Abstract

Global climate is changing, and the occurrence of climate disasters has been rising. There is growing concern that climate change is expected to increase the frequency and intensity of weather events. Yet, the consequential effects of disasters and the ensuing implications of policymakers’ responses remain unclear. While the majority of research on climate change is ex ante, this paper explores the ex post transmission of disaster damages on economic conditions. In doing so may offer a glimpse of key, future policy options around how a disaster shock influences economic conditions, not only with regards to how a disaster affects output, as in the existing research, but also to aid policy makers and the public to further understand the influences on inflation, interest rate and economic policy uncertainty (EPU). Using a multivariate regression, we find that the impact of a natural disaster on EPU is positive and statistically significant during an expansionary phase while controlling for other determinants. Using a non-linear VAR model with local projections (LP), the aftermath of a disaster is estimated to marginally decrease output and increase inflation during an expansionary state. Accordingly, the empirical findings suggest the interest rate set by the U.S. Federal Reserve (Fed) remains relatively unchanged to a disaster shock, which is operating in a manner that is proportional to the magnitude of change in output and inflation. Consistent with the multivariate regression model, the VAR-LP demonstrates that the impact of a natural disaster magnifies the increase in EPU during periods of economic expansion.

Similar content being viewed by others

Notes

EPU is seasonally adjusted via ARIMA X-12 algorithm from the U.S. Census Bureau.

Costly disaster data is set to \(\ln D_{t} = {\sum }_{i=1}^{n} \ln (1+cost_{i,t}^{data})\) considering the data is non-negative.

While the NOAA disaster data uses a threshold of $1 Billion, these damages represent the majority of damage costs. According to the NOAA website, ”Even though $1B is an arbitrary threshold, these specific events account for the majority (> 80%) of the damage from all recorded U.S. weather and climate events.” See https://www.ncdc.noaa.gov/billions/faq.

The hypothesis of normality is not accepted using the Jarque Bera test or Shapiro-Wilk test (p-value is 0.00 for both tests).

All data used in the models are available from the authors upon request.

This has the potential benefit of capturing the short-term effects that a disaster has on the economy, as opposed to using annual data as in the majority of studies. Disaster shocks, when they occur, can transmit rapidly and may also have long-term effects. The model includes disaster data defined in real cost terms, which is a preferred measure to condition on the magnitude of the disaster than count data at annual frequency.

Note that Hailemariam et al. (2019) also consider the oil price, which is not done here to maintain a parsimonious model.

The robust regression is based on an MM-estimator with a design adaptive scale estimate (Koller and Stahel 2011) using iteratively reweighted least squares estimation.

Note that we abstract from deterministic terms with the exception of the intercept term for expositionary purposes.

The output gap for quarterly data is based on the real GDP potential provided by the Congressional Budget Office (FRED mnemonic GDPPOT) and real GDP (FRED mnemonic GDPC1). This is consistent with the U.S. Federal Reserve, see https://research.stlouisfed.org/publications/page1-econ/2021/05/03/minding-the-output-gap-what-is-potential-gdp-and-why-does-it-matter. The output gap at monthly frequency is based on industrial production via the HP filter, where the trend is based on λ = 1,600, a standard value for data at quarterly frequency (see e.g. Ravn and Uhlig 2002)

References

Albala-Bertrand J (1993) Natural disaster situations and growth: A macroeconomic model for sudden disaster impacts. World Dev 21(9):1417–1434

Albala-Bertrand J (2007) Globalization and localization: an economic approach. In: Handbook of Disaster Research, pp 147–167

An S-I, Wang B (2000) Interdecadal change of the structure of the ENSO mode and its impact on the ENSO frequency. J Clim 13(12):2044–2055

Antonakakis N, Chatziantoniou I, Filis G (2013) Dynamic co-movements of stock market returns, implied volatility and policy uncertainty. Econom Lett 120(1):87–92

Antonakakis N, Chatziantoniou I, Filis G (2014) Dynamic spillovers of oil price shocks and economic policy uncertainty. Energ Econom 44:433–447

Auerbach A, Gorodnichenko Y (2012) Measuring the output responses to fiscal policy. American Economic Journal: Economic Policy 4(2):1–27

Auerbach A, Gorodnichenko Y (2013) Fiscal Multipliers in Recession and Expansion. University of Chicago Press, Chicago

Baker S, Bloom N, Davis S (2016) Measuring economic policy uncertainty. Quarter J Econom 131(4):1593–1636

Barro RJ (2006) Rare disasters and asset markets in the twentieth century. Quarter J Econom 121(3):823–866

Batten S, Sowerbutts R, Tanaka M (2020) Climate change: Macroeconomic impact and implications for monetary policy. Ecological, Societal, and Technological Risks and the Financial Sector 13–38

Bloom N (2009) The impact of uncertainty shocks. Econometrica 77(3):623–685

Boivin J, Giannoni M (2006) Has monetary policy become more effective? Rev Econ Stat 88(3):445–462

Bouwer LM (2011) Have disaster losses increased due to anthropogenic climate change? Bull Am Meteorol Soc 92(1):39–46

Caggiano G, Castelnuovo E, Figueres J (2017) Economic policy uncertainty and unemployment in the United States: A nonlinear approach. Econom Lett 151:31–34

Caggiano G, Castelnuovo E, Groshenny N (2014) Uncertainty shocks and unemployment dynamics in US recessions. J Monet Econ 67:78–92

Cavallo A, Cavallo E, Rigobon R (2014) Prices and supply disruptions during natural disasters. Rev Income Wealth 60:S449–S471

Cavallo E, Galiani S, Noy I, Pantano J (2013) Catastrophic natural disasters and economic growth. Rev Econom Stat 95(5):1549–1561

Cavallo E, Noy I (2009) The economics of natural disasters: a survey. Inter-American Development Bank

Chen C. -C., McCarl B, Adams R (2001) Economic implications of potential ENSO frequency and strength shifts. Clim Chang 49(1):147–159

Colombo V (2013) Economic policy uncertainty in the US: Does it matter for the euro area? Econom Lett 121(1):39–42

Dell M, Jones B, Olken B (2014) What do we learn from the weather? the new climate-economy literature. J Econ Lit 52(3):740–98

Dietrich A, Müller G, Schoenle R (2021) The expectations channel of climate change. Implications for monetary policy

Estrada F, Botzen W, Tol R (2015) Economic losses from US hurricanes consistent with an influence from climate change. Nat Geosci 8(11):880–884

Fomby T, Ikeda Y, Loayza N (2013) The growth aftermath of natural disasters. J Appl Econom 28(3):412–434

FOMC (2005) Press release: September 20, 2005

Gabaix X (2011) Disasterization: a simple way to fix the asset pricing properties of macroeconomic models. Am Econ Rev 101(3):406–09

Gabaix X (2012) Variable rare disasters: an exactly solved framework for ten puzzles in macro-finance. Quarter J Econom 127(2):645–700

Gagnon E, López-Salido D (2020) Small price responses to large demand shocks. J Eur Econ Assoc 18(2):792–828

Gourio F (2012) Disaster risk and business cycles. Am Econ Rev 102(6):2734–66

Groth A, Dumas P, Ghil M, Hallegatte S (2011) Impacts of natural disasters on a dynamic economy. Extreme Events: Observations, Modeling and Economics. In: Chavez M, Ghil M, Urrutia-Fucugauchi J (eds) Geophysical Monograph, vol 214, pp 343–359

Hailemariam A, Smyth R, Zhang X (2019) Oil prices and economic policy uncertainty: Evidence from a nonparametric panel data model. Energy Economics 83:40–51

Hallegatte S, Ghil M (2008) Natural disasters impacting a macroeconomic model with endogenous dynamics. Ecol Econ 68(1-2):582–592

Handley K, Limao N (2015) Trade and investment under policy uncertainty: theory and firm evidence. American Economic Journal: Economic Policy 7(4):189–222

Heinen A, Khadan J, Strobl E (2019) The price impact of extreme weather in developing countries. Econ J 129(619):1327–1342

Hsiang S, Jina A (2014) The causal effect of environmental catastrophe on long-run economic growth: Evidence from 6,700 cyclones. Technical report, National Bureau of Economic Research

Isoré M., Szczerbowicz U (2017) Disaster risk and preference shifts in a New Keynesian model. J Econ Dyn Control 79:97–125

Jordà Ò (2005) Estimation and inference of impulse responses by local projections. Am Econ Rev 95(1):161–182

Kang W, Lee K, Ratti R (2014) Economic policy uncertainty and firm-level investment. J Macroecon 39:42–53

Kang W, Ratti R (2013a) Oil shocks, policy uncertainty and stock market return. Journal of International Financial Markets Institutions and Money 26:305–318

Kang W, Ratti R (2013b) Structural oil price shocks and policy uncertainty. Econ Model 35:314–319

Keen B, Pakko M (2011) Monetary policy and natural disasters in a DSGE model. South Econ J 77(4):973–990

Kilian L, Kim Y (2011) How reliable are local projection estimators of impulse responses? Rev Econom Stat 93(4):1460–1466

Klomp J (2020) Do natural disasters affect monetary policy? a quasi-experiment of earthquakes. J Macroecon 64:103164

Klomp J, Valckx K (2014) Natural disasters and economic growth: a meta-analysis. Glob Environ Chang 26:183–195

Koller M, Stahel W (2011) Sharpening Wald-type inference in robust regression for small samples. Comput Stat Data Anal 55(8):2504–2515

Loayza N, Olaberria E, Rigolini J, Christiaensen L (2012) Natural disasters and growth: Going beyond the averages. World Dev 40(7):1317–1336

Ludvigson S, Ma S, Ng S (2020) COVID19 and the macroeconomic effects of costly disasters. NBER Working Paper

Mochizuki J, Mechler R, Hochrainer-Stigler S, Keating A, Williges K (2014) Revisiting the disaster and development debate–toward a broader understanding of macroeconomic risk and resilience. Clim Risk Manag 3:39–54

NGFS (2021) Climate change and monetary policy: initial takeaways. network for greening the financial system

Noy I (2009) The macroeconomic consequences of disasters. J Dev Econ 88(2):221–231

Panwar V, Sen S (2019) Economic impact of natural disasters: an empirical re-examination. Margin J Appl Econom Res 13(1):109–139

Parker M (2018) The impact of disasters on inflation. Economics of Disasters and Climate Change 2(1):21–48

Raddatz C (2009) The wrath of God: macroeconomic costs of natural disasters. The World Bank

Ramey V, Zubairy S (2018) Government spending multipliers in good times and in bad: evidence from US historical data. J Polit Econ 126(2):850–901

Ravn M, Uhlig H (2002) On adjusting the hodrick-prescott filter for the frequency of observations. Rev Econom Stat 84(2):371–376

Rietz T (1988) The equity risk premium a solution. J Monet Econ 22(1):117–131

Rosenzweig C, Karoly D, Vicarelli M, Neofotis P, Wu Q, Casassa G, Menzel A, Root T, Estrella N, Seguin B (2008) Attributing physical and biological impacts to anthropogenic climate change. Nature 453(7193):353–357

Rosner B (1983) Percentage points for a generalized ESD many-outlier procedure. Technometrics 25(2):165–172

Rousseeuw P (1984) Least median of squares regression. J Am Stat Assoc 79(388):871–880

Skidmore M, Toya H (2002) Do natural disasters promote long-run growth? Econ Inq 40(4):664–687

Strobl E (2011) The economic growth impact of hurricanes: Evidence from US coastal counties. Rev Econom Stat 93(2):575–589

Timmermann A, Oberhuber J, Bacher A, Esch M, Latif M, Roeckner E (1999) Increased El niño frequency in a climate model forced by future greenhouse warming. Nature 398(6729):694–697

Van Aalst MK (2006) The impacts of climate change on the risk of natural disasters. Disasters 30(1):5–18

Yohai V (1987) High breakdown-point and high efficiency robust estimates for regression. The Annals of Statistics 642–656

You W, Guo Y, Zhu H, Tang Y (2017) Oil price shocks, economic policy uncertainty and industry stock returns in China: Asymmetric effects with quantile regression. Energy Economics 68:1–18

Zaman A, Rousseeuw P, Orhan M (2001) Econometric applications of high-breakdown robust regression techniques. Econom Lett 71(1):1–8

Author information

Authors and Affiliations

Corresponding author

Additional information

Availability of Data and Materialy

The data presented in this study are available on request from the corresponding author.

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

The author would like to thank the editor, Ilan Noy, and two anonymous referees for their thoughtful comments

Appendix

Appendix

A.1 Alternative Model 1

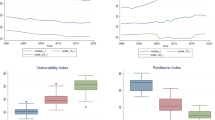

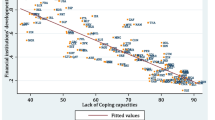

Disaster Shock Based on State-Dependence (Unemployment Rate). IRFs depict nonlinear responses from a disaster shock for periods of economic expansion (right panel) and periods of economic slack (left panel)

Transition Function Based on State-Dependence (Unemployment Rate). The figures shows the weighted regime (i.e., F(z)). Shaded areas indicate NBER recession dates

A.2 Alternative Model 2

Disaster Shock Based on State-Dependence (Output Growth). IRFs depicts nonlinear responses from a disaster shock for periods of economic expansion (left panel) and periods of economic slack (right panel)

Transition Function Based on State-Dependence (Output Growth). The figures shows the weighted regime (i.e., F(z)) based on the centered moving average of output growth. Shaded areas indicate NBER recession dates

A.3 Alternative Model 3

Disaster Shock Based on State-Dependence (Capital Utilization). IRFs depict nonlinear responses from a disaster shock for periods of economic expansion (right panel) and periods of economic slack (left panel)

Transition Function Based on State-Dependence (Capital Utilization). The figures shows the weighted regime (i.e., F(z)). Shaded areas indicate NBER recession dates

Rights and permissions

About this article

Cite this article

Ginn, W. Climate Disasters and the Macroeconomy: Does State-Dependence Matter? Evidence for the US. EconDisCliCha 6, 141–161 (2022). https://doi.org/10.1007/s41885-021-00102-6

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s41885-021-00102-6