Abstract

We aim to compare marginal distributions of a bivariate random vector (X, Y) with reference to their hazard rates, \((h_F(t), h_G(t))\). In many applications, it is likely that the marginal hazard rates are ordered, e.g., \(h_F(t) \le h_G(t)\). We consider two U-statistics based tests for testing equality of the marginal hazards against the alternative that they are ordered. Further, we compare these tests with the existing W and S tests when X and Y are assumed to be independent. The two proposed statistics are also extended to cover situations when the pair (X, Y) is subjected to independent univariate censoring. We provide extensive simulation studies based on copulae where the power performance of these tests is assessed. The marginal distributions considered are Weibull, linear failure rate, Gompertz and three other families of distributions based on copulae. We apply the tests to two real data examples.

Similar content being viewed by others

References

Bagai I, Kochar SC (1986) On tail-ordering and comparison of failure rates. Commun Stat Theory Methods 15(4):1377–1388. https://doi.org/10.1080/03610928608829189

Cai J, Kim J (2003) Nonparametric quantile estimation with correlated failure time data. Lifetime Data Anal 9:357–371

Callaert H, Veraverbeke N (1981) The order of the normal approximation for a studentized U-Statistic. Ann Stat 9(1):194–200

Cheng KF (1985) Tests for the equality of failure rates. Biometrika 72(1):211–215

Chikkagoudar MS, Shuster JS (1974) Comparison of failure rates using rank tests. J Am Stat Assoc 69:411–413

Frees EW, Carriere JF, Valdez EA (1996) Annuity valuation with dependent mortality. J Risk Insur 63(2):229–261

Hofert M, Kojadinovic I, Maechler M, Yan J (2023) copula: multivariate Dependence with copulas. R package version 1.1-2, https://CRAN.R-project.org/package=copula

Hoeffding W (1948) A class of statistics with asymptotically normal distribution. Ann Math Stat 19:293–325

Huang H, Zhao Y (2018) Empirical likelihood for the bivariate survival function under univariate censoring. J Stat Plan Inference 194:32–46

Huster WJ, Brookmeyer R, Self SG (1989) Modelling paired survival data with covariates. Biometrics 45(1):145–156

Kalbfleisch JD, Prentice RL (2002) The statistical analysis of failure time data, 2nd edn. Wiley, New York

Kochar SC (1978) Distribution-free comparisons of two probability distributions with reference to their hazard rates. PhD thesis

Kochar SC (1979) Distribution-free comparison of two probability distributions with reference to their hazard rates. Biometrika 66(3):437–41

Kochar SC (1981) A new distribution-free test for the equality of two failure rates. Biometrika 68(2):423–426

Kulathinal S, Dewan I (2023) Weighted U-statistics for likelihood-ratio ordering of bivariate data. Stat Pap 64:705–735. https://doi.org/10.1007/s00362-022-01332-w

Le CT, Lindgren BR (1996) Duration of ventilating tubes: a test for comparing two clustered samples of censored data. Biometrics 52(1):328–334

Lee AJ (2020) U-statistics: theory and practice. CRC Press, Cambridge

Lehmann EL (1951) Consistency and unbiasedness of certain nonparametric tests. Ann Math Stat 22:165–179

Lai CD, Xie M (2006) Stochastic ageing and dependence for reliability. Springer, New York

Li R, Cheng Y, Chen Q, Fine J (2017) Quantile association for bivariate survival data. Biometrics 73:506–516. https://doi.org/10.1111/biom.12584

Luciano E, Spreeuw J, Vigna E (2008) Modelling stochastic mortality for dependent lives. Insur Math Econ 43:234–244

Nelsen RB (1999) An introduction to copulas. Springer, New York

R Core Team (2022) R: a language and environment for statistical computing. R Foundation for Statistical Computing, Vienna

Shaked M, Shanthikumar JG (2007) Stochastic orders. Springer, New York

Therneau T (2023) A package for survival analysis in R. https://cran.r-project.org/web/packages/survival/index.html

Acknowledgements

We wish to thank the Society of Actuaries, through the courtesy of Edward (Jed) Frees and Emiliano A. Valdez, for providing the Canadian data used in this paper. The authors would like to thank the referees and the editor for their constructive comments that have led to the improved version of the manuscript.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

On behalf of all authors, the corresponding author states that there is no conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

LK’s work was carried out while she was a visiting scientist at the Indian Statistical Institute, New Delhi, India.

Supplementary Information

Below is the link to the electronic supplementary material.

Appendices

Symmetric Kernel and Asymptotic Distribution of \(U_{fc}\) (10)

The symmetric version of the kernel (9) is obtained by averaging over 6 combinations, as defined below.

In order to obtain the asymptotic variance of \(U_{fc}\), we first define and derive \(\psi _{fc}(z_i)\) as follows.

Then

and

If \(E[\psi _{fc}(Z_i)]^2 < \infty \) and \(\sigma _{1c}^2>0,\) then \(\sqrt{n} (U_{fc}-E(U_{fc})) \xrightarrow {d} N(0, 9\sigma _{1c}^2) \ as \ n \rightarrow \infty .\) Under the null hypothesis, \(E(U_{fc}) = 0.\)

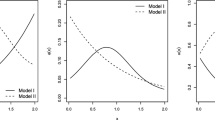

Otitis media data. Ratio of the Kaplan-Meier estimates of the survival functions of survival times of the surgically inserted ventilating tubes in the left ear (X) to that in the right ear (Y). Black and red colour show the estimated ratios for the control and the treatment groups, respectively

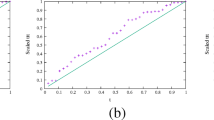

Insurance data. Ratio of estimates of survival functions of ages of a couple at contract initiation for the entire data (ALL) and a randomly selected sample of size 500 (Sample), for \(20\%\) censoring imposed on the complete data and on the selected sample (ALL 20% and Sample 20%)

Theorem 2

When \(\sigma _{1c}^2 = Var[\Psi _{fc}(Z_i)] >0\), \(\sqrt{n}(U_{fc} - E(U_{fc})) \xrightarrow {d} N(0,9\sigma _{1c}^2) \ as \ n \rightarrow \infty \). Also, \(E(U_{fc}) = 0\) under \(H_{0f}.\)

W and S Tests

We review tests W and S (Kochar [13, 14]), and provide computational details here. Let \(X_1, X_2,...X_n\) and \(Y_1, Y_2,..., Y_m\) be independent random samples from the two distributions F and, G respectively. Let \(X_{(1)}, X_{(2)},...,X_{(n)}\) be the order statistics of the X-sample and \(Y_{(1)}, Y_{(2)},...,Y_{(m)}\) be the order statistics of the Y-sample. The U-statistic W in terms of rank representation, is defined as

where \(R_{(i)}, i= 1,2,...,n\) and \(S_{(j)},j=1,2,...,m\) are the ranks of \(X_{(i)}\) and \(Y_{(j)},\) respectively, in the combined sample of X and Y observations. Detailed proof of the above representation is available in Kochar [12].

To compare the performance of the proposed tests with the W test, we take \(n=m.\) Hence, under \(H_0, E(W)=0,\) and

Asymptotically as \(n \rightarrow \infty \), \(\sqrt{2n} ~ W \sim N(0, 128/105).\)

Let \(Y_{(1)}, Y_{(2)},...,Y_{(m)}\) be the order statistics of the Y-sample, and let \(\tilde{S}_{(j)}\) denote the rank of the \(Y_{(j)}\) in the combined increasing arrangement of \(X's\) and \(Y's\). Then the S-statistic can be expressed as

where \(a_j = \frac{1}{2}+log\{1-j/(m+1)\}.\) Under \(H_0\) and when \(n=m\),

where the matrix \(\Omega =((w_{ij})) (i,j = 1,2,...,n),\) has \(w_{ij}=i(m+1-j)=w_{ji}\) for \(i\le j\) and \(a' = (a_1, a_2,...,a_n).\) Then, asymptotically, as \(n \rightarrow \infty \), \((S-E(S))/\sqrt{V(S)} \sim N(0,1).\)

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Kulkarni, L., Kulathinal, S. & Dewan, I. U-statistics Based Tests for Marginal Hazard Rate Orderings of Two Dependent Variables. J Stat Theory Pract 18, 19 (2024). https://doi.org/10.1007/s42519-024-00372-9

Accepted:

Published:

DOI: https://doi.org/10.1007/s42519-024-00372-9