Abstract

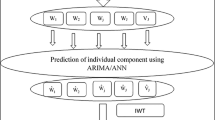

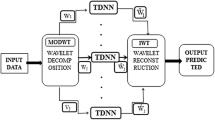

Forecasts of spot or future prices for agricultural commodities make it possible to anticipate the favorable or above all unfavorable development of future profits from the exploitation of agricultural farms or agri-food enterprises. Previous research has shown that cyclical behavior is a dominant feature of the time series of prices of certain agricultural commodities, which may be affected by a seasonal component. Wavelet analysis makes it possible to capture this cyclicity by decomposing a time series into its frequency and time domains. This paper proposes a time-frequency decomposition based approach to choose a seasonal auto-regressive aggregate (SARIMA) model for forecasting the monthly prices of certain agricultural futures prices. The originality of the proposed approach is due to the identification of the optimal combination of the wavelet transformation type, the wavelet function and the number of decomposition levels used in the multi-resolution approach (MRA), that significantly increase the accuracy of the forecast. Our SARIMA hybrid approach contributes to take into account the cyclicity and of the seasonality when predicting commodity prices. As a relevant result, our study allows an economic agent, according to his forecasting horizon, to choose according to the available data, a specific SARIMA process for forecasting.

Similar content being viewed by others

Notes

Yves Meyer is a Emeritus Professor at Superior Normal School of Cachan, Member of the Academic of Sciences since 1993. Specialist of harmonic analysis, he discovered the orthogonal wavelets.

\(L^2(R)\) is the set of square integrable functions: \(\int _{-\infty }^{+\infty } \left| f(t)\right| ^2dt < +\infty\) and a Hilbert’s space for the scalar product \(\left\langle f, \psi _{u,s} \right\rangle\).

The data time series are available on https://www.quandl.com.

symmetric distribution and a flattened like Gauss’s.

graphics of standardised residual, graphic of simple and partial autocorrelation function and graphic of Ljung-Box test.

References

Abry, P. 1997. Ondelettes et turbulences Nouveaux essais , arts et sciences, Diderot.

Box, G.E., and D. R. Cox. (1964). An Analysis of Transformations. Journal of the Royal Statistical Society. Series B(Methodological), 26: 211–252

Box, G.E., and G.M. Jenkins. (1976) Time series analysis forecasting and control. Rev.

Box, G.E., G.M. Jenkins, G.C. Reinsel, and G.M. Ljung. 2015. Time series analysis: Forecasting and control. London: John Wiley Sons.

Chao, S., and Y.C. He. 2015. SVM-ARIMA agricultural product price forecasting model based on wavelet decomposition. Statistics and Decision 13: 92–95.

Choudhary, K., G.K. Jha, R.R. Kumar, and D.C. Mishra. 2019. Agricultural commodity price analysis using ensemble empirical mode decomposition: A case study of daily potato price series. Indian Journal of Agricultural Sciences 89 (5): 882–886.

Cleveland, R.B., W.S. Cleveland, J.E. McRae, and I. Terpenning. 1990. STL: A seasonal trend decomposition procedure based on loss. Journal of Official Statistics 6 (1): 3–73.

Conejo, A.J., J. Contreras, R. Espínola, et al. (2005). Forecasting electricity prices for a day-ahead pool-based electric energy market. International journal of forecasting 21(3):435–462

Daubechies, I. 1992. Ten lectures on wavelets. SIAM.

Dickey, D.A.., W.A. Fuller. (1979). Distribution of the Estimators for Autoregressive Time Series with a Unit Root. Journal of the American Statistical Association 74: 427–431.

Gomez, V., and A. Maravall. (1998). Seasonal adjustment and signal extraction in economic time series. Documentos de trabajo / Banco de España 9809, 21-abr-1998, ISBN: 847793598X

Gencay, R., F. Selçuk, and B. Whitcher. 2001. An introduction to wavelets and other filtering methods in finance and economics. San Diego: Academic Press.

Gencay, R., F. Selçuk, and B. Whitcher. 2005. Multiscale systematic risk. Journal of International Money and Finance 24 (1): 55–70.

Ghysels, E. 1998. On stable factor structures in the pricing of risk: Do time-varying betas help or hurt? Journal of Finance 53 (2): 549–573.

Hannan, E.J., J. Rissanen. (1982). Recursive estimation of mixed autoregressive-moving average order. Biometrika 69(1):81–94

Hayat, A., and M.I. Bhatti. 2013. Masking of volatility by seasonal adjustment methods. Economic Modelling 33: 676–688. https://doi.org/10.1016/j.econmod.2013.05.016.

Hyndman, R. J., and Y. Khandakar. (2008). Automatic Time Series Forecasting: The forecast Package for R. Journal of Statistical Software 27(3):1–22

Hyndman, R., A. Koehler, K. Ord, et al. (2008). Forecasting with exponential smoothing: the state space approach. Springer Science & Business Media.

Jadhav, V., B.V.C. Reddy, and G.M. Gaddi. 2018. Application of ARIMA model for forecasting agricultural prices. Journal of Agriculture Science and Technology A 19 (5): 981–992.

Kwiatkowski, D., P. C. B. Phillips, P. Schmidt and Y. Shin. (1994). Testing the Null Hypothesis of Stationarity against the Alternative of a Unit Root. Journal of Econometrics. Vol. 54, pp. 159-178. 2. Hamilton, J. D. Time Series Analysis. Princeton, NJ: Princeton University Press.

Levhari, D., and H. Levy. 1977. The capital asset pricing model and the investment horizon. The Review of Economics and Statistics 59 (1): 92–104.

Li, B., J. Ding, Z. Yin, K. Li, X. Zhao, and L. Zhang. 2021. Optimized neural network combined model based on the induced ordered weighted averaging operator for vegetable price forecasting. Expert Systems with Applications 168: 114–232. https://doi.org/10.1016/j.eswa.2020.114232.

Liu, C.-Y. and Z.-Y. Zheng. (1989). Stabilization Coefficient of Random Variable. Biom. J. 31: 431–441.

Mallat, Stéphane. 1989. A theory for multiresolution signal decomposition: The wavelet representation. IEEE Transactions on Pattern Analysis and Machine Intelligence 11 (7): 674–693.

Melard, G., and J.M., Pasteels. (2000). Automatic ARIMA modeling including interventions, using time series expert software. International Journal of Forecasting 16(4): 497–508

Misiti, M., Y. Misiti, G. Oppenheim, and J. M. Poggi. (2003). Les ondelettes et leurs applications. Hermès science publications.

OCDE. (2008). Rapport annuel de l'OCDE 2008, Éditions OCDE, Paris. https://doi.org/10.1787/annrep-2008-fr

Osborn D.R., A.P.L. Chui, P.J.P. Smith, C.R. Birchenhall. (1988). Seasonality and the order of integration for consumption. Oxford Bulletin of Economics and Statistics 50(4): 361–77

Philips, P.C.B., P. Perron. (1987). Testing for a Unit Root in Time Series Regression. Biometrika 75:335–346.

Rivas, M. et al. (2013). Linking the energy system and ecosystem services in real landscapes. Biomass and Bioenergy 55:17–26

Sadefo Kamdem, J., A. Nsouadi, and M. Terraza. 2016. Time-frequency analysis of the relationship between EUA and CER carbon markets. Environmental Modeling and Assessment 21: 279–289.

Shumway, R.H., D.S. Stoffer. (2006). Time series regression and exploratory data analysis. Time Series Analysis and Its Applications: With R Examples 48–83

Unser, M. 1996. Wavelet in medecine and biology. London: CRC Press.

Vannucci, M., and F. Corradi. 1999. Covariance structure of wavelet coefficients: Theory and models in a Bayesian perspective. Journal of Royal Statistical Society B 4: 971–986.

Wang, J., Z. Wang, X. Li, and H. Zhou. 2019. Artificial bee colony-based combination approach to forecasting agricultural commodity prices. International Journal of Forecasting. https://doi.org/10.1016/j.ijforecast.2019.08.006.

Xiong, T., C. Li, and Y. Bao. 2018. Seasonal forecasting of agricultural commodity price using a hybrid STL and ELM method: Evidence from the vegetable market in China. Neurocomputing 275: 2831–2844. https://doi.org/10.1016/j.neucom.2017.11.053.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

See Figs. 11, 12, 13, 14, 15, 16, 17, 18, 19, 20.

Annual average data series

Monthly average indices prices

Residuals diagnostics by Seasonal Arima model for cereals data series

Residuals diagnostics by Seasonal Arima model for oleaginous data series

MRA on Soy times series

MRA on LogSoy times series

Wavelet Simple autocorrelation function - Wheat

Wavelet Partial autocorrelation function - Wheat

Wavelet Simple autocorrelation function - Soy

Wavelet Partial autocorrelation function - Soy

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Diop, MD., Sadefo Kamdem, J. Multiscale Agricultural Commodities Forecasting Using Wavelet-SARIMA Process. J. Quant. Econ. 21, 1–40 (2023). https://doi.org/10.1007/s40953-022-00329-4

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s40953-022-00329-4