Abstract

This paper explores the role of hydrogen fuel cell vehicles (HFCVs) in helping to meet global climate goals of limiting long-term greenhouse gas (GHG) emissions to 1.5 °C. Employing the GREET Model and data from the International Energy Agency (IEA), the study comprehensively compares the full fuel-cycle emission profiles of HFCVs and battery electric vehicles (BEVs). The paper conducts an in-depth examination of the interplay between the carbon intensity of the electric grid and the resulting GHG emissions within the context of refueling HFCV vehicles via electrolyzers, and the analysis draws a comparison to BEVs charged using the same electric grid. The study finds that while emissions for BEVs increase, emissions for HFCVs are significantly larger when HFCVs are refueled from retail outlets producing hydrogen via electrolysis from grid electricity—a finding that was not previously reached in the current literature. The research underscores that countries operating electric grids characterized by high GHG emissions or lacking robust pathways to emission reduction would face suboptimal outcomes by adopting HFCVs powered by hydrogen sourced from distributed grid electricity generation. The gCO2e/mi for BEVs and HFCVs are also calculated when the electricity is produced from renewable energy resources. When electricity is derived from renewable energy sources, it becomes evident that the gCO2e/mi for both HFCVs and BEVs converge towards ‘zero’. The emission metric of gCO2e/mile for a HFCV refueled with the hydrogen produced from natural gas via steam methane reforming (SMR) without carbon capture utilization and storage (CCUS), stands at 105 gCO2e/mile, whereas in the absence of CCUS, it escalates notably to 247 gCO2e/mile, an approximate 150% increase in stark contrast to CCUS inclusion. This quantitative portrayal serves to underscore the substantial potential for curtailing carbon footprints achievable through the integration of CCUS, thereby amplifying its significance within the realm of hydrogen-based transportation and the broader purview of climate change mitigation endeavors. In order to provide a comprehensive perspective, the study delves into the examination of hydrogen production pathways and associated costs for the years 2021, 2030, and 2050. The forecasted supply costs are elucidated, particularly in relation to the potential hydrogen supply originating from variable renewable energy (solar PV and wind) sources and from CCUS-equipped hydrogen production facilities (considering the project pipeline of projects upto 2030). These factors are of substantial importance in shaping the hydrogen supply landscape and subsequently influencing the adoption of HFCVs in the market. The study also examines the cost implications of hydrogen delivery for varying transportation distances (for 2030), acknowledging their important role in the broader context. The challenges posed by the integration of variable renewable energy sources are also addressed, along with the imperative for effective energy storage solutions. This discourse unfolds within the overarching framework of the energy transition, prominently characterized by the ascendancy of solar PV and wind energy. The intricate interplay of these aspects assumes a critical role in shaping the trajectory of future hydrogen supply dynamics over the medium and long term.

Highlights

-

Comparative Analysis of HFCVs and BEVs Characteristics.

-

Analysis of Well-to-Wheel Emission Pathways for HFCVs and BEVs.

-

Application of the GREET Model to Examine Full Fuel Cycle GHG Emissions in Relation to Electric Grid Emissions.

-

Presentation of gCO2e/mi Values for Hydrogen-Fueled HFCVs and Electricity-Powered BEVs Derived from Renewable Energy Sources (Solar PV and Wind).

-

Comparison of Hydrogen Production Routes and Costs (2021, 2030, and 2050), and Cost of Hydrogen Delivery for Various Transport Distances (2030).

-

Exploration of Potential Hydrogen Supply from Renewable Energy Sources (Solar PV and Wind), and from CCUS-equipped hydrogen production facilities.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction and literature review

The goal of limiting the long‐term increase in average global temperatures to 1.5 °C—as articulated in the 2015 Paris Agreement and the UN Sustainable Development Goals 7 (Affordable and Clean Energy) and 13 (Climate Action) [1, 2]—requires deep reductions in global greenhouse gas (GHG) emissions across all sectors to achieve net-zero carbon dioxide emissions globally by the early 2050s [3].

The International Energy Agency (IEA) has defined more than 400 milestones for reaching the global pathway to net‐zero emissions by 2050 that are consistent with the efforts to limit global warming to 1.5 °C [4]. These efforts are essential because it has been determined that global warming causes climate change, and climate change, in turn, elevates the potential of catastrophic climate events such as sea level rise, glacial retreat, desertification, ocean acidification, drought, extreme flooding, heat waves, and hurricanes that can result in serious damage to human and planetary life [5,6,7].

The global 1.5 °C target demands that two-thirds of the known fossil fuel reserves will have to remain unexploited and unmonetized [8]. At the same time, motorized road transport is almost entirely dependent on oil, which represented more than 90% of fuel use in 2020 [9]. This constitutes a clear dilemma, in which significant choices will have to be made regarding how to decarbonize the road transport sector. Throughout history, transportation has driven economic progress and protected social welfare, with road transport essential to the trade of goods and movement of people for millennia. Beginning in the twentieth century, economic development has gone hand in hand with the growth in the number of light-duty vehicles as well as medium and heavy trucks, a trend that is expected to continue in today’s increasingly mobile society. The road transport sector will have to achieve deep reductions in emissions if the world is to reduce its overall emissions since such a large share comes from road transport (Fig. 1). To meet the 2050 Net Zero requirements, transport sector emissions must fall by roughly 20% to less than 6 gigatons (Gt) by 2030 (Fig. 1) [10].

Source: IEA, Transport, 2023

CO2 Emissions from Transport (2000–2021).

Figure 1 shows a steep decline in global CO2 emissions in 2020 due to the lockdowns associated with the Covid-19 pandemic, but as these restrictions were lifted, emissions from the transport sector rebounded, growing by 8% in 2021 to nearly 7.7 Gt CO2 from 7.1 Gt CO2 in 2020. To keep global temperature rise below 2 °C, this trend simply must be reversed through emissions reductions, which in turn requires internal combustion engines (ICEs) be replaced with low-emission electric-powered vehicles as soon as possible. The European Commission’s Fit for 55 Package, in which the EU’s 2030 climate targets were delineated [11], introduced legislation banning petrol and diesel-fueled engines by 2035 [12]. For cars and vans, the EU also adopted new CO2 standards in line with Fit for 55 [13].

After many years of research, government programs, and commercial development, battery electric vehicles (BEVs) and hydrogen fuel cell vehicles (HFCVs) have emerged as the two main candidates to replace ICEs. BEVs and HFCVs have zero tail-pipe emissions and could enable deep cuts in transport sector emissions by using electricity or hydrogen that is generated from low-emission sources.

Government policies have widely supported the introduction of BEVs, a key factor in the boom in EV sales, which shows how industrial, climate, and energy policies can work together [13]. Incentives for the BEVs have been strong, as a detailed summary of 29 research studies on electric vehicle incentives reveals state-level heterogeneity regarding such incentives [14]. In the United States, BEV adoption has been promoted through federal tax incentives since 1992 and even earlier with the California Zero-Emission Vehicle mandate in the late 1980s [15]. Governments continue to deploy new rules to accelerate the transition to BEVs. For example, with the new California Advanced Clean Cars II rule and the federal Inflation Reduction Act (IRA) make it possible to achieve a 50% market share for BEVs by 2030, in line with the United States’ national target [16].

Governments and car manufacturers are providing incentives to promote hydrogen in transportation, including supporting HFCV purchases and installing hydrogen refueling outlets. California, the Northeast United States, Japan, China, South Korea, Germany, France, and other European countries all have such programs, which often involve joint efforts between government and industry, for example, Hydrogen Mobility Europe, H2USA, Germany (the H2 Mobility Initiative), California Fuel Cell Partnership, UK (H2 Mobility UK), South Korea (H2Korea) and Japan (H2 Mobility Japan).

A comparison of well-to-wheel (WTW) energy use and the emissions of HFCVs relative to ICEs exists in the current literature. “[E]ven fueled by hydrogen from a fossil-based production pathway (via steam methane reforming of natural gas) uses 5%-33% less WTW fossil energy and has 15%-45% lower WTW GHG emissions compared to a gasoline conventional ICEV [Internal Combustion Engine Vehicle].” [17]. This is beneficial considering that most hydrogen production (62% in 2021 [18]) is produced from natural gas via steam methane reforming (SMR) without carbon capture utilization and storage (CCUS). Yet what is even more imperative to the goal of achieving deep global GHG emissions reductions in transportation is not only producing hydrogen but supplying it to the vehicle with the lowest possible emissions.

Previously, several studies have demonstrated that BEVs provide emission reductions compared to ICEs when the power generation mix is not CO2 intensive [19]. However, Doucette and McCulloch 2011 underline that depending on the CO2 intensity of a country’s power generation mix, increased penetration of BEVs could lead to higher CO2 emissions as compared to those for ICEs. A similar conclusion was reached by Woo et al. [20] for the GHG emissions of BEVs in 70 countries after making a comparison between ICEs and BEVs, and the authors again found that BEVs may be associated with higher GHG emissions than ICEs. Fifteen other studiesFootnote 1 also discuss that for countries that do not have a low GHG emission power generation mix, BEV penetration may not be effective in reducing GHG emissions.

By conducting environmental and economic life-cycle assessments for ICEs and EVs (BEVs and PHEVs), Faria et al. [21] found that a power generation mix with a large contribution from renewable energy does not always translate into low GHG emissions for EVs, underlining that driving in an aggressive style can increase energy consumption by 48% and that climate control can also increase energy consumption between 24 and 60%. While comparing BEVs with ICEs, other studies such as Hawkins et al. [22] concentrated more on the vehicle production side but underlined that BEVs should be coupled with low-carbon electricity sources to reduce GHG emissions.

Another line of research on GHG emissions for HFCVs in China found that they depended on the power generation mix, showing that “HFCV[s] based on water electrolysis using the renewable electricity perform the best with a value of 31 g CO2-eq/km while that based on on-site water electrolysis using grid electricity perform the worst with a value of 431 g CO2-eq/km in 2017… [and] … in terms of NOx, SOx, PM2.5, and PM10, HFCV based on on-site water electrolysis by grid electricity electrolysis has the highest emissions due to high emission factors of the electricity generation process.” [23].

A group of researchers also discovered in China that compared with ICEs “All HFCV pathways, except electrolysis using grid electricity or liquefied hydrogen pathways, have GHG, volatile organic compounds (VOCs), nitrogen oxides (NOX), fine particulate matter (PM2.5), and sulfur dioxide (SO2) emissions lower than, or comparable to, gasoline vehicles.” [23]. Meanwhile, Yoo et. al. showed in Korea that “electrolysis with Korean grid mix (on-site) pathway has the highest GHG emissions due to its high emission factor of the power generation process.” [24]. These studies concentrate on emissions from hydrogen production pathways solely in China and Korea; however, a comparison of the emissions of HFCVs and BEVs that takes into account electricity and hydrogen production pathways regarding the carbon intensity of the grid has not been conducted.

This paper conducts an in-depth examination of the interplay between the carbon intensity of the electric grid and the resulting GHG emissions within the context of refueling HFCV vehicles via electrolyzers, with the analysis drawing a comparison to BEVs charged using the same electric grid. As the embedded GHG emissions in the grid increase, the gCO2e/mi value increases much more significantly for HFCVs if they are refueled from retail outlets producing hydrogen via electrolysis. Concurrently, the full fuel-cycle GHG emissions of BEVs are significantly lower than for ICEs, even if the electricity grid from which they draw carries a significant amount of electricity produced from fossil fuels. Moreover, if an HFCV system relies on distributed generation using electrolyzers and if the electric grid has a significant share of hydrocarbon electricity production, the GHG emissions of HFCVs could even be higher than conventional ICEs, and significantly higher than BEVs recharging from the same electrical grid, a finding that has not yet appeared in the existing secondary literature. The study emphasizes that countries with high GHG-emitting grids or limited emissions-reduction paths may not benefit optimally from adopting HFCVs fueled by distributed grid-generated hydrogen. When sourced from renewable energy, both HFCVs and BEVs approach nearly zero gCO2e/mile (Fig. 5).

Furthermore, the quantitative analysis pertaining to the gCO2e/mile metric for HFCVs fueled by hydrogen originating from natural gas through steam methane reforming (SMR), both with and without CCUS, is rendered. The discernible contrast emerges as the gCO2e/mile stands at 105 when CCUS is adopted, whereas in the absence of CCUS, this metric significantly escalates to 247. The conspicuous rise in emissions is pronounced, signifying that the incorporation of CCUS is instrumental in mitigating the overall carbon footprint associated with such vehicles. This quantitative elucidation underscores the considerable potential inherent in the integration of CCUS technology, thereby accentuating its significance not only within the scope of hydrogen-based transportation but also within the broader context of endeavors dedicated to climate change mitigation.

Additionally, the study delves into the examination of hydrogen production pathways and associated costs for the years 2021, 2030, and 2050. The forecasted supply costs are elucidated, particularly in relation to the potential hydrogen supply originating from variable renewable energy (solar PV and wind) sources and from CCUS-equipped hydrogen production facilities (considering the project pipeline of projects upto 2030). These factors are of substantial importance in shaping the hydrogen supply landscape and subsequently influencing the adoption of HFCVs in the market. A depiction of the cost implications of hydrogen delivery for varying transportation distances (for 2030) is also provided, recognizing their important role in the broader context.

This discourse unfolds within the overarching framework of the energy transition, prominently characterized by the ascendancy of solar PV and wind energy. The intricate interplay of these aspects assumes a critical role in shaping the trajectory of future hydrogen supply dynamics over the medium and long term. Given the recent surge of interest in and discourse around the role of hydrogen as the “energy carrier of the future” and that global renewable capacity dedicated to producing hydrogen is expected “to increase 100-fold in the next five years, offering opportunities to decarbonize industry and transport” [25], this research asks the question: what role could HFCVs play in decarbonizing transport?

1.1 Global stocks and commercialization

HFCVs broke the 10,000-vehicle mark in 2018, 50,000 in 2021, and 70,000 in 2023 with roughly 1020 hydrogen refueling stations (HRS) worldwide [13]. In 2017, only 330 HRS were in operation worldwide, with the majority in Japan [13]. The HFCV global stock is shown in Fig. 2 (HFCV = FCEV) below.

Source: IEA, Global Electric Vehicle Outlook 2023 (Notes: FCEV/HFCV = Fuel Cell Electric Vehicles, HRS = Hydrogen Refueling Station, PLDV = Passenger Light-Duty Vehicles, LCV = Light Commercial Vehicles, RoW = Rest of the World.)

Stock of HFCV/FCEV in 2022.

While the number of HFCVs is almost two orders of magnitude less than BEVs and plug-in-hybrid electric vehicles (PHEVs) (Fig. 3), HFCV introduction is just starting while initial commercial production of BEVs began many years ago and took more than a decade before the world vehicle stock reached hundreds of thousands and now millions. Tripling in just the last three years, the number of BEVs and PHEVs on the road climbed to over 25 million in 2022 (Fig. 3) with over 450 electric car models globally available. Nonetheless, even with this rapid uptake of BEVs and PHEVs, in total, they represent approximately 1% of the global light-duty vehicle stock.

Source: IEA, Global Electric Vehicle Outlook 2023 (Notes: BEV = battery electric vehicle; PHEV = plug-in hybrid electric vehicle. Electric car stock in this figure refers to passenger light-duty vehicles. “Other” includes Australia, Brazil, Canada, Chile, India, Japan, Korea, Malaysia, Mexico, New Zealand, South Africa, and Thailand. Europe in this figure includes the EU27, Norway, Iceland, Switzerland, and the United Kingdom.)

Global Electric Car Stock 2010–2022.

Given the numbers in Figs. 2 and 3, the current commercialization of BEVs is far ahead of HFCVs, as the BEV uptake has not required a completely new fuel production, transportation, or distribution system. BEVs took the advantage of existing electricity generation and distribution infrastructure, and unlike the early introduction of BEVs and PHEVs, home refueling is unavailable for potential early adopters of HFCVs.

Consumer preference levels for HFCVs and ICEs are similar regarding range and refueling time (3 to 5 min, while it takes 30 min or more to achieve an 80% charge with a high-voltage supercharger). The ranges of current HFCV offerings are between 550 and 650 km and pass the “just like what I am used to” test, while current BEVs do not. These factors give advantages to HFCVs over BEVs in gaining acceptance in the private light-duty vehicle market. However, there exist three barriers to the uptake of the HFCVs: (1) the vehicle cost is higher than the ICEs and BEVs, (2) the production and transportation costs associated with H2 play a vital role in HFCVs market viability, and (3) the need to provide enough refueling infrastructure to motivate HFCV purchases. An early adopter considering a purchase of an HFCV must have at least one convenient refueling outlet—which is the most fundamental need before significant commercialization of HFVCs can commence.

Intrinsic to the discourse surrounding HFCVs is the requisite balance between environmental conscientiousness and financial feasibility. The landscape of technology adoption for HFCVs is notably influenced by a confluence of metrics, transcending the singular realm of GHG emissions reduction. While the mitigation of GHG emissions remains a central impetus, the broader considerations of production and transportation costs associated with HFCVs play an equally vital role in their market viability and necessitate due emphasis on investments.

The production of H2 at low cost is feasible under certain conditions; steam methane reforming (SMR) via natural gas and coal gasification (Fig. 6), established as economically viable avenues for hydrogen generation, nevertheless engender significant quantities of CO2 emissions. Consequently, their transformation into environmentally benign sources of hydrogen necessitates the incorporation of hydrogen from renewables and CCUS technologies that will be explored in the next sections.

Compared to the current uptake of BEVs, HFCV uptake will require a more robust policy intervention before motorists can be expected to purchase them. It might be argued that BEVs are less dependent on the widespread availability of retail recharging infrastructure due to the use of home chargers and chargers at other locations, and in fact, BEVs have evolved without a widely established commercial recharging infrastructure; however, BEVs also do require a new extensive retail recharging infrastructure with all charging options having their specific challenges and, to enable further BEV uptake, public charging points are increasingly necessary. A network of refueling outlets is required for general sales of both BEVs and HFCVs.

Assuming widespread hydrogen refueling availability, HFCVs would provide consumers an experience more similar to ICEs than to BEVs since HFCVs’ range and refueling times are much closer to what consumers are used to. If the problem of vehicle range is solved for BEVs, the other significant concern, namely the longer recharging times for BEVs, may remain despite technological progress. For consumers who require longer vehicle ranges and refueling characteristics, HFCVs would be attractive once the requisite refueling infrastructure is in place.

BEV refueling times are too long to provide consumers with the usual refueling experience and would pose logistical and space problems for retail fuel outlets to accommodate many BEVs at one time. Home and workplace recharging of BEVs takes considerably longer than would be available without a high-voltage supercharger. Longer recharging times (often to a partially charged battery pack) at home and workplace recharging stations would reduce the frequency of BEV recharging at retail outlets compared to the refueling of HFCVs or conventional vehicles. Nonetheless, for long-distance travel, providing adequate BEV charging infrastructure would be problematic considering the amount of time each BEV would take to be recharged and to occupy space at the service outlet.

Another significant issue is that battery-electric technology is less applicable to medium and heavy-duty trucks, as a significant portion of the vehicle weight consists of batteries. Consequently, another low-emission vehicle technology may be needed that provides the same consumer experience as ICEs and with broader applicability to medium and heavier-duty vehicles. Even for the sport-utility vehicle (SUV) segment, more batteries are needed; SUV BEVs often have batteries that are two to three-times larger than small cars.

Considering the emissions, the consumer preference for SUVs is in itself another problem – and one that lies outside the scope of this research – for ICEs, SUV BEVs, and HFCVs. An IEA report states that: “In 2022, ICE SUVs emitted over 1 Gt CO2, far greater than the 80 Mt net emissions reductions from the electric vehicle fleet that year.” [13]. Large cars and SUVs still account for over half of all available BEVs [13], and SUV BEV sales made up 51% of global BEV sales in 2022 [26]. Larger batteries require larger amounts of critical minerals, which in turn elevates the environmental impact per mile traveled, and, as the SUVs continue to get larger, naturally the car will need more energy to operate. For a semi-truck carrying a cargo, the legal weight limit including the cargo is 80,000 pounds, with the 16,000-pound battery making up nearly a quarter of the total weight of the truck [27].

1.2 HFCV heavy-duty applications: trucks and buses

HFCVs are being developed to serve the heavy-duty vehicle market since heavy-duty vehicles require large bursts of power, something that BEVs have less capacity for. In these sectors, HFCVs can provide low-emission electric power to a range of medium and heavy-duty trucks and buses as well as various other applications in which batteries would not be a practical source of electricity. It should also be considered that, based on IEA projections, the growth of oil demand is projected to take place in the transportation and petrochemical sectors [13]. Consequently, electrifying road transport will be needed to reach global GHG emission goals and appears to be an important opportunity for hydrogen-powered vehicles to help achieve these goals.

HFCV trucks and buses that follow fixed routes can be more easily commercialized than private light-duty HFCVs because they are centrally fueled, making refueling more practical. But even for long-distance travel, trucks can hold sufficient hydrogen tanks and travel over longer distances without refueling. Also, as most long-haul truck transport occurs over major highways, installing hydrogen refueling infrastructure at existing truck stops could accommodate a high percentage of road transport.

China leads the production and sales of electric (and fuel cell) trucks and buses. Approximately 66,000 electric buses and 60,000 medium/heavy-duty trucks were sold globally in 2022, with China accounting for 80% of the electric bus sales and 85% of electric truck sales (Fig. 4) [13].

Source: IEA, Global Electric Vehicle Outlook 2023

Electric Bus and Truck Registrations and Sales by Region (2015–2022).

1.3 Emissions and well-to-wheel emission pathways

When developing transportation policies intended to reduce GHG emissions, the different GHG emission characteristics of BEVs and HFCVs should be considered. BEVs and HFCVs are often referred to as zero-emission vehicles (ZEVs) as both have zero “tailpipe” emissions. While BEVs and HFCVs eliminate the tailpipe emissions of carbon dioxide and other pollutants, the full fuel cycle emissions may be much higher depending on the technologies and energy sources used to produce electricity and hydrogen. Near-zero full fuel-cycle GHG emissions require that the power sector supplying these vehicles also have near-zero GHG emissions.

Early development of a hydrogen refueling system would more likely involve distributed hydrogen production at the retail service outlet. Depending on the GHG emissions of the electric grid from which the hydrogen is produced, HFCVs that rely on the distributed generation of hydrogen produced via electrolysis will not necessarily provide any GHG emission reductions, and may actually increase them. Instead, electricity and hydrogen produced from renewable energy, or from facilities equipped with CCUS could be considered as will be discussed in the next section. While BEV full fuel cycle emissions also reflect the emissions of the grid, BEVs produce 37% of the emissions of HFCVs if charged from the same electric grid that is used to produce hydrogen for HFCVs. This high sensitivity of HFCV emissions to the emissions of the electric grid means that locality and commercialization strategies could have a large impact on the potential GHG benefits of HFCVs.

Figure 5 shows the relationship between the carbon intensity of the electric grid to the GHG emissions of an HFCV being refueled from electrolyzers using grid electricity and a BEV being charged from the same electricity. Figure 5 also shows, for comparison, the full fuel cycle emissions of a comparable ICE vehicle and the full fuel cycle emissions of an HFCV that is being refueled from hydrogen produced by SMR from natural gas with and without CCUS. The y-axis value for each is 105 gCO2e/mile and 247 gCO2e/mile, respectively. The gCO2e/mi values in the case of fueling the BEV and HFCV -when the vehicle derives its hydrogen via distributed electrolysis- from renewable energy are depicted in the enlarged green circle.

Source: Author’s chart based on Argonne GREET Model and IEA data

HFCV & BEV Full Fuel Cycle GHG Emissions vs. the GHG Emissions of the Electric Grid (Assuming Distributed Generation of Hydrogen from Electricity for HFCVs).

If both BEVs and HFCVs derive their fuel from an electric grid that has essentially zero full fuel-cycle GHG emissions—for example, Norway with its high share of hydroelectric power—then both BEVs and HFCVs have near-zero full fuel-cycle GHG emissions. As the embedded GHG emissions in the grid increase, both BEV and HFCV emissions rise, but HFCV emissions rise much faster if the HFCV is refueled from retail outlets producing hydrogen with electrolysis.

For example, assuming average U.S. power sector emissions, the BEV produces 190 gCO2e/mi compared to 522 gCO2e/mi for the HFCV, whish means, for the U.S. grid, the HFCV produces more GHG emissions than the conventional ICE vehicle while the BEV has less than half the emissions of an ICE. The situation becomes starker for the Chinese electric grid, where an HFCV fueled at a typical service station using electrolysis would have full fuel-cycle GHG emissions that are 70% as high as an ICE vehicle even though a BEV, recharged at the same service station, would provide a 62% emission reduction.

The distributed generation of hydrogen via SMR produces significantly lower emissions than conventional ICEs even without CCUS. SMR without CCUS produces almost 150% more gCO2e/mi compared to SMR with CCUS. As Fig. 5 shows, the GHG emissions of the electric grid must be below 220 gCO2e/kWh before distributed hydrogen generation by electrolysis would provide lower full fuel-cycle GHG emissions than by SMR without CCUS, and below 110 gCO2e/kWh to provide lower full fuel-cycle GHG emissions than by SMR with CCUS. The provided result offers a clear insight into the significant impact of CCUS on the GHG emissions associated with hydrogen production for HFCVs. The comparison between gCO2e/mile value for HFCVs refueled with hydrogen produced via SMR from natural gas without CCUS, but especially the value with CCUS, underscores the critical role of CCUS in mitigating carbon emissions, especially for the countries that have a grid with a high gCO2/kWh value (on the X-axis.)

The observed difference of 142 gCO2e/mile between SMR with CCUS (105 gCO2e/mile) and SMR without CCUS (247 gCO2e/mile) shows the remarkable reduction achieved through the implementation of CCUS. This evidence underscores the critical importance of integrating carbon capture technologies into hydrogen production processes to substantially enhance their environmental sustainability. Countries with average electric grid emissions this low typically have high percentages of hydroelectric or nuclear power, such as is the respective case in Canada and France. If hydrogen were to be produced from natural gas in a merchant hydrogen plant, there would be an opportunity to apply CCUS and achieve low full-fuel cycle emissions. Likewise, low full-fuel cycle emissions could be achieved by hydrogen merchant plants using electricity if they bypassed the electric grid to use electricity directly from low-emission sources such as renewable energy or nuclear power.

In the case of fueling the BEV and HFCV from renewable energy, the green square (where the x and y axes of Fig. 5 meet at the 0.0 point), is enlarged into the green circle to provide the range between 1 to 5 numerically, to show the gCO2e/mi of an HFCV when the vehicle derives its hydrogen via distributed electrolysis from renewable sources, and a BEV when the vehicle derives its electricity from renewables. The y-axis value for each is 3 gCO2e/mi for an HFCV and 1 gCO2e/mi for BEV, respectively. However, producing hydrogen from renewables is costly as seen in Fig. 6, which presents the levelized cost of hydrogen production by technology.

Source: IEA, Global Hydrogen Review 2022 Levelized cost of hydrogen production by technology in 2021 and in the Net Zero Emissions by 2050 Scenario, 2030 and 2050 “The dashed areas reflect the CO2 price impact, based on CO2 prices ranging from USD 15/tonne CO2 to USD 140/tonne CO2 between regions in 2030 and USD 55/ tonne CO2 to USD 250/ tonne CO2 in 2050.” (IEA, Global Hydrogen Review 2022)

Comparison of hydrogen production routes and costs.

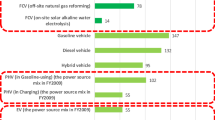

As of the year 2021, the fiscal outlay associated with the production of low-emission hydrogen surpassed that of fossil fuels without CCUS across most geographical domains. The average financial juxtapositions are as follows: unabated natural gas yielding hydrogen at USD 1.0–2.5/kg H2; natural gas integrated with CCUS yielding hydrogen at USD 1.5–3.0/kg H2; and electrolytic processes driven by renewable electricity manifesting a production cost ranging from USD 4.0–9.0/kg H2 (Fig. 6) [28].

Forecasts indicate that, in regions characterized by favorable solar conditions (approximately 2600 full load hours), the cost of producing hydrogen from solar PV sources could potentially decline to less than USD 1.5/kg H2 by 2030 and even further to under USD 1/kg H2 by 2050 [28]. This scenario would render hydrogen production from solar PV sources, in regions characterized by favorable resource conditions, competitive when compared to hydrogen generation from SMR with CCUS by 2030 (red bars in Fig. 6) [28]. The ranges for wind (green bars in Fig. 6) resemble the patterns of solar PV forecasts (yellow bars), however with slightly higher numbers.

The yellow and green bars that show the potential cost reductions in hydrogen production from solar PV and wind (in line with cost reductions of renewable energy, and cost reductions and enhancements in electrolyzer efficiency), respectively, provide us with a picture where hydrogen from renewables can be competitive compared to fossil fuel forms of production (with or without CCUS) portrayed in Fig. 6. In the aggregate, by 2030, the cost of renewable-based hydrogen could settle into a range of USD 1.3–4.5/kg H2 [28]. Reaching these levels of costs in hydrogen production from renewables could enable the realization of the y-axis value (in Fig. 5) of 3 gCO2e/mi for an HFCV feasible.

1.4 Cost of hydrogen delivery

Commercial uptake of HFCVs also hinges on the logistical intricacies of conveying H2 to the HRS. Without adequate investments, the transportation of hydrogen to these stations could remain economically unfeasible. Thus, a holistic approach considering both GHG emissions reduction and cost-effectiveness is crucial in driving the broader adoption of HFCVs. Adoption of HFCVs entail multifaceted challenges for its commercialization. The cost-effective production of hydrogen must be complemented by a well-developed distribution network that ensures its availability at refueling stations. Figure 7 depicts the spectrum of costs for various transport distances; for longer distances, transportation via wider pipelines provides lower costs (USD/kgH2) [28].

Source: IEA, Global Hydrogen Review 2022 (Levelised costs of delivering hydrogen by pipeline and by ship as LH2, LOHC and ammonia carriers, and electricity transmission, 2030)

Cost of Hydrogen Delivery for Various Transport Distances (2030).

The method of delivery is significant as it has a considerable impact on the cost of the hydrogen. Centralized hydrogen production at a large merchant plant can produce hydrogen at a lower cost due to economies of scale, however, it adds to the cost to deliver the hydrogen to the point of use because of the distance. On the other hand, decentralized (distributed) production facilities produce hydrogen on-site, but the production cost of the hydrogen is higher in this case due to low utilization since the production volumes are lower. Hence, there is a trade-off between the hydrogen production options and the hydrogen delivery options. Therefore, as governments, industries, and researchers pursue the advancement of hydrogen technologies, it becomes evident that addressing the economic feasibility of hydrogen production, delivery, and distribution is pivotal for a comprehensive transition toward a cleaner transportation future.

1.5 Potential hydrogen supply via renewable sources (solar PV and wind)

In the event that the electrolyzer initiatives currently in progress materialize and the projected expansion in manufacturing capacities is successfully executed, the associated expenses for electrolysers could potentially experience a reduction of approximately 70% by the year 2030 [28], in contrast to the present conditions. Concurrently, the anticipated decline in the expense associated with renewable energy deployment can contribute to a noteworthy decrease in the cost of hydrogen production sourced from renewables (Fig. 6). As a result, the cost of renewable-based hydrogen may potentially range between USD 1.3–4.5/kg H2 by the same time frame (Fig. 6).

With reference to the depicted supply costs illustrated in Fig. 7, Fig. 8 details on the corresponding annual hydrogen supply (Mt H2/year). The left graph delineates the cost of hydrogen production stemming from hybrid solar PV and wind systems, considering various alternatives of minimum load projections by the year 2030. The graph on the right focuses on offshore wind systems, and within the offshore wind chart, a smaller inset (indicated by the red rectangle and encompassing the X-axis span of 0–1000) demonstrates the worldwide potential to produce hydrogen from offshore wind installations at costs below USD 3/kg H2, characterized by capacity factors within the range of 50–75%. Accordingly, the projected hydrogen supply attainable from offshore wind sources could reach 250 million tonnes by the year 2030 [28].

Source: IEA, Global Hydrogen Review 2022

Potential Hydrogen Supply from Solar PV and Wind (given the forecasted supply costs in Fig. 6).

The transition towards cleaner energy sources and the increasing integration of renewable energy would likely have a significant impact on the uptake of HFCVs. As renewable energy sources like solar and wind become more dominant in the energy mix, this could trigger a growing interest in utilizing these sources to produce hydrogen. This ‘green hydrogen’ production aligns with the broader goal of reducing carbon emissions. The availability of green hydrogen produced from renewable sources could make HFCVs more attractive in terms of environmental sustainability addressing concerns about emissions and air quality. Moreover, based on the forecasts discussed, the growth in renewable energy installations (solar PV and wind) contributes to a more favorable context for producing green hydrogen efficiently via enhancements in electrolyzer efficiency and at lower costs. This could pave the way for the fueling infrastructure for HFCVs to become more accessible and economically viable.

The expansion of renewable energy sources would require corresponding advancements in hydrogen production, storage, and distribution technologies to support the growth of HFCVs effectively. In essence, the increased availability of green hydrogen due to the rise of renewable energy could positively influence the adoption of HFCVs, as these vehicles align well with the goals of a low-emission and sustainable transportation sector. However, challenges such as intermittent renewable energy generation and the need for energy storage solutions still need to be addressed to ensure a reliable supply from the variable renewable energy resources (VRE) in order to supply green hydrogen for HFCVs.

1.6 Caveat of variable renewable energy (VRE)

As the transition to clean energy gains momentum, global investments are progressively shifting towards this domain. According to World Energy Investment 2023 [29], a significant milestone is anticipated this year: for the first time, investments in renewable energy are projected to surpass those in fossil fuels. This represents a noteworthy indicator as these investments constitute the foundation of the future. In 2023, a total investment of approximately USD 1.7 trillion is expected across various sectors under the clean energy umbrella, encompassing renewable energy, nuclear, grids, energy storage, low-emission fuels, efficiency enhancements, and electrification. Slightly more than one trillion dollars will be allocated to investments in fossil fuels.

Electricity generated from wind and solar PV sources is projected to double by 2027, contributing up to 20% of the global electricity supply, and renewable energy is on course to surpass coal and become the predominant source of electricity generation by the year 2025 [30]. Electricity generation from renewable sources has now become the most cost-effective investment for majority of countries. Consequently, ~ 90% of the newly established power plants globally in 2022 were solar PV and wind energy installations [30]. This indicates a significant transition to renewable energy sources.

Solar PV continues to lead the way; according to the projections for 2023, it is expected that two-thirds of the increase in global renewable energy capacity will stem from solar. In the realm of wind energy, the trajectory points toward a substantial upswing with a record-breaking year, as there will be an introduction of 107 GW capacity, signifying a remarkable 70% increase [31].

The availability and expansion of variable renewable energy sources, solar PV, and wind bear the possibility to play a pivotal role in producing green hydrogen, however, in the context of electricity provisioning, solar PV and wind power sources are inherently characterized by their variable output, leading to intermittent production patterns, rendering them non-continuous in their energy supply. This intermittency can pose challenges for energy grid management and requires additional strategies for balancing supply and demand to ensure a stable and reliable electricity supply.

The share of VRE grew at record levels in the recent years, and there will be a growing share of wind and solar in total electricity generation. Hence, “What is the meaning of increasing VRE for the electricity sector?” comes forward as a key question, as the answer to this would be one of the most significant factors affecting future hydrogen supply, besides other important factors such as electrolyzer technology, policy and regulation, infrastructure development, cost-competitiveness, carbon emission targets, research and innovation, international collaboration, and geopolitical factors.

Assimilating modest levels of VRE penetration poses a relatively straightforward task, as the infrastructure can effectively accommodate such additions. However, in instances marked by elevated levels of VRE integration, intricate challenges manifest, predominantly relating to the domains of energy storage and demand-side response. Hence, the expanding integration of wind and solar energies necessitates a strong transformation within electricity systems. Therefore, a second key question arises: how shall the integration of VRE be orchestrated within electricity frameworks in an economically optimal manner, given the inherent intermittency of solar and wind generation during periods of insufficient sunlight or wind activity? The answer to this inquiry, serving as a determinant, will influence emissions and the operational dynamics of current systems, and ultimately, it will define the structure of future energy systems, which will play a crucial role in enabling low-emission transportation.

Over the long term, the adoption of HFCVs utilizing renewable energy-derived hydrogen could be closely linked to the overall structure of the future energy system, where the increasing contribution of wind and solar power to total electricity generation will be growing—necessitating a flexible system design since solar PV and wind power sources provide variable output. Hydrogen -by its very nature as an energy carrier- has the potential to play a key role in this junction, incorporating high fractions of VRE into the energy system serving as a prominent cost-effective option for energy storage, the other option being battery storage.

Both hydrogen and battery storage technologies have their merits and can be utilized in various scenarios depending on factors like application requirements, available infrastructure, cost considerations, and technological advancements. While battery storage is generally more efficient and suitable for rapid response applications, hydrogen storage offers advantages for longer-term energy storage and situations where grid stability and large-scale energy needs are a priority. Regarding policy and regulatory aspects, government incentives will be very important to create operational flexibilities that will be needed in order to address the challenges coming from the increasing share of renewables.

Hydrogen is almost entirely supplied from fossil fuels for the time being and producing hydrogen from renewable energy is costly today, however, the energy landscape is rapidly changing as the clean energy transition is becoming a reality. The contemporary objective resides in the endeavor to achieve a substantial scale of hydrogen production devoid of the concomitant emission of greenhouse gases, most notably carbon dioxide.

The utilization of renewable energy resources, particularly in regions abundant in solar PV and wind potential, could be strategically realized by coupling an electrolyzer with a dedicated, off-grid renewable system. The progressively declining cost dynamics of renewable technologies coupled with the inherent advantage of evading the high expenses linked to grid connection render off-grid systems conducive to cost-effective electricity generation. This, in turn, drives the operation of an electrolyzer for hydrogen production at a low cost. It is at this very junction where hydrogen generated through renewable electricity using an electrolyzer plays a crucial role. This method would be particularly effective in regions endowed with robust solar PV and wind resources.

In this context, the generation of hydrogen through renewable electricity could emerge as an enabler for the assimilation of substantial proportions of VRE into the energy landscape as hydrogen bears the potential to serve as a prominent cost-effective option for energy storage, offering the possibility of extended time-range of days, weeks, months, and seasonal storage. This storage capacity facilitates the effective incorporation of VRE into the energy matrix, aligning with the imperative to enhance the operational flexibility -flexibility being the keyword here- of the power system, and catering to power and heat requirements. Consequently, the potential to harness surplus VRE that would otherwise be curtailed during periods of supply excess can be achieved, facilitating the utilization of substantial hydrogen storage over protracted intervals.

Nonetheless, the proposition of utilizing low-cost electricity derived from VRE introduces a caveat—the propensity for low utilization which increases the capital costs per unit of hydrogen output. Thus, while the realization of cost-effectiveness through declining electrolyzer costs, robust utilization rates (at distinct production sites), and economical renewable electricity is conceivable for hydrogen production from renewable sources, the applicability of such outcomes needs detailed evaluation in the context of production sites in regions characterized by favorable solar and wind resource conditions.

Overall, through facilitating the integration of renewable energy and enabling power generation, hydrogen can assume a pivotal role in the decarbonization of not only transport but also challenging-to-decarbonize sectors other than transportation, such as residential areas (comprising building heat and power), and industrial domains of the economy that require high-grade heat. This, in the long-term, would be the realization of the “Hydrogen Economy”Footnote 2 where the hydrogen economy refers to a theoretical framework or concept in which hydrogen is widely used as a clean and versatile energy carrier. This entails producing, storing, and utilizing hydrogen in various applications to replace or complement traditional fossil fuels.

1.7 Potential hydrogen supply via CCUS

In the year 2021, global hydrogen demand reached 94 million tonnes (Mt), predominantly met by hydrogen generation derived from unabated fossil fuel sources. Of this, 62% was produced from natural gas without CCUS, 19% originated from coal, and 18% was a by-product of naphtha reforming processes. Considering the array of policies and climate pledges by governments worldwide, the IEA postulates that hydrogen demand could escalate to 115 Mt by the year 2030. In order to fulfill the climate commitments articulated by various governments globally thus far, and to align with the trajectory towards achieving net-zero emissions by 2050, an estimated 200 Mt of hydrogen would be required by 2030 [28].

As of 2021, the production of low-emission hydrogen was less than 1 Mt. This volume was entirely sourced from facilities employing fossil fuels in conjunction with CCUS methodologies, with only an additional 35 kt of hydrogen generated through water electrolysis. Notably, the landscape of low-emission hydrogen production is undergoing rapid expansion with a pipeline of projects. Should all ongoing projects realize, projections indicate that the annual output of low-emission hydrogen could increase to 16–24 Mt by 2030, with approximately 9–14 Mt attributed to electrolysis and 7–10 Mt to fossil fuels integrated with CCUS technologies [28].

At present, nearly 45 Mt of carbon dioxide are being captured within 35 CCUS facilities. In the scenario where projects unveiled during the span of 2021 to 2022 (up until the third quarter) materialize as planned, an estimated 80 Mt of CO2 could be captured from hydrogen production by 2030. Excluding consideration of under developmentFootnote 3 projects, and focusing solely on the operational capacities of hydrogen production initiatives with disclosed start years for operation, it is conceivable that the production of low-emission hydrogen from CCUS-equipped facilities could amount to around 7 Mt of hydrogen by 2030 (as depicted in Fig. 9) [28].

Source: IEA, Global Hydrogen Review 2022

Past and planned capacity of CCUS-equipped hydrogen production facilities, 2000–2030.

The presented analysis provides a comprehensive snapshot of the current state and potential future trajectories of global hydrogen demand and production, particularly in the context of environmental considerations. The breakdown of hydrogen production sources underscores the prevailing reliance on unabated fossil fuel sources, primarily natural gas and coal, contributing to a significant portion of the overall hydrogen demand in 2021. This reality prompts a critical reflection on the energy transition imperatives highlighted in climate pledges and policies across nations.

The projection of hydrogen demand escalation by the IEA to 115 Mt by 2030 echoes the urgency and magnitude of global efforts to curb emissions. The alignment of hydrogen demand with climate commitments further accentuates the profound impact and interplay of energy policies and environmental targets on future hydrogen landscape. The stipulated requisite of 200 Mt of hydrogen by 2030 to achieve net-zero emissions by 2050 is indicative of the scale of transformation required in the energy sector and the pivotal role hydrogen is anticipated to play in this transition.

The contrast between the current production volume of low-emission hydrogen and the ambitious projections highlight the evolving nature of hydrogen production technologies and the rapidly advancing pipeline of projects. The commendable progress in low-emission hydrogen production, particularly through water electrolysis, highlights a promising avenue towards sustainable hydrogen generation. The prospective increase to 16–24 Mt of annual low-emission hydrogen production by 2030 demonstrates the potential for transformational change in the hydrogen sector, emphasizing the transition from fossil fuel-based to low-emission hydrogen sources.

The potential to capture substantial amounts of carbon dioxide from hydrogen production processes via CCUS signals a proactive approach towards mitigating emissions from hydrogen generation. The scenario analysis involving unveiled projects accentuates the significance of project realization in attaining CO2 capture goals, thereby highlighting the intricate interdependence of technology implementation and environmental objectives.

Ultimately, this analysis illuminates the intricate web of hydrogen demand, production sources, environmental aspirations, and technological advancements. The synthesis of these elements reflects the complex landscape that policymakers, industry stakeholders, and researchers navigate to align hydrogen production with the imperatives of sustainable development and global climate commitments.

2 Conclusions

HFCVs, being relatively latecomers with only about a decade of commercial availability, could potentially exhibit strong consumer appeal once challenges related to vehicle cost and fuel availability (including production and delivery costs) are overcome. Government programs aimed at addressing these challenges hold the potential to achieve regional success, rendering HFCVs viable options for consumers. Regional successes from current programs, for example in California, could stimulate programs in other regions and countries resulting in a growing HFCV fleet that encompasses light-duty vehicles, trucks, and buses. While this is occurring, BEVs suit the commuting needs of many light-duty vehicle consumers and are also likely to experience continued growth.

HFCVs are much closer to current ICEs from the consumer perspective. Their range is predominantly longer than most BEVs and refueling times are similar to ICEs. These traits position HFCVs as a more intuitive consumer preference for replacing conventional BEVs, particularly due to their suitability for long-distance travel, contingent upon widespread access to hydrogen refueling stations. The raison d'être for developing HFCVs as complementary or replacements for BEVs is their potential consumer appeal compared to BEVs.

Nonetheless, a substantial distinction exists between BEVs and HFCVs in terms of their potential to mitigate greenhouse gas emissions. Although both BEVs and HFCVs eliminate direct “tailpipe” emissions of carbon dioxide and other pollutants, the comprehensive emissions across the entire fuel cycle may significantly differ, contingent upon the technologies and energy sources engaged in the production of electricity and hydrogen. Remarkably, BEVs display substantially reduced full fuel-cycle GHG emissions in comparison to ICEs, even in instances where the electric grid they rely upon is characterized by a substantial proportion of fossil fuel-based power generation. In cases where an HFCV infrastructure relies on decentralized generation facilitated by electrolyzers and if the electric grid predominantly relies on hydrocarbon-based electricity generation, the GHG emissions of HFCVs have the potential to exceed those of conventional ICE vehicles and far surpass the emissions of BEVs recharging from the same electric grid.

The analysis of hydrogen production through SMR utilizing natural gas demonstrates that the gCO2e/mile of an HFCV refueled with hydrogen produced via SMR with CCUS stands at 105 gCO2e/mile, compared to 247 gCO2e/mile without CCUS. The absence of CCUS in SMR leads to an increase of nearly 150% in gCO2e/mi in contrast to involving CCUS. This quantification of emissions highlights the substantial carbon footprint reduction potential achievable through the adoption of CCUS, emphasizing its significance in the context of hydrogen-based transportation and the broader efforts to address climate change.

It is recommended for national pilot initiatives to rely on decentralized hydrogen generation in cases where the emissions from their power grid are characterized by their low level or are anticipated to attain such a status in the near future. In the absence of this condition, producing hydrogen from merchant facilities utilizing electricity generated through renewable energy sources, nuclear power, or fossil fuels with CCUS would be a more propitious approach. If the H2 production of the HFCV ecosystem gets “locked into” distributed generation via the grid due to infrastructure investments and other factors, the ability of HFCVs to reduce GHG emissions could be compromised. Thus, during the formulation of transport policies aimed at mitigating GHG emissions, it is crucial to account for the distinct GHG emission characteristics exhibited by BEVs and HFCVs.

As the surge in renewable energy installations is dominated by solar PV and wind energy, integration of these VRE raises key questions about electricity provisioning, hydrogen production, and the overall energy system structure. The transition to renewables necessitates addressing challenges related to energy storage and demand-side response, as the demand-side response seeks to establish a more flexible and balanced electricity system, and optimizing resource utilization. At this juncture, the role of hydrogen in integrating renewables, enhancing energy storage and extending it to seasonal level, and enabling low-emission transportation could be pivotal in shaping the future energy landscape, which, on a large scale, will hinge on governmental decisions and incentives.

Lastly, from a theoretical standpoint, hydrogen possesses the potential to serve as a critical instrument for decarbonizing challenging-to-decarbonize sectors, including but not limited to steel, cement, and petrochemical industries, alongside transportation, industrial operations, and residential consumption—thereby contributing to the decarbonization of the entire economy. The realization of a hydrogen-centric framework within the ‘Hydrogen Economy’ concept, which currently remains within the realms of theory, may hold the promise of transitioning from abstraction to practicality over the upcoming decades, thus catalyzing a paradigm shift.Footnote 4 Such a shift would signify a transformative departure from the existing system, potentially encompassing not only the realm of transportation but also permeating across every facet of economic sectors. Consequently, a pivotal question emerges: will the momentum of the transition towards renewable energy be sufficiently robust to instigate a paradigmatic transformation, leading to a departure from the existing modus operandi and culminating in a new era characterized by net-zero emissions?

Data avaılabılıty

The International Energy Agency (IEA) dataset used and analysed during the current study are available immediately upon request. Respectfully, Mehmet Dogan Ucok.

Notes

cited in [20

The Hydrogen Economy envisions a shift towards a sustainable energy system where hydrogen, often generated through renewable sources, serves as a means to store and distribute energy, power fuel cells for electricity generation, and contribute to decarbonization efforts across various sectors, including transportation, industry, and residential use. The idea of hydrogen economy from governments, industry and academia that had started in the 1970s, and has been on the rise in the last decade, to further develop of hydrogen’s role as a clean energy carrier.

Under development projects: Projects that only a co-operation agreement among stakeholders has been announced, but a start year for hydrogen production not provided.

Thomas Kuhn's concept of a "paradigm shift" (in his influential book "The Structure of Scientific Revolutions") refers to a fundamental change in the dominant framework or perspective that guides scientific research and understanding within a particular field. Kuhn introduced this term in 1962. He argued that scientific progress is not solely an accumulation of new knowledge but rather a process of shifting from one established scientific paradigm to another. A paradigm shift occurs when anomalies, inconsistencies, or limitations in the existing paradigm become significant enough to challenge its validity and provoke the emergence of a new and more comprehensive framework. This shift involves a change in the fundamental assumptions, methods, and theories that guide scientific inquiry, leading to a transformation in the way scientific problems are approached, understood, and solved. Kuhn's work has had a profound impact on the philosophy of science and has been widely discussed and debated in various academic disciplines.

References

United Nations (UN). Sustainable development goals. The 17 Goals; 2016. https://sdgs.un.org/goals.

United Nations (UN) Global sustainable Development Report (GSDR); 2016. https://sdgs.un.org/gsdr.

Intergovernmental Panel on Climate Change (IPCC). IPCC press release, IPCC sixth assessment report working group III: Mitigation of Climate Change. Geneva; 2022. https://www.ipcc.ch/report/ar6/wg3/resources/press/press-release/.

International Energy Agency (IEA). Net Zero by 2050: A roadmap for the global energy sector. Paris: IEA; 2021, p. 3. https://www.iea.org/reports/net-zero-by-2050.

Stabinsky D, Juan P. Hoffmaister, Establishing institutional arrangements on loss and damage under the UNFCCC: the Warsaw International Mechanism for Loss and Damage. Int J Global Warming. 2015;8(2):295–318. https://doi.org/10.1504/IJGW.2015.071967.

van der Geest K, Warner K. Loss and damage from climate change: emerging perspectives. Int J Global Warming. 2015;8(2):133–40.

Hauser M, Orth R, Seneviratne S. Role of soil moisture versus recent climate change for the 2010 heat wave in western Russia. Geophys Res Lett. 2016;43(6):2819–26. https://doi.org/10.1002/2016GL068036.

International Energy Agency (IEA). World energy outlook. Paris: IEA; 2012. p. 25. https://www.iea.org/reports/world-energy-outlook-2012.

International Energy Agency (IEA). Net Zero by 2050. Paris: IEA. 2021. p. 61.

International Energy Agency (IEA). CO2 emissions from trucks and buses, 2000-2021, and 2030 in the Net Zero Scenario. Paris: IEA; 2022. https://www.iea.org/data-and-statistics/charts/co2-emissions-from-trucks-and-buses-2000-2021-and-2030-in-the-net-zero-scenario.

European Commission. Fit for 55 - Delivering the EU’s 2030 climate target on the way to climate neutrality; 2021. https://www.fao.org/faolex/results/details/en/c/LEX-FAOC211249/.

European Parliament News. EU ban on the sale of new petrol and diesel cars from 2035 explained; 2023. https://www.europarl.europa.eu/news/en/headlines/economy/20221019STO44572/eu-ban-on-sale-of-new-petrol-and-diesel-cars-from-2035-explained.

International Energy Agency (IEA). Global EV Outlook 2023. Paris: IEA; 2023. https://www.iea.org/reports/global-ev-outlook-2023.

Jenn A, Springel K, Gopal AR. Effectiveness of electric vehicle incentives in the United States, Energy Policy. 2018;119:349–56. ISSN: 0301–4215.

Stokes LC, Breetz HL. Politics in the U.S. energy transition: case studies of solar, wind, biofuels and electric vehicles policy. Energy Policy. 2018;113:76–86.

International Energy Agency (IEA). Energy technology perspectives. Paris: IEA; 2023. https://www.iea.org/reports/energy-technology-perspectives-2023.

Liu X, Reddi K, Elgowainy A, Lohse-Busch H, Wang M, Rustagi N. Comparison of well-to-wheels energy use and emissions of a hydrogen fuel cell electric vehicle relative to a conventional gasoline-powered internal combustion engine vehicle. Int J Hydrog Energy. 2020;45(1):972–83.

International Energy Agency (IEA). Global hydrogen review. Paris: IEA; 2022. https://www.iea.org/reports/global-hydrogen-review-2022.

Doucette RT, McCulloch MD. Modeling the CO2 emissions from battery electric vehicles given the power generation mixes of different countries. Energy Policy. 2011;39(2):803–811. ISSN: 0301-4215. https://doi.org/10.1016/j.enpol.2010.10.054.

Woo J, Choi H, Ahn J. Well-to-wheel analysis of GHG emissions for electric vehicles based on electricity generation mix: A global perspective. Transp Res Part D Transp Environ. 2017;51:340–50.

Faria R, Marques P, Moura P, Freire F, Delgado J, de Almeida AT. Impact of the electricity mix and use profile in the life-cycle assessment of electric vehicles. Renew Sustain Energ Rev. 2013;24:271–87. https://doi.org/10.1016/j.rser.2013.03.063.

Hawkins TR, Singh B, Majeau-Bettez G, Strømman AH. Comparative environmental life cycle assessment of conventional and electric vehicles. J Ind Ecol. 2013;17:53–64. https://doi.org/10.1111/j.1530-9290.2012.00532.x.

Wang Q, Xue M, Lin B-L, Lei Z, Zhang Z. Well-to-wheel analysis of energy consumption, GHG and air pollutants emissions of hydrogen fuel cell vehicle in China. J Cleaner Prod. 2020;275:123061. ISSN: 0959-6526. https://doi.org/10.1016/j.jclepro.2020.123061.

Yoo E, Kim M, Song HH, Well-to-wheel analysis of hydrogen fuel-cell electric vehicle in Korea. Int J Hydrog Energ. 2018;43(41):19267–78. ISSN: 0360-3199. https://doi.org/10.1016/j.ijhydene.2018.08.088.

International Energy Agency (IEA). Renewables. In: Analysis and forecast to 2027. Paris: IEA; 2022. https://www.iea.org/reports/renewables-2022.

Cozzi L, Petropoulos A, Paoli L, Huismans M, Dasgupta A, IEA commentary. As their sales continue to rise, SUVs’ global CO2 emissions are nearing 1 billion tonnes. 2023. https://www.iea.org/commentaries/as-their-sales-continue-to-rise-suvs-global-co2-emissions-are-nearing-1-billion-tonnes.

Giacobone B. Electrifying trucking will mean sacrificing critical weight for heavy batteries, eating into already-slim margins. Bus Insider. 2023. https://www.businessinsider.com/article-url.

International Energy Agency (IEA). Global hydrogen review. Paris: IEA; 2022. https://www.iea.org/reports/global-hydrogen-review-2022.

International Energy Agency (IEA). World energy investment report. Paris: IEA; 2023. https://www.iea.org/reports/world-energy-investment-2023.

International Energy Agency (IEA). Renewables. Paris: IEA; 2022. https://www.iea.org/reports/renewables-2022.

IEA Renewable Energy Market Update, Outlook for 2023 and 2024.

Acknowledgement

The views and opinions expressed in this paper are solely those of the author and do not necessarily reflect the official views or opinions of the institution with which the author is affiliated.

Author information

Authors and Affiliations

Contributions

The research paper is written solely by myself. Respectfully, Mehmet Dogan Ucok

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Üçok, M.D. Prospects for hydrogen fuel cell vehicles to decarbonize road transport. Discov Sustain 4, 42 (2023). https://doi.org/10.1007/s43621-023-00159-1

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s43621-023-00159-1