Abstract

Slow global economic growth, frequent fluctuations in international financial markets, and increasing wealth disparity have become common concerns facing the globe. Risk prevention and stable economic growth have become the basic requirements for high-quality economic development, and macroprudential policy tools are at the center of these two policy objectives. This paper constructs a unified empirical analysis framework and incorporates the two policy objectives of preventing economic crises and stabilizing economic growth to analyze the comprehensive effects of macroprudential policy. Using data from 100 economies from 2000 to 2017, we find that the impact of macroprudential policy on economic growth can be divided into direct and indirect channels. For all economies, macroprudential policy can indirectly promote economic growth by suppressing economic crises, but its direct effect is heterogeneous. Furthermore, the heterogeneity of the direct effect of macroprudential policy on economic growth is mainly generated through channels such as investment, loan interest rates, and leverage. In high-income economies, the direct impact of macroprudential policy on economic growth is not obvious; in middle- and high-income economies, it promotes economic growth by influencing investment and leverage; in low- and lower-middle-income economies, it hinders economic growth through investment and loan interest rates.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Under the dual pressures of the unprecedented changes in the world and the COVID-19 pandemic, the economic growth of major economies worldwide has generally slowed down, and the wealth gap has accelerated. Geopolitical crises such as the Russia-Ukraine conflict have further intensified the turbulence in the global commodity market and the volatility in international financial markets, with economic and financial risks increasing day by day. President Xi Jinping emphasized at the 10th meeting of the Central Financial and Economic Affairs Commission the need to promote common prosperity in high-quality development, coordinate efforts to prevent and resolve major financial risks, solidify the foundation of financial stability, handle the relationship between stable growth and risk prevention, consolidate the momentum of economic recovery, and use high-quality economic development to resolve systemic financial risks, prevent secondary financial risks from arising during the disposal of risks in other fields. The "Macroprudential Policy Guidelines" released by the People's Bank of China in 2021 provide policy guidance for achieving the combination of stable growth and risk prevention.Footnote 1

Previous studies have shown that the outbreak of economic and financial risks can lead to economic fluctuations and have a negative impact on economic growth (Halmai and Vasary 2012; AlBassam 2013; Elwell 2013; Sultanova and Chechina 2016). Macroprudential policies aimed at preventing systemic financial risks can mitigate economic fluctuations and reduce the probability of economic crises, thus promoting economic growth (Melnic 2019). At the same time, macroprudential policies also have a direct impact on both financial and real economies, affecting economic growth. Existing literature on the direct impact of macroprudential policies mostly suggests that such policies may have negative effects on economic growth by generating economic costs while stabilizing economic growth (Ma 2020; Belkhir et al. 2020), but the mechanism of their impacts remains inconclusive. Therefore, further research is needed to determine whether macroprudential policies will overall hinder economic growth and how they affect economic growth through what mechanisms. On the other hand, there are significant differences among countries in their use of macroprudential policies, with emerging market countries using them relatively more than developed countries (Claessens et al. 2013). Due to different national conditions, it is of great theoretical and practical significance to study whether macroprudential policies play different roles in different countries and whether the same policies have different impact pathways.

Existing literature on the impact of macroprudential policies on economic crises shows a relatively consistent conclusion, that the implementation of macroprudential policies can significantly reduce the probability of a crisis (Behn et al. 2016; Arregui et al. 2013; Belkhir et al. 2020; Nakatani 2020). After the global financial crisis in 2008, both developed and emerging economies have become more active in using macroprudential policies (Akinci et al. 2018; Fan and Ye 2020). Ma (2020) introduced endogenous growth into a small open economy model with binding collateral and concluded that optimal macroprudential policy can reduce the probability of a crisis by two-thirds. Claessens et al. (2013) and Belkhir et al. (2020) found that the inhibitory effect of macroprudential policies on bank crisis outbreaks is more significant in emerging market economies than in developed countries. Frost and Stralen (2018) found in their study that the implementation of macroprudential policies can not only alleviate income and wealth inequality but also reduce the likelihood of a financial crisis.

Among various types of crises, bank crisis has always been one of the major causes of economic fluctuations and systemic risks (Nakatani 2020), and in today's more integrated economy, the outbreak of bank crisis has a greater adverse impact on economic growth compared to other crises (Lin et al. 2012). Chen et al. (2021) found that systemic financial risks often originate from the securities and futures industry and ultimately are absorbed by the banking industry. Lim et al. (2011) believe that systemic risk is largely driven by the fluctuations of economic and financial cycles over time and the interconnectivity of financial institutions and markets. Compared to other types of financial crises, the cost of bank crises in terms of overall output loss is the highest (Babecky et al. 2014; Nakatani 2019). Fernandez et al. (2016) found that the stability of the banking industry is highly correlated with economic stability, and in countries with more developed financial and institutional systems, the stability of the banking industry can reduce economic fluctuations in industries with greater external financial dependence. Furthermore, the impact of bank crisis not only persists during the crisis period but also has a greater impact on the economy after the crisis (Gropp et al. 2022). Therefore, this paper also focuses on bank crises in the study of economic crises.

Macroeconomic prudential policies aim to comprehensively alleviate systemic risk and maintain stable economic growth, especially for countries affected by external economic shocks. However, the implementation of macroeconomic prudential policies may also affect resource allocation, generate economic costs, and thus inhibit economic growth (Claessens et al. 2013; Belkhir et al. 2020). Existing literature on this issue is limited and the conclusions are not consistent.

On the one hand, many scholars have found that macroeconomic prudential policies have a positive effect on economic development. Melnic (2019) believes that macroeconomic prudential policies can enhance the resilience of the financial system, reduce the accumulation of systemic risk, stabilize the financial system, and ensure healthier financial and macroeconomic relationships, thus promoting economic growth. Hodula and Ngo (2022) found in their study of Eurozone countries that economies that actively use macroeconomic prudential policies to prevent credit booms and limit systemic risk often benefit more from financial development than economies that do not adopt such policies. Agenor et al. (2018) found that macroeconomic prudential policies help to promote growth, but financial openness often reduces the growth benefits of prudential tightening. Based on an analysis of policy responses to the 2008 global financial crisis and the supply-side structural reforms that began in 2015, Zhang and Liu (2020) found that while active macroeconomic prudential policies may impede short-term economic growth, they can promote long-term economic growth.

On the other hand, existing research has also found that macroprudential policies may reduce economic growth. Belkhir et al. (2020) found that macroprudential policies can reduce the probability of an economic crisis but at the cost of reducing the average growth rate. Kim and Mehrotra (2017) used a structural panel vector autoregression model and found that contractionary macroprudential policies used to curb credit growth have significant negative effects on macroeconomic aggregates such as real GDP and price levels. Sanchez and Rohn's (2016) research shows that the use of macroprudential policies reduces the average economic growth rate. Richter et al. (2019) quantified the impact of changes in the maximum loan-to-value ratio on output and found that a 10 percentage point decrease in the maximum loan-to-value ratio over four years leads to a 1.1% decline in output.

Given that existing literature has not yet clarified the long-term effects of macroprudential policies on economic growth, this paper constructs a unified empirical framework that incorporates both direct and indirect channel of macroprudential policy on economic growth, and analyzes its comprehensive effects. The main findings of this paper are as follows: (1) On average, the direct effect of macroprudential policies on economic growth is not significant for all economies, but macroprudential policies can indirectly promote economic growth by reducing the probability of economic crisis outbreaks. (2) For high-income economies, the direct effect of macroprudential policies on economic growth is not significant. (3) For upper-middle-income economies, the implementation of macroprudential policies can directly promote economic growth, which is achieved through promoting investment and reducing leverage. (4) For lower-middle-income and low-income economies, the implementation of macroprudential policies will have a direct negative impact on economic growth, which is caused by a decrease in investment and an increase in loan rates.

The main contributions of this article are twofold. Firstly, we examine the direct and indirect effect of macroprudential policies on economic growth within a unified framework. This framework helps us better understand the interactions between macroprudential policies, economic crisis and economic growth. Secondly, we examine the heterogenous effects of macroprudential policy among countries of different development stages. The results indicate the importance of choosing macroprudential policies according to a country’s economic conditions and level of development.

The remainder of this article is organized as follows: Part II presents the research design and data description; Part III presents the empirical results; Part IV analyzes the mechanisms behind the results; Part V examines robustness and heterogeneity; Part VI concludes.

2 Research design and data

In this section, we developed a unified empirical framework to decompose the impact of macroprudential policy on economic growth into two channels: the direct channel, which refers to the direct effect of macroprudential policy on economic growth, and the indirect channel, which involves the impact of macroprudential policy on the probability of economic crisis occurrence and subsequently on economic growth. The main advantage of this approach is that it allows us to quantitatively compare the relative magnitudes of the effects of macroprudential policy on economic growth through different channels.

2.1 Theory foundation

For the theoretical study of the impact of macroprudential policies on economic growth and economic crisis, most scholars use the DSGE model. Rubio and Carrasco-Gallego (2013) used this model to evaluate the interaction between loan-to-value (LTV) rules and traditional monetary policy implemented by central banks, with the real estate market as a representative, and found that introducing macroprudential rules to limit credit can alleviate overheating problems in the economy. Dominic and Pau (2014) used a DSGE model to study the optimal combination of monetary policy and macroprudential policy in two models of the euro area. The study found that introducing macroprudential policy can help reduce macroeconomic volatility, improve welfare, and supplement the shortcomings of a country's monetary policy to some extent. The implementation of macroprudential policy can increase the welfare of depositors, but its impact on borrowers depends on the type of economic shocks. In particular, macroprudential policy may increase the countercyclical behavior of loan spreads, thereby imposing welfare costs on borrowers under technical shocks. Unsal (2011) focused on the effectiveness of macroprudential policy tools such as bank capital adequacy ratio, loan asset ratio, countercyclical loan-to-value ratio, reserve requirements, credit growth limits, and dynamic provisioning rules based on a New Keynesian DSGE model. The results confirmed the role of macroprudential policy in stabilizing the macroeconomy and finance and pointed out that the rational combination of various policy tools can significantly improve the level of social welfare.

Fouejieu et al. (2019) discussed issues related to financial risk suppression. They constructed an economic model with a bubble process and simulated a New Keynesian model with endogenous financial bubbles. The results showed that a central bank that goes against the wind may face a trade-off between inflation, output stability, and financial stability. Therefore, the authors suggested that macroprudential tools should be applied to supplement policy rates to address the accumulation of financial risks. Popoyan et al. (2017) constructed an agent-based macroeconomic model to study the impact of macroprudential regulation on the macroeconomy and the interaction between macroprudential policy and different monetary policy rules. The results showed that the Taylor rule and Basel III prudential regulation, which focus on the triple task of output gap, inflation, and credit growth, are the best policy combination for improving bank soundness and smoothing output fluctuations.

2.2 Empirical methodology and estimation procedure

2.2.1 Empirical methodology

Our empirical analysis adds a macroprudential policy composite index and a dummy variable for economic crises into a standard growth model.Footnote 2 There are two types of macroprudential composite indexes used in this study. The first type of composite index is based on Cerutti et al. (2017), which is composed of 12 subcategories of macroprudential policies, and each country is assigned a score of 1 if it adopts the policy and 0 if it does not. The scores of the 12 subcategories are then summed to obtain the macroprudential policy composite index. The second type of composite index is based on the IMF definition in 2019, which also includes 12 subcategories of macroprudential policies, but assigns a score of + 1 if the policy is adopted and -1 if it is not, and then sums the scores. Furthermore, we treat economic crises as an endogenous variable, the occurrence of which is affected by macroprudential policies.

This framework allows us to analyze the interactions of macroprudential policies, economic crisis and economic growth. Under this setting, the impact of macroprudential policies on economic growth has two channels: (1) an indirect impact through affecting the occurrence of economic crises, and (2) a direct impact on economic growth while controlling for the effects of economic crises.

Specifically, the empirical model in this paper includes both a growth model and a crisis model. The panel form of the growth model is as follows:

Here, \(i\) represents the country and \(t\) represents time; \({y}_{i.t}\) is the growth rate of real GDP;\({y}_{i,t-1}\) is the lagging period of the real GDP growth rate; \({X}_{i,t}\) are a series of control variables including degree of trade openness, degree of financial development, human capital investment, and population growth rate; \({MPI}_{i,t}\) is the composite index of macroprudential policies, which is constructed by assigning a value of 1 to the implementation of a specific subcategory of macroprudential policies in a country at time t, and a value of 0 to the non-implementation of a specific subcategory of macroprudential policies, and then adding up the indicators of each subcategory of macroprudential policies; \({I}_{i,t}^{crisis}\) is a dummy variable for economic crises, with a value of 1 when an economic crisis occurs in a country at time t, and 0 otherwise; and \({\varepsilon }_{i,t}\) is the error term with i.i.d assumption.

In the crisis model, the dummy variable of economic crisis \({I}_{i,t}^{crisis}\) depends on an unobserved latent variable \({W}_{i,t}^{*}\), and its specific data generating equation is as follows:

The latent variable \({W}_{i,t}^{*}\) depends on a set of control variables \({Z}_{i,t}\), which include, stability of the exchange rate system, degree of trade openness, economic policy uncertainty, inflation rate and the degree of financial development, macroprudential policy index \({MPI}_{i,t}\), and a random error term \({\theta }_{i,t}\). Under the assumption that the disturbance term follows a normal distribution \({\theta }_{i,t}\sim N(\mathrm{0,1})\), the crisis model can be written as:

where \(\phi\) is the cumulative distribution function of the standard normal distribution. Therefore, the parameters of the crisis model can be estimated using a probability model such as a probit model.Footnote 3

2.2.2 Estimation process

Equations (1) and (2) are identical in form to the Treatment Effect Model, and the dummy variable of economic crisis can be seen as the treatment variable in the Treatment Effect Model. Therefore, we can use the general Treatment Effect Model to estimate the empirical model, such as Maddala (1986). Equation (1) is the result equation of economic growth, and Eq. (2) is the treatment equation. According to Maddala (1986), if the error term \({\varepsilon }_{i,t}\) and \({\theta }_{i,t}\) are normally distributed and non-independent, we can estimate the equations in two steps.

In the first step, we estimate Eq. (2) and obtain the probability of a crisis occurring.

\(\phi\) is the standard normal cumulative distribution function. Meanwhile, we calculate the hazard ratio (IMR) and add it in Eq. (1) as an additional control variable in the second step of the growth equation to solve the sample selection bias in estimating Eq. (1).

It is worth noting that macroprudential policies, as economic policies formulated by governments, inevitably have endogeneity issues with economic crises. The occurrence of financial crises and economic recessions is precisely the reason for formulating macroprudential policies. Therefore, there is a mutual causality problem between economic crises and macroprudential policies, which cause a simultaneity bias. To address this issue, we use a binary selection model with instrumental variables to estimate the coefficients(\(\widehat{a} , \widehat{b}\)). The instrumental variable selected is the lagged average of macroprudential policies in countries other than the home country at the global level.Footnote 4

In estimating the growth model, we add the hazard ratio obtained in the first step to Eq. (1) and estimate the coefficient (\(\alpha\),\(\beta\),\(\gamma\)). In this step, there is also a problem of simultaneous causality between macroprudential policies and economic growth. To effectively control this endogeneity issue, we use the system GMM model proposed by Arellano and Bond (1991), Arellano and Bover (1995), and Blundell and Bond (1998), which is widely used in the growth literature and is well-suited for estimating the empirical model in this paper. The system GMM has several advantages over the OLS or fixed effect model. First, the system GMM model deals with data similarly to fixed-effect models, effectively controlling unobservable factors that do not vary over time and mitigating omitted variable bias. Secondly, it combines the advantages of instrumental variable methods, using lagged data of existing independent variables as instruments for current data, which better controls for simultaneous causality bias in the model. Finally, the growth model is a dynamic model, with the lagged period of the dependent variable introduced as an important control variable on the right-hand side of the model. The system GMM method can better handle the dynamic nature of the dependent variable, and its estimation results are theoretically superior to methods such as OLS or fixed-effect panel models.

The overall effect of macroprudential policy is the sum of its direct effect on economic growth \(\beta\) and its indirect effect through its impact on economic crises. The total effect of macroprudential policy can be expressed as:

2.3 Data

The data sample includes 100 economies spanning from 2000 to 2017.Footnote 5

The dependent variables are the logarithmic difference of real GDP, that is, economic growth rate (growth model), and economic crises (crisis model). We use the systemic banking crisis indicator provided by the IMF (Laeven and Valencia 2020) to denote economic crises. A systemic banking crisis is identified when the following two conditions are satisfied: (1) the banking system is in significant financial distress (such as significant bank runs, banking losses, and/or bank liquidation losses), and (2) significant banking policy intervention measures are taken in response to significant losses in the banking system. Banking crisis leads to a sustained decline in economic activity, financial intermediation, and social welfare, which is a highly destructive event to economic growth. The IMF's database records 151 systemic banking crises that occurred from 1970 to 2017, and this indicator has become a standard reference for global banking crisis information. Therefore, we use this crisis indicator as the proxy for economic crisis.

The core explanatory variable is macroprudential policy. Macroprudential policy refers to the use of regulatory and supervisory measures to reduce the risks and vulnerabilities of the financial system. Its main objective is to prevent or mitigate the buildup of systemic risks that can lead to financial crises. The main effect of macroprudential policy is to promote financial stability by reducing the likelihood and severity of systemic crises. This is achieved by monitoring and regulating the financial system as a whole, rather than individual institutions or markets. For example, macroprudential policies include capital requirements, leverage ratios, stress tests, loan-to-value ratios, liquidity requirements, and other measures aimed at controlling systemic risks.

The macroprudential policy used in this study is composed of 12 sub-policies.Footnote 6 There are two specific construction methods, one based on Cerutti et al. (2017) and the other on Alam et al. (2019). The macroprudential policy index compiled by Cerutti et al. (2017) is based on a combination of 12 sub-policies. When a sub-policy is implemented, it is scored as 1, and when it is not implemented, it is scored as 0. The total macroprudential policy intensity is then obtained by summing the scores. The macroprudential policy index compiled by Alam et al. (2019) focuses on changes in policy implementation intensity based on the former. If the implementation of this type of policy is strengthened, it is scored as “ + 1”. If the implementation of this type of policy is weakened, it is scored as “-1”. If there is no change, the score is 0. The main results of this study are based on the former analysis, and the robustness results based on the latter are reported in Table 7.

In addition, we also classify macroprudential policies into different types based on their policy aims and specific implementation, and examine the effects of these subcategories of macroprudential policies on economic growth. According to Article 15 of the “Macroprudential Policy Guidelines” issued by the People's Bank of China in 2021, macroprudential policy tools can be classified according to the type of systemic financial risk. One way is to classify macroprudential policies by time and structural dimensions. Time dimension macroprudential policy tools are used for countercyclical adjustment to smooth the pro-cyclical fluctuations of the financial system. These tools include constraining the debt-to-income ratio of residents, requiring banks to provide higher risk reserves during economic upturns, requiring banks to provide more capital reserves during economic upturns, limiting the amount of foreign currency loans by banks, directly controlling credit growth rate, setting a limit on the loan-to-value ratio of mortgage loans, and requiring additional margin for foreign exchange deposits during economic upturns. Structural dimension macroprudential policy tools aim to prevent systemic financial risks from spreading across institutions, markets, sectors, and borders by increasing regulatory requirements for key nodes of the financial system. These tools include setting a limit on banks' leverage ratios, requiring nationwide large banks to provide more capital reserves, controlling the proportion of cross-holdings of debt by the banking industry or individual banks, controlling excessive concentration of financial asset holders, and imposing increased taxes on the income of financial institutions. Bernier and Plouffe (2019) and Miao and Wang (2010) used this classification to analyze the relationship between macroprudential policies and systemic risks.

In addition to this classification, according to the research of Fang (2013), Bernier and Plouffe (2019), and Aizenman et al. (2020), macroprudential policy tools can be divided into capital, liquidity, and credit policies. Capital policies include requiring banks to provide higher risk reserves and more capital reserves during economic upswings, requiring national banks to provide more capital reserves, and controlling the proportion of debt held by the banking industry or individual banks. Liquidity policies include limiting the amount of foreign currency loans by banks, directly controlling credit growth, increasing taxes on financial institutions' income, and imposing additional margin requirements on foreign currency deposits. Credit policies include restricting the debt-to-income ratio of households, setting a limit on the leverage ratio of banks, controlling excessive concentration of financial asset holders, and setting a limit on the risk-weighted ratio of mortgage lending. The IMF, Financial Stability Board, and Bank for International Settlements officially announced and adopted this classification method in 2016.

The control variables for the growth model and crisis model include the degree of trade openness, measured by the share of merchandise trade in GDP, the degree of financial development, measured by the share of private sector domestic credit in GDP, human capital investment, measured by education level, population growth rate, stability of the exchange rate system, economic policy uncertainty, and inflation rate measured by the GDP deflator.Footnote 7 The selection of control variables refers to relevant literature, such as Belkhir et al. (2020) and Ranciere et al. (2006). In addition to all the control variables in the growth and crisis models, the control variables involved in the mechanism analysis also include the investment rate (percentage of investment in GDP), leverage ratio (share of private sector credit in GDP), the share of total debt repayment in GDP, economic volatility index (global economic volatility index VIX), the share of bank liquid reserves in bank assets, and loan interest rates. Table 1 provides descriptive statistics for the data in the model, and Appendix 2 provides definitions and sources of data indicators in the regression analysis.

From the first row of Table 1, it can be seen that the mean value of macroprudential policy is 2, indicating that on average, the use of macroprudential policy is relatively low. However, there is significant variations in the implementation of macroprudential policies among countries. The maximum value of the macroprudential policy index is 10, indicating that this country has implemented 10 macroprudential policies. The country with the least use of macroprudential policies has not implemented any corresponding policies. The results in the second row of Table 1 indicate that, on average, the intensity of macroprudential policy is strengthening, with an average annual increase of 0.329 in macroprudential policy intensity, and there are significant differences in the changes in macroprudential policy intensity among countries.

3 Empirical results

3.1 The impact of macroprudential policy on economic growth and economic crises

In this section, we analyze the comprehensive impact of macroprudential policy on economic growth and economic crises within a unified framework. First, we use a binary selection model with instrumental variables to analyze the impact of macroprudential policy on economic crises. Then, we use a dynamic panel economic growth model to analyze the impact of macroprudential policy and economic crises on economic growth. Finally, we calculate the total effect of macroprudential policy on economic growth.

Columns (1) and (2) of Table 2 report the results of the whole sample. Column (1) reports the estimates of the crisis model, and column (2) reports the estimates of the growth model. The regression results for the sample of all countries can be summarized as follows: Firstly, macroprudential policy can significantly reduce the probability of economic crisis outbreak at a 1% level of significance. For every one-unit increase in macroprudential policy intensity, the probability of an economic crisis outbreak decreases by \(0.013(E\left\{\varphi(\widehat aZ_{i,t}+\widehat b)-\varphi(\widehat aZ_{i,t})\right\})\). In the growth model equation, the direct impact of macroprudential policy on economic growth is not significant. However, the outbreak of an economic crisis will hinder economic growth at a significant level of 5% (\(\widetilde{\upgamma }\)<0), and the outbreak of an economic crisis will have a negative impact of 3.459 percentage points on economic growth. Therefore, the total marginal effect of macroprudential policy on economic growth is:Footnote 8

Due to the direct effect of macroprudential policy being zero in the overall sample, the total effect of macroprudential policy on economic growth is equal to the indirect effect; that is, for each unit increase in the implementation of macroprudential policy, the economic growth rate will increase by 0.045 percentage points.

Overall, the positive impact of macroprudential policy on growth results mainly from its inhibitory effect on economic crises.

3.2 Heterogeneity of macroprudential policy: regression results by subsample

Cerutti et al. (2017) found that emerging market economies rely more on macroprudential policies than advanced economies. Developed countries often have more developed financial systems that provide various alternative sources of funding and risk mitigation, which makes it difficult for macroprudential policies to be effective in these countries. Lim et al. (2011) found that emerging market economies use macroprudential tools more extensively than advanced economies because their financial markets are underdeveloped and banks typically dominate the financial sector. Due to the strong correlation between institutional quality and per capita income, countries that benefit from capital account liberalization are mostly middle- to high-income countries (Klein 2005). This finding raises an important question for our research: Does the effectiveness of macroprudential policies vary across countries with different levels of development?

In order to better illustrate whether the role of macroprudential policy in economic growth is influenced by institutional quality and national development level, we divided the sample into high-income economies, upper middle-income economies, and other income economies (lower middle-income and low-income economies).Footnote 9 Columns (3)-(8) in Table 2 report the regression results for the sub-samples.

3.2.1 Effects of macroprudential policies on economic crisis and economic growth in high-income economies

The results in columns (3) and (4) of Table 2 show that for high-income economies, macroprudential policy can significantly reduce the probability of economic crises at the 1% level of significance. An increase of one unit in macroprudential policy implementation can lower the probability of economic crises by 0.024. At the same time, the direct effect of macroprudential policy on economic growth is not significant, with a direct effect of 0. However, the occurrence of economic crises significantly damages economic growth, with a 0.645 percentage point loss in economic growth rate at the 5% level of significance (\(\widetilde{\upgamma }\)<0)Footnote 10.The total effect of macroprudential policy on economic growth is:

High-income economies have relatively sound contractual frameworks and more developed financial systems, resulting in insignificant direct effects of macroprudential policies on economic growth in these countries. Therefore, the total effect of macroprudential policies on economic growth in high-income countries comes from the indirect effects of reducing the probability of crisis occurrence. For every unit increase in the intensity of macroprudential policies, the economic growth rate is expected to increase by 0.016 percentage points.

3.2.2 Effects of macroprudential policies on economic crisis and economic growth in upper middle-income economies

The results in columns (5) and (6) of Table 2 show that for upper middle-income economies, macroprudential policies can significantly reduce the probability of economic crisis at a 1% level of significance, with a marginal effect of -0.009. In the growth model, macroprudential policies have a significant direct effect (\(\widetilde{\upbeta }\)>0) on economic growth. A one unit increase in the implementation of macroprudential policies can increase the economic growth rate by 0.338 percentage point at 10% significance level. The outbreak of an economic crisis decreases the growth rate by 7.916 percentage points at 1% significance level. Therefore, in upper middle-income economies, the total effect of macroprudential policies on economic growth is:Footnote 11

In upper middle-income economies, the implementation of macroprudential policies has a positive impact on economic growth, with one unit increase leading to a 0.406 percentage point increase in economic growth. As the institutional quality of these economies is relatively lower than that of high-income economies, they have sufficient economic strength and room to allow macroprudential policies to take effect. Therefore, in upper middle-income economies, macroprudential policies have both direct and indirect positive effects on economic growth.

3.2.3 Effects of macroprudential policies on economic crisis and economic growth in lower middle-income and low-income economies

The results in columns (7) and (8) of Table 2 indicate that macroprudential policy has a significant effect in reducing the probability of an economic crisis outbreak at the 5% level for lower middle-income and low-income economies. For each unit increase in the intensity of macroprudential policy, the probability of an economic crisis outbreak decreases by 0.013. In the growth model, the direct effect of macroprudential policy on economic growth is significantly negative (\(\widetilde{\upbeta }\)<0), with each unit increase in the intensity of macroprudential policy decreasing the economic growth rate by 0.069 percentage point at the 5% level. The negative direct effect of macroprudential policy in other income economies is due to their lower level of economic development, which is insufficient to support the cost of implementing macroprudential policy. The outbreak of an economic crisis has a significant negative impact on economic growth, with a crisis outbreak reducing the growth rate by 2.528 percentage points at the 5% significance level. The total marginal effect of macroprudential policy on economic growth is:

Increasing the implementation of macroprudential policy by one unit will reduce economic growth rate by 0.036 percentage points.

Through sub-sample analysis, we found that the effects of macroprudential policy vary greatly across three types of economies. Although the indirect effect of macroprudential policy on economic growth is always positive by reducing the probability of a crisis, its direct effect on economic growth differs due to differences in the developmental stage. Macroprudential policy can directly promote economic growth in upper middle-income economies, significantly reduce economic growth in lower middle-income and low-income economies, but its direct impact on economic growth in high-income economies is not significant.

4 Mechanism analysis

As shown in the previous section, the direct effect of macroprudential policy on economic growth is significantly positive in upper middle-income economies, but significantly negative in lower middle-income and low-income economies. This heterogeneity has been widely documented in the literature. Ranciere et al. (2008) found that financial liberalization, by relaxing lending restrictions and promoting investment, can benefit countries with intermediate development levels the most. Other studies have also found that the implementation of macroprudential policy can maintain financial system stability, create a favorable investment environment, promote investment, and drive economic growth (Meng et al. 2018; Huang et al. 2019; John 2012). In our previous research, we also found that the impact of macroprudential policy on economic growth differs between upper middle-income economies and other economies. Therefore, in the following analysis, we will examine the mechanisms through which macroprudential policy produces completely opposite effects on economic growth in the two different income-level economies.

4.1 The mechanism of macroprudential policy in high and middle-income economies

Loayza et al. (2018) found that leverage ratio and countercyclical capital buffers are a means of containing systemic risk. Aikman et al. (2019) found that appropriate macroprudential frameworks can significantly reduce macroeconomic recessions caused by the bursting of real estate bubbles by affecting the leverage ratio of the financial system. In addition, tightening credit conditions through prudent policies to curb excessive credit growth and reduce financial risks often leads to higher economic growth (Agenor et al. 2018). Aizenman et al. (2020) compared peripheral economies that had experienced credit growth with those that had not, and found that macroprudential policies only had a significant impact on peripheral economies that had experienced credit growth.Footnote 12 Cerutti et al. (2017) found that macroprudential policies stabilize the fluctuation of economic growth by lowering the leverage ratio. Therefore, in this paper, we consider how macroprudential policies affect economic growth through investment and leverage ratios in upper middle-income countries.

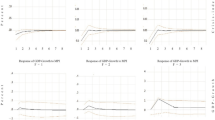

Table 3 presents the mechanism analysis of the impact of macroprudential policies on economic growth in upper middle-income economies. Columns (1) and (2) in Table 3 illustrate that an increase of one unit in the intensity of macroprudential policy would increase the investment rate by 0.606 percentage points at the 5% significance level, and an increase of one unit in the investment rate would raise the economic growth rate by 0.078 percentage points at the 5% significance level. Combining (1) and (2), we conclude that macroprudential policies can accelerate economic growth by promoting investment.

Column (3) and (4) show that an increase in the intensity of macroprudential policy by one unit will lead to a significant decrease of 0.043 in the leverage ratio at the 10% significance level. At the same time, an increase in the leverage ratio by one unit will result in a decrease of 0.424 percentage points in economic growth at the 10% significance level. Combining the results of columns (3) and (4), we conclude that macroprudential policy can promote economic growth by lowering the leverage ratio.

The (5) and (6) columns of Table 3 show that for every one-unit increase in macroprudential policy strength, loan interest rates increase by 1.167 percentage point, but the impact of this increase on economic growth is not significant. Therefore, the mechanism by which macroprudential policy affects economic growth through loan interest rates is not significant in upper middle-income economies.

It can be seen from this that in upper middle-income economies, macroprudential policies promote economic growth by stimulating investment and reducing leverage, which is consistent with relevant findings in current literature.

4.2 Mechanism of macroprudential policy in lower middle-income and low-income economies

Claessens et al. (2013) argue that adopting macroprudential policies may bring about some costs for countries that are subject to international shocks. While macroprudential policies affect resource allocation, they may also influence economic activity and growth, and limit the development of the financial sector. A considerable body of literature suggests that stricter macroprudential policies reduce lending, which can have adverse effects on growth (Bernanke and Blinder 1988; Lim et al. 2011; Cerutti et al. 2017; Teixeira and Venter 2021).

Therefore, based on the analysis of economic growth at the beginning of this section, this paper will consider how macroprudential policies affect economic growth in lower middle-income and lower-income countries through investment and loan interest rates.

Table 4 presents the mechanism analysis of the impact of macroprudential policy on economic growth in these countries. Columns (1) and (2) of Table 4 illustrate that the a one unit increase in implementation of macroprudential policy reduces investment by 0.130 at the 1% significance level, while every unit increase in investment raises the economic growth rate by 0.038 percentage points at the 10% significance level. Combining columns (1) and (2), we can conclude that the negative effect of macroprudential policy on economic growth is achieved through suppressing the investment.

Columns (3) and (4) of Table 4 indicate that although an increase in the leverage ratio by one unit has a inhibitory effect of 0.018 percentage points on economic growth at the 10% significance level, the implementation of macroprudential policy has no significant impact on changes in the leverage ratio. Therefore, the mechanism by which macroprudential policy affects economic growth through the leverage ratio is not significant in lower middle-income and low-income economies.

Columns (5) and (6) of Table 4 illustrate the mechanism of how macroprudential policy affects economic growth through loan rate in lower middle-income and low-income economies. The results show that for every one unit increase in the implementation of macroprudential policy, loan rates will rise by 0.874 percentage point at the 5% significant level; and for every one unit increase in loan rates, the economic growth rate will decrease by 0.036 percentage points at the 1% significance level. Combining columns (5) and (6), we conclude that macroprudential policy negatively affects economic growth by increasing loan rates.

The analysis reveals that, unlike in upper middle-income economies, the institutional and economic systems in lower middle-income and low-income economies are generally less advanced. Therefore, the implementation of macroprudential policies is more difficult to stimulate economic growth through investment and can instead result in high economic costs and damage to the existing investment environment, thus suppressing investment and hindering economic growth. At the same time, macroprudential policies also suppress economic growth by increasing the threshold for corporate financing through raising the loan interest rates.

The performance of the two mechanisms, leverage ratio and loan interest rate, varies across economies with different income levels. In upper middle-income economies with a relatively well-developed financial system, although the implementation of macroprudential policy may increase loan interest rates, the constraint effect on corporate financing will be offset by other financial policies. Therefore, the mechanism of macroprudential policy on economic growth through loan interest rate is not significant. In contrast, in lower middle-income and middle-income economies with a less developed financial system, the implementation of macroprudential policy already incurs certain economic costs, and the policy's effect on reducing the leverage ratio is not significant. Hence, in such economies, the mechanism of macroprudential policy on economic growth through leverage ratio is not significant.

5 Robustness and heterogeneity analysis

Due to different economic environments, policy objectives vary across countries. Emerging economies pay more attention to cross-border capital flows and domestic credit growth, and therefore use more policy tools related to capital, liquidity, and credit growth (Shi and Xu 2020). Developed countries pay more attention to financial risks caused by excessive leverage and deleveraging and use more credit supply tools such as debt-to-income ratios. In terms of controlling the scale of credit growth, macroprudential tools targeting household borrowers have been more effective in emerging market economies, while macroprudential tools targeting financial institutions have been more effective in developed countries. Global macroprudential policies exhibit some countercyclicality and can effectively alleviate the negative impact of financial cycles on the macroeconomy. Compared to normal economic times, the credit restraint effect of macroprudential policies is strengthened when credit growth is too fast and weakened when credit growth is weak (Fan and Ye 2020). Aizenman et al. (2020) classified macroprudential policies into credit, capital, and liquidity categories and concluded that asset-based macroprudential policies have the greatest effect in the least developed countries and developing countries, while liquidity-based macroprudential policy tools have a significant restraining effect on the outbreak of economic crises.

According to the above literature, macroprudential policy is a combination of various financial policy tools, and different types of macroprudential policies are likely to have significant heterogeneity in their effectiveness in countries with different income levels. Therefore, based on the differences in analysis dimensions, we divide macroprudential policies into time dimension macroprudential policies (used for countercyclical adjustment and smoothing of the pro-cyclical fluctuations of the financial system) and structural dimension macroprudential policies (through increasing regulatory requirements for critical nodes in the financial system to prevent systemic financial risk transmission). At the same time, this article classifies policies into three categories according to the most common classification method in previous research based on the different objectives of macroprudential policies: capital-type macroprudential policies (aiming to increase the resilience of the financial system and maintain credit supply under adverse conditions), liquidity-type macroprudential policies (aiming to manage liquidity and foreign exchange risks), and credit-type macroprudential policies (aiming to manage asset prices in the loan market and credit pro-cyclicality).

This section examines the impact of different types of macroprudential policies on economic crises and economic growth.

5.1 Time dimension and structural dimension macroprudential policies

Table 5 reports the effects of macroprudential policies categorized by analysis dimension on different income economies. The first part of Table 5 reports the impacts on high-income economies. For high-income economies, time dimension macroprudential policies have a significant effect on reducing the probability of economic crisis outbreak. For each unit increase in policy implementation, the probability of economic crisis outbreak decreases by 0.037. From the growth model in column (2), it can be inferred that time dimension macroprudential policies do not have a significant direct effect on economic growth. However, the outbreak of economic crises significantly hinders economic growth, leading to a decrease of 3.841 percentage points in economic growth rate. Therefore, the total effect of implementing time dimension macroprudential policies on economic growth in high-income economies is:

For high-income economies, each unit increase in time-dimension macroprudential policy has a promoting effect of 0.142 percentage points on economic growth.

The results in columns (3) and (4) show that structural macroprudential policies can significantly reduce the probability of an economic crisis outbreak at the 1% level of significance; each unit increase in policy implementation reduces the probability of an economic crisis outbreak by 0.047. The results from the growth model indicate that the direct effect of implementing this type of macroprudential policy on economic growth is not significant; however, the outbreak of an economic crisis significantly reduces economic growth by 1.094 percentage points. Therefore, the total effect of structural macroprudential policies on economic growth is:

Therefore, in high-income economies, the structural dimension of macroprudential policies has a direct positive effect on economic growth of 0.051 percentage points per unit increase.

The above analysis finds that for high-income economies, both time dimension and structural dimension macroprudential policies can promote economic growth, and the time dimension macroprudential policy has a more significant effect on economic growth.

Panel B of Table 5 reports the effects of time and structural dimension macroprudential policies on upper middle-income economies. In upper middle-income economies,Footnote 13 the implementation of time dimension macroprudential policies can significantly reduce the probability of economic crisis. In the growth model, this type of policy has a significant positive direct effect on economic growth, while the outbreak of economic crisis has a significant negative impact on economic growth. It is calculated that the total effect of time dimension macroprudential policies on economic growth is:

Therefore, in upper middle-income economies, the implementation of macroprudential policy in the time dimension has a promotion effect on economic growth, with an increase of 0.468 percentage points in economic growth for each unit increase in the policy implementation.

Structural macroprudential policies can also significantly reduce the probability of economic crises in middle- and high-income economies. However, in the growth model, such policies do not have a significant direct impact on economic growth, and economic crises have a significant negative impact on economic growth. Therefore, it is calculated that the overall effect of implementing structural macroprudential policies on economic growth in middle- and high-income economies is:

Therefore, the total effect of the implementation of structural dimension macroprudential policies on economic growth in middle- and high-income economies is calculated to be 0.154 percentage points for each additional unit.

The above analysis indicates that in upper middle-income economies, both time dimension and structural dimension of macroprudential policies can significantly increase economic growth rates by reducing the probability of crises. The time dimension of macroprudential policy can directly promote economic growth.

The third part of Table 5 reports the effects of two types of macroprudential policies on lower middle-income and low-income economies. In these economies, the implementation of time-dimension macroprudential policy can significantly reduce the probability of economic crises. However, in the growth model, both time-dimension macroprudential policy and the outbreak of economic crises will have a significant negative impact on economic growth. Therefore, it is calculated that the total effect of implementing time-dimension macroprudential policy on economic growth is:

Therefore, in lower middle-income and low-income economies, the implementation of time-dimension macroprudential policies will have a negative effect of 0.698 percentage points on economic growth for each unit increase. This is consistent with our earlier conclusion that the implementation of macroprudential policies will incur economic costs, affect resource allocation efficiency, and have a negative impact on the economy. Lower middle-income and low-income economies have relatively imperfect economic systems, thus the implementation of macroprudential policies incurs the greatest cost.

The results in the last two columns indicate that the structural dimension of macroprudential policies can significantly reduce the probability of economic crises. However, both the implementation of structural dimension policies and the outbreak of economic crises will have a significant negative impact on economic growth. Therefore, it can be calculated that in middle-to-low-income and low-income economies, the total effect of implementing structural dimension macroprudential policies on economic growth is:

As a result, the total effect of structural macroprudential policies on economic growth in lower middle-income and low-income economies is a negative 0.065 percentage points for each additional unit of implementation.

The above analysis indicates that both the time dimension and the structural dimension of macroprudential policies would reduce economic growth rates in lower middle-income and low-income economies, with the time dimension having a more significant effect.

5.2 Capital type, liquidity type and credit type macroprudential policies

Table 6 presents the effects of macroprudential policies categorized by their purpose in different income economies. The first part of Table 6 reports the effects of various macroprudential policies on high-income economies. In high-income economies, capital-type macroprudential policies' implementation can significantly reduce the probability of economic crises, which have a significant negative impact on economic growth. However, their direct impact on economic growth is not significant. The results in columns (1) and (2) show that in high-income economies, the total effect of implementing capital macroprudential policies on economic growth is:

The implementation of capital type macroprudential policies in high-income economies increases economic growth by 0.044 percentage points for each additional unit.

For liquidity-type macroprudential policies, their implementation significantly reduces the probability of economic crises, but the direct impact on economic growth is not significant. Based on the results from columns (3) and (4), it is calculated that in high-income economies, the total effect of implementing liquidity-type macroprudential policies on economic growth is:

Therefore, in high-income economies, the implementation of liquidity-type macroprudential policies increases economic growth by 0.064 percentage points for each additional unit.

Columns (5) and (6) report the impact of credit-type macroprudential policies on economic crises and economic growth. The results show that the implementation of macroprudential policies significantly reduces the probability of economic crises, but the direct impact on economic growth is not significant. It is calculated that in high-income economies, the total effect of implementing credit-type macroprudential policies on economic growth is:

Therefore, in high-income economies, the implementation of credit-type macroprudential policies increases economic growth by 0.05 percentage points for each additional unit.

The above analysis shows that in high-income economies, all three categories of macroprudential policies can significantly increase the economic growth rate, mainly by indirectly promoting economic growth through reducing the probability of economic crises.

Second section of Table 6 reports on the effects of various macroprudential policies on upper middle-income economies. The results in the first two columns show that the implementation of macroprudential policies for capital can significantly reduce the probability of economic crises in middle- and high-income economies. The growth model results further indicate that this type of policy has a significant positive direct effect on economic growth. Combining the results from the first two columns, it is calculated that the total effect of implementing macroprudential policies for capital on economic growth in middle- and high-income economies is,

Therefore, in upper middle-income economies, the implementation of capital-type macroprudential policies can promote economic growth by 0.878 percentage points for each additional unit.

The middle two columns report the effects of liquidity-type macroprudential policies. The results show that the implementation of liquidity-type macroprudential policies does not have a significant impact on the probability of economic crisis, but it has a significant positive direct effect on economic growth. It can be calculated that the total effect of the implementing liquidity-type macroprudential policies on economic growth is:.

Therefore, in upper middle-income economies, the implementation of liquidity-type macroprudential policies increases economic growth by 0.363 percentage points for every unit increase in policy strength.

The last two columns report the effects of credit-type macroprudential policies. The results show that credit-type macroprudential policies can significantly reduce the probability of economic crises, and these policies have a significant positive direct effect on economic growth. Combining the results from columns (5) and (6), it is calculated that the total effect of implementing credit-type macroprudential policies on economic growth is:

Therefore, in upper middle-income economies, each unit increase in credit-type macroprudential policies can promote economic growth by 1.256 percentage points.

The above analysis indicates that in upper middle-income economies, the three types of macroprudential policies categorized by their purposes can all promote economic growth, and credit-type macroprudential policies have the greatest impact on economic growth.

The third section of Table 6 reports the effects of various macroprudential policies in lower middle-income and low-income economies. The results of the first two columns indicate that for these economies, the implementation of capital-type macroprudential policies does not have a significant impact on the probability of economic crisis outbreak, and this type of policy also does not have a significant direct effect on economic growth. Therefore, in upper middle-income and low-income economies, the impact of capital-based macroprudential policies on economic growth is not significant.

The middle two columns report the effects of liquidity-type macroprudential policies. The results indicate that liquidity-based macroprudential policies can significantly reduce the probability of economic crises, but their implementation has a significant negative impact on economic growth. It is calculated that in lower middle-income and low-income economies, the overall effect of implementing liquidity-type macroprudential policies is:

Therefore, in lower middle-income and low-income economies, each unit increase in liquidity-type macroprudential policy leads to a decrease in economic growth rate of 0.013 percentage points.

The last two columns report the effects of credit-type macroprudential policies. The results show that credit-type macroprudential policies do not have a significant impact on the probability of an economic crisis outbreak, but they do have a significant negative effect on economic growth. It is calculated that in middle- and low-income and low-income economies, the total effect of implementing credit-related macroprudential policies on economic growth is:

Therefore, in lower middle-income and low-income economies, for each unit increase in credit-type macroprudential policies, there is a decrease of 0.979 percentage points in economic growth.

The above analysis shows that for lower middle-income and low-income economies, capital-type macroprudential policies have no significant effect on economic growth, while liquidity and credit-type macroprudential policies will reduce the economic growth rate. Due to the underdeveloped financial systems of lower middle-income and low-income economies, the negative impact of credit-type macroprudential policies on economic growth is particularly evident.

5.3 Alternative macroprudential policy variables

In the previous analysis, we used the macroprudential policy indicators compiled by Cerutti et al. (2017) and classified policies based on these indicators. In the subsequent robustness analysis, we adopted the macroprudential policy data from Alam et al. (2019) and examined its effects in countries with different income levels.

Columns (1) and (2) of Table 7 report the results of the crisis and growth models for the overall sample of all countries. Similar to Table 2, column (1) displays the estimates for the crisis probability equation, while column (2) shows the estimates for the growth equation. The results can be summarized as follows: firstly, in the crisis model equation, policy implementation can significantly reduce the probability of economic crises. In the growth model equation, macroprudential policy does not directly affect economic growth; whereas the outbreak of economic crises has a significant negative effect on economic growth. Based on the results in columns (1) and (2) of Table 7, the total effect of macroprudential policy on economic growth can be calculated as:

As the direct effect of macroprudential policy in the overall sample is 0, the total effect of macroprudential policy on economic growth comes from its indirect effect of reducing the occurrence of economic crises. For every one unit increase in the implementation of macroprudential policy, it will promote economic growth by 0.029 percentage points.

Similar to Table 2, we divide the sample countries into high-income economies, upper middle-income economies, lower middle-income and low-income economies, and test the effect of macroprudential policy in countries with different income levels.

The results in columns (3) and (4) of Table 7 show that for high-income economies, the implementation of macroprudential policy can significantly reduce the probability of economic crises. However, the direct effect of macroprudential policy on economic growth is not significant. Based on the results in columns (3) and (4) of Table 7, the total effect of macroprudential policy on economic growth in high-income economies can be calculated as:

Therefore, the total effect of macroprudential policy on economic growth in high-income economies is equal to 0.053, that is, for every one unit increase in the implementation of macroprudential policy, it will increase the economic growth rate by 0.053 percentage points.

The results in columns (5) and (6) of Table 7 show that for upper middle-income economies, the implementation of macroprudential policy can significantly reduce the probability of economic crises, and also directly promote economic growth. Based on the results in columns (5) and (6) of Table 7, the total effect of macroprudential policy on economic growth in upper middle-income economies can be calculated as:

Therefore, in upper middle-income economies, for every one unit increase in the implementation of macroprudential policy, it will promote economic growth by 0.793 percentage points.

The results in columns (7) and (8) of Table 7 show that macroprudential policy can significantly reduce the probability of economic crises in lower middle-income and low-income economies. However, the implementation of macroprudential policy has a significant negative impact on economic growth in these economies. The overall effects of macroprudential policy on economic growth is:

Therefore, in lower middle-income and low-income economies, the implementation of macroprudential policy will result in a negative effect on economic growth, with a significant decrease in economic growth rate by 0.037 percentage points for each unit increase in macroprudential policy implementation.

The subsample analysis shows that the implementation of macroprudential policies significantly promotes economic growth in upper middle-income and high-income economies but significantly inhibits economic growth in other economies. The results in Table 7 indicate that the main findings of this paper do not change with the variation of macroprudential policy intensity measures, and the analysis results of macroprudential policies in this paper are robust.

6 Conclusion

Amid the unprecedented global changes and the pressures of the COVID-19 pandemic, macroprudential policy aimed at risk prevention and stabilizing growth has become an important policy tool for many countries. However, macroprudential policy may also impose economic costs and suppress economic growth. As the literature has not yet clarified the long-term effects of macroprudential policy on economic growth, this paper constructs a unified empirical analysis framework, incorporating both its direct effect and indirect effect through curbing the probability of economic crisis, to analyze its comprehensive effects on economic growth.

Based on empirical analysis using data from 100 countries and regions from 2000 to 2017, we find that, in general, macroprudential policy mainly indirectly promotes economic growth by mitigating economic crises. The growth enhancing effect of macroprudential policy is most pronounced in upper middle-income economies. On the one hand, macroprudential policy can indirectly promote economic growth by mitigating economic crises; on the other hand, macroprudential policy can directly promote economic growth. This direct effect is mainly achieved through two channels: investment and leverage ratio. Furthermore, this study conducted a series of heterogeneity and robustness tests and concluded that (1) the direct effect of macroprudential policy on economic growth is not significant in high-income economies; (2) macroprudential policy can directly promote economic growth in upper middle-income economies, and this is achieved by promoting investment and reducing leverage ratio; (3) macroprudential policy can directly inhibit economic growth in lower middle-income and low income economies, and this is achieved by reducing investment and increasing loan interest rates; and (4) different types of macroprudential policies have different effects on economic growth and economic crises.

The conclusions of this article have important policy implications. First, macroprudential policies have strong heterogeneity across different economies. Therefore, to maximize the effects of macroprudential policies, policymakers should adopt policies that are tailored to local country conditions, avoiding excessive implementation that could lead to high economic costs and thus hinder economic growth. Second, different categories of macroprudential policies have different effects on different economies. For high-income economies, which have more developed financial systems, comprehensive macroprudential policies can be implemented to reduce the likelihood of crises and promote economic growth. For upper middle-income economies, direct promotion of economic growth can be achieved through the implementation of macroprudential policies of time dimension, or by increasing the proportion of structural, capital, and credit policies implemented. For lower middle-income and low-income economies, which have less developed financial systems, macroprudential policies should be implemented to reduce the probability of crises, while improving the financial market system to reduce the economic costs associated with implementing macroprudential policies. Third, for China, which is at an important stage of transitioning from an upper middle-income country to a high-income country, any misstep could lead China to fall into the middle-income trap. The change in global economic environment and the digitalization of economy pose both more challenges and opportunities for China (Jia et al.,2023). The effective promotion of economic growth through macroprudential policies in upper middle-income countries is consistent with China’s current stage of development and the complex and ever-changing global situation. Therefore, further improving the effectiveness of China’s macroprudential policies and is of great practical significance for China’s high-quality economic development.

Notes

Guidelines for macroprudential Policy of the People’s Bank of China (Trial).http://www.pbc.gov.cn/huobizhengceersi/214481/3868581/3868584/4437051/index.html

There are two types of macroprudential composite indices used in this article. The first type of composite index is based on Cerutti et al. (2017), which consists of 12 subcategories of macroprudential policies, and counts whether each country adopts this subcategory of policies, using 1 and not using 0, and then adding up the 12 subcategories to obtain the macroprudential policy composite index; The second type of composite index, according to the IMF definition in 2019, consists of 12 sub-categories of macroprudential policy, which are + 1 and -1 are not used, thus being summed.

In practical estimation, we considered various probability models other than the Probit model, and the estimation results are very robust.

We also used the lagged one period of our country's macroprudential policies as an instrumental variable, and the results were consistent.

At the same time considering the availability of macroprudential policies and control variables, we finally selected 100 countries and regions.

Please refer to Appendix 1 for a detailed description and classification of macroprudential policy subcategories.

Direct effect = \(\widetilde{\upgamma }*\mathrm{E}\left\{\mathrm{\varphi }(\widehat{\mathrm{a}}{\mathrm{Z}}_{\mathrm{i},\mathrm{t}}+\widehat{\mathrm{b}})-\mathrm{\varphi }(\widehat{\mathrm{a}}{\mathrm{Z}}_{\mathrm{i},\mathrm{t}})\right\}\).

The World Bank in 2021 divided countries into different income levels based on their gross national income per capita. High-income countries are those with a gross national income per capita greater than $12,535, upper-middle-income countries have a gross national income per capita between $4,046 and $12,535, lower-middle-income countries have a gross national income per capita between $1,036 and $4,046, and low-income countries have a gross national income per capita less than $1,036. Please refer to Appendix 3 for the specific country classifications.

Compared with high-income, upper-middle-income, and other income economies, it was found that the impact of economic crisis on economic growth is minimal in high-income countries. This is because high-income countries have higher levels of financial development and more sophisticated financial defense systems.

Total effect = = \(\widetilde{\upbeta }+\widetilde{\upgamma }*\mathrm{E}\left\{\mathrm{\varphi }(\widehat{\mathrm{a}}{\mathrm{Z}}_{\mathrm{i},\mathrm{t}}+\widehat{\mathrm{b}})-\mathrm{\varphi }(\widehat{\mathrm{a}}{\mathrm{Z}}_{\mathrm{i},\mathrm{t}})\right\}\), same as above.

The peripheral economies refer to countries outside of the United States, Japan, and the Eurozone.

Since the analysis method is the same as that in Sect. 5.1, the subsequent parts of this article will not provide a detailed introduction to the analysis process.

References

Agenor, P. R., L. Gambacorta, E. Kharroubi, and L.A. Pereira da Silva. 2018. The effects of prudential regulation, financial development and financial openness on economic growth. BIS Working Papers. No 752.

Aikman, D., J. Bridges, A. Kashyap, and C. Siegert. 2019. Would macroprudential regulation have prevented the last crisis? Journal of Economic Perspectives 33 (1): 107–130.

Aizenman, J., M.D. Chinn, and H. Ito. 2020. Financial spillovers and macroprudential policies. Open Economies Review 31 (3): 529–563.

Akinci, O., and J. Olmstead-Rumsey. 2018. How effective are macroprudential policies? An empirical investigation. Journal of Financial Intermediation 33: 33–57.

AlBassam, B.A. 2013. The relationship between governance and economic growth during times of crisis. European Journal of Sustainable Development 2 (2): 1–1.

Alam, Z., Alter, M. A., Eiseman, J., Gelos, M. R., Kang, M. H., Narita, M. M, and N Wang. 2019. Digging deeper--Evidence on the effects of macroprudential policies from a new database. International Monetary Fund.

Arellano, M., and S. Bond. 1991. Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. The Review of Economic Studies 58 (2): 277–297.

Arellano, M., and O. Bover. 1995. Another look at the instrumental variable estimation of error-components models. Journal of Econometrics 68 (1): 29–51.

Arregui, M.N., M.J. Benes, M.I. Krznar, M.S. Mitra, and Santos, M. A. 2013. Evaluating the net benefits of macroprudential policy: A cookbook. International Monetary Fund .NO 167.

Babecky, J., T. Havránek, J. Matějů, M. Rusnák, K. Šmídková, and B. Vašíček. 2014. Banking, debt, and currency crises in developed countries: Stylized facts and early warning indicators. Journal of Financial Stability 15: 1–17.

Behn, M., M. Gross, and T.A. Peltonen. 2016. Assessing the costs and benefits of capital-based macroprudential policy. ECB Working Paper NO1935.

Belkhir, M., M.S.B. Naceur, B. Candelon, and J.C. Wijnandts. 2020. Macroprudential policies, economic growth, and banking crises. International Monetary Fund, 54–99.

Bernanke, B. S., and A.S. Blinder. 1988. Credit, money, and aggregate demand. NBER working paper. NO2354.

Bernier, M., and M. Plouffe. 2019. Financial innovation, economic growth, and the consequences of macroprudential policies. Research in Economics 73 (2): 162–173.

Blundell, R., and S. Bond. 1998. Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics 87 (1): 115–143.

Cerutti, E., S. Claessens, and L. Laeven. 2017. The use and effectiveness of macroprudential policies: New evidence. Journal of Financial Stability 28: 203–224.

Chen, S., Li, J., Tan, L, and H Yang. 2021. High-dimensional time-varying measurement and transmission mechanism of China's systemic financial risk. World Economy(in Chinese) (12):28–54.

Claessens, S., S.R. Ghosh, and R. Mihet. 2013. Macro-prudential policies to mitigate financial system vulnerabilities. Journal of International Money and Finance 39: 153–185.

Dominic Quinta and Pau Rabana. 2014.Monetary and Macroprudential Policy in an Estimated DSGE Model of the Euro Area.International Journal of Central Banking (6): 169–236.

Elwell, C. K. 2013. Economic recovery: Sustaining US economic growth in a post-crisis economy. Congressional Research Service. R41332.

Fan, T., and S. Ye. 2020. The Use and Effectiveness of Macroprudential Policies—Evidence form 62 countries. International Finance Research 12: 33–42.

Fang Y. 2013. Research on China's Macro-prudential Regulatory Framework. Ph.D. Dissertation, Nankai University.

Fernandez, AI., González, F, and N Suárez. 2016. Banking stability, competition, and economic volatility. Journal of Financial Stability 22: 101–120.

Fouejieu, A., A. Popescu, and P. Villieu. 2019. Trade-offs between macroeconomic and financial stability objectives. Economic Modelling 81: 621–639.

Frost, J., and R. van Stralen. 2018. Macroprudential policy and income inequality. Journal of International Money and Finance 85: 278–290.

Gropp, R., S. Ongena, J. Rocholl, and V. Saadi. 2022. The cleansing effect of banking crises. Economic Inquiry 60 (3): 1186–1213.

Halmai, P., and V. Vásáry. 2012. Convergence crisis: Economic crisis and convergence in the European Union. International Economics and Economic Policy 9 (3): 297–322.

Hodula, M., and N.A. Ngo. 2022. Finance, growth and (macro) prudential policy: European evidence. Empirica 49 (2): 537–571.

Huang, Y., Y. Cao, K. Tao, and C. Yu. 2019. Monetary policy and macroprudential policy stabilize economy. Financial Research 12: 70–91.

Jia, W., A. Collins, and W. Liu. 2023. Digitalization and economic growth in the new classical and new structural economics perspectives. Digital Economy and Sustainable Development 1 (1): 1–14.

John, K. D. 2012. Linking Economic Modeling and System Dynamics: A Basic Model for Monetary Policy and Macroprudential Regulation. In 30th International Conference of the System Dynamics Society. pp. 22–26.

Kim, S., Mehrotra, A. N. 2017. Effects of monetary and macro-prudential policies–evidence from inflation targeting economies in the Asia-Pacific region and potential implications for China. ZBW working paper 50(5):967–992.

Klein, M. W. 2005. Capital Account Liberalization, Institutional Quality and Economic Growth: Theory and Evidence. NBER Working Paper, (w11112).

Laeven, L., and F. Valencia. 2020. Systemic banking crises database II. IMF Economic Review 68 (2): 307–361.

Lim, C. H., A. Costa, F. Columba, P. Kongsamut, A. Otani, M. Saiyid, T. Wezel, and X. Wu. 2011. Macroprudential policy: what instruments and how to use them? Lessons from country experiences. NO 238.

Lin, P.C. 2012. Banking industry volatility and growth. Journal of Macroeconomics 34 (4): 1007–1019.