 1970. On the measurement of inequality. Journal of Economic Theory 2(3): 244–263.

Atkinson, T. 2015. What can be done about inequality? Juncture 22(1): 32–41. https://doi.org/10.1111/j.2050-5876.2015.00834.x.

Atkinson, A. B., and A. Leigh. 2010. The distribution of top incomes in five Anglo-Saxon countries over the twentieth century. Discussion Paper 4937. Bonn: IZA. https://doi.org/10.2139/ssrn.1631072

Avom, D. 2011. Les politiques fiscales en Afrique Centrale: une analyse empirique. Canadian Journal of Development Studies/revue Canadienne D’études Du Développement 32(3): 239–253.

Bachas, P., L. Gadenne, and A. Jensen. 2020. Informality, consumption taxes and redistribution. Working paper 27429. Cambridge, MA: National Bureau of Economic Research. https://www.nber.org/system/files/working_papers/w27429/w27429.pdf

Bahamonde, H., and M. Trasberg. 2021. Inclusive institutions, unequal outcomes: Democracy, state capacity, and income inequality. European Journal of Political Economy 70: 102048. https://doi.org/10.1016/j.ejpoleco.2021.102048.

Bang, J.T., A. Mitra, and P.V. Wunnava. 2016. Do remittances improve income inequality? An instrumental variable quantile analysis of the Kenyan case. Economic Modelling 58: 394–402. https://doi.org/10.1016/j.econmod.2016.04.004.

Bargain, O., and P. Kwenda. 2014. the informal sector wage gap: New evidence using quantile estimations on panel data. Economic Development and Cultural Change 63(1): 117–153. https://doi.org/10.1086/677908.

Baskaran, T., and A. Bigsten. 2013. Fiscal capacity and the quality of Government in Sub-Saharan Africa. World Development 45: 92–107.

Bastagli, F., D. Coady, and S. Gupta. 2012. Income inequality and fiscal policy. International Monetary Fund. https://doi.org/10.5089/9781475510850.006.

Beck, T., R. Levine, and N. Loayza. 2000. Finance and the sources of growth. Journal of Financial Economics 58(1–2): 261–300.

Becker, G.S., and B.R. Chiswick. 1966. Education and the distribution of earnings. The American Economic Review 56: 358–369.

Benhabib, J., A. Bisin, and S. Zhu. 2011. The distribution of wealth and fiscal policy in economies with finitely lived agents. Econometrica 79(1): 123–157. https://doi.org/10.3982/ECTA8416.

Berg, A.G., and J.D. Ostry. 2017. Inequality and unsustainable growth: Two sides of the same coin? IMF Economic Review 65(4): 792–815. https://doi.org/10.1057/s41308-017-0030-8.

Bergh, A., and T. Nilsson. 2010. Do liberalization and globalization increase income inequality? European Journal of Political Economy 26(4): 488–505. https://doi.org/10.1016/j.ejpoleco.2010.03.002.

Bhorat, H., M.E. Kimani, J. Lappeman, and P. Egan. 2021. Characterisation, definition, and measurement issues of the middle class in sub-Saharan Africa. Development Southern Africa. https://doi.org/10.1080/0376835X.2021.1945912.

Billger, S., and R. Goel. 2009. Do existing corruption levels matter in controlling corruption? Cross-country quantile regression estimates. Journal of Development Economics 90(2): 299–305. https://doi.org/10.1016/j.jdeveco.2008.07.006.

Bird, R.M. 2003. Taxation in Latin America: Reflections on sustainability and the balance between equity and efficiency. Available at SSRN 1393962.

Björklund, A. 1991. Unemployment and income distribution: Time-series evidence from Sweden. The Scandinavian Journal of Economics 93(3): 457–465. https://doi.org/10.2307/3440187.

Blanchard, O., and D. Rodrik. 2021. Combating inequality: Rethinking Government’s role. Cambridge: MIT Press.

Brinca, P., M.H. Ferreira, F. Franco, H.A. Holter, and L. Malafry. 2021. Fiscal consolidation programs and income inequality. International Economic Review 62(1): 405–460. https://doi.org/10.1111/iere.12482.

Cabrera, M., N. Lustig, and H.E. Moran. 2015. Fiscal policy, inequality, and the ethnic divide in Guatemala. World Development 76: 263–279. https://doi.org/10.1016/j.worlddev.2015.07.008.

Cevik, S., and C. Correa-Caro. 2019. Growing (un)equal: Fiscal policy and income inequality in China and BRIC+. Journal of the Asia Pacific Economy 25(4): 634–653. https://doi.org/10.1080/13547860.2019.1699985.

Chancel, L., and T. Piketty. 2021. Global income inequality, 1820–2020: The persistence and mutation of extreme inequality. Journal of the European Economic Association 19(6): 3025–3062. https://doi.org/10.1093/jeea/jvab047.

Chernozhukov, V., and C. Hansen. 2005. An IV model of quantile treatment effects. Econometrica 73(1): 245–261. https://doi.org/10.1111/j.1468-0262.2005.00570.x.

Chinn, M.D., and H. Ito. 2008. A new measure of financial openness. Journal of Comparative Policy Analysis: Research and Practice 10(3): 309–322.

Chletsos, M., and S. Roupakias. 2020. Education and wage inequality before and during the fiscal crisis: A quantile regression analysis for Greece 2006–2016. Review of Development Economics 24(4): 1333–1364. https://doi.org/10.1111/rode.12695.

Christopoulos, D., and P. McAdam. 2017. Do financial reforms help stabilize inequality? Journal of International Money and Finance 70: 45–61. https://doi.org/10.1016/j.jimonfin.2016.05.003.

Ciminelli, G., E. Ernst, R. Merola, and M. Giuliodori. 2018. The composition effects of tax-based consolidation on income inequality. European Journal of Political Economy 57: 107–124. https://doi.org/10.1016/j.ejpoleco.2018.08.009.

Claus, I., J. Martinez-Vazquez, and V. Vulovic. 2013. Coping with rising inequality in Asia: How effective are fiscal policies? The Earth Institute at Columbia University and the Massachusetts Institute of Technology.

Clements, B.J., R.A. Mooij, M. Francese, S. Gupta, and M. Keen. 2015. Fiscal policy and income inequality: An overview. In Inequality and fiscal policy, ed. B.J. Clements, R.A. Mooij, S. Gupta, and M. Keen. Washington, D.C: International Monetary Fund.

Coady, D., and A. Dizioli. 2017. Income inequality and education revisited: Persistence, endogeneity and heterogeneity. Applied Economics 50(25): 2747–2761. https://doi.org/10.1080/00036846.2017.1406659.

Compton, R.A., D.C. Giedeman, and G.A. Hoover. 2014. A distributional analysis of the benefits of economic freedom. European Journal of Political Economy 33: 121–133. https://doi.org/10.1016/j.ejpoleco.2013.12.001.

Cornia, G.A., A. Odusola, H. Bhorat, and P. Conceição. 2017. Introduction, motivation and overview. In Income Inequality Trends in sub-Saharan Africa: Divergence, determinants and consequences, ed. A. Odusola, G.A. Cornia, H. Bhorat, and P. Conceição. New York: United Nations Development Programme.

Cornia, G.A., J.C. Gómez-Sabaini, and B. Martorano. 2011. A new fiscal pact, tax policy changes and income inequality: Latin America during the last decade.WIDER Working Paper, No. 2011/70, ISBN 978-92-9230-437-9, The United Nations University World Institute for Development Economics Research (UNU-WIDER), Helsinki

De Freitas, J. 2012. Inequality, the politics of redistribution and the tax mix. Public Choice 151(3–4): 611–630. https://doi.org/10.1007/s11127-010-9761-z.

Demir, A., V. Pesqué-Cela, Y. Altunbas, and V. Murinde. 2020. Fintech, financial inclusion and income inequality: A quantile regression approach. The European Journal of Finance 28(1): 1–22. https://doi.org/10.1080/1351847X.2020.1772335.

Djankov, S., R. La Porta, F. Lopez-de-Silanes, and A. Shleifer. 2008. The law and economics of self-dealing. Journal of Financial Economics 88(3): 430–465.

Domeij, D., and J. Heathcote. 2004. On the distributional effects of reducing capital taxes. International Economic Review 45(2): 523–554. https://doi.org/10.1111/j.1468-2354.2004.00135.x.

Doyle, M.W., and J.E. Stiglitz. 2014. Eliminating extreme inequality: A sustainable development goal, 2015–2030. Ethics & International Affairs 28(1): 5–13. https://doi.org/10.1017/s0892679414000021.

Duncan, D., and K. Sabirianova Peter. 2016. Unequal inequalities: Do progressive taxes reduce income inequality? International Tax and Public Finance 23(8): 762–783. https://doi.org/10.1007/s10797-016-9412-5.

Durham, J.B. 1999. Econometrics of income distribution: Toward more comprehensive specification of institutional correlates. Comparative Economic Studies 41(1): 43–74. https://doi.org/10.1057/ces.1999.2.

Easterly, W., and S. Fischer. 2001. Inflation and the poor. Journal of Money Credit and Banking 33(2): 160. https://doi.org/10.2307/2673879.

Engel, E.M., A. Galetovic, and C.E. Raddatz. 1999. Taxes and income distribution in Chile: Some unpleasant redistributive arithmetic. Journal of Development Economics 59(1): 155–192.

Feger, T.D. 2014. An analysis of the tax revenue components in Sub-Sahara Africa. The Journal of Developing Areas 48(4): 363–379.

Fields, G. 1980. Education and income distribution in developing countries: a review of the literature. In T. King, Education and income. World Bank Staff Working Paper No. 402 (pp. 231–315). Washington, DC: The World Bank.

Fosu, A.K. 2018. Economic structure, growth, and evolution of inequality and poverty in Africa: An overview. Journal of African Economies 27(1): 1–9. https://doi.org/10.1093/jae/ejx036.

Goñi, E., H.J. López, and L. Servén. 2011. Fiscal redistribution and income inequality in Latin America. World Development 39(9): 1558–1569. https://doi.org/10.1016/j.worlddev.2011.04.025.

Gupta, S., and J.T. Jalles. 2022. Do tax reforms affect income distribution? Evidence from developing countries. Economic Modelling 110: 105804. https://doi.org/10.1016/j.econmod.2022.105804.

Gupta, S., J.T. Jalles, and J. Liu. 2022. Tax Buoyancy in Sub-Saharan Africa and its determinants. International Tax and Public Finance 29: 890–921.

Gylfason, T., and J. Zoega. 2002. Inequality and Economic Growth: Do Natural Resources Matter? CESifo Working. Paper No. 712.

Hacibedel, B., P. Mandon, P. Muthoora, and N. Pouokam. 2019. Inequality in good and bad times: A cross-country approach. IMF Working Paper 19/20.

Hao, L., and D.Q. Naiman. 2007. Quantile regression: Series-quantitative applications in the social sciences. New York: Sage Publications. https://doi.org/10.4135/9781412985550.

Hayes, T.J., and X.D. Medina Vidal. 2015. Fiscal policy and economic inequality in the U.S. States: Taxing and spending from 1976 to 2006. Political Research Quarterly 2(68): 392–407. https://doi.org/10.1177/1065912915578461.

Heimberger, P. 2020. Does economic globalisation affect income inequality? A meta-analysis. The World Economy 43: 2960–2982. https://doi.org/10.1111/twec.13007.

Henley and Partners. 2023. Africa Wealth Report 2023.

Holcombe, R.G., and C.J. Boudreaux. 2016. Market institutions and income inequality. Journal of Institutional Economics 12(2): 263–276. https://doi.org/10.1017/S1744137415000272.

Huang, K., W. Yan, N. Sim, Y. Guo, and F. Xie. 2022. Can trade explain the rising trends in income inequality? Insights from 40 years of empirical studies. Economic Modelling 107: 105725. https://doi.org/10.1016/j.econmod.2021.105725.

Hubmer, J., P. Krusell, and A.A. Smith. 2016. The historical evolution of the wealth distribution. Working paper 23011. Cambridge, MA: National Bureau of Economic Research. https://www.nber.org/system/files/working_papers/w23011/w23011.pdf

International Monetary Fund. 2015. Inequality and economic outcomes in sub-Saharan Africa. Washington, D.C.: International Monetary Fund.

International Monetary Fund. 2023. World Economic Outlook Database 2023. Washington D.C.: International Monetary Fund

Jellema, J., and C. Tassot. 2018. Analyse de l'impact des politiques fiscales et de protection sociale sur les inégalités et la pauvreté au Togo. Document d'orientation de l'OCDE sur le développement 12.

Jimenez, E. 1986. The public subsidization of education and health in developing countries: A review of equity and efficiency. Research Observer 1: 111–129.

Kaplan, D.M. 2022. Smoothed instrumental variables quantile regression. The Stata Journal 22(2): 379–403.

Kaplan, D.M., and Y. Sun. 2017. Smoothed estimating equations for instrumental variables quantile regression. Econometric Theory 33(1): 105–157. https://doi.org/10.1017/S0266466615000407.

Kaplan, D.M. 2021. SIVQR: Stata module to perform smoothed IV quantile regression, Statistical Software Components S459002, Boston College Department of Economics, revised 14 Mar 2023.

Karakotsios, A., C. Katrakilidis, D. Dimitriadis, and T. Christoforidis. 2016. Examining the relationship between income inequality, taxation and economic freedom: A panel cointegration approach. Economics and Business Letters 9(3): 206–215. https://doi.org/10.17811/ebl.9.3.2020.206-215.

Kim, D.-H., T.-C. Chen, and S.-C. Lin. 2020. Does oil drive income inequality? New panel evidence. Structural Change and Economic Dynamics 55: 137–152. https://doi.org/10.1016/j.strueco.2020.08.002.

Kindleberger, C.P. 1965. Europe’s post-war growth: The role of labour supply. New York: Oxford University Press.

Koudalo, Y.M.A., and J. Wub. 2022. Does financial liberalization reduce income inequality? Evidence from Africa. Emerging Markets Review. https://doi.org/10.1016/j.ememar.2022.100945.

Kudryavtsev, A.A. 2009. Using quantile regression for rate-making. Insurance: Mathematics and Economics 45(2): 296–304.

Kuznets, S. 1955. Economic growth and income inequality. American Economic Review 45(1): 1–28.

La Porta, R., F. Lopez-de-Silanes, A. Shleifer, and R. Vishny. 1999. The quality of government. Journal of Law Economics and Organization 15: 222–279. https://doi.org/10.1093/jleo/15.1.222.

La-Porta, R., F. Lopez-de-Silanes, and A. Shleifer. 2008. The economic consequences of legal origins. Journal of Economic Literature 46(2): 285–332. https://doi.org/10.1257/jel.46.2.285.

Li, J., and H. Yu. 2014. Income inequality and financial reform in Asia: The role of human capital. Applied Economics 46(24): 2920–2935. https://doi.org/10.1080/00036846.2014.916390.

Martínez-Vázquez, J., V. Vulovic, and Y. Liu. 2011. Direct versus indirect taxation: Trends, theory, and economic significance. In The Elgar guide to tax systems, ed. E. Albi and J. Martinez-Vazquez. Northampton MA: Edward Elgar Publishing.

Martínez-Vázquez, J., B. Moreno-Dodson, and V. Vulovic, 2012. The impact of tax and expenditure policies on income distribution: Evidence from a large panel of countries. Retrieved from https://aysps.gsu.edu/working-papers.html-18/04/2022

Martins, P.S., and P.T. Pereira. 2004. Does education reduce wage inequality? Quantile regression evidence from 16 countries. Labour Economics 11(3): 355–371. https://doi.org/10.1016/j.labeco.2003.05.003.

Martorano, B. 2018. Taxation and inequality in developing countries: Lessons from the recent experience of Latin America. Journal of International Development 30(2): 256–273. https://doi.org/10.1002/jid.3350.

McNabb, K., A. Oppel, and D. Chachu, 2021. Government Revenue Dataset (2021): Source Selection’. WIDER Technical Note 2021/10. Helsinki: UNU-WIDER.

Medina, L., and F. Schneider. 2018. Shadow Economies Around the World: What Did We Learn Over the Last 20 Years? International Monetary Fund.

Meltzer, A., and S.F. Richard. 1981. A rational theory of government size. Journal of Political Economy 89(5): 914–927. https://doi.org/10.1086/261013.

Milanovic, B. 2016. Global inequality: A new approach for the age of globalization. Harvard University Press.

Mincer, J. 1974. Schooling, experience, and earnings, 2. Human Behavior & Social Institutions.

Mirrlees, J.A. 1971. An exploration in the theory of optimum income taxation. The Review of Economic Studies 38(2): 175–208. https://doi.org/10.2307/2296779.

Modica, E., S. Laudage, and M. Harding. 2018. Domestic revenue mobilisation: A new database on tax levels and structures in 80 countries. Paris: OECD Taxation Working Papers, OECD Publishing.

Muinelo-Gallo, L., and O. Roca-Sagales. 2011. Economic growth and inequality: The role of Fiscal policies. Australian Economic Papers 50(2–3): 74–97. https://doi.org/10.1111/j.1467-8454.2011.00412.x.

Muinelo-Gallo, L., and O. Roca-Sagalés. 2013. Joint determinants of fiscal policy, income inequality and economic growth. Economic Modelling 30: 814–824. https://doi.org/10.1016/j.econmod.2012.11.009.

Musgrave, R.A. 1959. The theory of public finance: A study in public. New York: McGraw Hill.

Nantob, N. 2016. Taxation and income inequality in developing countries: An empirical investigation. Economics Bulletin 36(3): 1508–1522.

Odusola, A. 2017. Fiscal space, poverty and inequality in Africa. African Development Review 29(S1): 1–14. https://doi.org/10.1111/1467-8268.12229.

Okunogbe, O., and F. Santoro. 2023. Increasing tax collection in African Countries: The role of information technology. Journal of African Economies 32: i57–i83.

Ostry, J.D., A. Berg, C.G. Tsangarides, and O.J. Blanchard. 2014. Redistribution, inequality, and growth. Washington, DC: International Monetary Fund.

Pan-Long, T. 1995. Foreign direct investment and income inequality: Further evidence. World Development 23(3): 469–483. https://doi.org/10.1016/0305-750x(95)00136-z.

Piketty, T. 2001. Les hauts revenus en France au XXè siècele: Inégalités et redistributions, 1901–1998. Paris: Bernard Grasset.

Piketty, T. 2014. Capital in the 21st century. London: Beldknap/Harvard.

Poterba, J.M. 2007. Income inequality and income taxation. Journal of Policy Modeling 29(4): 623–633.

Pryor, F.L. 2014. A note on income inequality in East and Central Europe. Comparative Economic Studies 56(1): 42–51. https://doi.org/10.1057/ces.2013.31.

Ragot, X. 2017. Hétérogénéité et économie: Inégalité et imperfections financières. Revue D’economie Financière 128: 109–124. https://doi.org/10.3917/ecofi.128.0109.

Rajan, R.G., and L. Zingales. 2003. The great reversals: The politics of financial development in the twentieth century. Journal of Financial Economics 69(1): 5–50.

Ramos, X., and O. Roca-Sagales. 2008. Long-term effects of fiscal policy on the size and distribution of the pie in the UK. The Journal of Applied Public Economics/fiscal Studies 29(3): 387–411. https://doi.org/10.1111/j.1475-5890.2008.00079.x.

Ramsey, F.P. 1927. A contribution to the theory of taxation. The Economic Journal 37(145): 47–61. https://doi.org/10.2307/2222721.

Risso, W.A., L.F. Punzo, and E.J. Sánchez Carrera. 2013. Economic growth and income distribution in Mexico: A cointegration exercise. Economic Modelling 35: 708–714. https://doi.org/10.1016/j.econmod.2013.08.036.

Rodrik, D. 2000. Institutions for high-quality growth: What they are and how to acquire them. Studies in Comparative International Development 35(3): 3–31. https://doi.org/10.1007/BF02699764.

Sala-i-Martin, X., and A. Subramanian. 2012. Addressing the natural resource curse: An illustration from Nigeria. Journal of African Economies 22(4): 570–615. https://doi.org/10.1093/jae/ejs033.

Salotti, S., and C. Trecroci. 2018. Cross-country evidence on the distributional impact of fiscal policy. Applied Economics 50(51): 5521–5542. https://doi.org/10.1080/00036846.2018.1487001.

Schultz, T. 1963. The economic value of education. New York: Colombia University Press.

Song, Y. 2013. Rising Chinese regional income inequality: The role of fiscal decentralization. China Economic Review 27: 294–309. https://doi.org/10.1016/j.chieco.2013.02.001.

Stiglitz, J.E. 2012. Le prix de l’inégalité. New-York: WW Norton & Compagny.

Stolper, W.F., and P.A. Samuelson. 1941. Protection and real wages. Review of Economic Studies 9(1): 58–73.

Sulemana, I., E. Nketiah-Amponsah, E.A. Codjoe, and J.A.N. Andoh. 2019. Urbanization and income inequality in Sub-Saharan Africa. Sustainable Cities and Society 48: 101544. https://doi.org/10.1016/j.scs.2019.101544.

UNDP. 2017. Income inequality trends in sub-Saharan Africa: Divergence determinants and consequences. New York, NY: United Nations Development Programme.

UNECA.2019. Economic report on Africa. 2019: Fiscal Policy for financing Sustainable Development in Africa. Addis Abeba: Ethiopia.

United Nations Department of Economic and Social Affairs. 2019. Income inequality trends: The choice of indicators matters. UNDESA Social Development Brief.

UNU-WIDER .2021a. World Income Inequality Database (WIID). Version 31 May 2021. Helsinki : UNU-WIDER.

UNU-WIDER .2021b. Government Revenue Dataset. Version 2021. Helsinki: UNU-WIDER. https://doi.org/10.35188/UNU-WIDER/GRD-2021

Vale, S., and F. Camões. 2023. Households’ exposure to the financial sector as a driver of inequality: An analysis of advanced and emerging economies. Comparative Economic Studies 65(2): 362–402. https://doi.org/10.1057/s41294-022-00200-8.

World Bank. 2022. World development indicators. Washington D.C: World Bank.

Wu, J.-Y., and C.-C. Hsu. 2012. Foreign direct investment and income inequality: Does the relationship vary with absorptive capacity? Economic Modelling 29: 2183–2189. https://doi.org/10.1016/j.econmod.2012.06.013.

Xu, C., M. Han, T.A. Dossou, and F.V. Bekun. 2021. Trade openness, FDI, and income inequality: Evidence from sub-Saharan Africa. African Development Review 33(1): 193–203. https://doi.org/10.1111/1467-8268.12511.

Yang, T.-C., V.Y.-J. Chen, C. Shoff, and S.A. Matthews. 2012. Using quantile regression to examine the effects of inequality across the mortality distribution in the U.S. counties. Social Science & Medicine 74(12): 1900–1910. https://doi.org/10.1016/j.socscimed.2012.02.029.

Yu, K., X. Xin, P. Guo, and X. Liu. 2011. Foreign direct investment and China’s regional income inequality. Economic Modelling 28: 1348–1353.

Zucman, G. 2014. Taxing across borders: Tracking personal wealth and corporate profits. Journal of Economic Perspectives 28(4): 121–148.

Acknowledgements

We thank the two anonymous referees for their insightful comments and suggestions which have significantly improved the quality of this research paper. We are also grateful to Abel Gwaindepi, Abrams Tagem, Evgeniya Dubinina, Herman Ndoya, Ibrahim Dia, Rasmane Guigma, Rita Nikiema, Steve Hall, colleagues at the Department of Economics of the Thomas Sankara University in Burkina Faso, and participants at the United Nations University (UNU)—World Institute for Development Economics Research (WIDER) April 2022 Workshop on ‘Data for tax revenue mobilization’ for their insightful comments. The authors acknowledge financial support from UNU-WIDER Research Grant: 605UU-3384.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

Appendix 1: The tables

See Tables 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, 18, 19 and 20

Appendix 2: The figures

Trends of income inequality measured by Palma ratio in SSA, 1980–2018. Source: Authors’ construction using data from UNU-WIDER (2021a)

Source: Authors

Epanechnikov Kernel density estimate of the Gini coefficient. Notes This figure is created using the Epanechnikov kernel density estimation

Source: Authors

Epanechnikov Kernel density estimate of the Palma ratio of income. Notes This figure is created using the Epanechnikov kernel density estimation

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Ouedraogo, I., Dianda, I., Ouedraogo, P.P. et al. The Effects of Taxation on Income Inequality in Sub-Saharan Africa. Comp Econ Stud (2024). https://doi.org/10.1057/s41294-024-00235-z

Accepted:

Published:

DOI: https://doi.org/10.1057/s41294-024-00235-z